Uncategorized

Canadian Lending Looks Strong Post-Pandemic

January 11, 2022 After having their entire industry threatened by pandemic-induced restrictions, the Canadian alternative finance space has started 2022 off with a bang. Canadian lending saw billions in growth, as the industry hopes to utilize fintech’s technology and the government’s new take on open banking to bring their industry back to full swing.

After having their entire industry threatened by pandemic-induced restrictions, the Canadian alternative finance space has started 2022 off with a bang. Canadian lending saw billions in growth, as the industry hopes to utilize fintech’s technology and the government’s new take on open banking to bring their industry back to full swing.

“Main Street small business recovery is looking very strong for 2022 as restrictions ease moving into the warmer weather,” said Tal Schwartz, Senior Advisor for the Canadian Lenders Association. “However, in the short term, lenders are paying close attention to the Omicron variant, and particularly how aggressive the federal government is prepared to be in terms of sustained subsidies.”

Despite the uncertainty of the next several months, Canadian finance seems to have a healthy balance of offering modern financial products alongside an effort a return to normalcy. The crypto-lender Ledn raised $70M USD for the world’s first crypto-secured mortgage product, while the BNPL company Flexiti received a $527M facility from the National Bank of Canada. Merchant Growth, a small business lender, also raised $4m in equity financing.

According to Schwartz, most lenders who stayed in business used the last year to deeply invest in their technology across the board.

“[Lenders] have equally repositioned themselves in ways that better service a post-pandemic SMB clientele,” he said. “There is significant effort among lenders to evolve into financial health dashboards of a business, rather than being viewed exclusively as a financing source.”

According to the numbers, there has been significant growth by two notable Canadian lenders that are acting both as a financial management tool and a lending source. Canada’s largest subprime lender goeast Ltd, and Borrowell, a mobile loan marketplace, achieved $2B in portfolios and 2M users respectively to end the year.

“Fintech platforms become more sticky and can capture more client data if they become a hub for business management, with financing simply being a component of their platform,” said Schwartz. “Fintech lenders are coming out of the pandemic much stronger and with a sharper mandate than before.”

The Industry is Back; Broker Fair Takes NYC

December 7, 2021 Broker Fair 2021’s showcasing in lower Manhattan on Monday brought together an unprecedented amount of attendees, that not too long ago saw their entire livelihoods and industry threatened by a pandemic-hampered economy.

Broker Fair 2021’s showcasing in lower Manhattan on Monday brought together an unprecedented amount of attendees, that not too long ago saw their entire livelihoods and industry threatened by a pandemic-hampered economy.

“We are so happy to be here,” said Sonia Alvelo, CEO of Latin Financial and speaker on the ‘Great Debate’ panel. “With everything that has happened in the past two years, we are just super excited to be a part of this.”

Speakers at the event included keynote Slava Rubin, founder of Indiegogo, Oz Konar of Business Lending Blueprint, and Leo Kanell of 7 Figures Funding.

“We’re here to rekindle,” said Adam Abraham, Partner at Blueline Capital Group. “It’s always good to meet face to face. We’ve all been speaking on the phone for years at this point, so if you put a face to the name, it changes everything.”

That alone, is the best part about this event,” said Abraham. “Here, it’s about who you’re networking with.”

Other attendees felt that alongside the networking opportunities, events like Broker Fair allow the industry to truly leverage its core strength — its relatively small size compared to other areas of the financial world.

“Despite what many people think, this industry isn’t really as big as other finance industries,” said Josh Feinberg, CEO of Everlasting Capital. “When we come together like this, it really drives inspiration, thoughts, and dreams to be able to make this industry what it is today. I think these events really bring everyone together to drive the industry to the next level.”

A total of five panels took the stage throughout the day, and included individuals from across the business financing landscape. Other highlights of the event included a Small Business Finance Professional certification course, an expo room with over fifty companies and tables, and a hip-hop performance with viral artist Kosha Dillz.

At the event, deBanked Connect Miami was announced, which will take place on March 24. For the first time, deBanked will shift away from Miami Beach and into Downtown Miami, an area in which many members of the finance, crypto, lending, and banking industries have resettled and developed new flagship offices.

“I’m super pumped about the announcement of the show,” said Feinberg. “We’ll see everyone in Miami.”

