Uncategorized

Game Stopped? Short Selling, Social Media, and Retail Investors Collided in House Hearing

February 21, 2021 Nearly a month after the GameStop (GME) stock price shot halfway to the moon, the House Committee on Financial Services gathered representatives from the trading conflict in a hearing to examine what happened.

Nearly a month after the GameStop (GME) stock price shot halfway to the moon, the House Committee on Financial Services gathered representatives from the trading conflict in a hearing to examine what happened.

The focus was on a struggle between big institutional money and retail, everyday investors. Armed with nothing but zero-commission investment apps, government stimulus, and with nothing to do but sit at home waiting for a pandemic to end, retail traders exploded onto the securities markets. One of the results was a dramatic rise and fall of GME at the end of January.

Vlad Tenev, the Robinhood app’s co-founder, faced the highest number of questions after the firm blocked trading of GME on January 28th. Across the videocall-octagon was Keith Gill, a r/WallStreetBets retail investor long on GME since the summer, known by some as u/DeepFuckingValue.

With his signature headband hanging in the background, sitting in a gaming chair, Gill donned an uncharacteristic suit and tie while representing himself as a stand-in for the millions of retail investors who were along for the ride.

His message: he is no expert, is not responsible for the volatility of a multi-billion dollar securities market, and after everything, he still likes the stock.

“I support retail investors right to invest in what they want when they want to,” Gill said. “I do not have clients, and I do not provide personalized investment advice for fees or commissions. I am an individual investor.”

Gill went on in his testimony to state that his posts and video appearances about GME to other investors were not trading advice and no different than talking in a bar about a stock he liked.

Before the run-up of GME, Gill had a small audience of around 500 viewers. After GME started gaining ground, Gills’s online popularity exploded alongside the Reddit stock betting forum r/WallStreetBets.

Gill gained hundreds of thousands of followers, while WSB saw a rise of 8 million members in just one week. In the end, his positions in the stock earned him $22 million, as he shared with his extended family over the holidays, “we’re millionaires.” Many were not as lucky, and some have looked toward social influencers like Gill as speculators and market manipulators.

The Congressional Committee were light on their interrogation of Gill, acknowledging the importance of protecting retail investor rights. In challenging Tenev of Robinhood, Committee Chairwoman Maxine Waters set the tone, stating: “The market volatility around GameStop has highlighted how many people believe the cards are stacked against them.”

Waters asked numerous yes or no questions to Robinhood’s Tenev, who could only respond with drawn-out statements. Overall, the fintech founder was apologetic but still insisted Robinhood did nothing wrong and does not answer to hedge funds.

“Look, I’m sorry for what happened, and I apologize. I’m not going to say Robinhood hasn’t made mistakes in the past,” Tenev said. “We’re going to learn from this and make sure it doesn’t make the same mistake in the future.”

