Related Headlines

| 01/20/2020 | Scott Tucker to be on American Greed |

| 09/28/2018 | Scott Tucker victims to get $505M |

| 01/05/2018 | Scott Tucker sentenced to 16 years |

| 03/13/2017 | Payday kingpin Scott Tucker trial delayed |

Related Videos

FTC SCOTUS Ruling Summarized |

Stories

Payday Loan Convict Scott Tucker to be Featured in Netflix Docuseries

January 14, 2018Payday loan mastermind Scott Tucker, who was recently sentenced to 16 years in prison, will be featured in Dirty Money, a Netflix docuseries focused on tales of greed.

Tucker was among the most prolific payday lenders in the United States, using Native American tribes to shield himself from state laws while generating billions of dollars in revenue. Prior to his conviction on charges of participating in a racketeering enterprise through the collection of unlawful debt, wire fraud, money laundering, and violations of the Truth In Lending Act, he garnered the largest FTC judgment in history, a staggering $1.3 billion.

Tucker was among the most prolific payday lenders in the United States, using Native American tribes to shield himself from state laws while generating billions of dollars in revenue. Prior to his conviction on charges of participating in a racketeering enterprise through the collection of unlawful debt, wire fraud, money laundering, and violations of the Truth In Lending Act, he garnered the largest FTC judgment in history, a staggering $1.3 billion.

Tucker’s penchant for racing fancy cars that includes a professional career with some notable victories likely secured his place in the annals of financial villains.

The docuseries begins on January 26th.

Payday Lending King Scott Tucker Convicted

October 14, 2017 One year after a federal judge awarded a record-setting $1.3 billion judgment to the FTC against Scott Tucker for damages caused by his payday lending empire, a jury in the Southern District of New York found him guilty on criminal charges that include participating in a racketeering enterprise through the collection of unlawful debt, wire fraud, money laundering, and violations of the Truth In Lending Act.

One year after a federal judge awarded a record-setting $1.3 billion judgment to the FTC against Scott Tucker for damages caused by his payday lending empire, a jury in the Southern District of New York found him guilty on criminal charges that include participating in a racketeering enterprise through the collection of unlawful debt, wire fraud, money laundering, and violations of the Truth In Lending Act.

Tucker and another defendant, who happened to be his attorney in the scheme, are set to be sentenced on January 5th. He will remain on house arrest until then. Tucker is facing more than 20 years in prison. He is 55.

Among the luxuries Tucker spent his ill-gotten gains on were his professional racing hobby. His auto racing team, Level 5 Motorsports, participated in international tournaments and won 4 championships. The feds auctioned off his race cars that included two Ferraris and a Porsche earlier this year.

According to the DOJ:

TUCKER devised a scheme to claim that his lending businesses were protected by sovereign immunity, a legal doctrine that, among other things, generally prevents states from enforcing their laws against Native American tribes. Beginning in 2003, TUCKER entered into agreements with several Native American tribes (the “Tribes”), including the Santee Sioux Tribe of Nebraska, the Miami Tribe of Oklahoma, and the Modoc Tribe of Oklahoma. The purpose of these agreements was to cause the Tribes to claim they owned and operated parts of TUCKER’s payday lending enterprise, so that when states sought to enforce laws prohibiting TUCKER’s loans, TUCKER’s lending businesses would claim to be protected by sovereign immunity.

At trial, the jury wasn’t fooled. Read the full DOJ report here.

Payday Loan King Scott Tucker Loses FTC Fight: Must Pay $1.3 Billion

October 2, 2016

Deceptive payday lending has come at a steep price for one Scott Tucker, who was briefly an accomplished professional race car driver. On Friday, September 30th, United States District Judge Gloria M. Navarro ordered a judgment be entered in favor of the FTC in the amount of $1,301,897,652. That concludes a case that had carried on for four years.