AMEX’s Journey from Courier to Creditor

November 24, 2021 Have you swiped your American Express card lately?

Have you swiped your American Express card lately?

If so, you belong to one of the most ambitious company pivots ever known. The credit card company known for its prestigious clientele was once a shipping company and up until the early 1900’s, it exclusively shipped stuff at an expedited pace across America.

The origins of the namesake comes from the company’s previous model, an express courier service in the mid 1800s. During that time, “express” services were the next up-and-coming industry. These services allowed quick and precise shipping of small, valuable items around the United States, and were frequent among people who were concerned with the fragility of their items. It was also a second, faster option to the US Postal Service.

By 1850, the top express services realized that their competition was doing more harm than good for one another. That’s when three New York-based express companies owned by Henry Wells, William Fargo, and John Butterfield combined their companies into one, dubbing the new service American Express.

During the formation of American Express, the California gold rush was at its peak. Promises of new cities that were an escape from the smog dens of the east coast brought millions of Americans out west. Wells and Fargo, the first President and Vice President of American Express, respectively, moved out to San Francisco in an attempt to extend American Express to the west coast during this time.

Wells and Fargo were discouraged by their colleagues at American Express to branch out west, and were forced to simultaneously run American Express in the East, and their new company in the west. This western venture became known as Wells Fargo.

Throughout the rest of the 1800s, American Express continued their ventures in express shipping, expanding operations into railways and expanding their routes around the east coast. The Civil War was a huge growth spurt for the company as the demand for express shipping skyrocketed.

After both Wells and Fargo made their way through the ranks at American Express, both serving as President prior to their departure, it was James Fargo, the son of William, who some say is the individual who introduced the idea of providing financial services for customers in 1891. James was the one to introduce American Express’ money order, a cheaper and more modern version of a system already in place by the postal service at that time. American Express became the provider of the go-to money order for immigrants who wished to send money to their families in various parts of the world. After the huge success of the money orders, this led to the company releasing their trademark product, the traveler’s check, at the turn of the century.

Their full blown transition to financial services occurred in 1918, when the US government nationalized all express shipping companies as part of the World War I fighting effort. This resulted in the company being left only to function off of its two side ventures, money orders and travelers checks.

These stayed relatively stagnant for the next fifty-or-so years until American Express started to become what we know them as in today’s market. In 1958, the company issued its first credit card. Half a million people signed up for the card in its first 90 days on the market.

The rest is history. The charge card, then the tier’d cards, followed by their prestigious centurion or “black” card, the options expanded into different tiers of luxury through credit. This prestige that justifies the consumer fee, combined with the high fees they charge merchants to process the payments, is why the company is so successful. As American Express clients tend to make and spend more money, merchants are inclined to take American Express cards to attract their market, and just consider the higher fees as just a cost of doing business.

Not only is American Express an impeccable example of brand construction and marketing, but a great learning opportunity for any business who is forced to change their business model due to extenuating circumstances. Their story gives the notion that no matter the size of the company, the opportunities are endless with the right balance of dedication, innovation, and calculated risk taking.

Media, Market Duped Again in Fintech Fake News

September 13, 2021 Multiple media outlets fell victim to a major hoax Monday morning, after GlobeNewsWire claimed that Walmart was beginning to accept Litecoin as tender for purchases in its stores. The wire seemed legit — a formally structured release from a credible source that was packed with quotes form Walmart’s CEO Doug McMillon about the company’s apparent move.

Multiple media outlets fell victim to a major hoax Monday morning, after GlobeNewsWire claimed that Walmart was beginning to accept Litecoin as tender for purchases in its stores. The wire seemed legit — a formally structured release from a credible source that was packed with quotes form Walmart’s CEO Doug McMillon about the company’s apparent move.

With a bad link on the release alongside silence of the supposed partnership on Walmart’s end, skeptics quickly realized that no move was ever in the works. After denying the validity of the release, tons of major outlets began scurrying to announce the hoax.

The motive may have been to artificially inflate Litecoin, as it shot up 35% minutes after outlets ran with the story.

