Archive for 2021

Sonia Alvelo, CEO of Latin Financial Will Appear on deBanked TV

October 6, 2021 Sonia Alvelo, CEO of Latin Financial, will join Sean Murray live on deBanked TV on Thursday at approximately 12:15pm EST. Latin Financial is based in Newington, CT and Alvelo has contributed valuable insight to deBanked over the years, particularly on the Puerto Rican small business finance market.

Sonia Alvelo, CEO of Latin Financial, will join Sean Murray live on deBanked TV on Thursday at approximately 12:15pm EST. Latin Financial is based in Newington, CT and Alvelo has contributed valuable insight to deBanked over the years, particularly on the Puerto Rican small business finance market.

Anyone can tune in to debanked.com/tv/ for free without any registration to watch.

Who is Latin Financial?

A family owned and operated brokerage firm with a variety of backgrounds and expertise. We’re here to help all of our clients with their business’ unique financial needs. No loan is too big or too small for us; our goal is to simply help create a positive future for all of our clients. Here at Latin Financial, we understand that working capital can be difficult to obtain. With banks approving fewer and fewer loans, borrowing for your business’ future can be frightening and uncertain, especially in today’s economy. With Latin Financial you’re in good hands.

Latin Financial has over 10 years of business financial experience between its advisors.

We are at the forefront of this quickly changing economy and we work closely with our clients and investors because we are fully committed to meeting and exceeding expectations. We also believe in keeping our services affordable, working around your budget while never charging fees.

We are proud that so many of our clients have repeatedly turned to us for guidance and assistance with their business capital needs. We work hard to earn their loyalty every day.

LOOP Brings Real Tech to Auto Insurance

October 6, 2021 LOOP, a insurtech company that is launching a new concept of AI-driven auto insurance polices, was able to land $21M in Series A funding last week. The group of investors varied from venture capital groups to media companies to celebrities like hip-hop star Nas. The company claims to do auto insurance differently by changing the way they design premiums and qualify discounts.

LOOP, a insurtech company that is launching a new concept of AI-driven auto insurance polices, was able to land $21M in Series A funding last week. The group of investors varied from venture capital groups to media companies to celebrities like hip-hop star Nas. The company claims to do auto insurance differently by changing the way they design premiums and qualify discounts.

“We get rid of all the stuff that doesn’t matter in pricing [customers],” said John Henry, Co-CEO and Co-founder of LOOP, when explaining how the ways traditional insurance companies price their customer’s rates. This is where LOOP separates themselves from the pack. Things like credit scores, education, and income are not considered when pricing out their customer’s rates according to Henry, rather it’s how and where they are driving that determines the cost of insurance.

As an [Managing General Agent] MGA, LOOP underwrites its own risk and chooses the services they partner with to operate their claims. “This is not some digital brokerage or a quoting engine,” said Henry. “When you are insured by LOOP, it’s our actual product you’re insured by. We don’t sell any other products, we don’t sell leads, we are in the business of insuring people.”

LOOP will provide information to its customers that enables them to improve their driving and decrease their future rates. They will send customers tips on where and when to drive, and how to drive if they are driving erratically via a phone-based app. Their initial rate is based on population-level statistics from the respective area, and their personalized rate is a standard 6-month premium, meaning that the monthly rate won’t change month-to-month based upon how customers drive at certain times.

“We have millennials encumbered with student loan debt, we have immigrant populations with consumer loans, baby boomers selling their homes and losing their home and auto bundles, and the realities of the post-pandemic era means that we need more flexible and contemporary insurance solutions, and we are proud to be emerging as that,” Henry said.

![]() “We are the third step of insurtech,” he said, when asked how LOOP compares to others in the AI-based insurance sphere. “We’ve fundamentally built a novel insurance product from the ground up. Rather than sprinkle a digital layer on top of a legacy product, we completely rearchitected it.”

“We are the third step of insurtech,” he said, when asked how LOOP compares to others in the AI-based insurance sphere. “We’ve fundamentally built a novel insurance product from the ground up. Rather than sprinkle a digital layer on top of a legacy product, we completely rearchitected it.”

Henry boasted about how his company is the only one writing policies without traditional demographics in mind. “Today, I’m really proud to say that LOOP is the only insurance product that is a standard auto product that doesn’t have any of those demographic factors, it’s completely technology driven,” Henry said.

