Articles by deBanked Staff

CFPB Mends Mortgage Rules to Serve Small Creditors

March 22, 2016The Consumer Financial Protection Bureau (CFPB) broadened the Qualified Mortgage rule to certain special provisions for small creditors that operate in rural or underserved areas under the Helping Expand Lending Practices in Rural Communities (HELP) Act.

The Bureau’s mortgage rules which was brought into effect in January 2014 had a rule called ‘Ability-to-Repay’ which laid the onus of determining creditworthiness strictly on lenders.

As a result, the category of ‘Qualified Mortgages’ that emerged out of it kept certain risky features of the loan from borrowers who could not comply with the ability-to-repay rule. For instance, small creditors operating in rural areas were not allowed to originate balloon payments. Additionally, escrow accounts for higher-priced mortgage loans were not permitted.

The Bureau received flak for this from the House Financial Committee which alleged that the rule harmed consumer access and choice when it comes to home loans and mortgages by forcing many community banks and credit unions to downsize or shut down their mortgage operations.

The CFPB in its statement acknowledged that the “rule is being adopted to fit within the background of the CFPB’s prior regulations in the mortgage market.”

Financial Services Committee Chairman Jeb Hensarling in his critique against the rule said, “We are already hearing numerous feedback concerning the harmful impact on consumers of the Bureau’s Qualified Mortgage rule, which went into effect just days ago.”

Is this a way of making amends?

Why Marketplace Lenders Want to Share Borrowers

March 22, 2016 In a not-so-strange coming together, loandepot and Avant launched a borrower referral program.

In a not-so-strange coming together, loandepot and Avant launched a borrower referral program.

Loandepot and Avant are both marketplace lending platforms. Loandepot identifies itself as the ‘nonbank consumer lender’ and sells home equity loans, refinances mortgages and credit card loans and added personal loans in May 2015. Avant mostly sells personal loans and as of very recently, consumer auto loans.

Under the mutual borrower program, the two companies will have access to each other’s customer base to “expand credit options to responsible borrowers.”

California-based Loandepot has to date funded $60 billion in loans since 2010, $400 million of which was in personal loans. Chicago-based Avant has funded $3 billion in personal loans since 2012.

Industry analyst Michael Tarkan at Compass Point Research called the partnership a turndown program from Loandepot to Avant. “Referrals are an easy channel to facilitate loan volume,” he said.

There have been other partnerships in the industry with either banks or other lenders. JPMorgan and OnDeck, OnDeck and Prosper being noteworthy ones.

Tarkan expected more such collaborations before the industry consolidates itself. Marketplaces look for new borrowers to reach in different ways. “Goal for the platforms is to build a brand and a relationship with the customer so there is a repeat loan purchase,” Tarkan said. “There will be some degree of consolidation simply because there are many platforms out there searching for the similar borrower and industry won’t be able to support so many platforms.”

Avant Will Refinance Auto Loans

March 21, 2016 Online lending platform Avant said it will refinance consumer auto loans.

Online lending platform Avant said it will refinance consumer auto loans.

The Chicago-based marketplace platform, Avant added auto-secured loans earlier. This refinancing option is available to borrowers in California with Illinois and Georgia to follow in the coming months.

According to the company website, Avant’s auto refinance loans range between $4,000 and $35,000 with APRs between 10.11 percent and 25 percent ranging over 2-5 years.

“Today’s middle-income consumers have to often settle for auto loans with high interest rates and poor lending experiences,” said Al Goldstein, CEO of Avant. “We want to be the one stop shop for the borrowing needs of consumers across the credit spectrum,” he said in a statement.

Earlier this month, the company crossed $3 billion in personal loans. Avant uses big data and machine learning to underwrite loans.

This move however comes at a time when subprime auto delinquencies are higher now than they were during the height of the most recent recession. The 60-day-plus delinquency rate of the subprime loan group reached 5.16% last month, compared to 5.09 percent in January, 2009. Credit ratings agency Fitch attributes this surge to increased competition among lenders resulting in weaker underwriting standards and more originations.

