p2p lending

Will Marketplace Lending Revert Back to Peer-to-Peer Lending?

March 28, 2016 Institutional investors wanted higher yields on Prosper’s latest bond offering, an entire five percentage points higher, according to the WSJ. This wasn’t necessarily brought on by performance either. Instead the once voracious appetite for all things online lending is being tempered by uncertainty.

Institutional investors wanted higher yields on Prosper’s latest bond offering, an entire five percentage points higher, according to the WSJ. This wasn’t necessarily brought on by performance either. Instead the once voracious appetite for all things online lending is being tempered by uncertainty.

Bain Capital Ventures partner Matt Harris told the WSJ that online lenders will need to replace the easy hedge fund money by “longer-term capital.” Normally, that would include traditional bank lines and credit facilities, but moving that direction could irreversibly sever the ties with their peer-to-peer roots and image.

Peer-to-peer (p2p) lenders embraced Wall Street’s easy money to scale, rationalizing to the peers on which they were founded that this was all necessary to change the status quo. The road to the sharing economy utopia required hobnobbing with the very institutions they were set on disrupting, they said. The P2p term wasn’t compatible with this narrative so it was replaced with “marketplace lending,” which helped it retain its Silicon Valley feel and gave it the range to argue that hedge funds and peers were virtually the same thing since they were both buyers in a new-age marketplace.

But early this year, something started to happen. Loan originators like SoFi (which was never peer-to-peer) could not sell loans fast enough. One solution they came up with was to launch their own hedge fund to buy their own loans. SoFi CEO Mike Cagney said, “In normal environments, we wouldn’t have brought a deal into the market, but we have to lend. This is the problem with our space.”

But blaming financial institutions for pulling back credit is a scenario that has played out thousands of times in history. One only need watch The Big Short to connect why it’s dangerous for a lender to depend on the institutional credit markets. That’s where the peer-to-peer model was supposed to come in, a new way for a new day without Wall Street to prevent these problems.

But it’s not too late to go back. Lending Club for example, has capped their wholesale channel (the institutional portion) at 50%. They’ve kept more than 100,000 retail investors and intend to grow that even larger. “We’ve always been more exposed to retail, and I think we want to keep it that way,” said Lending Club CEO Renaud Laplanche to the Financial Times. “We’ll probably see that as a competitive advantage, as a source of stability and predictability, particularly in an economic downturn,” he added.

Prosper meanwhile has depended almost entirely on the institutional channel, an astounding 92% of their loans were sold to that category of investors. It’s a far cry from the slogan that appeared on their website back in 2007. “People-to-people lending. It’s an old idea that’s new again,” it said. Today it says, “We connect people looking to borrow money with investors.” Those investors are predominantly Wall Street.

But what to do when Wall Street will one day no longer be interested? It’s not too late to go back in time.

“Borrow money from people just like you,” said Prosper’s website nine years ago. People just like you might not suddenly decide they want five percentage points more. Peer-to-Peer implied a human aspect to the marketplace, that empathy played a role in a world where Wall Street had always been stone cold.

Will the industry revert back to the people? Or will ideas such as starting your own hedge fund to buy your own loans rule the day?

Hedge Funds Will Call The Shots in P2P Lending, Survey Says

March 6, 2016 P2P lending platforms will increasingly rely on larger hedge funds to fund their expansion, The New York Hedge Fund Roundtable believes.

P2P lending platforms will increasingly rely on larger hedge funds to fund their expansion, The New York Hedge Fund Roundtable believes.

The Roundtable is a non-profit organization committed to promoting education and best practices in the hedge fund industry. Timothy P. Selby, the organization’s president, said of a recent study they conducted, that institutional investors can’t afford to ignore Peer-to-Peer (P2P) lending. “Investing in peer to peer loans not only means the promise of high risk-adjusted returns, such private debt investments also provide less correlated risk relative to more traditional fixed income portfolios,” he said.

And as P2P platforms expand and need money, hedge funds feel it is they that will have the leverage in the negotiations.

In a survey of their members, 21% of respondents chose Lending Club as the business they believe best represents the future of banking 10 years from now. 11% picked Capital One. 6% chose Facebook.