According to Henry, LOOP’s status as a public-benefit corporation, or B-Corp, will give his company the moral obligation it needs to fulfill its mission of being a fair, non-biased, and non-discriminatory auto insurance provider. The B-Corp status creates a “double bottom line” as Henry put it, creating a legal obligation for the company to hold the values in its mission statement for its customers, as well as the traditional corporate obligation to what’s best for its shareholders.

“From a business perspective, it’s kind of a risky thing,” Henry stressed when talking about the obligation to their customers as part of the public-benefit agreement. “The public can sue us if they ever feel like we are straying away from our mission.”

Customers are saving an average of 35% on their auto insurance premiums when quoted by LOOP, according to Henry. The company name directly correlates with the envisioned series of events that a LOOP customer will experience while holding a policy. A LOOP customer signs up, gets a good rate, utilizes the information given by LOOP, their driving is tracked and the data is analyzed, and the rate drops upon renewal after the policy expires. By repeating this, the customer “loops” around a cycle of better information leading to better rates.

“This is a mass market product. There is mass consumer demand. Our waitlist has grown to over 30,000 people across all fifty states, with different age groups and backgrounds,” Henry said. “I think people are excited to have an insurance company they can love again.”

Fintech Déjà Vu: Wait, Has This All Happened Before?

October 6, 2021 All one needs to do is answer a few short questions about their personal and business finances, have their answers evaluated by multiple leading lenders, and they’ll get a loan decision instantly, the advertisement said. Then, “select the loan that’s best for your business and get back to work all in less than 5 minutes.”

All one needs to do is answer a few short questions about their personal and business finances, have their answers evaluated by multiple leading lenders, and they’ll get a loan decision instantly, the advertisement said. Then, “select the loan that’s best for your business and get back to work all in less than 5 minutes.”

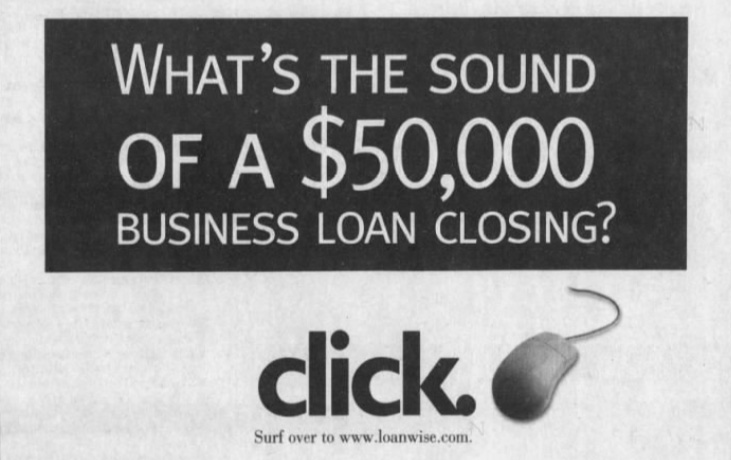

Touted as the “5-minute online business loan,” the ad for LoanWise ran in newspapers starting in 1999. That was 22 years ago. Back then, LoanWise was described as a marketplace that connected small businesses with lenders where borrowers could comparison shop for loans.

Provident Bank was the first to join the platform, where it would approve between $5,000 – $50,000 in as little as five minutes. At the time, the Los Angeles Times said that there were only 2,160 matches on Google for the phrase “small business finance.”

“2,160 is a big number no matter how you look at it,” the Times reported.

There’s over 6 million today by comparison.

LoanWise had set up 10 lenders on the platform by the end of 1999, with names that included American Express, Compass Bank, and PNC Bank. There was competition as well. Business Finance Mart and America’s Business Funding Directory also connected interested borrowers with lenders, according to the Times.

Today, all 3 websites no longer exist, forgotten vestiges from the land before fintech.

Or has this all happened before?

