Regulation

Earnin, Say What’s Your Price? Nas-backed Earnin Comes Under Investigation

September 17, 2019 Earnin, the self-proclaimed alternative to payday loans, is part of a new online lending category that is under investigation in eleven states and Puerto Rico for its similarities to payday loans. With such loans being banned in sixteen states, the app-based personal loans company has drawn the attention of various regulators after it was suggested that its lending model potentially shares a similar APR with payday loans.

Earnin, the self-proclaimed alternative to payday loans, is part of a new online lending category that is under investigation in eleven states and Puerto Rico for its similarities to payday loans. With such loans being banned in sixteen states, the app-based personal loans company has drawn the attention of various regulators after it was suggested that its lending model potentially shares a similar APR with payday loans.

Backed by rapper Nas (only as of June and on undisclosed terms), the company came under fire after it was reported that in a meeting its founder and CEO, Ram Palaniappan, discussed hiring a private investigator to look into the past of a New York Post journalist that was writing about them.

Operating under a ‘tipping’ system, Earnin profits from the loans it provides by suggesting that customers give a voluntary tip when repaying their loans. The default amount is $9 per $100 taken, but people have paid up to $14 per $100, this being the limit one can tip.

According to the New York Post, these tips can lead to APRs of over 400% for an individual advance. Uncertainty looms over Earnin’s model as the phrasing of ‘tipping’ confuses whether or not this can be classified as a loan fee. Say what’s your price? Borrowers may not be aware that their tip could put the loan’s cost on par with costly payday loans.

Earnin relies on analytics gathered from customers’ phones, with the company knowing how much users are paid per hour as well as knowing how long they were at work via their location, Earnin can accurately predict incoming wages.

In a company statement, Earnin said that its system “is a brand new model, so we expect, and welcome questions from regulators like the New York Department of Financial Services.” Since this announcement, Earnin no longer suggests a tip to users in New York and Nas has yet to comment on the situation.

Up Next On The New York Legislative Agenda: Funder, Lender, and Broker Licensing

September 10, 2019 New York State Senator James Sanders Jr. has introduced S6688, a commercial financing licensing bill that would require persons or entities engaging in the business of making or soliciting commercial financing products in New York state to obtain a license from the New York Department of Financial Services. The bill covers small business lenders, merchant cash advance companies, factors, and leasing companies for transactions under $500,000.

New York State Senator James Sanders Jr. has introduced S6688, a commercial financing licensing bill that would require persons or entities engaging in the business of making or soliciting commercial financing products in New York state to obtain a license from the New York Department of Financial Services. The bill covers small business lenders, merchant cash advance companies, factors, and leasing companies for transactions under $500,000.

The bill likely won’t see any activity until the New York legislative session resumes in 2020, at which point it could be amended or killed.

As currently drafted, applicants for a license would be subject to a criminal background search and be required to submit their fingerprints for a review by agencies such as the FBI. In addition to paying an application fee, applicants would be required to maintain liquid assets of $50,000.

Sanders, the bill’s sponsor, is the Chairman of the banking committee. You can read the full text of the bill here.

New York’s COJ Restrictions Have Been Signed Into Law

August 30, 2019 Governor Cuomo has signed S6395, the law that outlaws entering a Confession of Judgment in New York against a non-New York debtor.

Governor Cuomo has signed S6395, the law that outlaws entering a Confession of Judgment in New York against a non-New York debtor.

Rich Azzopardi, a senior advisor to the governor, said on social media that the law has “closed a loophole that allowed unscrupulous creditors to use NY courts to penalize out-of-state consumers with no ties to the state.” He congratulated Senators Brad Hoylman and Assembly Member Jeffrey Dinowitz for their work on the bill.

Senator Hoylman tweeted in response that “the entire business model of lenders who exploited New York’s court system and laws to prey on out-of-state small businesses through confessions of judgment was immoral.”

The Confession of Judgment ban is very specific, it prohibits the entering of a COJ in New York against a non-New York party. It does not prevent parties from filing lawsuits in New York. It does not prohibit COJs from being filed in other states. This law is significant because approximately 99% of COJs being utilized in the small business finance industry were being filed in New York regardless of where the debtor resided. That is because the New York Court system is the fastest and most efficient when it comes to entering COJs and securing a judgment.

The bill was drafted in response to a controversial story series published by Bloomberg reporters Zeke Faux and Zachary Mider that alleged abuses were taking place in the New York courts via COJs.