The $1.3 Billion judgment is no doubt a bad omen for Tucker as he awaits his criminal trial in New York. He was arrested earlier this year in February and charged with multiple counts of conspiracy, collection of unlawful debts and false TILA disclosures. In that case, US Attorney Preet Bharara seeks a forfeiture of at least $2 Billion. An initial accounting of his assets subject to forfeiture are his ferraris, porsches, a private jet, homes and more than a dozen bank accounts, according to the indictment.

That should be a big blow to Tucker considering that an asset freeze has forced him to rely on court-appointed attorneys in the criminal case. However, the FTC alleged last month that Tucker was still managing to live a lavish lifestyle that included steakhouses, country clubs, and spa visits. Documents filed in the FTC case show that as recent as July 22nd, the court was still ordering newly discovered bank accounts related to Tucker to be frozen. Given the billions sought in damages, one local newspaper in Kansas City, named The Pitch, questioned back in May where all of the money went.

That should be a big blow to Tucker considering that an asset freeze has forced him to rely on court-appointed attorneys in the criminal case. However, the FTC alleged last month that Tucker was still managing to live a lavish lifestyle that included steakhouses, country clubs, and spa visits. Documents filed in the FTC case show that as recent as July 22nd, the court was still ordering newly discovered bank accounts related to Tucker to be frozen. Given the billions sought in damages, one local newspaper in Kansas City, named The Pitch, questioned back in May where all of the money went.

We may soon find out. The judge’s order in the FTC case not only banned Tucker and his co-defendants from participating in consumer lending for life but also ordered that he must identify all business activities for which he performs services whether as an employee or otherwise and any entity in which he has an ownership interest in. The FTC was also awarded the authorization to obtain additional discovery without court consent and the permission to pose as a consumer, supplier, or other individual or entity to the defendants or any individual or entity affiliated with the defendants without the necessity of identification or prior notice.

The judgment was entered in case number 2:12-cv-00536.

United States Supreme Court Defangs FTC in Explosive Decision

April 22, 2021 The United States Supreme Court issued an explosive decision in AMG Capital Management, LLC et al v Federal Trade Commission, invalidating the Commission’s attempt and assumed power to pursue equitable monetary relief such as restitution or disgorgement under 13(b).

The United States Supreme Court issued an explosive decision in AMG Capital Management, LLC et al v Federal Trade Commission, invalidating the Commission’s attempt and assumed power to pursue equitable monetary relief such as restitution or disgorgement under 13(b).

Held: Section 13(b) does not authorize the Commission to seek, or a court to award, equitable monetary relief such as restitution or disgorgement. Pp. 3–15.

The immediate result is that the FTC’s largest judgment in history ($1.3 billion) against the companies belonging to payday lending kingpin Scott Tucker, has been undone.

The larger implication is that all of the FTC’s pending lawsuits seeking such relief against defendants under 13(b) are in mortal peril.

“Nothing we say today, however, prohibits the Commission from using its authority under §5 and §19 to obtain restitution on behalf of consumers,” the Court said. “If the Commission believes that authority too cumbersome or otherwise inadequate, it is, of course, free to ask Congress to grant it further remedial authority.”

Over the past five years alone, the FTC has refunded $11.2B to consumers through awards granted under 13(b).

Scott Tucker is currently in prison serving time for charges related to the FTC lawsuit. He was the subject in a Netflix Series called “Dirty Money” in 2018.

This story will be updated…

The FTC’s Power to “Wipe Out” is Under Siege

October 9, 2020 As the FTC contemplates how to “wipe out” entire industries, federal courts around the country have recently ruled that the regulator can’t accomplish such a goal under Section 13(b) of the FTC act. That’s the statute the FTC relied on to bring its most recent actions against merchant cash advance companies. It might not have bite.

As the FTC contemplates how to “wipe out” entire industries, federal courts around the country have recently ruled that the regulator can’t accomplish such a goal under Section 13(b) of the FTC act. That’s the statute the FTC relied on to bring its most recent actions against merchant cash advance companies. It might not have bite.