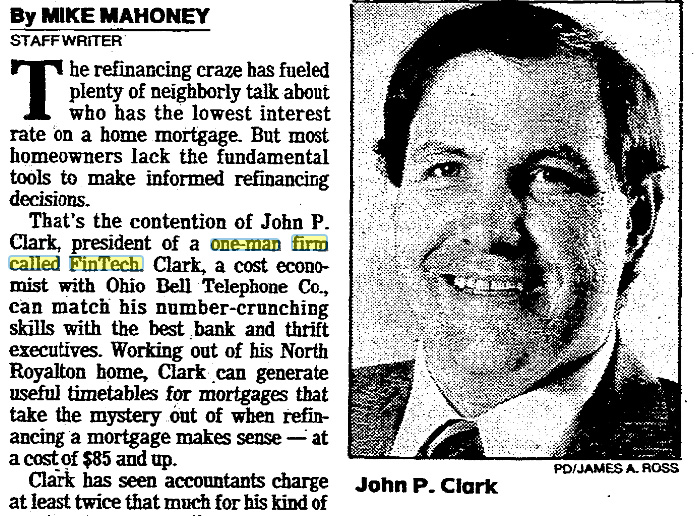

John P. Clark, a cost economist with Ohio Bell Telephone Co., ran a mortgage number crunching business in Cleveland on the side in 1986. Naming his company “FinTech,” Clark would help people calculate the best time to refinance.

John P. Clark, a cost economist with Ohio Bell Telephone Co., ran a mortgage number crunching business in Cleveland on the side in 1986. Naming his company “FinTech,” Clark would help people calculate the best time to refinance.

“Clark can generate useful timetables for mortgages that take the mystery out of when refinancing a mortgage makes sense,” wrote The Plain Dealer. Had it been 2021, Clark sounds like it would have been a billion dollar fintech app.

It was not a one-off.

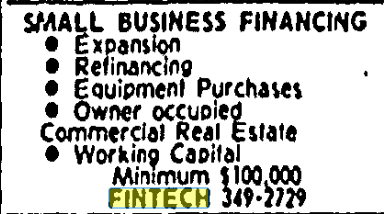

Fintech was the place to call if you wanted a working capital small business loan in San Antonio, TX starting in 1989. Ads for Small Business Financing advised people to call Fintech to get their business funded.

You could also just subscribe to the newletters. The Financial Times had four “FinTech Newsletters” in 1989 that were dedicated to covering electronic office, advanced manufacturing, telecom markets, and mobile communications. The price was £344 to £395 per year to receive them bi-weekly.

“FinTech newsletters tend not to be excessively technical,” The Guardian wrote on Aug 10, 1989, “but provide management guides to developments in each field, with lots of bullet points.” Perhaps the striking difference between that and today is that the newsletters arrived “hole-punched for filling in a binder.”

“FinTech newsletters tend not to be excessively technical,” The Guardian wrote on Aug 10, 1989, “but provide management guides to developments in each field, with lots of bullet points.” Perhaps the striking difference between that and today is that the newsletters arrived “hole-punched for filling in a binder.”

But hey, it’s all just a coincidence that ideas were roughly the same thirty years ago. Out in say, Des Moines, Iowa in the 1960s, for example, none of these things would’ve occurred to anyone.

Or would they have?

Sidney Feintech, a supermarket owner, expanded his store in 1963 to sell appliances, car batteries, clothing, and televisions. He got the idea that selling on credit would boost sales so he formed his own in-house credit company so that customers could Buy Now, Pay Later. Innocent enough, except the newspapers mispelled his last name.

“Fintech,” the papers said, had gotten into the credit business.

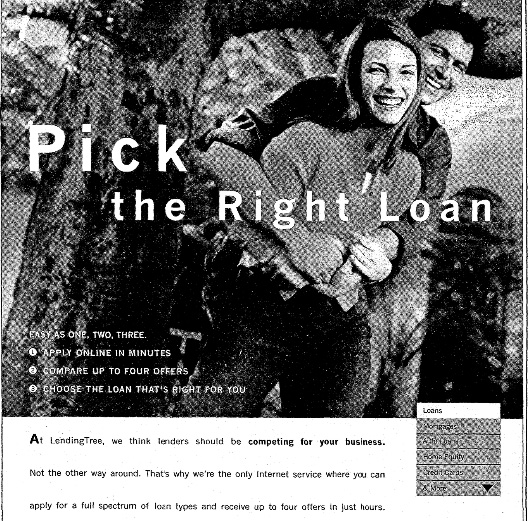

Fast forward 33 years to 1996 when a 26-year-old named Douglas Lebda thought the process of going from bank to bank to get a loan was too burdensome.