Yet only 17% of respondents had actually actually invested in P2P lending so far. Part of the hesitation comes from the present state of interest rates. 20% of respondents believe that institutional capital will move away from P2P lending and back into traditional finance once interest rates start to really increase.

In the meantime, increasing interest in P2P lending by institutional investors will lead to riskier loans, they say, and it could lead to another credit crisis.

Credit crisis? What Credit crisis?

78% of respondents said history has proven that investors have incredibly short memories and that if securitizations backed by P2P loans offer attractive returns investors will likely dive in.

Of the survey respondents, 24% were fund managers; 9% were allocators; 9% were risk management or trading; 46% were service providers; and 12% were other industry participants.

Lending Club Loan Size Cap Raised to $40,000 (Should Investors Be Worried?)

March 5, 2016 Consumers can now borrow up to $40,000, an increase from the previous cap of $35,000.

Consumers can now borrow up to $40,000, an increase from the previous cap of $35,000.

The new maximum should raise eyebrows. That’s because while one of Lending Club’s biggest allures is the ability to refinance credit cards into a lower rate over a fixed term, there are zero safeguards in place to ensure that the borrower actually uses the proceeds to do just that. Instead, the applicant simply checks a box and if approved, gets the loan minus the origination fee wired to their bank account. That means today’s consumer can obtain 40 grand in one lump sum online. Unsecured. In their bank account. For whatever purpose. From a lending marketplace that puts none of their own money in the loans.

No Recessionary Data for Loans Over $25,000

The numbers look okay, for now. Using NSR’s backtesting tool revealed that loans of exactly $35,000 have generated higher returns for investors than loans of smaller sizes, but have a higher loss rate. This is because the interest rate increases with loan size. The all time loss rate on $35,000 loans is 6.60%, according to the tool, but Lending Club didn’t start making loans this big until February 2011, after the recession had already ended.

That in itself should be alarming because when we examine the time period of June 2007 through June 2010, when the Great Recession occurred, loss rates hit the largest loans the hardest. At that time, the maximum loan size was $25,000 and the loss rate on those was 11.54%.

That in itself should be alarming because when we examine the time period of June 2007 through June 2010, when the Great Recession occurred, loss rates hit the largest loans the hardest. At that time, the maximum loan size was $25,000 and the loss rate on those was 11.54%.

With the maximum size having increased to $35,000 and now to $40,000, there is no recessionary data to indicate how these large loans will perform.

The Temptations of a Cash Windfall?

Credit cards can moderate spending habits because there is a limit on the type of goods and services one can acquire with them. With cash, consumers may be tempted to indulge themselves in other things. One has to wonder if the average consumer really needs 40 grand wired to their account on an unsecured basis with no strings attached on what to do with it.

Lending Club might have considered this already though. In December, they announced Direct Pay, a pilot program in which Lending Club actually requires borrowers to use up to 80% of the proceeds to pay off their outstanding debt. There’s one caveat, it’s only open to a category of the most risky borrowers, those with Debt-to-Income (DTI) ratios of up to 50%. Lending Club’s traditional DTI cap is 30%.

That means that investors have to rely on the ability of borrowers to do the right thing with 40 grand in unsecured cash. Should they trust them?

Lending Club Shifts Fee Arrangement With WebBank

February 26, 2016 It’s a “belt and suspenders” precaution according to Lending Club CEO Renaud Laplanche. The Madden v Midland case has forced the company to rethink their arrangement with WebBank, the chartered bank that allows them to make loans nationwide. Under the new terms, the fee LendingClub pays to WebBank for the loans it issues will be related to how the loans perform over time.

It’s a “belt and suspenders” precaution according to Lending Club CEO Renaud Laplanche. The Madden v Midland case has forced the company to rethink their arrangement with WebBank, the chartered bank that allows them to make loans nationwide. Under the new terms, the fee LendingClub pays to WebBank for the loans it issues will be related to how the loans perform over time.

Even if the U.S. Supreme Court were to rule unfavorably in Madden, Lending Club would still have been able to operate freely under their old arrangement. The change then may be a response to several cases, including ones that have accused online lenders of using chartered bank relationships to carry out alleged abuses. According to law firm Ballard Spahr, a “federal court refused to dismiss Pennsylvania racketeering claims against companies alleged to have partnered with a state bank to market Internet loans illustrates the risks inherent in these relationships and the importance of proper structuring.”

