Regulation

CFPB’s New Arbitration Rule Does Not Apply to Business Loans

July 10, 2017The CFPB’s new rule to regulate arbitration clauses in consumer finance contracts does not apply to business loans, according to the agency’s fine print. Page 403 of 775 (that’s how long the rule is) includes a footnote that says:

As is explained in proposed comment 3(a)(1)(i)-1, Regulation B defines “credit” by reference to persons who meet the definition of “creditor” in Regulation B. Persons who do not regularly participate in credit decisions in the ordinary course of business, for example, are not creditors as defined by Regulation B. 12 CFR 1002.2(l). In addition, by proposing to cover only credit that is “consumer credit” under Regulation B, the Bureau was making clear that the proposal would not have applied to business loans.

Watch the video on what the CFPB’s rule is about below:

CFPB Pushes Back Small Business Lending Comment Deadline

July 7, 2017The CFPB has pushed back its small business lending comment deadline from July 14th to September 14th. The Request for Information is the first step of its initiative to monitor business loans to women and minorities, as directed by Section 1071 of Dodd-Frank.

Only 15 comments have been submitted so far, a number likely too small to even be helpful to the CFPB. Nonetheless, the comments have been overwhelmingly negative with respondents mostly asking to be exempt from the law or to repeal it.

The Director of Business Lending at a credit union for example, said that the law “puts our staff in the unenviable and unfair position of making an assessment of a borrower’s ethnicity when this information is not provided as if often the choice.” Between that and the cost burden of compliance, he also said his credit union is seriously considering the discontinuance of all small business lending going forward.

The total and complete discontinuance of small business lending is probably not what legislators wanted when they wrote the law.

Prior to that, the Puerto Rico Bankers Association questioned the value of spending big bucks to collect data on minorities when 99% of Puerto Rico’s residents are legally classified as minorities. “The potential complexity and cost of compliance with the minority-owned businesses data collection and reporting requirements of Section 704(B), will impose on our banks an unintended and unreasonable burden,” they said in their public comment.

All Companies Can Now Submit Draft IPO Registrations Confidentially

June 29, 2017 There’s a reason the public never got to view BFS Capital’s September 2015 IPO registration documents. Thanks to the JOBS Act, “an emerging growth company may confidentially submit to the Commission a draft registration statement for confidential, non-public review by the Commission staff prior to public filing.” They can then choose to abandon the offering altogether without having to suffer the fate of their financial statements being made public, which is what BFS Capital did. But if they ultimately had chosen to move forward, their documents would’ve been shared in the public domain.

There’s a reason the public never got to view BFS Capital’s September 2015 IPO registration documents. Thanks to the JOBS Act, “an emerging growth company may confidentially submit to the Commission a draft registration statement for confidential, non-public review by the Commission staff prior to public filing.” They can then choose to abandon the offering altogether without having to suffer the fate of their financial statements being made public, which is what BFS Capital did. But if they ultimately had chosen to move forward, their documents would’ve been shared in the public domain.

A new decision handed down by the SEC is now expanding that privilege beyond “emerging growth companies” to all companies. That means that any company can submit draft documents confidentially. It will take effect on July 10th.

“This is an important step in our efforts to foster capital formation, provide investment opportunities, and protect investors,” said Director of the Division of Corporation Finance, Bill Hinman. “This process makes it easier for more companies to enter and participate in our public company disclosure-based system.”

The only reason BFS Capital’s confidential filing is known, is because the company broadcasted that they had filed accordingly in a press release.

“By expanding a popular JOBS Act benefit to all companies, we hope that the next American success story will look to our public markets when they need access to affordable capital,” said Chairman Jay Clayton. “We are striving for efficiency in our processes to encourage more companies to consider going public, which can result in more choices for investors, job creation, and a stronger U.S. economy.”

It is possible that other companies in the industry have filed draft registration statements, got discouraging feedback from the SEC and then decided to withdraw without any of their competitors being the wiser.

SoFi Bank Puts ILC Charter in Spotlight

June 28, 2017

Online lender SoFi’s decision to apply for a bank charter has snagged the attention of alternative lenders, big and small banks and regulators alike. Market participants appear split between cheering the move and drawing a line in the sand. One thing they agree on is that the signs were there all along.

Christopher Cole, executive vice president and senior regulatory counsel at the Independent Community Bankers of America (ICBA) said it was only a matter of time.

“We were expecting the application from a fintech company to come eventually and it came pretty rapidly,” Cole told deBanked. “What was surprising to me was that they took the ILC route as opposed to the OCC special purpose national bank charter.”