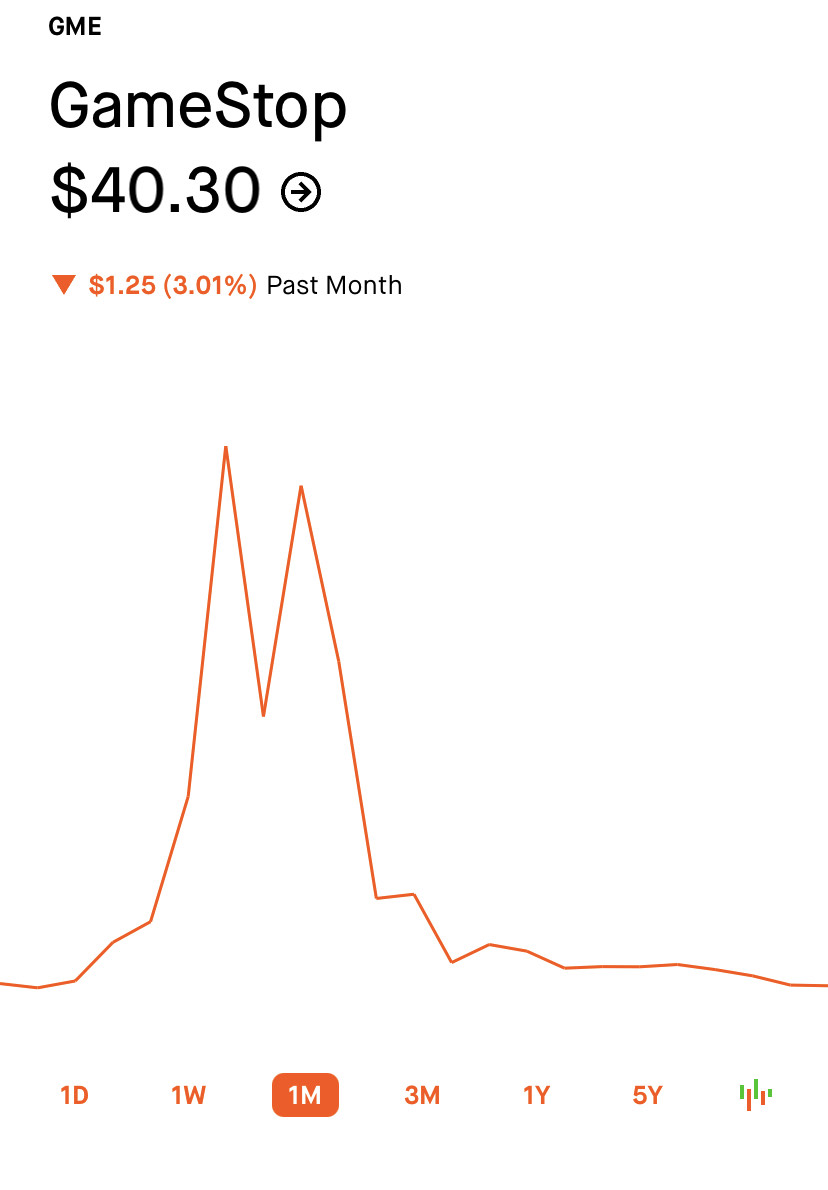

At the height of the trading frenzy Thursday, January 28th, Robinhood suddenly restricted the purchase of GME and other “meme” stocks and only allowed selling. Demand plummeted because, despite problems in the past, Robinhood is still a favorite in the r/WallStreetBets community. Prices roller coasted downward. From a high of $468/share, the GME price dropped down to trading in the $40 range in the month that followed.

Tenev was explaining his financial responsibilities to clearinghouses as a brokerage firm.

On the morning of January 28th, Robinhood suddenly received an email from a subsidiary of the DTCC, holder of all U.S. traded securities. It asked for an increase of $3 billion to ensure Robinhood could back the explosion of GME trading, an astronomical price. Robinhood complied by shutting down buying, offering sell-only, bringing the insurance price down to more than $700 million. The firm also reached out to existing investors to raise billions in capital, yet Tenev still insists there was never a liquidity problem.

Representing traditional, “smart money” investors was Ken Griffin of Chicago hedge-fund Citadel LLC and market-maker Citadel Securities, known for its short-selling positions. Alongside was Gabe Plotkin, the founder of Melvin Capital, a hedge fund with many short positions in GME, lost $6 billion in just 20 trading days. During the crazy trading week, Melvin was offered $2.7 billion in new investment from Citidel funds after losing 30% of its value.

Citadel is also a prime market maker for Robinhood, completing many of the app’s trades. Some, including those house members lobbing questions, saw a firm that self describes its mission as “to democratize investing,” cut out the poor and give to the rich. It looked like a collaboration between a major investor making up for losses due to app trading while retail investors were left out.

Chair member Blaine Luetkemeyer, a Republican from Missouri, expressed his concern that GME had been an over shorted stock and that “naked shorting” drove the price down.

“You have stated in your testimony that you had no intention of manipulating the stock,” he said. “If you’re short selling your stock 140%, for me from the outside, that looks like what you’re doing.”

Both Citidel and Melvin Capital representatives said there was no collusion to drive the price down, no over shorting, and no buy-out when the short positions failed.

The end of Gills’ testimony, read in front of a “hang in there” cat poster summed up the hearing well.