Are Subprime Auto Loans Showing Cracks or Not?

March 19, 2016 Subprime auto delinquencies are even higher now than they were during the height of the most recent recession, according to Fitch Ratings. The 60-day-plus delinquency rate of the subprime loan group that Fitch evaluates reached 5.16% last month, compared to 5.09% in January, 2009.

Subprime auto delinquencies are even higher now than they were during the height of the most recent recession, according to Fitch Ratings. The 60-day-plus delinquency rate of the subprime loan group that Fitch evaluates reached 5.16% last month, compared to 5.09% in January, 2009.

Fitch attributed this to weaker underwriting standards as well as sharp origination growth and increased competition.

The prime sector is mostly stable, they say. Further weakness is anticipated across all credit categories, though the outlook is stable.

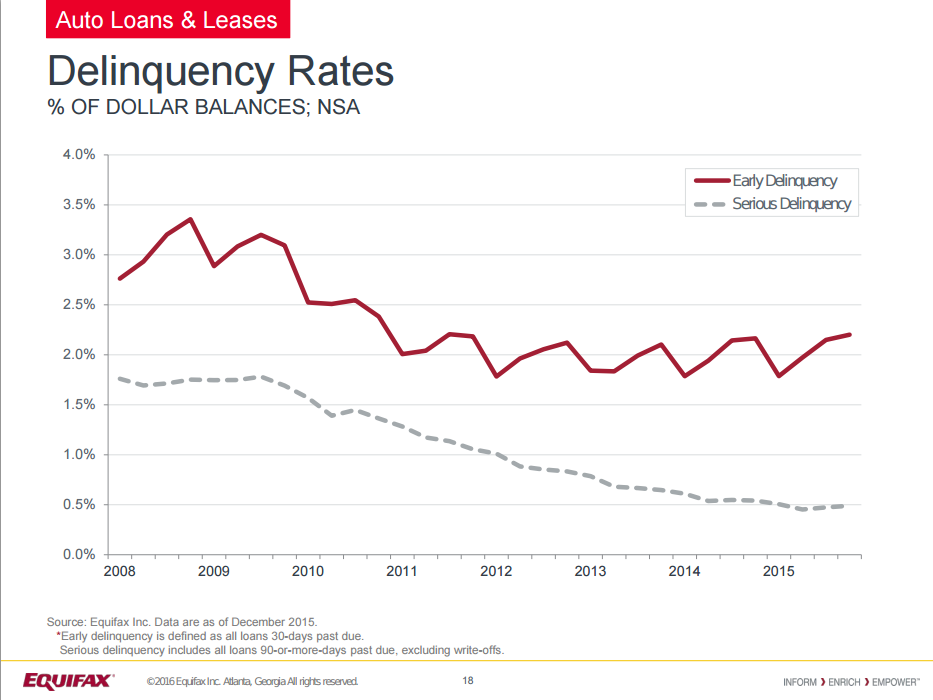

But while Fitch spoke of weaker underwriting and nearly unprecedented delinquencies, consumer credit reporting agency Equifax spun a different picture just four days later when they announced the results of their own auto lending study.

“Lenders are making more informed lending decisions and the underwriting process has been strengthened as a result of new data and technology that is available to the marketplace,” said Amy Crews Cutts, chief economist at Equifax.

Indeed, the rates of both early delinquency and serious delinquency as a percentage of dollar balances are nowhere near recession levels, at least according to Equifax’s data set.

Both Fitch and Equifax agree there has been an increase in auto loan originations.

In a WSJ interview, hedge fund manager Ben Weinger said that demand for auto debt has led lenders to systematically loosen underwriting standards.

Equifax’s Cutts recently said however that “credit performance is still excellent, showing that lenders are prudently extending credit to well-underwritten borrowers.”

Who’s right?

Minority Small Business Owners Have More Income but Less Credit?

March 18, 2016 A third of minority small businesses are run by women and nearly 45 percent of all minority-owned businesses are from California, Florida and Texas.

A third of minority small businesses are run by women and nearly 45 percent of all minority-owned businesses are from California, Florida and Texas.