Under 13(b), the FTC is empowered to bring a lawsuit to obtain an injunction against unlawful activity that is currently occurring or is about to occur. It’s powerful, but very limited. However, for the last several decades, the FTC, with the help of federal courts, has interpreted the statute to mean that it can also force the defendants to “disgorge” with illegally obtained funds.

That’s how the FTC wiped out Scott Tucker and his payday lending empire. In a lawsuit the FTC brought against his companies under 13(b) in 2012, the Court entered a judgment of $1.3 billion against him.

Not so fast, modern legal analysis says. Tucker’s case is being brought before the Supreme Court of the United States to settle once and for all what 13(b) allows for and what it doesn’t.

The momentum does not weigh in the FTC’s favor.

On September 30, the Third Circuit ruled in FTC v AbbVie that the FTC is not entitled to seek disgorgement under 13(b). The Seventh Circuit arrived at a similar conclusion last year in FTC v Credit Bureau Center.

In an interview with NBC, FTC Commissioner Rohit Chopra said in August “We’ve started suing some [merchant cash advance companies] and I’m looking for a systemic solution that makes sure they can all be wiped out before they do more damage.”

As the FTC attempts to be more proactive in the area of small business finance, it will be important to monitor what the Supreme Court ultimately decides it can actually accomplish.

Updates On Several Industry Court Cases

October 4, 2017Curious to know the status of industry court cases we’ve reported on? Here’s an update on several:

| Case | When filed | Where pending | Status |

| Yellowstone Capital LLC and EBF Partners, LLC v. Corporate Bailout, LLC, Mark D. Guidubaldi & Associates, LLC dba Protection Legal Group, PLG Servicing, LLC, American Funding Group, Coast to Coast Funding, LLC, ROC Funding Group, LLC, ROC South LLC, and Mark Mancino. | 9/27/17 | New York State Supreme Court | Complaint filed. No anwswer filed yet |

| Sean Pullen, Christina Cane, Michael Cane, Michael Carrera, Matthew Taylor, and Yulia Zamaora v Social Finance, Inc. and Does 1-50 | 8/14/17 | Superior Court of California | SoFi filed an answer to the complaint on 9/15 |

| Craig Cunningham v. Mark D. Guidubaldi & Associates, LLC dba Protection Legal Group, and Corporate Bailout, LLC, Sanford J. Feder Esq, Mark D. Guidubaldi, Esq, Cashflow Care, LLC | 5/10/17 | Northern District of Texas | Motion for default judgment filed against Corporate Bailout on 9/12/17. Defendant never responded |

| Natures Market Corp v. Creditors Relief | 4/28/17 | New York State Supreme Court | Creditors Relief’s motion to dismiss and sanctions are still pending |

| Pearl Gamma Funding, LLC and Pearl Beta Funding, LLC v. Creditors Relief, LLC | 11/16/16 | New York State Supreme Court | Pearl has moved to dismiss Creditors Relief’s counterclaims |

| United States v. Sergiy Bezrukov | 10/26/16 | Western District of New York | The criminal indictment was amended on 8/3/17 to add more charges. Bezrukov is facing up to 30 years in prison |

| Ronald Bethune, on behalf of himself and all others similarly situated v. Lendingclub Corporation;WebBank, Steel Partners Holdings, L.P.; The Lending Club Members Trust; and does 1 through 10, inclusive | 4/6/16 | Southern District of New York | The judge granted the defendants motion to compel arbitration on Jan 30, 2017 |

| Kalamata Capital LLC v. Biz2Credit, Inc. and Itria Ventures, LLC | 12/8/14 | New York State Supreme Court | Kalamata plans to amend the complaint and the Court is scheduled to decide on the debate over whether certain documents should be sealed from public view |

| Federal Trade Commission v. AMG Services, Inc., et al. | 4/2/12 | District of Nevada | $1.3 billion judgment entered. Company owner Scott Tucker is also currently being tried criminally in the Southern District of New York for ill-gotten profits related to his payday lending empire. The jury is expected to decide the outcome this month |

A Q4 To Remember – A Timeline

December 18, 2016In case you haven’t noticed, it’s been an interesting few months for alternative finance. The below timeline is an expanded version of what appears in the print version of our Nov/Dec magazine issue.