In a brief, Ballard Spahr wrote:

In Commonwealth of Pennsylvania v. Think Finance, Inc., et al., the Pennsylvania AG, working with a well-known private plaintiffs’ firm, claimed that the companies and their individual principal had engaged in a “rent-a-bank” scheme in which a Delaware state bank “acted as the nominal lender while the non-bank entity was the de facto lender—marketing, funding and collecting the loan.”

By WebBank maintaining an interest in the outcome of the individual loans, Lending Club will reduce its potential standing as the de factor lender.

Notably, the breaking story focused on Lending Club. WebBank also has a relationship with others in the alternative finance community such as CAN Capital, Prosper, AvantCredit and PayPal. It’s uncertain if their arrangements will also be subject to change.

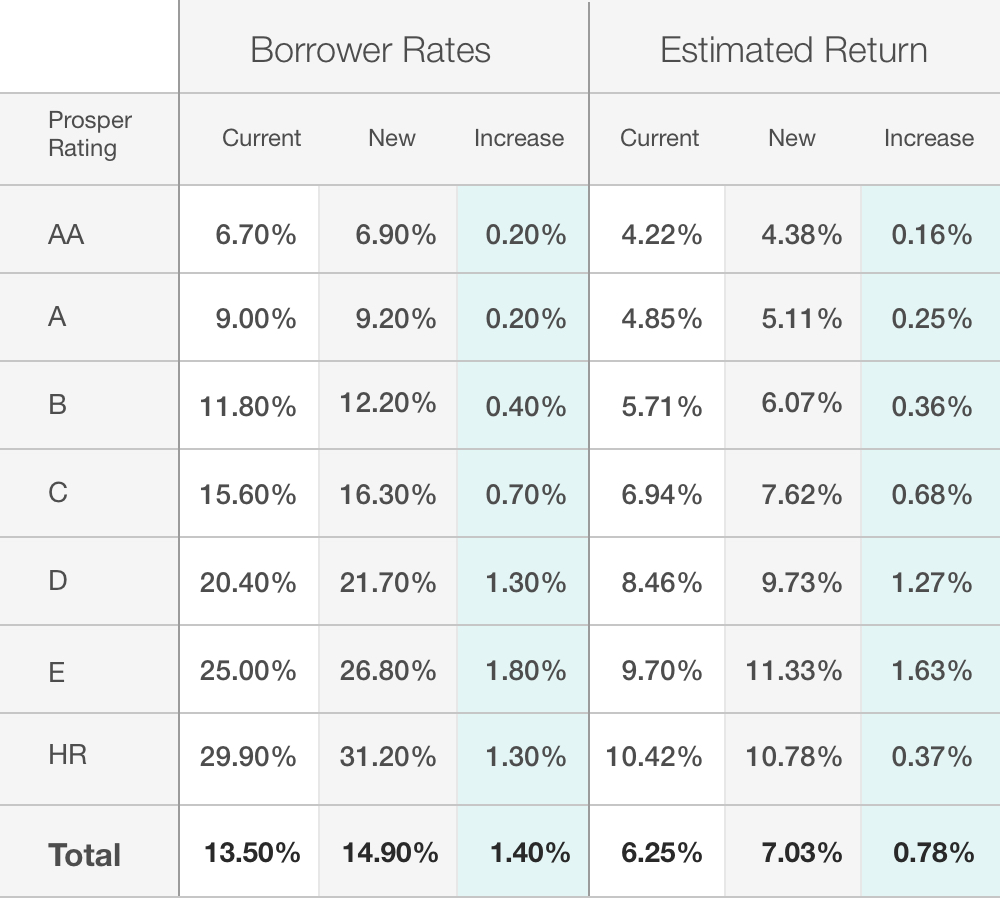

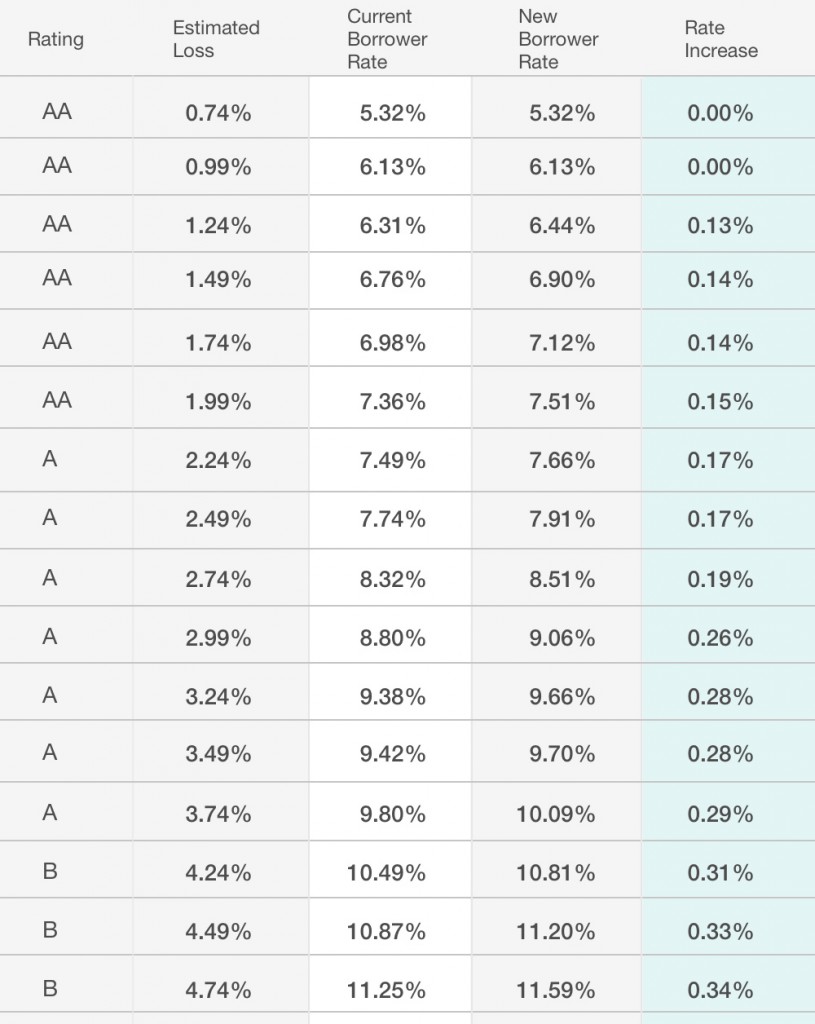

Prosper Has Increased Its Estimated Loss Rates

February 15, 2016“Effective today, Prosper has increased its estimated loss rates and the price charged for risk on the loans originated through the platform,” said an email to investors on Monday. “We believe this move ensures that our borrower payment dependent note and whole loan products remain competitive for our investors in the current turbulent market environment that we have witnessed since the beginning of 2016.”

Prosper is one of only two marketplace lending platforms in the US that is open to retail investors. Founded in 2005, the company has made over $5 billion in loans. They were surpassed by Lending Club in the race to dominate the market after being nearly destroyed by both the Great Recession and a class action lawsuit that claimed they sold unqualified and unregistered securities in violation of the California and federal securities laws. The suit was settled in 2013.

The going forward rate increase affects one category of high risk borrowers by as much as 199 basis points. Meanwhile, even prime borrowers will experience increases of up to 29 basis points.

These are the changes according to Prosper:

Estimated Aggregate Impact to Prosper Portfolio of Loss and Price Changes

Proposed Pricing Modifications for the Week of 2/15

Last week, the company also refaced their entire site. As a Prosper investor, the new user interface greatly improves the user experience.

Lending Club TurboTax Integration Attempts to Solve Marketplace Lending’s Tax Problem

February 15, 2016 Lending Club’s retail investors scored big on February 12th when they announced an integration with TurboTax software. The complexity of marketplace lending from a tax perspective has historically been one of the most prohibitive cost barriers for retail investors. Unlike savings accounts which issue a standard 1099-INT, Lending Club (and Prosper) issue both a 1099-OID and a 1099-B.

