Archive for 2021

Loan Fraudsters Resorting to AI Generated Faces

April 27, 2021 According to a sneak peek posted by Lendio CEO Brock Blake, fraudsters are stopping at nothing to game the government’s emergency loan system.

According to a sneak peek posted by Lendio CEO Brock Blake, fraudsters are stopping at nothing to game the government’s emergency loan system.

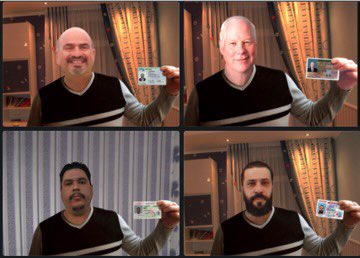

“Wanna glimpse into what lenders are experiencing with attempted fraudulent applications?” Blake wrote in a tweet. “Here are four ‘applicants’ seeking a loan.”

Four pictures showing computer-generated “business owners” all have the same sweater, but different heads. People are using AI tech to create randomized, just barely discernible pics of borrowers holding IDs beside them to beat new compliance measures.

It’s like a techno arms race between an automated scanning system that looks for fakes versus an automated fake ID and person generator that tries to make passable fakes.

After a year of PPP and EIDL success stories and fraud concerns, funders are still beating back scam artists. During a recent U.S. Senate hearing, SBA Inspector General Mike Ware said his office had secured $2.1 billion in fraudulently claimed PPP and EIDL loans.

In related news, the SBA announced the $28.6 billion Restaurant Revitalization Fund applications would open on Monday, May 3. Fraudsters start your fake restaurant owner generators.

Wanna glimpse into what lenders are experiencing with attempted fraudulent applications?

Here are 4 different “applicants” seeking a #ppploan. pic.twitter.com/kdbLmNGlvt

— Brock Blake (@BrockBlake) April 26, 2021

Move Over PPP, There’s a New Gov Grant in Town

April 23, 2021 We’ve heard rumblings of funding slowdowns because of competition from Uncle Sams’s emergency stimulus programs. But a soon-to-launch grant specifically targeting restaurants, food, and alcohol services may put PPP to shame.

We’ve heard rumblings of funding slowdowns because of competition from Uncle Sams’s emergency stimulus programs. But a soon-to-launch grant specifically targeting restaurants, food, and alcohol services may put PPP to shame.

The $1.9 trillion American Rescue plan signed last month set aside $28.6 billion toward the Restaurant Revitalization Fund. Just like PPP, the fund will dole out refundable grants up to $10 million to the most hard-hit food-related businesses.

Since PPP funds tend to run out quickly, the SBA apportioned $500 million just for merchants with less than $50,000 gross receipts in 2019. $4 billion will be set aside for the $50k- $500k bracket and $4 billion toward the $500k- $1 million bracket.

During the first 21 days of the program, the SBA will also focus efforts on disadvantaged businesses controlled by veterans, women, or those that suffer bias due to race or ethnic prejudice.

Just as in the PPP program, eligible businesses will have to devote the grant toward business expenses. That means payroll, loan financing, utilities, supplier, and equipment costs. Only companies that have survived the pandemic thus far with a physical location are eligible. The stipulations forbid a recipient to use funds to open a new venue.

Recipients will have to spend the money before the SBA end date, possibly December 2021 or later, or they will have to return the funds. The program is not live yet, but rumor has it will be opening in late April.

Yellowstone Capital, FTC Lawsuit Results in Settlement

April 22, 2021 The lawsuit filed by the FTC against Yellowstone Capital et al has resulted in a settlement. The defendants agreed to pay $9,837,000 for the matter to be resolved.

The lawsuit filed by the FTC against Yellowstone Capital et al has resulted in a settlement. The defendants agreed to pay $9,837,000 for the matter to be resolved.

As part of it, the defendants did not admit or deny the allegations of the complaint. They also agreed to have the FTC monitor their compliance with the agreement for varying but long periods of time.