This is eerily like one of the industry’s most infamous hoaxes, when the news service known as Internet Wire made headlines for the wrong reasons back in 2000. Then 23-year old Mark Jakob was out almost $100,000 after shorting stock for the Emulex Corporation, which he attempted to recoup by writing a fake press release stating that the company was going to restate quarterly earnings as losses, and their CEO was quitting the company. Jakob was a former employee of Internet Wire and a community college student at the time.

His faux release resulted in Emulex losing over $2 billion in market cap, while Jakob netted almost a quarter of a million dollars to cover his shorts and then some.

Jakob later pled guilty to creating the fake release in order to cover his shorts. He earned himself over 40 months behind bars, forfeited all of his earnings, and was handed a 6-figure penalty for his actions.

Then there was PRWeb’s publishing of a press release that falsely stated that Google had made a $400 million deal to purchase a Rhode Island- based wireless hotspot provider in 2012, which made the provider’s shares jump dramatically. Many major media outlets took PRWeb at their word and ran with the story. It was later discovered that the release was completely bogus and had come from a Gmail account that had originated in Aruba.

Reporting with one hundred percent accuracy is difficult. Information updates, numbers fluctuate, and deadlines loom. Vetting sources is an integral part of being a quality journalist, but even the best can get fooled, turning perceived truth into a manipulated consensus of reality.

In fintech news however, these hoaxes aren’t just blurring facts and changing narratives, they could result in the moving of billions of dollars around the market before the deception is revealed.

Square Loans (Formerly Square Capital) Originated $627M in Small Business Loans in Q2

August 4, 2021 Square Loans, the lending arm of the fintech bank Square, originated $627M of its Flex Loans in Q2, according to the company’s latest announcement. That brings the year-to-date total to $1.02B across 167,000 loans. The numbers produce a rough average of only $6,000 per loan.

Square Loans, the lending arm of the fintech bank Square, originated $627M of its Flex Loans in Q2, according to the company’s latest announcement. That brings the year-to-date total to $1.02B across 167,000 loans. The numbers produce a rough average of only $6,000 per loan.

“After pausing flex loan offers from early March to late July of 2020, we continued to expand loan offers during the second quarter behind improvements in underlying Seller GPV trends, nearing pre-pandemic quarterly origination levels for core flex loans,” the company said.

Square is on pace to meet or eclipse its pre-covid volume. (It originated $2.3B in 2019.)

Square touted much bigger news in the past few days, however, its planned acquisition of Australia-based Afterpay in a $29B all stock deal.

PayPal Originated ~$2.6B in Funding During 2020

May 10, 2021 PayPal reported originating a total of about $2.6B in capital for U.S. SMBs in 2020, which doesn’t include the more than $2B in PPP loans it arranged.

PayPal reported originating a total of about $2.6B in capital for U.S. SMBs in 2020, which doesn’t include the more than $2B in PPP loans it arranged.

“PayPal delivered record performance in 2020 as businesses of all sizes have digitized in the wake of the pandemic,” Dan Schulman, President and CEO, said.

Exact origination figures are hard to track through the firm’s quarterly reports. The Working Capital product is only mentioned in passing. At the outset of the pandemic, PayPal reported that they helped merchants by “Granting deferral of repayments on business loans and cash advances at no additional cost.”

Throughout the remainder of the year, PayPal was echoing the problems of the industry and slowed down funding as a whole. In the 2021 first quarter call, John Rainey the CFO Global Customer Operations, said that the firm “Tightened underwriting and strong repayment activity contributed to lower balances in our merchant loan portfolio.”

PayPal’s origination volume fell relative to their 2019 estimate.

MSU Spartans Presented by Rocket Mortgage

March 15, 2021 March Madness began with Mortgage madness, in line with 2021. College Basketball fans came to a boil last week when the Michigan Spartans briefly rebranded to a longer name, MSU Spartans Presented by Rocket Mortgage.

March Madness began with Mortgage madness, in line with 2021. College Basketball fans came to a boil last week when the Michigan Spartans briefly rebranded to a longer name, MSU Spartans Presented by Rocket Mortgage.

Fans immediately took to Twitter to complain, as competitors imagined if their beloved teams were also suddenly named after fintech companies. Shortly after, Michigan released a statement claiming they would not be changing their name:

STATEMENT FROM MSU ATHLETICS (MARCH 12):

Michigan State is not renaming its men’s basketball team. While this is a new extension of the partnership for Rocket Mortgage with Men’s Basketball, this is not a first-of-its-kind sponsorship for the Spartans or a new concept in professional or collegiate team partnerships.