9/27 Able Lending secured $100 million in debt financing

9/30 The FTC won a judgement of $1.3 billion against payday loan kingpin Scott Tucker, its largest ever award through litigation

10/11 The United States Court of Appeals for The District of Columbia ruled the CFPB’s organizational structure unconstitutional. To remedy, the agency will either have to convert its one-person directorship to a multi-member commission or the director will have to report to the President of the United States. The CFPB is appealing the decision.

10/13 Affirm secured $100 million in debt financing

10/14

- CircleBack Lending was reported to have ceased lending operations

- Goldman Sachs unveiled its new online consumer lending division, Marcus

10/20 CommonBond secured a $168 million securitization deal

10/24 Bizfi announced that John Donovan had joined the company as CEO. Donovan was the COO of Lending Club from 2007 to 2012.

10/25

- Expansion Capital Group announced new management team. Vincent Ney, the company’s majority shareholder became the CEO

- Lendio raised $20 million through a new equity round led by Comcast Ventures and Stereo Capital

- Lending Club announced its foray into the $1 trillion auto refinancing market

11/1

- Cross River Bank raised $28 million in equity led by Boston-based investment firm Battery Ventures along with Silicon Valley venture capital firms Andreessen Horowitz and Ribbit Capital

- Square beat earnings estimates and extended $208 million through 35,000 loans in Q3

11/3

- OnDeck announced earnings, continued use of balance sheet to fund loans and extended $613 million in Q3

- Independent merchant cash advance training course goes live, allowing brokers and underwriters to earn a certificate

11/4 SEC concluded its investigation into Lending Club

11/7 Lending Club announced earnings and a deal to sell $1.3 billion worth of loans to a National Bank of Canada subsidiary

11/8 CFG Merchant Solutions secured a $4 million revolving line of credit

11/9 Donald Trump became the President-Elect

11/11

- Fintech leader Peter Thiel joins the executive committee of Trump’s transition team

- Kabbage appointed Amala Duggirala as Chief Technology Officer and Rama Rao as Chief Data Officer

11/14 Prosper’s CEO Aaron Vermut, stepped down

11/16

- UK-based p2p lender Zopa applied for a banking license

- Small business lender Dealstruck reportedly ceases lending operations

- Former Lending Club CEO revealed to be launching a new rival, Credify

11/17

- LiftForward secured a $100 million credit facility

- Prosper filed their Q3 10-Q, revealing that they only originated $311.8 million in loans for the quarter compared to $445 million in Q2

- The IRS sent a broad request to Coinbase, the nation’s largest bitcoin exchange, as part of a hunt for tax evaders

- PeerStreet raised a $15 million Series A funding round led by Andreessen Horowitz

11/18 P2Bi raised $7.7 million in venture financing

11/22 LendIt announced the first ever industry awards event

11/29 Three C-level executives at CAN Capital are placed on a leave of absence after the company identified assets that were not performing as expected

12/2

- Total Merchant Resources secures $20 million in private equity, launches wholesale funding division

- Bitcoin-based P2P lending platform BitLendingClub shuts down

- OCC announces they are moving forward with a special purpose national charter for fintech companies

12/8 Former CEO and co-founder of World Wrestling Entertainment tapped to run Small Business Administration

12/9 OnDeck announced new $200 million revolving credit facility with Credit Suisse

12/12 Knight Capital Funding announced new Chief Data Scientist

12/13 Fifth Third Bank is reported to buy a stake in franchise marketplace lender ApplePie Capital

12/14 BlueVine raised $49 million in Series D funding

12/15

- Swift Capital named Tim Naughton as Chief Legal Officer

- John MacIlwaine, Lending Club’s Chief Technology officer, submitted his resignation to the company to pursue another opportunity