Fast forward 33 years to 1996 when a 26-year-old named Douglas Lebda thought the process of going from bank to bank to get a loan was too burdensome.

“I thought, ‘why can’t I put my information somewhere and let the banks compete for my business,” Lebda said. Launching a website, his company went on to generate $460 million worth of loans in just the fourth quarter of 1999 alone.

“There are other sites on the internet where you can apply for a loan, but those sites are operated by the lenders themselves,” Lebda said at the time. “We don’t lend money; that’s what makes us unique.”

That website was LendingTree, a company that today still has over 900 employees and a market cap of $1.8B. And Lebda is still the CEO.

In 1999, the hardest part was educating consumers to shop for loans online.

“Consumers have always done this one way, and this requires a behavioral change,” said consultant James Punishill in 1999. “In the old world, you’d pick up the newspaper and see a bunch of rates.”

“I knew from the start this would work because consumers really hate getting loans,” Lebda said at the time. “The market is huge and it’s perfect for e-commerce.”

How to Comment on New York’s Commercial Finance Disclosure Law

October 4, 2021With New York’s commercial financing disclosure law on the horizon for Jan 1, the state’s Department of Financial Services is seeking input on how the law should officially be rolled out. Their draft was published on September 21st. Directions for how to submit a comment were said to be forthcoming, but the when and how to do that, were not easily discernible.

The DFS website says that comments should be submitted via email to George Bogdan, but that the time to do that has already expired, the deadline having been October 1st.

A spokesperson for DFS on social media, however, said that comments on the law can be sent to: Comments@dfs.ny.gov.

This process of emailing comments contrasts with processes at the federal level which typically employ formal portals. While it may apparently be too late, anyone that had hoped to contribute their feedback but didn’t get to, could try the above contacts.

Canada is Looking Forward to Open Banking

October 4, 2021 “It’s a fairly big deal,” said Tal Schwartz, Senior Advisor to the Canadian Lenders Association, when discussing the Canadian government’s renewed interest in alternative lenders after the recent Canadian election. As potential government officials from both parties discussed ideas about open banking in their election campaigns, such a conversation had been quelled by the “Big Five” Canadian banks— until now.

“It’s a fairly big deal,” said Tal Schwartz, Senior Advisor to the Canadian Lenders Association, when discussing the Canadian government’s renewed interest in alternative lenders after the recent Canadian election. As potential government officials from both parties discussed ideas about open banking in their election campaigns, such a conversation had been quelled by the “Big Five” Canadian banks— until now.

“The closer we get to some kind of entrenched regulatory framework, the better positions fintechs will be in to actually compete, get access to financial data, and raise money in an environment where there is regulatory certainty,” said Schwartz.

In August, the Canadian department of Finance welcomed a Final Report from the Advisory Committee on Open Banking that showcased a plan to modernize the Canadian financial regulatory system, with open banking and fintech in mind.

“Consumer-driven finance, or open banking, is already part of Canadians’ lives,” said Chrystia Freeland, Canada’s Deputy Prime Minister and Minister of Finance, in the report.

“Many use digital services every day to manage their money, to budget for expenses, and to make investments. Working towards a regulated, made-in-Canada system will make sure that we continue to enjoy a strong, stable, and innovative financial sector that is globally competitive, promotes consumer choice, prioritizes data privacy, and contributes to economic growth,” Freeland continued.

Schwartz said that the traditional oligopolistic structure of Canadian banking can offer advantages in times of financial crisis, but not when the government is shelling out money to help businesses during pandemic-related shutdowns.

“The reality was, if you’re a small business, you don’t have a credit relationship with a big bank, the only credit relationship you have is with an alternate lender,” said Schwartz. “By distributing money through big banks, in one sense, you’re not servicing customers the way they want to be served, and you’re cutting oxygen to a flourishing part of the innovation economy in Canada.”

“The reality was, if you’re a small business, you don’t have a credit relationship with a big bank, the only credit relationship you have is with an alternate lender,” said Schwartz. “By distributing money through big banks, in one sense, you’re not servicing customers the way they want to be served, and you’re cutting oxygen to a flourishing part of the innovation economy in Canada.”