“It’s alarming how little we know about the inner-workings of the market, and I am thankful that this Committee is examining what happened,” He wrote. “I’m as bullish as I’ve ever been on a potential turnaround. In short, I like the stock.”

The New Largest Merchant Cash Advance in History: $90 million +

September 9, 2020The largest merchant cash advance in history (at $40 million), first publicly disclosed in 2018, has been outdone. On Tuesday, the Receiver in the Par Funding SEC case revealed that its largest customer had outstanding purchased receivables of $91.3 million. The customer is an office and cleaning supply company based on Long Island. The amount is now the largest known merchant cash advance deal in history.

Par’s second largest customer had outstanding purchased receivables of $35 million.

Par’s total receivables are estimated to be $420 million. $228.8 million of it stems from just 10 customers including the two referenced above, according to a recently filed report.

How NYC Fintech Women is Keeping its Community Going in a Pandemic

May 23, 2020 How does a community of people continue to support each other and network in a pandemic? What is lost when in-person meet ups are replaced by stop-start Zoom conversations? Do geographical limits even exist anymore when everyone is bound to their homes? These are the questions that NYC Fintech Women are dealing with now.

How does a community of people continue to support each other and network in a pandemic? What is lost when in-person meet ups are replaced by stop-start Zoom conversations? Do geographical limits even exist anymore when everyone is bound to their homes? These are the questions that NYC Fintech Women are dealing with now.

Founded in 2017, NYC Fintech Women is an organization of roughly 5,000 members that aims to provide its members with the opportunity to build a web of connections that might otherwise be out of reach. Open to both men and women, the group revolved around regular gatherings that afforded the chance to rub shoulders with both those entrenched in fintech as well as figures from institutional finance. Ranging from mid-tier employees all the way up to executives, the organization encompasses a broad section of those working in the intersection of finance and technology.

Born out of the frustration that Founder Michelle Tran felt when trying to locate fintech people at New York events which largely catered to institutional and traditional finance, the plan for the organization was two-pronged: get all these fintech types together for easier communication while also creating an environment that will allow women to “build their own board.”

Described by Tran as part of Fintech Women’s ethos, the idea is that you’ll have to build your own team if you’re going to get anywhere. “You really need to build your own personal board in order for any type of career advancement,” Tran explained over a call. “So making sure you’re pulling in the right leaders, the right support systems that are also diverse, and the best way to do that is to have a strong network of people at your fingertips.”

And it’s this ethos as well as the social aspects of community that have been challenged by the pandemic. But determined not to let covid-19 get the best of what the organization has become in the past three years, the group has been forced to adapt.

Like the rest of us, telecommunication is being brought in to replace what once came naturally. Slack will offer the chance to chat as a large group, smaller coffee chats will replace the opportunities to talk amongst peers, and a mentoring program launched in January is in the process of being turned fully virtual. And as well as these developments, the decision to expand beyond New York, a move that’s been on Tran’s mind for a while, is now looking more likely as events go online, removing the barriers that come with location.

“It’s a bit harder to just meet somebody, but we’re going to facilitate a number of different platforms in order to do that,” Tran said. “That’s one of the things that we continue to say is really important, and I think that’s what a lot of people miss too, as we’re all sitting alone in our home or with our families. We missed that engagement that we have with others, so we’re finding ways to do that.”

Robinhood Goes Down Three Times in One Week, And The Timing Couldn’t Be Worse

March 10, 2020 The free stock trading app Robinhood has gone down three times in the last week, causing angst and legal challenges from customers at a time when the US stock market is tanking. Stemming from uncertainty instilled by the coronavirus as well as worries over Saudi-Russia oil relations, the Dow Jones Index Average had dropped by 2,013 points at market close; the S&P 500 by 7.6%; and the Nasdaq by 7.29%.

The free stock trading app Robinhood has gone down three times in the last week, causing angst and legal challenges from customers at a time when the US stock market is tanking. Stemming from uncertainty instilled by the coronavirus as well as worries over Saudi-Russia oil relations, the Dow Jones Index Average had dropped by 2,013 points at market close; the S&P 500 by 7.6%; and the Nasdaq by 7.29%.