12/16 CAN Capital is reported to have laid off more than 100 employees

Text The Merchant, Close The Deal

April 15, 2017

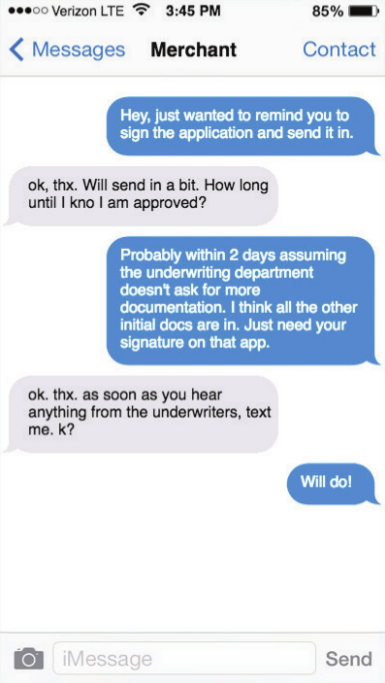

About a year ago, Cheryl Tibbs, general manager of Douglasville, Ga.-based One Stop Funding, was having trouble getting in touch with one of her clients. The merchant in question runs a lawn care service and is usually out on the job, so he isn’t quick to return phone calls or respond to email messages.

“I just got the idea to send a text,” Tibbs recalls. She typed a message expressing her regret for intruding but letting her client know that he needed to take certain steps to advance the funding process for his loan application. He texted right back.

After that initial success, the texting continued between Tibbs and the lawn care provider. He’s been a customer for us for a while, and that’s just how we communicate,” she says. “It’s easy for him to stop and shoot me a text as opposed to having a full conversation with me.”

Tibbs isn’t alone in her appreciation for text messaging as a part of the sales process. Quick responses to texts are making the medium increasingly important in the alternative small-business funding business, maintains Gil Zapata, CEO of Miami-based Lendinero. “Text messaging is more powerful than emailing nowadays,” he declares.

One reason for that shift is that texts are easy to use, according to Tibbs. “It’s a matter of convenience for the merchant,” she contends. “In this business, any way you can make it easier for the merchant to facilitate the transaction with you is the method you have to use.”

Besides the convenience, there’s the sense of urgency people feel when they receive a text, asserts Jeb Blount, a sales trainer who’s written eight sales-oriented books, including the bestselling Fanatical Prospecting. “When you send a text message you move to the top of a person’s priority list,” he says. In fact, people who are talking face-to-face often disengage from the conversation to respond to a text message, he notes. “It’s treated as something that’s urgent.”

As texting becomes more commonplace in the alternative-finance business, some industry salespeople are beginning to view the medium in the same way they regard email, telephones and fax machines. “I use them as another tool for follow-up communications,” John Tucker, managing member of 1st Capital Loans in Troy, Mich., says of text messages. “In addition to sending them an email, I’ll shoot them a text.”

As texting becomes more commonplace in the alternative-finance business, some industry salespeople are beginning to view the medium in the same way they regard email, telephones and fax machines. “I use them as another tool for follow-up communications,” John Tucker, managing member of 1st Capital Loans in Troy, Mich., says of text messages. “In addition to sending them an email, I’ll shoot them a text.”

Texting has become almost standard procedure at Florida-based Financial Advantage Group LLC, according to Scott Williams, the firm’s managing member. He prefers that sales associates make the initial contact by phone to get a sense of what the merchant is looking for in a funding deal. After gathering information and getting approval, it’s best to send the offer by email so the merchant has “all the numbers in black and white” and more details than a text message can hold, he notes. After that, text messages can deliver requests for additional documentation and provide updates on the progress of the funding process. “We can tell them, ‘Hey, everything got cleared this morning – we should be able to do the funding this afternoon,’” he says.

Texting expedites communication regarding renewals, too, Williams observes. “If a merchant is 50 percent paid back, you can check in and see if they need some additional capital right now,” he says. “It’s really good for that.”