New York’s COJ Bill Has Been Delivered To The Governor

August 28, 2019 New York’s infamous Confession of Judgment bill has finally been delivered to the governor for his signature. Although the legislative process offers flexibility to depart from the statutory timelines (as we have witnessed), the governor now presumably has 10 days or less to sign it. Stay tuned.

New York’s infamous Confession of Judgment bill has finally been delivered to the governor for his signature. Although the legislative process offers flexibility to depart from the statutory timelines (as we have witnessed), the governor now presumably has 10 days or less to sign it. Stay tuned.

The Confession of Judgment ban is very specific, it prohibits the entering of a COJ in New York against a non-New York resident. It does not prevent parties from filing lawsuits in New York. It does not prohibit COJs from being filed in other states. This law is significant because approximately 99% of COJs being utilized in the small business finance industry were being filed in New York regardless of where the debtor resided. That is because the New York Court system is the fastest and most efficient when it comes to entering COJs and securing a judgment.

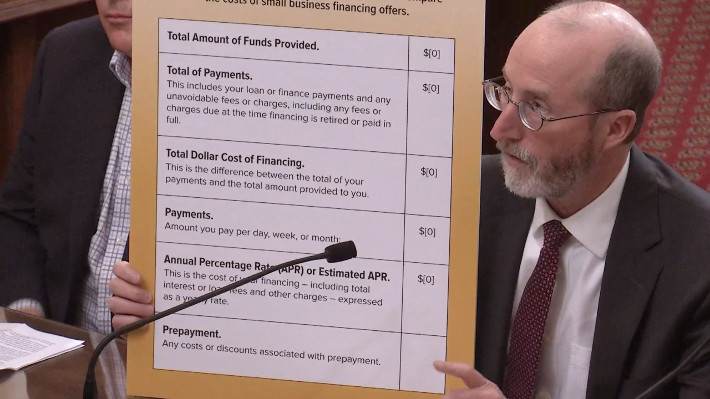

California DBO Making Progress On Finalizing Rules Required By The New Disclosure Law

July 29, 2019 Last October, California Governor Jerry Brown signed a new commercial finance disclosure bill into law. The bill, SB 1235, was a major source of debate in 2018 because of its tricky language to pressure factors and merchant cash advance providers into stating an Annual Percentage Rate on contracts with California businesses. The final version of the bill, however, delegated the final disclosure format requirements to the State’s primary financial regulator, the Department of Business Oversight (DBO).

Last October, California Governor Jerry Brown signed a new commercial finance disclosure bill into law. The bill, SB 1235, was a major source of debate in 2018 because of its tricky language to pressure factors and merchant cash advance providers into stating an Annual Percentage Rate on contracts with California businesses. The final version of the bill, however, delegated the final disclosure format requirements to the State’s primary financial regulator, the Department of Business Oversight (DBO).

The DBO then issued a public invitation to comment on how that format should work. They got 34 responses. Among them were Affirm, ApplePie Capital, Electronic Transactions Association, Commercial Finance Coalition, Fora Financial, Equipment Leasing and Finance Association, Innovative Lending Platform Association, International Factoring Association, Kapitus, OnDeck, PayPal, Rapid Finance, Small Business Finance Association, and Square Capital.

On Friday, the DBO published a draft of its rules along with a public invitation to comment further. The 32-page draft can be downloaded here. The opportunity to comment on this version of the rules ends on Sept 9th.

You can review the comments that companies submitted previously here.

Is The COJ Law In Effect Yet?

July 18, 2019

The COJ bill passed, but where’s the governor’s signature?

When the legislature passes a bill in New York State, there’s a documented procedure on the Senate’s website for how it becomes law. If the legislature is still in session, the governor has only 10 days to sign it. If the passed bill is sent to the governor when the legislature is out of session, the governor has 30 days to sign it.

Caught in this process is S6395, the now-infamous COJ bill that prohibits the filing of a COJ in New York State against a non-New York resident. Its passage on the 18th of June and the closing of the legislative session theoretically put the bill on the 30-day track for the governor’s signature.

Indeed, the Farm Laborers Fair Labor Practices Act, which was debated on the Senate floor for several hours during the closing few days, has already been signed. So too have other bills, but not the COJ bill whose deadline for a signature was perceived to be around now.

But such deadlines are a bit more fluid in practice, legislative insiders say. The act of “delivering” the bill to the governor is a step all on its own and the legislature can actually withhold its formal delivery to avoid setting the clock in motion.