Robinhood’s first outage was on Monday, March 2. Lasting only a few minutes, the loss of service coincided with the biggest one-day point gain of the Dow in history. The second came the next day, lasting two hours after the Federal Reserve announced a cut of 0.5% to interest rates.

The Sarasota-based tech giant’s co-CEOs released a statement that Tuesday on the company’s blog placing blame for the outages on their overstressed infrastructure. They claimed that their servers struggled with an “unprecedented load” that led to a “‘thundering herd’ effect—triggering a failure of our DNS system.”

The company has yet to release a statement explaining the third service blackout today, which took place during a period that saw the stock exchange pause trading for 15 minutes to prevent a freefall.

In response, Robinhood customers are threatening legal action. Numerous Twitter accounts have popped up under the name ‘Robinhood Class Action,’ or as some variation of this, with the largest of these having over 7,500 followers at the time this article was published. Travis Taaffe of Florida filed a federal lawsuit on Wednesday on behalf of himself and other traders, claiming that Robinhood was negligent and in breach of contract by failing to “provide a functioning platform” for traders, rendering them unable to move stocks.

Having 10 million customers, the company could be facing a lot of claims. As of last week, Robinhood has been offering its Gold members three months of the subscription for free. The price of this would amount to $15 dollars altogether; and the second cost of the subscription, 5% yearly interest on borrowing above $1,000, will not be waived as part of this compensation. Robinhood has described this offer as a “first step.”

United Capital Source Placed $199M In Deals In 2019

January 5, 2020 United Capital Source, a commercial finance brokerage based in New York, placed 3,883 deals in 2019 for a grand funding total of $199.3 million. Company CEO Jared Weitz said on LinkedIn of the milestone, “Our employees all saw growth (again) this year both professionally and personally. As we come into 2020 we are going into our 10th year of business!!!!! I cannot wait to see what these next year(s) hold for us. I’m so thankful for our Funding Partners and most of all our wonderful staff.”

United Capital Source, a commercial finance brokerage based in New York, placed 3,883 deals in 2019 for a grand funding total of $199.3 million. Company CEO Jared Weitz said on LinkedIn of the milestone, “Our employees all saw growth (again) this year both professionally and personally. As we come into 2020 we are going into our 10th year of business!!!!! I cannot wait to see what these next year(s) hold for us. I’m so thankful for our Funding Partners and most of all our wonderful staff.”

Weitz is scheduled to speak at deBanked CONNECT MIAMI on January 16th at the Loews Hotel on a panel discussion about how to make money in 2020.

Fears of Possible Recession Don’t Phase CRE Lenders

December 16, 2019 Depending on your vantage point, a slowdown is either already in progress, just around the bend or several years away. But some alternative commercial real estate professionals are trying to filter out the noise.

Depending on your vantage point, a slowdown is either already in progress, just around the bend or several years away. But some alternative commercial real estate professionals are trying to filter out the noise.

Instead, they are more aggressively forging ahead with growth plans, including trying to grab market share from banks.

The commercial real estate lending market remains highly competitive and alternative lenders say they remain focused on looking for opportunities to expand their business, even as the possibility of recession looms. At present, a number of professionals don’t see an imminent threat of recession, and even if there is one, they say they stand to benefit from picking up business banks don’t want to take on—or can’t—because of increased regulatory controls imposed on them since the last recession.

There are plenty of opportunities for alternative commercial real estate lenders to get ahead, even in this environment, says Chris Hurn, founder and chief executive of Fountainhead Commercial Capital, a Lake Mary FL-based, non-bank direct small business lender in the commercial real estate lending space.

To be sure, alternative commercial real estate lenders say that for the most part, there hasn’t been a major pullback in their space. But due in part to mounting economic concerns and changing business priorities, banks—which had already scaled back from their pre- Great Recession exuberance—have been taking an even more cautious approach to lending. This is especially true in certain regions of the country, or in sectors deemed higher-risk such as hospitality and retail, alternative lenders say. While the pullback hasn’t been broad-based, it’s been enough in some cases to create strategic pockets of opportunity for opportunistic non-bank lenders such as private equity funds, debt funds, crowdfunding portals and others.