Clients can use messaging to convey images of documents needed in the funding process, Tibbs says. “I had a merchant yesterday who sent me over her IRS tax agreement through picture message,” Tibbs says by way of example. Often, funders request color images of both sides of an applicant’s driver’s license, she notes. To fulfill such requirements, it’s generally easier to snap a photo with a phone and send it as a picture message than to scan pages of paper into a computer to create an electronic document and then send the resulting file by email. “We do a lot with picture messaging,” she observes.

But as useful as text messaging can become for contacting phone-shy clients or helping clients share an image to document a key cancelled check, companies should exercise care when using the medium for prospecting, warns Zapata. He and just about everyone else deBanked consulted emphasizes that sending unsolicited text messages can violate Federal Trade Commission regulations. “Just because our industry isn’t regulated doesn’t mean there aren’t regulations out there on the side,” he says.

Most say they learned of the regulations from third-party vendors who specialize in sending batches of text messages simultaneously. The key to sending those groups of messages legally is to get permission from the recipients in advance, notes Ted Guggenheim, CEO of TextUs, a Boulder, Colo., company specializing in multiple-texting services. “If you’re (randomly) contacting people you got off a list somewhere, that’s a pretty bad idea,” he maintains.

Most say they learned of the regulations from third-party vendors who specialize in sending batches of text messages simultaneously. The key to sending those groups of messages legally is to get permission from the recipients in advance, notes Ted Guggenheim, CEO of TextUs, a Boulder, Colo., company specializing in multiple-texting services. “If you’re (randomly) contacting people you got off a list somewhere, that’s a pretty bad idea,” he maintains.

The feds heavily regulate five-digit short-code texts but tread lightly with long-code texts – the ones sent from 10-digit phone numbers, Guggenheim says. The latter would apply in alternative finance, and if a text recipient calls back on the phone number associated with a long-code text, someone will answer, he notes.

Citing guidelines from the Cellular Telecommunications Industry Association (CTIA), Guggenheim stipulates that consumers should have the ability to opt out of additional messages after receiving the first one. Members of the industry who want to send groups of text messages can post conditions on their websites that compel users to grant permission to contact them by text if they submit their contact information, he suggests.

After ensuring everything’s legal, Tucker reports 1st Capital Loans nets a good response when he uses a vendor to blast multiple identical text messages to lists of prospective clients who have already granted permission for his company to contact them by text message. The strategy has helped bring in a reasonable number of deals because the prospects were “already in the pipeline,” he notes.

Remember, though, that cell phone numbers change more often than land line numbers, Tucker cautions. That means a call to a number that’s been reassigned could inadvertently fall into the unsolicited text message category that violates federal rules, he says. “You could be texting a 14-year-old,” instead of a small business, he warns.

When mounting a mass text campaign, marketers are wise to avoid lengthy missives, according to Tibbs. “Keep it simple,” she says. A typical message from her might read: “Looking for funding? Looking for capital? Give us a call,” she notes.

In business texts, avoid acronyms like “LOL” and write in complete sentences with proper punctuation and capitalization, Blount suggests. “Begin by typing out the message somewhere other than in the text box, read it, make sure it makes sense and then send it,” he says. Put your name with the word “from” at the top of the message so the recipient knows who sent it, he emphasizes.

Keep messages conceptual rather than marketing-oriented, Guggenheim advises. Messages should directly address the customer’s situation to avoid seeming they were sent by a robot, he says. As with any response a salesperson receives, getting back to customers quickly pays off in better results, he adds. When sending a batch of texts, vendors of the bulk service can ensure every text bears the same phone number that the sales rep uses to call the client, thus avoiding the possible confusion of using more than one number, says Guggenheim. The system he offers can trigger a pop-up on the computer screen of a specified salesperson when a text recipient responds, he says. It also keeps management informed of the volume of texts and the response rate, he says. That helps managers determine which types of text messages are working, he maintains.