According to an official who’s familiar with the process, it could be months before the dotted line is signed. The official, who asked not to be named, explained that upon the bill being delivered to the governor’s office, only then will Governor Andrew Cuomo have 10 days to sign it. The legislature can also technically withhold delivery up until the very end of the year. This, the official explained, is done to ensure that legislation is thoroughly vetted, with extra checks to guarantee that bills are not unconstitutional and that they’ll lead to no previously unforeseen consequences.

Cuomo has already signed a bill allowing Congress to access Trump’s state tax returns, a bill raising the tobacco & e-cig buying age to 21, a bill guaranteeing women equal pay, and many more. All of which means the COJ bill could be next at any moment or it could be sentenced to signature purgatory until the last business day of 2019.

As the public waits with bated breath, small business finance companies are already planning next steps. Ian Nadjari, the Managing Director of Riverstrong Capital Funding, who said that his office was “not feeling good about [the bill],” is planning to drop their use of COJs entirely and update the terms of their future contracts. Nadjari aims to continue business regardless of the impending changes, he said.

Uplyft Capital CEO Michael Massa, explained that the bill is just a “change that we’ll have to adapt to. Certain players will be okay if they understand how COJs work.”

Several small business funding CEOs explained to deBanked that they welcome S6395 with the belief that it will level the playing field. One asserted that it will “eliminate some of the bad practices in the market,” such as the “offensive, aggressive measures” taken by firms who filed COJs too quickly or potentially in bad faith.

That perception, that such practices are not only possible, but have occurred, has garnered attention far beyond New York State. On June 26, for example, several members of Congress held a hearing to discuss COJs and their impact to further support for a federal bill that would ban them from use nationwide. That bill has a quite a bit a ways to go before it ever potentially even comes up for a floor vote.

Confession of Judgment Bill Still Awaits Governor’s Signature

July 9, 2019 New York State Governor Andrew Cuomo will have only ten days to sign S6395, the bill that prohibits companies from entering Confessions of Judgment in New York against non-New York State debtors, once its delivered to him. Only two possible contingencies could prevent that from happening:

New York State Governor Andrew Cuomo will have only ten days to sign S6395, the bill that prohibits companies from entering Confessions of Judgment in New York against non-New York State debtors, once its delivered to him. Only two possible contingencies could prevent that from happening:

(1) An official veto

(2) a pocket veto

Neither is expected to take place. Reining in the use of COJs was an official part of the Governor’s 2019 justice agenda.

The law only requires that a debtor reside or have a place of business in a New York county and that the judgment only be filed and entered in that county. Whether the filing party is located in New York or Florida or Alaska makes no difference. For a personalized legal analysis, contact an attorney.

The law also only affects a narrow process, the entering of a COJ in New York. It does not prevent parties from filing lawsuits in New York.

As the bill requires the Governor’s signature to become law, the usage of COJs in New York has dwindled but has not disappeared. New York State court records examined by deBanked demonstrate that some companies are continuing to file COJs in New York against out-of-state debtors and that county clerks are continuing to honor them. However, a handful of debtors appear to be challenging previously entered COJs on the basis of S6395’s passage through the state legislature. It remains to be seen how fruitful such defenses might be.

In recent weeks, a number of companies in the small business finance industry have publicly announced that COJs will no longer be required going forward.

You can follow the bill’s path to the Governor’s office here.

This article has been updated to reflect that the deadline rules first require delivery to the Governor

WATCH CAPITOL HILL HEARING LIVE: Crushed by Confessions of Judgement: The Small Business Story

June 26, 2019 The House Committee on Small Business will meet for a hearing titled, “Crushed by Confessions of Judgement: The Small Business Story” today at 11:30am. This hearing is intended to bolster support for The Small Business Lending Fairness Act, a bill to outlaw COJs in small business loans and merchant cash advances nationwide. (Read more about this initiative here)

The House Committee on Small Business will meet for a hearing titled, “Crushed by Confessions of Judgement: The Small Business Story” today at 11:30am. This hearing is intended to bolster support for The Small Business Lending Fairness Act, a bill to outlaw COJs in small business loans and merchant cash advances nationwide. (Read more about this initiative here)

The hearing will be live streamed here when it commences.

The witnesses scheduled to testify include:

Mr. Hosea Harvey

Law Professor and Consumer Finance Law Expert

Philadelphia, PA

Mr. Jerry Bush

Former Owner of JB Plumbing & Heating of Virginia, Inc.

Roanoke, VA

Mr. Shane Heskin

Partner, White and Williams, LLP.

Philadelphia, PA

Mr. Benjamin R. Picker

Shareholder, McCausland Keen + Buckman

Devon, PA