To be sure, alternative commercial real estate lenders say that for the most part, there hasn’t been a major pullback in their space. But due in part to mounting economic concerns and changing business priorities, banks—which had already scaled back from their pre- Great Recession exuberance—have been taking an even more cautious approach to lending. This is especially true in certain regions of the country, or in sectors deemed higher-risk such as hospitality and retail, alternative lenders say. While the pullback hasn’t been broad-based, it’s been enough in some cases to create strategic pockets of opportunity for opportunistic non-bank lenders such as private equity funds, debt funds, crowdfunding portals and others.

For many of these commercial real estate professionals, whether or not a recession is on the horizon is not a guessing game that’s worth playing. And with good reason, given how much disagreement there is among market watchers, investment management professionals and others about where the economy is headed.

Certain economic data continues to be strong, for instance, but political and geopolitical factors such as trade wars continue to raise red flags. Then there’s the fatalistic notion that the economy has been on a tear for so long that it’s due for a pullback at some point. This all translates into a hodgepodge of speculation and indecision about the economy’s direction. The dichotomy is evident from the difference in sentiment expressed in two fund manager surveys from Bank of America Merrill Lynch taken a month apart. October’s survey was decidedly bearish; by November, the bulls were back, muddying the waters even more.

Instead of wavering in indecision, however, some alternative commercial real estate players are hunkering down and highly focused on building their business in a cautiously optimistic and strategic manner.

Hurn of Fountainhead Commercial Capital predicts a number of increased opportunities for alternative commercial real estate lenders due to pullback from banks and a growing need for capital. He cautions alternative lenders against being too pessimistic and losing out on potentially lucrative market opportunities as a result.

“I think we might be going into a period of slightly slower growth, but none of the indicators suggest we’re remotely close to where things were 10 years ago,” Hurn says. “If we’re not careful, we’re going to talk our way into recession. It’s a self-fulfilling prophecy.”

Indeed, even as perplexing questions about the economy’s long-term health persist, some alternative commercial lenders anticipate growth in the coming year. Evan Gentry, chief executive and founder of Money360, a tech-enabled direct lender specializing in commercial real estate, says the company’s loan origination business is on track to close between $650 million and $700 million in 2019. That’s expected to increase to about $1 billion in 2020, fueled by growth in some strategic markets, including Washington DC, Atlanta, Miami and Charlotte, N.C., where the company is seeking to add loan origination personnel. Gentry says the company also continues to experience strength in many of the western markets, including the intermountain west markets of Colorado, Utah and Idaho, where growth is expected to continue.

CommLoan, a commercial real-estate lending marketplace in Scottsdale, Ariz., also sees strategic opportunities to grow in this environment. Mitch Ginsberg, the company’s co-founder and chief executive, predicts 2020 will be a strong growth year for his company, after a several-year beta period. CommLoan has plans, for example, to start hiring account executives to build relationships in additional states. Initially, the focus will be on institutions in the Southwestern U.S., with plans to add lenders in Texas, Utah, Colorado and New Mexico in the early part of 2020, Ginsberg says.

Though certain regions or business lines within commercial real estate may be experiencing some pullback, he says his overall outlook for the economy and commercial real estate remains strong. “There is still an enormous amount of activity,” he says. “If and when a correction does happen, it’s going to be a lot softer and not that deep and not that long because of the fundamentals in the economy.”

FINDING WAYS TO COMPETE MORE EFFECTIVELY WITH BANKS AND OTHERS

Some commercial real estate professionals say they are focusing more attention on sectors, regions and concentrations that the banks aren’t going after so readily.

If an alternative lender can offer more money than a bank on a particular deal or offer more flexible terms, or do deals that traditional lenders simply won’t do, for example, then it’s a boon for them. For a slightly higher price, alternative lenders—especially those whose business model relies heavily on technology—are able to take on slightly riskier deals than a bank might be able to stomach, says Jacob Goldsmith, managing partner of Goldwolf Ventures LLC, a privately held alternative investment and asset management company with offices in Miami and Austin.