And most of them run restaurants and beauty services and their average credit score is nearly five points lower than the average for the general small-business population, even though they earn higher and are heel-to-heel in credit card delinquencies. 1.2 percent of minority small-business owners have at least one business credit card account that is severely delinquent (91-plus days) compared to 1.1 percent of the general small-business owner population. And the average consumer income for minority business owners is $92,489, more than the average income of the general small business owner of $92,338.

Credit-reporting company Experian in its new study on small businesses, however said that minority small business owners fall behind on managing credit — 15 points lower than the overall average for small-business owners, to be precise. The report does not explain why.

But “Gaining insight into the trends and behaviors of the small-business community is imperative given its importance to the growth and success of our overall economy,” said Pete Bolin, director of consulting and analytics for Experian, which also released tools and resources on credit management.

The market of lending to minority small business owners is well recognized. Apart from the SBA micro loans and community advantage loans that seek to bridge the gaps, the ‘Equal Credit Opportunity Act’ prevents lenders from discriminating against borrowers based on race and sex.

Bizfi Partners With West Coast Banking Group

March 17, 2016Bizfi will be the exclusive alternative finance solutions provider for small businesses that are members of the Western Independent Bankers, a trade association of community banks in the west coast.

Small businesses in the midwest and west coast in states including Alaska, Arizona, California, Colorado, Hawaii, Idaho, Montana, Nevada New Mexico, Oregon, Utah, Washington and Wyoming can benefit from this partnership. Bizfi’s marketplace partners with lenders like OnDeck, Funding Circle and Kabbage.

“WIB member banks are the leading funders of America’s small businesses,” said Michael Delucchi, President and Chief Executive Officer of WIB and WIB Service Corporation. “With Bizfi as a WIB Premier Solutions Provider we are able to offer their expertise in alternative financing and superior technology to our member banks and deliver a complete solution for small business funding.”

Earlier this month, Bizfi partnered with The New York State Restaurant Association to provide business financing for its 2,000 small businesses in the restaurant space.

Funding Circle To Expand Bay Area Staff

March 17, 2016 P2P Lender Funding Circle will expand its Bay Area staff by ten percent.

P2P Lender Funding Circle will expand its Bay Area staff by ten percent.

The company plans to hire 20 people in risk and compliance, product engineering and sales teams. Funding Circle’s marketplace connects borrowers, mostly small business merchants and investors. The company makes money in origination and servicing fees.

The San Francisco-based company was founded in 2010 in the United Kingdom and was launched in the US in 2013. It employs 550 people globally and has so far funded $2 billion to 15,000 businesses.

Earlier this month, Funding Circle announced that it hired former Executive Board Member of the European Central Bank (ECB), Jörg Asmussen, to join its board. This aligns with the company’s streak of boosting manpower. Last year, it hired top executives from Barclays and American Express to head its global risk and analytics team.

OnDeck, UK Trade Group Work on Fintech Policy

March 17, 2016 Don’t look now but OnDeck is getting knee-deep in fintech policy.

Don’t look now but OnDeck is getting knee-deep in fintech policy.

The online lender said that it will partner with UK’s Innovate Finance, a fintech trade group to launch a Transatlantic Policy Working Group to exchange intelligence and information on regulatory and policy issues governing fintech.

The group will work on universal fintech issues like the use of data, building a payments infrastructure for financial inclusion, open source APIs in banking and automated investment advice through robo advisors, when kicking off its first meeting at Google’s Washington DC office.

“The transatlantic policy working group represents a great opportunity to share key insights, best practices and knowledge between US and UK fintech stakeholders,” said Daniel Morgan, head of policy and regulation at Innovate Finance “It will help drive real change in the public policy arena when it comes to the development and growth of a vibrant fintech sector.”

Venture capital investment in fintech companies more than doubled last year compared to 2014, hitting an all time high of $14 billion, up 106 percent from $7 billion in 2014. The UK attracted a total of $623 million in fintech investment in 2014 and Innovate Finance committed to increasing that number to $8 billion by 2020 in venture and institutional investment.