As a Utah-chartered industrial bank SoFi would be subject to the regulation of the FDIC. There have not been any ILC applications for deposit insurance in years in part due to a temporary moratorium that Dodd Frank placed on the ILC loophole following the financial crisis, a roadblock that has since been removed.

Richard Hunt, president and CEO of the Consumer Bankers Association (CBA), said that SoFi’s application was certainly not a shock.

“The whole world is evolving, fintech is evolving. This was inevitable one way or another,” Hunt told deBanked, adding that there will probably be more applications coming down the pike, which he welcomes. “We’re glad more people are getting into banking. SoFi at one time railed against banks and now it wants to get into banking. Welcome to the world of banks and overregulation.”

The CBA is comprised of the country’s largest financial institutions as well as regional banks.

“This is the first true test of the FDIC in a new fintech world,” said Hunt, adding that it’s the duty of the FDIC to ensure that SoFi Bank is well capitalized. “That is part of the application process.”

The ICBA is comprised of approximately 6,000 small banks across $5 trillion in assets.

“This would actually create a risk to the deposit insurance system. An ILC would have deposit insurance from the FDIC. If SoFi Bank fails because parent SoFi can’t maintain it, the rest of the banking system must pay for it. They’re putting the banking industry at risk here,” said Cole.

And while the rise of fintech startups has created more competition for banks, neither trade organization has a problem with this.

“We’re not trying to keep fintech from competing, that’s not the case,” said Cole.

Meanwhile Hunt told of his trip to Silicon Valley in which he visited SoFi as well as many other fintech startups.

“I’ve always been a big fan of SoFi, especially after visiting. I’m head over heels they chose banking as their industry. We’re gloating that they want to join the banking industry. This is good for consumers, to have choices. We are not going to be afraid of SoFi joining the banking world. We welcome them to the banking world,” said Hunt, adding that banks are ready to compete as long as it’s fair.

Fair is precisely what the ICBA is seeking.

Level Playing Field

There are about 30 existing ILCs in existence now and thousands of insured banks. And SoFi’s use of the ILC charter is the ICBA’s main objection.

“It’s the fact that they’re using this loophole so that SoFi, the parent company of SoFi Bank the subsidiary, will not be subject to the same kind of restrictions that the owner of a commercial bank would. And therefore, you don’t have a level playing field,” said Cole.

The ICBA is also concerned that a successful SoFi ILC charter would set a precedent for other fintech firms.

“Who’s next? I could see Amazon trying to do this and waiting for SoFi to do it first. Who knows? I could see maybe Google and PayPal pursuing this. I could see some big commercial companies exploiting this loophole, and that is why we think it should be closed,” said Cole.

Meanwhile CBA’s Hunt sees things somewhat differently. He said SoFi’s application represents an opportunity for bank regulators to review the ILC in a new world environment and possibly make changes.

“No one envisioned when they wrote the ILC charter that we would have fintech companies that finance mortgages and student loans from private equity capital and not deposits. It’s a new world. Like with all rules and regulations, federal regulators should periodically review longstanding policy,” Hunt said.

Either way the influence of the banking sector should not be overlooked.

“We have been fighting the ILC charter for over a decade. When Walmart tried to apply for an ILC charter in 2006 we objected at that point. And that resistance was part of the reason why they never got a charter,” said Cole.

SoFi Bank

SoFi Bank

The ICBA is preparing commentary for the FDIC, which is due by July 18. “Our comments will be focused mostly on the use of the ILC charter,” said Cole.

Once the comments are in, the ball is in the FDIC’s court. “We’re anticipating that a decision will be made in the next two to three months. We should know by the end of this year whether or not SoFi Bank gets its charter and deposit insurance,” said Cole.

If SoFi does become a bank, Hunt says he’s pleased that the fintech company has expanded its lending beyond only the elite universities though he’s still not sure they’ve gone far enough. “If they are granted the ILC charter, every student should have fair access to SoFi’s products just as they do with every other bank in this country,” said Hunt.

SoFi declined to comment for this story.

Puerto Rico Bankers Association Calls Section 1071 Absurd and Unreasonable

June 28, 2017Section 1071, the law that grants the CFPB authority to collect loan application data on minority and women-owned businesses, is under fire, again. This time it’s the Puerto Rico Bankers Association in response to the CFPB’s RFI on the matter. In a letter, the PRBA points out the sheer irony of conducting costly disparate impact studies on minorities in minority-only communities.

An excerpt from their statement:

According to the 2010 US Census Bureau, 99% of the population of Puerto Rico is Hispanic.