Lending Club’s retail investors scored big on February 12th when they announced an integration with TurboTax software. The complexity of marketplace lending from a tax perspective has historically been one of the most prohibitive cost barriers for retail investors. Unlike savings accounts which issue a standard 1099-INT, Lending Club (and Prosper) issue both a 1099-OID and a 1099-B.

According to the IRS, the 1099-OID should “state the excess of an obligation’s stated redemption price at maturity over its issue price. Original Issue Discount (OID) on a taxable obligation is taxable as interest over the life of the obligation. If you are the holder of a taxable OID obligation, generally you must include an amount of OID in your gross income each year you hold the obligation.”

For the average person, explanations like these are enough to warrant the help of an accountant. But that’s a problem for people that are investing a small amount. For example, if $10,000 invested in Lending Club notes generated $700 in income for the year, it wouldn’t be practical to pay an accountant $500 to help you figure it all out. Between that and the actual taxes owed, an investor could easily end up losing money.

For the average person, explanations like these are enough to warrant the help of an accountant. But that’s a problem for people that are investing a small amount. For example, if $10,000 invested in Lending Club notes generated $700 in income for the year, it wouldn’t be practical to pay an accountant $500 to help you figure it all out. Between that and the actual taxes owed, an investor could easily end up losing money.

Lending Club tries to make it all as easy as possible for investors with their step-by-step tax guide, but it can still feel a little confusing. One problem to consider is that investors can only deduct up to $3,000 of their losses if they don’t have any other capital gains.

While an integration with TurboTax is a win for retail investors, marketplace lending had long been a thorn in the side for TurboTax. Complaints about the software not being “peer-to-peer friendly” have haunted Intuit’s help pages for years.

Real Estate Lender Patch of Land Sells $250 Million in Loans

February 11, 2016 Real estate lending platform Patch of Land announced that it signed a $250 million agreement with an east coast based credit fund to purchase its loans in a forward flow arrangement.

Real estate lending platform Patch of Land announced that it signed a $250 million agreement with an east coast based credit fund to purchase its loans in a forward flow arrangement.

The reluctance to name the city or state of the fund suggests that in doing so would too easily reveal who it is.

Patch, an LA-based lender which uses a data-driven underwriting model, promises investors a risk adjusted return with extensive available data to support the underlying credit decision on each loan.

The company founded in 2013 had raised a million in seed funding and $125,000 in debt in 2014, followed by $23 million in Series A funding last year. And it has funded more than 200 projects, with an average blended rate of return to investors of 12 percent

This is continued evidence of institutional interest in loans generated by marketplace lenders. JP Morgan Chase bought loans worth a billion dollars from Santander Consumer USA Holdings Inc earlier this month. The bank also partnered with OnDeck in December of last year to facilitate the underwriting of the bank’s small dollar small business loan program.

In an interview with Bloomberg, Funding Circle’s CEO Sam Hodges said that it’s the first of many such partnerships to come where big banks will realize the potential of fast-growing fintech startups.

Lending Club nets $4.3 million in Q4 profits

February 11, 2016Wants to buyback shares for $150 million.

Online lending marketplace Lending Club earned $4.3 million in profits in Q4 last year and facilitated loans worth $8.4 billion to small businesses and consumers in 2015.

The San Francisco-based P2P lender’s revenue grew in Q4 grew by 93 percent to $134.5 million compared to $69.6 million in the comparable period a year ago. Loan originations also grew to $2.58 billion from $1.41 billion in 2014.

The company, which was the first P2P lender to register its offerings as securities with the SEC is gung ho about its growth prospects. “We have earned the trust of 1.4 million customers,” said founder and CEO Renaud Laplanche. “We have considerable room to grow our existing products, and intend to continue to expand both our product line and addressable population going forward.”

The company which announced that it will also buyback shares worth $150 million through open market operations or in private transactions in compliance with Securities and Exchange Act Rule 10b-18.

This comes amidst doubts raised about the company’s algorithm-based lending model. A Bloomberg report last week questioned Lending Club models with data to show that its actual defaults (7 to 8 percent) were higher than forecasts (4 to 6 percent). The company responded to the report explaining the data and reassuring investors that the loan performance is within expectations.