“Alternative lenders are a lot more nimble,” says Goldsmith, who keeps close tabs on the commercial real estate lending industry.

Especially given the ambiguous economic climate, there are several areas that could be prime opportunities for savvy alternative commercial real estate lenders to gain a leg up. For instance, some banks of late have shied away from certain special purchase property types like hotels, day care facilities and free-standing restaurants, says Hurn of Fountainhead Commercial Capital. These types of properties are traditionally seen as riskier in the latter part of an economic cycle.

Especially given the ambiguous economic climate, there are several areas that could be prime opportunities for savvy alternative commercial real estate lenders to gain a leg up. For instance, some banks of late have shied away from certain special purchase property types like hotels, day care facilities and free-standing restaurants, says Hurn of Fountainhead Commercial Capital. These types of properties are traditionally seen as riskier in the latter part of an economic cycle.

Nonetheless, “there’s opportunity here for non-traditional lenders to step in and fill that gap,” he says. Retail loans are another category where banks have been pulling back. One reason banks are being more cautious is the sentiment that as online shopping becomes more pervasive, there’s less of a need for brick-and-mortar shops. This trend is underscored by the recent announcement of Transform Holdco—the company formed to buy the remaining assets of bankrupt retailer Sears Holdings Corp.—that it would close 96 Sears and Kmart stores by the end of February. Still, some industry watchers aren’t ready to concede retail’s demise.

While these types of announcements fan fears, concern over the death of retail is largely overblown, according to Troy Merkel, a partner and real estate senior analyst at RSM, which provides audit, tax and consulting services. “The banks are being too overly cautious,” he opines.

The opportunity for alternative lenders, he says, is not in funding loans that add to the supply, but rather in funding loans that change the existing supply. While the need for new development may not be as great, there is a growing demand for repurposed properties, he says. This includes upscaling an older mall or turning an existing retail building into a mixed use property, namely a mix of retail stores and multi-family apartment complexes. There is still a real need for these types of developments, Merkel says, and with banks shying away, the door is open for alternative lenders to “make a play,” he says.

Real estate professionals say they also see opportunities for alternative commercial real estate lenders to make loans in areas outside major metro cities, where the competition isn’t as strong.

“There will always be opportunities in the ups and downs, the ebbs and flows of the cycle. You just have to be a lot smarter in this part of the cycle,” says Goldsmith of Goldwolf Ventures.

BECOMING RECESSION-PROOF

Pockets of opportunity notwithstanding, alternative commercial real estate lenders have to play it smart, professionals say. For instance, they should not be overly bullish on a particular sector or throw caution to the wind when it comes to their underwriting practices.

That’s because when the market turns—as it inevitably will at some point—there will likely be more defaults and lenders that haven’t dotted their I’s and crossed their T’s will understandably face stronger headwinds. They need to keep their close eye on expenses as well, which may have ticked upward over the past several years. “People get complacent when times are good. This is probably not the time to be complacent anymore,” says Hurn of Fountainhead Commercial Capital.

Another protective measure against an eventual downturn is to diversify sales channels and property types. “If you put too many eggs in one basket, it’s a problem,” Hurn says.

It’s also important for lenders to have their guards up since higher risk deals can lead to losses if a recession hits. Lenders have to be smart when it comes to taking on risk, says Tim Milazzo, co-founder and chief executive of StackSource, an online marketplace for commercial real estate loans. “They have to have a certain expertise in underwriting these transactions correctly and assessing risk,” Milazzo says.

It’s also important for lenders to have their guards up since higher risk deals can lead to losses if a recession hits. Lenders have to be smart when it comes to taking on risk, says Tim Milazzo, co-founder and chief executive of StackSource, an online marketplace for commercial real estate loans. “They have to have a certain expertise in underwriting these transactions correctly and assessing risk,” Milazzo says.

In light of significant ambiguity about where the economy is heading, Gentry of Money360 says his company is protecting itself by taking an ultra- conservative approach. This means, for instance, only making first-lien position loans secured against income producing properties at a loan-to-value ratio on average of 65 percent, he says. Some alternative lenders are making these loans at a loan-to-value ratio of 80 percent or 85 percent, but Gentry says this is too high a rate for his taste. Also, Money360’s loans are also generally short- term—in the two-to-three-year range, which reduces some of the risk and seems especially prudent at this point in the cycle, he says.