Keep messages conceptual rather than marketing-oriented, Guggenheim advises. Messages should directly address the customer’s situation to avoid seeming they were sent by a robot, he says. As with any response a salesperson receives, getting back to customers quickly pays off in better results, he adds. When sending a batch of texts, vendors of the bulk service can ensure every text bears the same phone number that the sales rep uses to call the client, thus avoiding the possible confusion of using more than one number, says Guggenheim. The system he offers can trigger a pop-up on the computer screen of a specified salesperson when a text recipient responds, he says. It also keeps management informed of the volume of texts and the response rate, he says. That helps managers determine which types of text messages are working, he maintains.

Users can also rely on Guggenheim’s TextUs system to schedule messages for delivery in the future to remind clients of meetings. The system detects land-line numbers and informs the user that the phone will not receive text messages, and it integrates with customer-relationship management systems to exchange information, he says.

So used properly, texting can offer benefits for everyone involved. But some unscrupulous players still insist upon using the medium to mislead prospective clients, says Zapata. His customers have shown him texts from competitors who make initial contact or early contact by sending text messages that might look like offers but are really just marketing letters, says Zapata. That approach, which might tout the availability of $50,000, can cause problems when it turns out that the merchant qualifies for only $25,000, he explains. “Trust me, you’re not going to look like the good guy,” he says of the firms that send what he considers objectionable text messages.

Sensitivity comes into play with text messaging, according to Blount. He and other sources say a great number of people regard email as business-oriented and texts as personal. That leads them to nonchalantly delete unwanted email messages but to become angry when they receive a text they didn’t want, he says. “You can’t send text messages to customers if they don’t know you,” he counsels.

Once a relationship is established, however, text messages can nurture it, Blount maintains. Suppose two businesspeople meet at a networking event and exchange business cards, he says. He advises noting the cell number on the card and sending a LinkedIn invitation immediately after meeting the potential client. Twelve hours later he would send a text message mentioning the encounter. If the salesperson can get the potential client to respond to a text message, that prospect is granting permission to receive texts, he says.

Once a relationship is established, however, text messages can nurture it, Blount maintains. Suppose two businesspeople meet at a networking event and exchange business cards, he says. He advises noting the cell number on the card and sending a LinkedIn invitation immediately after meeting the potential client. Twelve hours later he would send a text message mentioning the encounter. If the salesperson can get the potential client to respond to a text message, that prospect is granting permission to receive texts, he says.

Blount’s example seems to suggest the line between business and personal may be blurring when it comes to texting. People often check their email messages on phones these days – instead of on a laptop or desktop computer – which also minimizes the difference between texting and emailing, says Tibbs. “Everybody does everything with their phone these days,” she notes.

Communicating through a more personal channel such as texting has advantages, too, Williams contends. That’s because some merchants consider their financing to be personal and don’t want to broadcast the details to employees, he says. To protect their privacy, merchants often provide financial institutions with their cell phone number instead of their office number or toll-free line, he notes.

Meanwhile, the world continues to become more comfortable with texting. When Williams and his sales associates began messaging clients about four years ago, they found younger customers receptive and older ones reluctant, he remembers. In the intervening years, however, the 50 plus crowd has warmed to the medium, he observes.

An advantage that accrues with text messaging – compared with email – arises from the fact that spam filters and spam folders don’t seem to have a place in the world of texting. Several sources cite that as a big advantage with using texts. “If you send someone a text message, they’re going to see it,” notes Zapata.

Asked about a downside to the proper use of text messaging in business, most sources could not name one. However, Williams has discovered one area where the mode of communication comes up short. “I would not deliver bad news over text-messaging,” he advises. “If the merchant is upset or frustrated by the news, it would be better-handled in a phone call so you could explain the reason for the negative news. A text message leaves too many things unsaid.”

See Post... scott tucker, his company would keep debiting the consumers account and only refund when the consumer contacted them.... |

See Post... scott tucker in the pdl space. his companies would leave the auto debits on and would not stop until their customers contacted them to make it stop and get a refund. if mca companies are doing this then they might ... |