Unlike in the United States, the Canadian government gave exclusive access of allocation to pandemic-induced federal assistance loans to the Big Five banks, leaving small business lenders relatively out to dry during that time. When asked about what issues he would like to see the new administration tackle first when it comes to alternative lenders, Schwartz mentioned the allocation of this type of money moving forward.

Other institutions outside of big banking in Canada are making strides in their effort to compete. Fintech giant Stripe announced hiring sprees for their new Toronto office last Thursday. Then there’s Nuula, a startup that aims to build a user-centric financial super app, announcing $120M in funding in early September.

To reach its full potential, Canadian fintech companies need the access to more data. The report recognizes the acknowledgement of the necessity this data is to fintech companies. “The scope of Canada’s open banking system in its initial phase should include data that is currently available to consumers and small business through their online banking applications,” it says. “Financial institutions should be allowed to exclude derived data – described as data enhanced by financial institutions to provide additional value to their consumers, such as internal credit risk assessments” the report reads.

“Historically, there hasn’t been very tech friendly or [Big Bank] challenger friendly regulations,” Schwartz said. “This is really the first time we’ve seen the political parties even mention issues of open banking and saying this will be a priority for our next government.”

“This has given the industry a lot of hope,” said Schwartz.

MCA Skeptic Rohit Chopra Confirmed by Senate to Head CFPB

October 1, 2021 More than eight months after deBanked announced that FTC Commissioner Rohit Chopra would be the next head of the Consumer Financial Protection Bureau, his appointment has finally been confirmed by the Senate.

More than eight months after deBanked announced that FTC Commissioner Rohit Chopra would be the next head of the Consumer Financial Protection Bureau, his appointment has finally been confirmed by the Senate.

The confirmation of Chopra is notable given the agency’s objectives to collect data from small business finance companies and the fact that Chopra himself has been very vocal about merchant cash advances in particular.

One year ago, in his capacity as an FTC commissioner, he referred to the industry as “opaque” with “pay-day style” products whose structure “may be a sham.”

In an interview with NBC around the same time, he used stronger language, saying that he was “looking for a systemic solution that makes sure they can all be wiped out before they do more damage.”

Chopra knows his way around the CFPB. He worked for the agency when it first started in 2010 and was there for five years as the Assistant Director & Student Loan Ombudsman. He later moved to the FTC as a commissioner and now returns back at the CFPB in the director’s seat.

Fake Press Release Announced That SEC Had Dropped Case Against Ripple

October 1, 2021 XRP, the digital assets tied to Ripple, surged this morning from a price of $0.95 to $1.04 on the supposed announcement that the SEC had dropped its lawsuit against Ripple.

XRP, the digital assets tied to Ripple, surged this morning from a price of $0.95 to $1.04 on the supposed announcement that the SEC had dropped its lawsuit against Ripple.

The news came via press release service Accesswire in the headline “SEC vs Ripple Legal Fight is Over.” Other news outlets immediately picked it up, including Yahoo, and it made its way to the top of Google’s search results.

The problem is that the entire press release was fake.

“Ripple, the leading provider of enterprise blockchain and cryptocurrency solutions for global payments, is pleased to announce that the SEC vs RIPPLE legal battle is finally over,” it began. “The lawsuit that lasted over ten months has finally been settled between the Securities and Exchange Commission (SEC) and the cryptocurrency company Ripple. The SEC has announced it would drop its charges.”

Accesswire deleted it as did Yahoo. deBanked obtained it via archive.org. Merely googling: ripple sec, however still shows the fake headline as the top result.

The public may not be fully aware that the news is false yet, if the price is any indication. It’s still trading at $1.04 as of the time this story is being written.

Two weeks ago, GlobeNewsWire fell victim to a similar scheme, when it distributed a fake announcement that Walmart would begin accepting Litecoin.