When the market turns—as it inevitably will at some point—there will be more loan defaults, and those that are on the more aggressive end of lending will bear most of the challenges, he says.

He cautions other alternative lenders to avoid taking on excessive risk. “You’ve got to be thinking ahead and planning and lending as if the downturn is right around the corner—because it could be,” he says. Even taking a conservative approach, there are still significant business opportunities, he says.

BE ON THE LOOKOUT FOR RECESSIONARY OPPORTUNITIES

Meanwhile, if a recession does hit, alternative commercial real estate lenders say they will have even more opportunities to gain market share, participate in workout financing and hire key personnel. Alternative lenders that are more steeped in technology may potentially have even more of an upper hand since this can enable them to close deals much more efficiently and quickly and at a lower cost, while at the same time giving borrowers broader access.

“In a tighter market, every reduction in rate and cost will make more of a significant difference to borrowers than it does at the moment,” says Ginsberg of CommLoan, the commercial real-estate lending marketplace.

Although there are a growing number of alternative commercial real estate lenders who are relying more heavily on technology than they did in the past, commercial real estate lending still hasn’t flourished online to the extent personal and small business lending has. One reason is that the loans are larger and human intervention is often seen as beneficial, says Gentry of Money360.

However, online lending within the commercial real estate lending space is still on the horizon, according to Ginsberg of CommLoan. “It’s slow-go, but it’s inevitable,” he says.

Will Millennials Bring Non-banks into Their Finances?

April 1, 2019 Following Apple’s announcement last week of its upcoming Apple Credit Card, one question that comes to mind is: Will people, particularly millennials (now roughly 22 to 37 years old), be up for banking with non-bank companies?

Following Apple’s announcement last week of its upcoming Apple Credit Card, one question that comes to mind is: Will people, particularly millennials (now roughly 22 to 37 years old), be up for banking with non-bank companies?

According to an Accenture survey from five years ago, 34% of millennials said they would bank with Apple if such a product were available. Well, five years later, the product is available and Apple is now hoping to capture that demographic. According to the same survey, even more millennials at the time said they would be open to banking with Amazon or Google, and all with no physical branches.

Sankar Krishnan, Executive Vice President, Banking and Capital Markets, at Capgemini, a technology services and consulting company, said that convenience is most important to millennials.

“Millennials and Gen Y live their lives on smartphones… [and] daily comforts such as Uber, Starbucks, Amazon, Tinder and Netflix, are just a swipe away,” Krishan said in an interview in Forbes last year. “As a result, [they] have become accustomed to a quality digital customer experience where ease of use and inbuilt functionality are front and center.”

The implication is that any digital company with enough visibility and the ability to execute is fair game to enter the banking business. Why not Netflix? But Tinder?

Regardless, most major technology companies, like Amazon, Google, Facebook and Uber, are already in the payments space in one way or another. While potentially jarring at first, it seems that many millennials are ready to allow non-bank brands to become more a part of their finances.

Yet despite all the talk of how millennials are willing to break with convention, almost half of millennials said they would not consider switching to a bank that had no physical branches, according to a January 2019 survey conducted by eMarketer.com, which creates marketing reports.

“Though [millennials] may use branches less than older consumers, they don’t want to forgo the option of going to a physical location,” said eMarketer principal analyst Mark Dolliver. “The step from ‘digital’ to ‘digital-only’ is a big one, and many millennials will be in no hurry to take it.”

Wintrust Expands Accounts Receivables Financing

December 17, 2018Today, Wintrust announced the creation of Wintrust Receivables Finance, an expansion of the company’s asset-based lending group, according to a story in Monitor Daily. This translates to the addition of a specialized team focused on accounts receivables financing to middle market companies, with revenues between $10 million and $300 million.

“We think this team is a great expansion to our current services,” said Edward J. Wehmer, Founder and CEO of the Chicago-based regional bank. “Wintrust Receivables Finance makes our asset-based lending even more robust and competitive.”