Aside from the cost, the FTC made its point in two areas, the requirement that the defendants comply with a specific system of customer disclosure and that they not debit or cause withdrawals to be made from any customer’s bank account without the customer’s express informed consent. On the former, they must (roughly speaking) disclose clearly and conspicuously the amount and timing of any fees, the specific amount a customer will receive at the time of funding, and the total amount customers will repay.

The announcement coincides with the Supreme Court decision that revoked the agency’s presumed authority to obtain restitution or disgorgement under Section 13(b), the basis that the FTC brought against Yellowstone Capital in August 2020.

The FTC signed and filed the agreement less than 24 hours before the SCOTUS decision.

The FTC is Very Upset With the SCOTUS Decision

April 22, 2021 Responding to the FTC’s devastating loss on AMG Capital Management, LLC et al v Federal Trade Commission before the Supreme Court of the United States in which the agency’s presumed authority to pursue relief such as restitution or disgorgement under Section 13(b) was revoked, Acting Chairwoman Rebecca Kelly Slaughter said:

Responding to the FTC’s devastating loss on AMG Capital Management, LLC et al v Federal Trade Commission before the Supreme Court of the United States in which the agency’s presumed authority to pursue relief such as restitution or disgorgement under Section 13(b) was revoked, Acting Chairwoman Rebecca Kelly Slaughter said:

“The Supreme Court ruled in favor of scam artists and dishonest corporations, leaving average Americans to pay for illegal behavior. With this ruling, the Court has deprived the FTC of the strongest tool we had to help consumers when they need it most. We urge Congress to act swiftly to restore and strengthen the powers of the agency so we can make wronged consumers whole.”

The FTC claims that thanks to 13(b) they had secured billions of dollars over the past four decades “in relief for consumers in a wide variety of cases, including telemarketing fraud, anticompetitive pharmaceutical practices, data security and privacy, scams that target seniors and veterans, and deceptive business practices, among many others.”

Over the past five years alone, the FTC has refunded $11.2B to consumers through awards granted under 13(b).

The FTC has already begun to petition Congress to change the law.

United States Supreme Court Defangs FTC in Explosive Decision

April 22, 2021 The United States Supreme Court issued an explosive decision in AMG Capital Management, LLC et al v Federal Trade Commission, invalidating the Commission’s attempt and assumed power to pursue equitable monetary relief such as restitution or disgorgement under 13(b).

The United States Supreme Court issued an explosive decision in AMG Capital Management, LLC et al v Federal Trade Commission, invalidating the Commission’s attempt and assumed power to pursue equitable monetary relief such as restitution or disgorgement under 13(b).

Held: Section 13(b) does not authorize the Commission to seek, or a court to award, equitable monetary relief such as restitution or disgorgement. Pp. 3–15.

The immediate result is that the FTC’s largest judgment in history ($1.3 billion) against the companies belonging to payday lending kingpin Scott Tucker, has been undone.

The larger implication is that all of the FTC’s pending lawsuits seeking such relief against defendants under 13(b) are in mortal peril.

“Nothing we say today, however, prohibits the Commission from using its authority under §5 and §19 to obtain restitution on behalf of consumers,” the Court said. “If the Commission believes that authority too cumbersome or otherwise inadequate, it is, of course, free to ask Congress to grant it further remedial authority.”

Over the past five years alone, the FTC has refunded $11.2B to consumers through awards granted under 13(b).

Scott Tucker is currently in prison serving time for charges related to the FTC lawsuit. He was the subject in a Netflix Series called “Dirty Money” in 2018.

This story will be updated…

420: SAFE Banking Cannabis Finance Bill Passes House

April 20, 2021 De-banked cannabis firms are a step closer to being danked.

De-banked cannabis firms are a step closer to being danked.

The house of Representatives voted to pass the SAFE Banking Act in a partisan vote 321-101. The bill protects legitimate cannabis businesses from federal sanctions and regulations that bar banks from funding cannabis firms.

The law will pass to the Senate, where it failed to get support last year (and the year before) when it was lumped into a trillion-dollar stimulus plan that the GOP blocked over the summer.