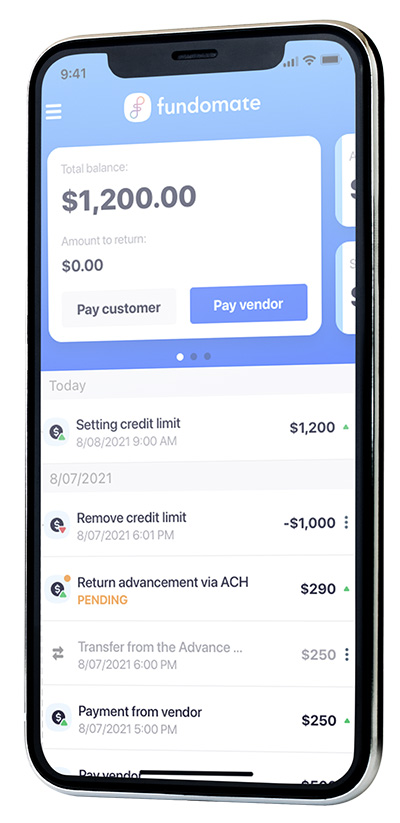

Fundomate Announces $50 Million Line of Credit to Bring Embedded Automated Funding and Real-Time Banking to Payments and SMB Marketplaces

September 30, 2021

Los Angeles, September 30, 2021 — Fundomate, a leading embedded finance provider of automated business funding solutions and real-time banking tools for merchant-facing platforms, announced the closing of a $50 million line of credit with Revere Capital today. The new line of credit is Fundomate’s largest to date.

Fundomate will leverage the credit facility to scale up its partnerships with merchant-facing businesses and grow the company’s new white-label banking platform. The platform enables merchant-facing platforms and marketplaces to rapidly expand their product suite and enhance engagement by offering automated financing and embedded banking tools under their own brand.

“With the closing of the $50 million credit line, Fundomate can scale its proven automated funding platform via its one-touch funding tool already embedded within 100+ payment processing partners and marketplaces”, says Sam Schapiro, CEO and Founder of Fundomate. “We’re excited to also focus on our new embedded real-time banking platform, which uses AI and advanced forecasting to provide our partners the ability to offer their customers free short-term working capital that’s available for immediate use.”

“With the closing of the $50 million credit line, Fundomate can scale its proven automated funding platform via its one-touch funding tool already embedded within 100+ payment processing partners and marketplaces”, says Sam Schapiro, CEO and Founder of Fundomate. “We’re excited to also focus on our new embedded real-time banking platform, which uses AI and advanced forecasting to provide our partners the ability to offer their customers free short-term working capital that’s available for immediate use.”

Revere Capital Managing Director Christopher Gilker said, “We’re incredibly excited to grow with Fundomate. As I tell all my colleagues, Fundomate is a company at the right place at the right time. The team is ambitious, and I have no doubt the company will disrupt the fintech, payments, and banking space in a big way.”

Revere Capital Managing Director Suman Mallick commented further, saying, “I’m very excited about Fundomate’s potential to change how businesses manage their banking and credit needs. I believe the company will benefit from strong secular tailwinds and has vast opportunities for growth with merchant-facing businesses throughout the US.”

Waterford Capital structured and arranged the line of credit on behalf of Fundomate. Dave Piotrowski, Managing Director at Waterford Capital, said, “Fundomate has an advantage over others in the merchant finance space through the products offered through their payment processor partners. This financing relationship with Revere Capital will help take the company to the next level and further broaden their competitive advantage.”

About Fundomate

Fundomate is an innovative fintech company that operates in the alternative lending space and provides both direct-to-business and white-labeled turnkey solutions, enabling merchant-facing platforms to offer alternative funding products to their customers as a value-added proposition.

The company has deployed over $100M to more than 2000 merchants across various industries in

the United States.

About Revere Capital

Revere Capital is a private credit manager with expertise in lower middle-market real estate bridge lending & specialty finance. The firm’s disciplined underwriting utilizes fundamental real estate analysis and research, emphasizing intrinsic value to create a diversified portfolio for investors. Revere also specializes in financing other commercial interests, consumer interests and insurance-backed interests. With a national footprint, Revere Capital offers speed, certainty of execution, and creativity to structure loans to fit borrowers’ needs and provide contractual income for investors.

About Waterford Capital

Waterford Capital is a leading arranger of structured finance and asset securitization transactions. The firm advises specialty finance companies and asset managers in connection with warehouse credit facilities, private placements of asset-backed securities, whole loan sale programs, and mezzanine and equity capital raises.