Though as some users and news media pointed out, the suffix will still be attached to the team name everywhere at its home games: the rollback is semantics, Rocket Mortgage will still be included in the name, and the logo will appear across the stadium.

“Michigan State University is very important to our company. It is the alma mater of our Founder and Chairman Dan Gilbert, me, and many team members throughout our organization,” Rocket CEO Jay Farner said. “We are honored to contribute to the university that has prepared so many of us for success.”

Strapped for cash, the Detroit Free Press reported the Michigan athletic department is projected to lose $75 million due to the COVID-19 pandemic.

Yahoo Sports writer Jack Baer said that when sports teams take on a corporate name, like the New York Red Bulls, “the business in question actually owns the team rather than giving them millions of dollars to slap their name onto a scoreboard and promotions. In that respect, the MSU Spartans Presented by Rocket Mortgage would be something akin to a little league team getting some help from a local business.”

Rocket Co-founder, Dan Gilbert, has previously donated at least $15 Million to Michigan’s athletics program, overhauling the Breslin Center stadium. Now his Rocket Companies logo will appear everywhere throughout the building.

Some fans still poked fun after the school walked back its original announcement.

Bummer. I was looking forward to taking my family to United Wholesale Mortgage Breslin Center to see the MSU Spartans presented by Rocket Mortgage play on the Auto Owners Insurance Tom Izzo court for a game day experience presented by Farm Bureau Insurance.

— Ryan Peterson (@RyanPD_Peterson) March 12, 2021

LoanMe, Liberty Tax Merger to Take on Intuit, Enova

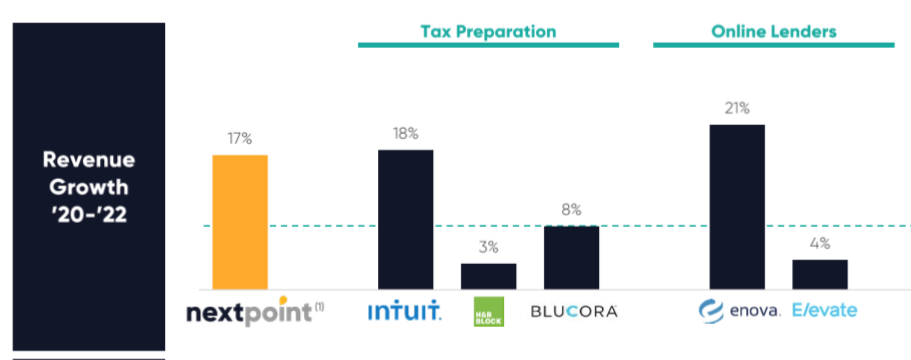

February 22, 2021NextPoint Financial will combine LoanMe’s business, consumer, and mortgage lending with Liberty Tax’s tax preparation business, according to merger announced on Monday. Liberty’s “2,700+ locations in the US and Canada” will become consumer and SMB loan shops.

The new firm will also offer Merchant Cash Advances; LoanMe launched MCA funding in January and expects to fund $15 million in MCAs in 2021. Based on the acquisition prospectus, NextPoint will be a tax readiness firm, with the added suite of financial products as a value and growth builder.

Ramping up consumer, installment, and MCA lending, paired with the third-largest tax-prep business in the U.S, NextPoint expects to compete directly with Intuit, H&R Block, Enova, and Elevate.

Fintech firms are setting themselves apart from the competition as one-stop shops for everything a business needs, including MCA products. Why branch into financial services now? NextPoint found that this year alt lenders have outperformed the S&P500 three times over.

“We are a one-stop financial services destination empowering hardworking and credit-challenged consumers and small businesses,” the investor presentation reads. “To get to the next point in their financial futures.”

Intuit offers a variety of financial products, like business loans through Quickbooks Capital, alongside their popular, 60%+ market share of tax prep software. H&R began offering small $1,000 lines of credit this year, but not much more.

The team leading the new company, NextPoint Financial, will feature execs like Brent Turner as CEO, Mike Piper CFO, both keeping their previous Liberty Tax positions. Jonathan Williams, former president and founding shareholder of LoanMe, will become president of lending.