[…]

The direct and evident effect of Section 704B of ECOA for the financial institutions in Puerto Rico will inevitably be the collection, recordkeeping and reporting of virtually all commercial loan applications received within the Puerto Rico marketplace, since most of such applicants would be regarded as “Minority Owned Business”, in accordance with Section 704B.

The PRBA believes that this absurd and unreasonable result must not have been intended by Congress when it enacted Section 1071 of the Dodd-Frank Act. The data so collected, maintained and reported will not serve the purposes for with Section 1071 was enacted since, for the reasons set forth above, it will be completely inaccurate and unreliable. The potential complexity and cost of compliance with the minority-owned businesses data collection and reporting requirements of Section 704(B), will impose on our banks an unintended and unreasonable burden.

Other responses to the CFPB’s RFI have so far called Section 1071, “literally impossible to comply with” and a duplicated effort.

Congressman Emanuel Cleaver, II Makes Inquiry Into Merchant Cash Advances

June 26, 2017 A US Congressman from the fifth district of Missouri is conducting an inquiry into “Fintech Lending,” according to a statement posted online. Rep. Emanuel Cleaver, II published letters that his office sent out last week to five companies seeking information on how they avoid discriminatory lending practices in small business lending.

A US Congressman from the fifth district of Missouri is conducting an inquiry into “Fintech Lending,” according to a statement posted online. Rep. Emanuel Cleaver, II published letters that his office sent out last week to five companies seeking information on how they avoid discriminatory lending practices in small business lending.

An excerpt:

I have recently launched a review into FinTech small business lending. I am particularly interested in payday loans for small businesses, also known as “merchant cash advance.” The payday loan industry has often targeted communities of color with high rates and fees, and Congress needs further information that small business payday lending is operating with transparency and free of discrimination

Ironically, two of the five recipients, Prosper and LendUp, don’t even operate in the small business space, so how exactly they were selected remains a mystery.

Only two of the five companies have any connection to merchant cash advances, but the Congressman’s connection between them and payday loans is perplexing nonetheless.

The subject matter at hand, however, is similar to another fact-finding endeavor that the Consumer Financial Protection Bureau is conducting as part of its mandate under Dodd-Frank.

A response is not required but the Congressman asked the recipients to respond by August 10th.