But now, as a standalone bill, supports believe it has a chance to succeed, enabling cannabis firms to delve into institutional coffers and directing federal regulators to create guidelines to supervise weed banking.

“We are grateful to the bill sponsors who have been working with us for the last eight years to make this sensible legislation become law,” said Aaron Smith, CEO of the National Cannabis Industry Association. “The SAFE Banking Act is vital for improving public safety and transparency and will improve the lives of the more than 300,000 people who work in the state-legal cannabis industry.”

Time may be running out for alternative finance to fund cannabis firms before more traditional finance gets in. Advocates believe the bill should go through the Senate Banking Committee and pass before the end of the year.

The American Bankers Association has lobbied aggressively for the bill.

“Banks find themselves in a difficult situation due to the conflict between state and federal law, with local communities encouraging them to bank cannabis businesses and federal law prohibiting it,” the group wrote in a letter to lawmakers on Monday. “Congress must act to resolve this conflict.”

President of Fora Financial on New Credit Facility

April 19, 2021 Andrew Gutman spent six years at Fora Financial, the hot non-bank financing company that deBanked profiled in 2016. Gutman worked his way up to CFO before taking over day-to-day operations as president in February 2020. In that role he began working with a team to build an aggressive growth plan for the coming year of 2020. A couple of weeks later, the world shut down.

Andrew Gutman spent six years at Fora Financial, the hot non-bank financing company that deBanked profiled in 2016. Gutman worked his way up to CFO before taking over day-to-day operations as president in February 2020. In that role he began working with a team to build an aggressive growth plan for the coming year of 2020. A couple of weeks later, the world shut down.

“Covid was really a kick in the pants,” Gutman said. “How we were doing at the time, our strategic plans were out the door, our growth plan shuttered.”

Flash forward to April 2021, Fora announced a new $100 million credit facility: Not just back on track but finally ready to pursue the plans from a year ago.

“The first months were rough; after the pandemic started, we lost our securitization facility,” Gutman said. “But we kept going, originating aggressively. By around June or July, we started to feel competitive again and rebounded; we started bringing people back– hiring back staff that was furloughed.”

Gutman said the firm was able to change the winds, and by December they were not far off from where they were in 2019. Now set up finally for the aggressive growth plan they had laid out before Covid, Gutman said that though the pandemic threw everything to the wind, Fora still had the capital to back up a good book of business when everything else failed.

Can’t Wait For An Inheritance? Someone Will Fund You

April 19, 2021 Another twist on purchasing receivables is making its way into the mainstream in the form of an Inheritance Cash Advance.

Another twist on purchasing receivables is making its way into the mainstream in the form of an Inheritance Cash Advance.

For some, the aftermath of losing a loved one can turn into a long drawn out legal process and delay the transfer of rightfully owed inheritance in the process. Probate funders fix the problem, paying cash upfront, purchasing the future receivable of a will. The small industry is remarkably similar to the merchant cash advance world and uses the same terminology. “Inheritance Cash Advances are not loans,” one website says, “with an Inheritance Cash Advance, we send immediate cash to heirs in exchange for an assignment of a fixed dollar amount of their eventual inheritance.”

David Horton, a University of California-Davis law professor who delved into 1,119 probate agreements in the San Francisco area as part of a UPenn Study, said of the product “in almost all cases, with rare exceptions, the lender not only gets their advance back but also gets a huge markup.”

Interestingly, this type of funding is most popular in California, where some of the most complicated estate laws in the country make inheriting a hassle. But a less than flattering industry profile in Consumer Reports says that such companies “earn millions offering cash advances to heirs, with effective interest rates as high as 490 percent.”

And yet, industry advocates say that they are providing a needed service. “We are proud of the service we provide and the highest ethical way we conduct our business at IFC,” said Doug Lloyd, CEO of Inheritance Funding Company to Consumer Reports. “It is easy to understand why banks and other financial institutions are not in this business.”

His company has already advanced more than $200 million to customers. The following video is featured on their website: