Student Loans

The Cash Advance of the Student Loan Industry Agrees to Be Treated Like a Loan

August 23, 2021 If you thought only small businesses were selling their future income for cash upfront, then you haven’t been paying attention to the student loan industry.

If you thought only small businesses were selling their future income for cash upfront, then you haven’t been paying attention to the student loan industry.

More than five years ago, fintech companies channeled the MCA concept into student lending. Called an Income Share Agreement, it works just as you would think, the funder advances tuition costs to the student and in return the student pays a fixed percentage of their gross income after graduation, but only if they are gainfully employed. They’re not loans and there’s no penalty if the amount paid back to the funder is less than the amount funded. It is essentially an MCA for college kids.

When deBanked interviewed a student named Paul Laurora about two years ago, Laurora said that in exchange for tuition money, he had agreed to pay 2.57% of his income for 7 years, whether he made a lot, a little, or nothing at all. The funder is making a bet that it will get a considerable return on its investment, but takes the risk of getting nothing if the graduate isn’t working during that time period or earns less than anticipated.

Laurora compared paying that way versus what his friend was faced with, which was to pay $230,000 either with cash or with student loans to attend NYU.

“ISAs” typically enjoy the regulatory benefit of not being a loan, but that could all change.

In California, the state’s Department of Financial Protection and Innovation took issue with a funder’s ISAs when they applied for a Student Loan Servicing license, a requirement in the state. That funder was named Meratas, a New York company that’s headquartered in Connecticut. Meratas’ encounter with the California DFPI resulted in a consent order on August 5th that will have the company’s ISAs treated as student loans and make Meratas an approved Student Loan Servicer.

“[This] action shows we are taking significant steps to better protect California student borrowers,” said DFPI Senior Deputy Commissioner Suzanne Martindale, whose Consumer Financial Protection Division oversees the student loan servicing law. “Regulating income share agreements like student loans levels the playing field and creates a fair marketplace that protects all consumers.”

Though the agreement only applies to Meratas, it could set a precedent for treatment of ISAs in the state.

Meratas celebrated the arrangement as a win.

“Because income share agreements do not fit neatly into existing federal or state legal regimes, we felt it prudent to be proactive at the state level, starting with California,” says Meratas founder and CEO Darius Goldman. “We are excited to work with the DFPI in its efforts to craft ISA-specific regulations for the benefit of all industry participants. Our partners take comfort in knowing that Meratas continues to be the leader in responsible and consumer-friendly ISA programs.”

Upstart Welcomes Policy Head Nat Hoopes

September 15, 2020 Upstart, an AI lending platform, welcomed longtime industry advocate Nat Hoopes to the team this week, to lead as Head of Government Policy and Regulatory affairs. Hoopes previously served as the Marketplace Lending Association executive director (MLA), where he grew the trade group and advocated on behalf of its members.

Upstart, an AI lending platform, welcomed longtime industry advocate Nat Hoopes to the team this week, to lead as Head of Government Policy and Regulatory affairs. Hoopes previously served as the Marketplace Lending Association executive director (MLA), where he grew the trade group and advocated on behalf of its members.

“My hope is to bring the energy that I did in growing the organization [MLA] and also just in tackling a lot of different workstreams to Upstart,” Hoopes said. “But also, deepen their ties with the DC policy community.”

Hoopes is excited to join the Upstart team and advocate for the company to state and federal legislators. Hoopes intends to address the development of two main issues as he enters his new office: facilitating better credit reporting with the help of AI, and using better credit to bring financing options to disenfranchised minority communities.

Upstart uses non-traditional data like a college education, job history, and residency to evaluate borrowers for personal loans. The company recently introduced an AI-powered Credit Decision API to deliver instant credit decisions. Upstart added auto loans to the platform in June, so the new API works with personal, student, and auto loans.

Hoopes said he and Upstart shared a similar motivation: to provide credit to people and improve financial futures, especially to people unfairly blocked from receiving credit.

“I think because of the structural inequality that we have in our society, a lot of minority groups get really left behind and stuck in a low credit score environment,” Hoopes said. “By using more data, and using it in new ways with artificial intelligence we can really level the playing field.”

Hoopes said that he has already seen Federal regulators in the FDIC and the OCC, and the CFPB working on using AI learning in credit underwriting. He said the Fed is planning out how to help banks adopt more of these models to approve more people.

“I think that’s a key initiative,” Hoopes said. “A key area where I’ll be working for Upstart: Engaging with regulators on how to help banks get more comfortable in serving more customers,”

While advocating for banks to use the credit capabilities of partners like Upstart, Hoopes said he would be devoted to ensuring decisions are made with equality and inclusion in mind. Hoopes will stay on as a member of the MLA board, and working in concert with his responsibilities advocating at Upstart.

“At MLA, I helped develop the diversity and inclusion strategies for our part of the fintech industry,” Hoopes said. “I’ll remain active on those issues at Upstart both collectively with other members of the industry as a member of the MLA.”

Hoopes referred to the Diversity and Inclusion strategy released by MLA last month. Board members signed off on the paper, written with the help of the National Urban Leauge. League president and CEO Marc Morial and Representative Gregory Meeks (D-NY) to create a vision of an inclusive fintech industry.

Hoopes addressed what he said was the failure of the American credit scoring system. For instance, according to Upstart’s study in 2019, 80% of Americans have never defaulted, yet only half have a prime credit score. It’s a problem he says disproportionately affects minority borrowers.

According to a Federal Reserve study, more than three times as many Black consumers (53%) and nearly two times as many Hispanic consumers (30%) as White consumers (16%) are in the lowest percentiles of credit scores.

Hoopes said Upstart does not collect racial data from applicants but cites a CFPB test that found Upstart’s platform increased access to credit across race and ethnicity by 23-29% while decreasing annual interest rates by 15%-17%.

New SoFi Stadium To Host Rams, Chargers, Super Bowl & Olympics

September 15, 2019 SoFi’s appetite to reach NFL viewers is going above and beyond just Super Bowl commercials. The fintech company that started with student loan refinancing, has secured the naming rights to a new professional football stadium in Inglewood, California. SoFi Stadium, which opens in 2020, will host both the Rams and the Chargers. The stadium will also be home to Super Bowl 56 in 2022 and will serve as the venue for the opening and closing ceremony of the 2028 Summer Olympics.

SoFi’s appetite to reach NFL viewers is going above and beyond just Super Bowl commercials. The fintech company that started with student loan refinancing, has secured the naming rights to a new professional football stadium in Inglewood, California. SoFi Stadium, which opens in 2020, will host both the Rams and the Chargers. The stadium will also be home to Super Bowl 56 in 2022 and will serve as the venue for the opening and closing ceremony of the 2028 Summer Olympics.

Anthony Noto, SoFi’s CEO, served as CFO of the NFL for almost 3 years from 2008 – 2010.

In an interview with CNBC, Noto explained that the naming rights are more than just people coming to a game and seeing their brand there and that it will also give them a TV broadcast platform for all types of events the stadium hosts. It’s the ultimate advertising campaign, which the company believes they need to market their new products such as SoFi Money.

“Now that we have a complete suite of financial services […] we have to build awareness of those products, which requires us also to build trust, so being part of this iconic destination, allows us to elevate and accelerate how quickly we can get there,” Noto said.

The move could be perceived as too flashy or premature given how young and new SoFi is, but Noto says that the naming rights only make up about 10% of their marketing budget.

A single night of football, they estimate, would put them in front of 10-15 million unique potential customers, equal to all of their other total sponsorships they’ve done combined.

LA Rams Chief Operating Officer Kevin Demoff said during a separate CNBC interview, “I think when you look at someone like Anthony Noto, who was in part of the NFL, who understands the allure of football and what it brings to people on sundays, and throughout the nation and helps bring people together, but also right there the entertainment factor when you think about what can happen, on this field right below, I think it’s something that gives everybody a point of pride.”

Forgiving the Unforgivable: Democrats Propose Wide Range of Solutions for Student Debt

July 1, 2019 To forgive or not to forgive? That is the question as Democratic presidential candidate hopefuls line up to state whether or not they are still repaying their student loans (and if this repayment reaches six figures) and what their intentions for the student loan crisis are, leading to the $1.6 trillion debt becoming one of the central issues of this race.

To forgive or not to forgive? That is the question as Democratic presidential candidate hopefuls line up to state whether or not they are still repaying their student loans (and if this repayment reaches six figures) and what their intentions for the student loan crisis are, leading to the $1.6 trillion debt becoming one of the central issues of this race.

With calls coming forward from all corners of the Democratic Party, voters are seeing a wide range of options for how to tackle what has been hailed as the potential cause of the next financial crash, the only thing is, not everyone is clear about how they intend to pay for it.

Last week Bernie Sanders surprised many with his calls to forgive all student debt. Prior to this, Elizabeth Warren announced that she planned to cancel debt “for more than 95%” of those burdened with loan debt. And while these candidates have led the charge of progressive arguments for how to deal with the debt crisis, the popularity of their proposed policies has baited other Democrats to follow suit.

Joe Biden, who remains the frontrunner despite criticisms of his performance in the first debate, has said that he wants to forgive teachers’ student loans. South Bend Mayor Pete Buttigieg wants to solve the problem by offering free college to those coming from lower-income and middle-class backgrounds, saying in the debate that he does not “believe it makes sense to ask working-class families to subsidize even the children of billionaires.” Robert O’Rourke has suggested cancelling the debt of those who work in fields or areas where there is a low supply of labor. Kamala Harris has called for debtless tuition and lower interest rates on existing loans. And Eric Swalwell, the Californian congressman, has proposed forgiving debt in exchange for engaging in work-study programs and community service while at college.

The means by which each of these proposals will be paid for has varied from candidate to candidate, with some offering detailed plans, and others, verbal assurances. Both Warren and Sanders have published how they will raise funds for their strategies, with the former stating that she will impose a 2% tax on Americans with $50 million or more in wealth, and the latter proposing a tax on Wall Street speculators that he claims will raise $2.4 trillion over a ten-year period. Meanwhile, other candidates have yet to clarify how their solutions will be financed; and these announcements are being made just as the Congressional Budget Office’s most recent evaluation of the 2017 Republican-backed tax cut has estimated the net cost of the cuts to come to $1.9 trillion – $3 trillion more than the total sum of student debt.

The conversation generated from these announcements has spilled out beyond debates and candidate interviews, as non-political figures such as Mark Cuban, Jamie Dimon, and Gary Vaynerchuk have each contributed their two cents. The last of these has explained that he sees the next generation of Americans as the ones who will “walk away” from colleges as they are known now; Dimon has gone on record in his annual letter to JPMorgan Chase shareholders to call the crisis a “disgrace” that is “hurting America”; and Cuban has partnered with ChangEd, a program that seeks to assist students in paying off their debts, as part of an event to help high school and college students learn more about their future finances.

Interactions like these, between popular figures and the hot topic that student debt has become, are increasing in frequency, and as the Democratic primaries run on it is likely this trend will continue. However, it is too early to say which side of Dems will win, pro-forgiveness or a lighter, less dramatic form of relief for students.

With reports indicating the extent to which student loans affect the 45 million indebted Americans who took them out, it appears that this will be one of the major issues to shape the primary and presidential races. Stories of graduates sacrificing opportunities to marry, have children, buy a home, and even continue careers in the fields they studied beg the question of what exactly the benefit of college is. The next year will demonstrate whether Democrats are able to drum up an answer.

College Students Abandon Student Loans, Offer Share Of Their Future Income Instead

April 29, 2019 At Purdue University, home of the Boilermakers, there’s a brick bell tower that stands high above everything else on this handsome campus of stately college buildings and green lawns. Paul Laurora, a senior Chemical Engineering student, said the bell rings on the hour and at 20 minute intervals throughout the day, as that’s when classes begin and end. And at 5 p.m., the bell rings out the melody of Purdue’s school song, “Hail Purdue.” That’s a lot of bell ringing. Laurora is a fraternity member, he lives with seven other roommates in a house on campus and he really likes film. He’s also a part of Purdue’s “Back a Boiler” Income Share Agreement (ISA) program, which is an alternative to a student loan. An ISA is an arrangement where college students pay a percentage of their future earnings to the college and other investors.

At Purdue University, home of the Boilermakers, there’s a brick bell tower that stands high above everything else on this handsome campus of stately college buildings and green lawns. Paul Laurora, a senior Chemical Engineering student, said the bell rings on the hour and at 20 minute intervals throughout the day, as that’s when classes begin and end. And at 5 p.m., the bell rings out the melody of Purdue’s school song, “Hail Purdue.” That’s a lot of bell ringing. Laurora is a fraternity member, he lives with seven other roommates in a house on campus and he really likes film. He’s also a part of Purdue’s “Back a Boiler” Income Share Agreement (ISA) program, which is an alternative to a student loan. An ISA is an arrangement where college students pay a percentage of their future earnings to the college and other investors.

Laurora was introduced to the ISA program by Purdue. It launched in 2016 and was the first of its kind. He said he signed up for it because he was denied student loans by banks and because he said the ISA is more transparent and easier to obtain.

Laurora was introduced to the ISA program by Purdue. It launched in 2016 and was the first of its kind. He said he signed up for it because he was denied student loans by banks and because he said the ISA is more transparent and easier to obtain.

“If I hadn’t gotten the ‘Back a Boiler’ ISA, I would have had to take a semester off to work to contribute to my tuition,” Laurora said.

Purdue’s ISA program works such that the percentage of a student’s future earnings that go to repaying the advance is based on the amount of money they are likely to make given their major. But the math works out such that all graduates are expected to pay roughly the same minimum amount. The graduates are given six months to find employment and then the clock starts ticking, like the one inside the campus bell tower.

As a senior, Laurora has been on an active job search. Earlier last week, he said he wasn’t too concerned about paying off his ISA, but he said it was definitely a factor when considering different jobs and their salaries. Last Friday, Laurora got a job offer from a Washington, D.C. firm to be an Engineering Technology Analyst, and he feels comfortable that he’ll earn enough money for himself while still being able to give a percentage of his salary to the ISA.

For Laurora, he is required to give 2.57% of his income for a little more than 7 years. What Laurora and other students find attractive about Purdue’s ISA Program is that, like all ISA programs, there is a time cap (usually 10 years) after which the graduate no longer owes money. The program simply concludes.

Florin Handelman is a junior at Purdue who wanted to go there because of its prestigious engineering program. He ended up switching his intended major to Industrial Design, which he’s very passionate about. He’s even part of a student club where upperclassmen mentor underclassmen in industrial design.

Florin Handelman is a junior at Purdue who wanted to go there because of its prestigious engineering program. He ended up switching his intended major to Industrial Design, which he’s very passionate about. He’s even part of a student club where upperclassmen mentor underclassmen in industrial design.

Handelman also has an ISA, which he said he really likes because of the time cap. But he noted a potential downside – which is that if you end up making far more than what Purdue anticipated, you still pay the same percentage on your income, which could end up being a lot more than a fixed-rate student loan. He conceded, though, that earning far more than expected is “an ok problem to have.” For extremely high earners, Purdue has a cap so that no one pays more than 2.5 times the principal amount they were given.

Handelman said that none of his friends have an ISA and that, unless you’re applying for financial aid, “no one really knows about it.”

Since 2016, Purdue’s “Back a Boiler” program has served over 500 students with 820 contracts for a total amount of almost $10 million, according to Tim Doty, Director of Public Information and Issues Management at Purdue. Last year’s freshman undergraduate class had more than 8,000 students, so 500 in the ISA program altogether is still a very small number. But the program has been growing steadily. And in the time since Purdue launched the first ISA program, there are now about 25 other ISA programs at institutions of higher education in the U.S., according to Charles Trafton, co-founder of Edly, a new online marketplace that connects ISA investors.

Since 2016, Purdue’s “Back a Boiler” program has served over 500 students with 820 contracts for a total amount of almost $10 million, according to Tim Doty, Director of Public Information and Issues Management at Purdue. Last year’s freshman undergraduate class had more than 8,000 students, so 500 in the ISA program altogether is still a very small number. But the program has been growing steadily. And in the time since Purdue launched the first ISA program, there are now about 25 other ISA programs at institutions of higher education in the U.S., according to Charles Trafton, co-founder of Edly, a new online marketplace that connects ISA investors.

Purdue is a public school, so tuition is less expensive in general, particularly for in-state students. For the 2018-19 academic year, tuition for in-state students was $9,992 a year and $28,794 a year for out-of-state students.

“College is ridiculously priced in general,” said Laurora, who is an out-of-state student from New Jersey. “I have a friend who’s paying $80,000 a year at NYU.”

Savanna Williams is an in-state junior and an Elementary Education major at Purdue. She’s also a member of a sorority and is an officer in a student run dance club. One thing Williams said she likes about the ISA program is that if she wants to start a family and not work for a few years, she wouldn’t owe money then. With Purdue’s program, a graduate can take off time and not pay for up to five years. But the ISA payment term is then extended for however long a period that the graduate stopped working.

Given their shared experience and future commitments, students in Purdue’s ISA program are kind of like members of a club. When Laurora was at Harry’s Chocolate Shop, a popular bar near campus, he ran into someone he knew who was in the program.

“We said hi and both agreed it was helpful.”

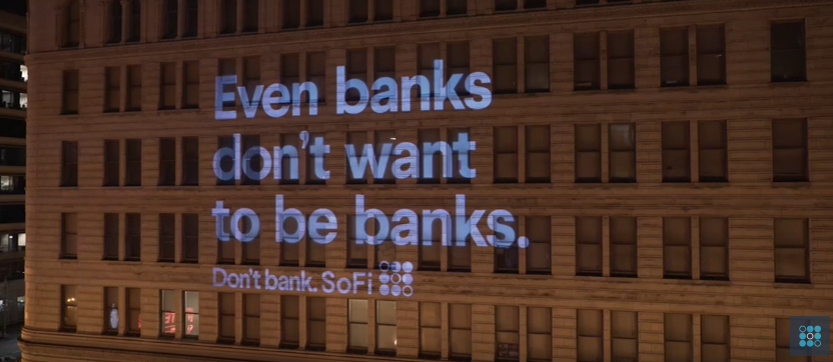

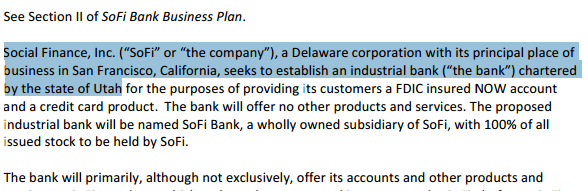

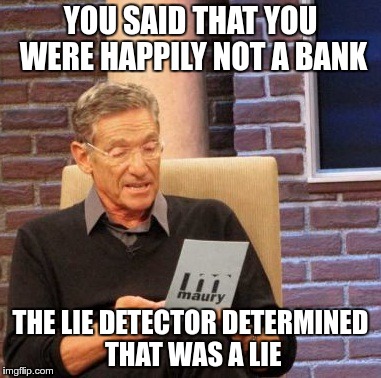

That Awkward Moment in Alternative Lending When…

June 13, 2017That awkward moment when you apply for a bank charter (::cough:: SoFi ::cough::) and you realize your company’s motto has literally been #dontbank all along…

Just, don't do it. #DontBank pic.twitter.com/lnxKJHH3QJ

— SoFi (@SoFi) February 11, 2016

Banks send you statements. Our statement is we don’t like banks. Check us out at https://t.co/B5YXtHWKL0. #DontBank pic.twitter.com/RshfsAhdYR

— SoFi (@SoFi) January 26, 2016

Happily not a bank. http://t.co/bDN6i1Fd5W #SoFiSoFun

— SoFi (@SoFi) August 25, 2015

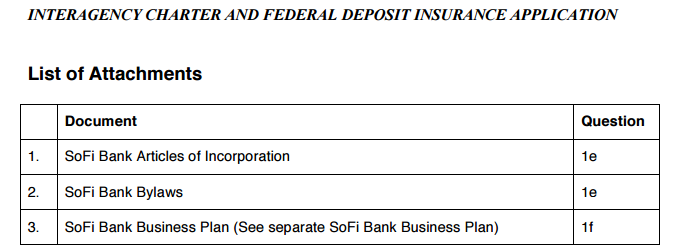

You can view the full bank charter application of the anti-bank whose slogan was #dontbank, here. You can also read an article about it on TechCrunch.

The Tesla of Alternative Lending

May 16, 2017 Tesla has autopilot. Apple has Siri. And Upstart has its own high-tech software model that places the startup in a category of its own for online lending. All three of these companies may be very different but what they have in common is a reliance on artificial intelligence and machine learning for their proprietary technology.

Tesla has autopilot. Apple has Siri. And Upstart has its own high-tech software model that places the startup in a category of its own for online lending. All three of these companies may be very different but what they have in common is a reliance on artificial intelligence and machine learning for their proprietary technology.

“You hear so much about how Tesla cars will drive themselves, how Google or Amazon home assistants talk to you to as if you’re human. In lending we are the first company to apply these types of technologies to lending,” Dave Girouard, Upstart co-founder and CEO told deBanked.

So what is machine learning exactly, particularly as it relates to finance? One of the main components that goes into machine learning is not looking at the same data everybody else does. “We are known for looking beyond FICO and the credit report. We look at who the employer is, what industry you work in, where you went to college, what you studied, several hundred variables affect how we price credit,” he said.

Upstart, a direct-to-consumer lending platform, uses artificial intelligence and machine learning for everything from verifying a potential borrower’s identity, to making a credit decision, to pricing credit. Today 25 percent of the company’s loans are 100% automated.

“This is a radical departure from the industry,” said Girouard. “It’s a function of being able to build more automation to verify information about the borrower.”

Indeed the differences between machine learning and traditional credit models is kind of like comparing a self-driving vehicle to walking.

“The whole term machine learning implies that software gets smarter and better on its own with no human intervention. Every day thousands of repayments are made to Upstart along with delinquencies, and defaults. As this happens the software is adjusting its pricing on the next loan, learning in real time every day,” Girouard said, without even the slightest concern of tipping his hand.

“We have a several year head start and a data science team that are math and statistics PhDs. These are the types of people hired by Google or Tesla or Amazon. Traditional consumer credit doesn’t tend to have machine learning skills,” he added.

Nevertheless his vision for artificial intelligence and machine learning in the lending community is far greater than as it applies to Upstart alone. “We think virtually all flavors of lending will depend on AI/ML within 10 years. We’re at the very early stages, but it’s hard to imagine a successful lender anywhere who doesn’t use similar technology over time,” Girouard said.

Inside Upstart

Upstart is a hybrid lender that funds 20% of loans from their balance sheet. Two months ago they began licensing software as a service (SaaS). The software is managed by Upstart but it appears on the partner’s website. “A bank could use our technology to originate loans,” said Girouard, adding that the company is in conversations with two-to-three dozen banks about future partnerships.

The machine learning approach seems to lend itself to favoring certain demographics. In the case of Upstart, this happens to be millennials, evidenced by the lender’s average customer age of 28, almost all of whom have college degrees.

“Obviously we understood early that the millennial generation doesn’t have 20 years of credit history and they have a hard time getting loans. It struck us, tell me you wouldn’t give a loan to a 25 year old just because they have a thin credit file? It doesn’t make sense. What if they studied at Stanford and work at Google? There is more to be known about an individual than a FICO score,” said Girouard.

Perhaps the greatest evidence of whether or not Upstart’s approach is working is to catch a glimpse of the company’s balance sheet. Upstart expects to reach the $1 billion milestone for loan originations in calendar 2017. And perhaps even more telling is they anticipate being profitable by the summer. “An IPO for us would be a couple of years out,” Girouard said.

That timing could be perfect, particularly considering Wall Street’s apparent love/hate relationship with some players in the alternative lending space.

“People tend to paint the whole industry with one brush and it’s not a very pretty brush at the moment. But soon they will begin to appreciate there is a significant difference between these companies. Upstart really does have a very differentiated and unique product,” said Girouard.

Does SoFi Want $500 Million for Global Expansion?

September 8, 2016Online lender SoFi is looking to raise $500 million in equity capital to fund new projects and possibly expand to international markets.

The San Francisco-based lender is in talks with investors and maybe just weeks away from finalizing the deal, according to The Wall Street Journal. If the deal goes through, it might be one of the biggest fintech deals of the year, said the report.

SoFi has had an eventful year so far, to say the least. Led by ex-Wells Fargo executive Mike Cagney, the company laid plans in the beginning of the year to start a dating app to appease millennial borrowers, started a hedge fund to buy loans, made a bunch cheeky, controversial commercials, appointed Deutsche Bank’s ex CEO Anshu Jain to its board, made unusual hires, funded $1 billion in student loans and got knee deep in mortgages. SoFi’s strategy since inception has been to stay relevant for its borrowers at every stage of their lives, starting with student loans, personal loans, all the way through to a mortgage.

One of the fastest growing private lending companies, SoFi’s backers include marquee investors like Peter Thiel, Prosper Loans’ President Ron Suber, Discovery Capital, Softbank and Morgan Stanley.