US Treasury Calls for Section 1071 to Be Repealed

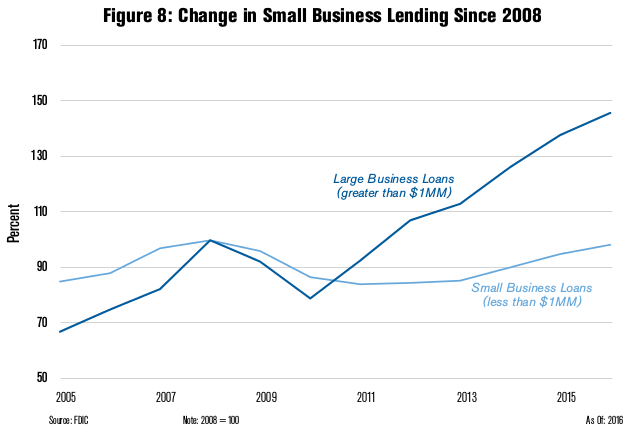

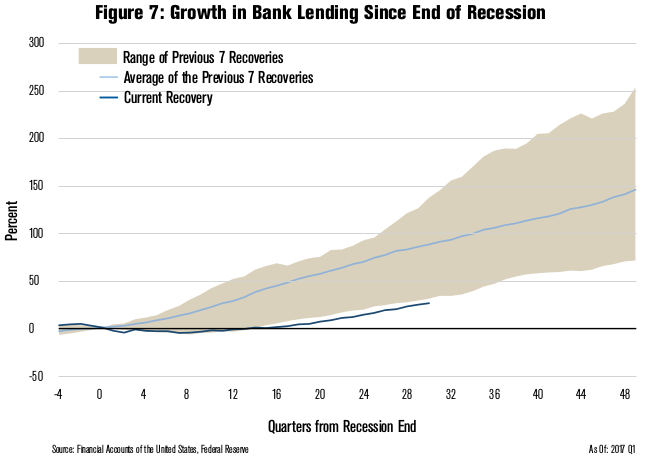

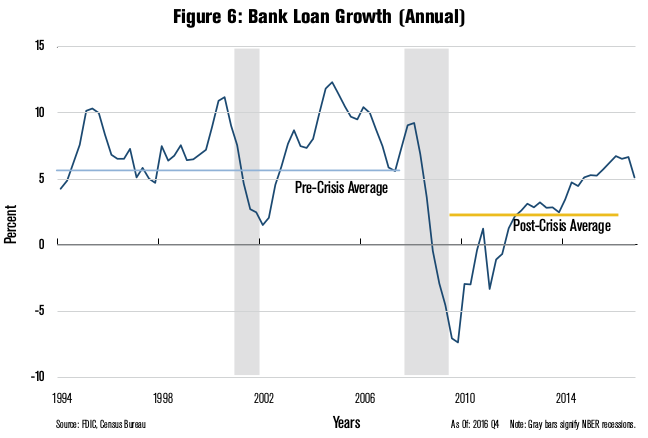

June 19, 2017In a 149-page report prepared for President Trump, the US Treasury has called for the repeal of Section 1071 of Dodd-Frank. Section 1071 is the governing law behind the CFPB’s jump into small business lending data collection. Citing the cost of data collection and anemic small business loan growth since 2008, the Treasury says, “Although financial institutions are not currently required to gather such information [required by the law], many lenders have expressed concern that this requirement will be costly to implement, will directly contribute to higher small business borrowing costs, and reduce access to small business loans.”

“THE PROVISIONS IN THIS SECTION OF DODD-FRANK PERTAINING TO SMALL BUSINESSES SHOULD BE REPEALED TO ENSURE THAT THE INTENDED BENEFITS DO NOT INADVERTENTLY REDUCE THE ABILITY OF SMALL BUSINESSES TO ACCESS CREDIT AT A REASONABLE COST” – US Treasury

The current deadline to reply to the CFPB’s Request For Information is July 14th though industry sources expect the deadline will be pushed back. Of course, if Section 1071 were successfully repealed, the RFI would be moot.

The Choice Act, a bill that just passed the House of Representatives, does indeed repeal Section 1071, but industry sources following the legislation believe the bill will die in the Senate.

Even if a repeal never happens, it is possible that regulations pursuant to Section 1071 may not even go into effect until the early 2020s if similar rulemaking trajectories are to be used as a guide. With payday lending, for example, the CFPB RFI on the matter ended in early 2012 but to-date there still has been no final rule.

New York State Assembly Proposes Online Lending Task Force

June 5, 2017On June 2nd, the New York Assembly drafted its answer to the recent joint-committee hearing on online lending. It’s called Bill A8260, an ACT to establish a task force on online lending institutions. As it’s proposed now, the task force would include individuals from the online lending community, the small business community, the financial services industry, and the consumer protection community that would be appointed by the Assembly, Senate and Governor.

The task force would be required to present a report on the following by April 15, 2018:

(a) an analysis of data received by the department of financial services on the prevalence of these institutions in the state, specifically, how many online lenders are lending to consumers and small businesses in this state;

(b) an analysis of data received by the attorney general and division of consumer affairs regarding the number of complaints, actions and investigations related to online lending institutions;

(c) an examination of the online lending industry and the key participants therein, and an investigation and understanding of the differences in small business and consumer borrowers, lenders and markets, such as the history, business models and practices of online lending institutions including identification of interest rates charged by online lenders;

(d) an examination of how consumers are utilizing online consumer credit to manage existing debt, potentially reduce borrowing costs or access needed funds;

(e) an examination of the existing small business credit gap and small business’ use of credit and credit needs;

(f) identification of alternatives for consumers and small businesses who are unable to access traditional financing and whether new technologies can enhance access to credit;

(g) an examination of whether existing federal and state laws already provide appropriate police powers and regulation of small business and consumer lending by online lending institutions;

(h) an evaluation of the impact of any contemplated or proposed law or regulation on the small business credit gap, including a quantitative analysis of the amount of increased or decreased credit available to small businesses as a result of such law or regulation, including the extent to which access to credit would be affected under the state’s current usury laws;

(i) an analysis of the potential interaction of federal law with any contemplated or proposed state regulation;

(j) an exploration of options for multi-state collaboration to harmonize the laws and regulations of various states related to small business and consumer lending across state borders;

(k) an assessment of best practices for small business and consumer loan disclosures, including current online lending industry efforts to advanced standardized and clear information for borrowers;

(l) an assessment of whether consumer loans and small business loans are treated differently by online lending institutions and if any level of oversight should take such differences into consideration;

(m) an identification of what consumer protections exist to protect consumers in this state from predatory practices of online lending institutions; and

(n) a determination of what new measures, if any, are needed to ensure consumers are protected from deceptive or predatory lending without unduly restricting access to credit.

Once the report is delivered, the task force would be disbanded. The bill is currently in committee.