p2p lending

First Comments to Treasury’s RFI Highlight the Importance of Marketplace Lenders Despite Higher Rates

August 4, 2015 The first responses to Treasury’s request for information about marketplace lenders were posted online yesterday. While only 3 responses have so far been posted, comments from a number of alternative finance providers are expected.

The first responses to Treasury’s request for information about marketplace lenders were posted online yesterday. While only 3 responses have so far been posted, comments from a number of alternative finance providers are expected.

The first response, however, came from Patrick Fitzsimmons, the executive director of Mountain BizWorks, a North Carolina-based community development financial institution. Mr. Fitzsimmons submitted an article published last month in The Citizen Times of Asheville, NC. The article details one small business owner’s efforts to obtain a business loan. After being turned down by banks numerous times, the owner was finally able to obtain financing from an online marketplace lender.

The article quotes a number of employees of CDFIs who criticized the rates charged by some online lenders. One CDFI employee went as far as to characterize the rates charged as “predatory”. In contrast, however, the business owner was—if not enthusiastic about—grateful for the assistance his business received from the online lender.

“It’s not deceiving. I knew what I was getting into,” he said of the loan. “I can’t say that OnDeck didn’t help my business because it did. To say it was great, though, would be an overstatement. For me, it was like getting a root canal: This is not going to be fun, but it’s what I need to do.”

Though the article is somewhat critical of rates charged, it highlights how important alternative marketplace lenders have become to the survival of many small businesses. As the quote above shows, marketplace lenders are, in many cases, the last lifeline available to businesses in need of working capital.

I expect the comments from industry participants to continue to emphasize the need for alternative sources of business capital. At the same time, the industry would be well served to take this opportunity to explain, in greater detail, why alternative product rates are higher than traditional bank financing as some community organizations do not fully appreciate the increased costs and risks associated with offering small business funding.

What’s in the SoFi AAA Rated Bonds?

July 30, 2015 Should you buy student loan debt from a startup tech-based lender? DBRS is signaling yes with a AAA grade to $387 million of the notes in a $418 million offering. To put that into perspective, the U.S. Dollar was given the same grade just months before. Bonds issued by Goldman Sachs however were rated two levels lower at A on July 6th.

Should you buy student loan debt from a startup tech-based lender? DBRS is signaling yes with a AAA grade to $387 million of the notes in a $418 million offering. To put that into perspective, the U.S. Dollar was given the same grade just months before. Bonds issued by Goldman Sachs however were rated two levels lower at A on July 6th.

As Safe as the U.S. Dollar?

Founded just four years ago in 2011, SoFi has already made more than $2.3 billion in student loans. The company CEO Mike Cagney is a regular fixture at FinTech trade shows and I myself admittedly often wear a SoFi t-shirt on hot summer days around the city.

Of all the loans to invest in though, I would’ve put student loans at the very bottom of my list. Everywhere I turn, recent college grads and the elderly alike are lobbying against what they perceive as an unfair system.

In a bombshell article in the New York Times last month titled, Why I Defaulted on My Student Loans, author Lee Siegel argued that repaying student loans will lead to “self-disgust and lifelong unhappiness, destroying a precious young life.”

The story ignited a political firestorm across social networks. But Siegel was unapologetic and encouraged others to follow his example of defaulting.

“I chose life,” he wrote. “That is to say, I defaulted on my student loans. As difficult as it has been, I’ve never looked back. The millions of young people today, who collectively owe over $1 trillion in loans, may want to consider my example.”

He’s found sympathy from millennials who came of age right during or after the financial crisis, since many of them have struggled to find jobs or move out of their parent’s homes.

And it’s not just them, “Over 16% of the $1.2 trillion in outstanding student loan debt belongs to individuals over 50 years old.” According to Forbes, the epidemic of student loan debt is even affecting seniors in retirement, some of whom are facing garnishment of their social security checks.

The outlook isn’t good either. According to the Wall Street Journal, the Class of 2014 is the most indebted ever, that is unless the Class of 2015 steals the title.

And there’s another statistic to consider. “The problem developing is that earnings and debt aren’t moving in the same direction,” reports the WSJ. “From 2005 to 2012, average student loan debt has jumped 35%, adjusting for inflation, while the median salary has actually dropped by 2.2%.”

And there’s another statistic to consider. “The problem developing is that earnings and debt aren’t moving in the same direction,” reports the WSJ. “From 2005 to 2012, average student loan debt has jumped 35%, adjusting for inflation, while the median salary has actually dropped by 2.2%.”

But the SoFi rating is based on data, not on emotionally charged arguments over social networks regarding the morality of paying for college. Obviously the numbers must indicate something to give them a creditworthiness equal to U.S. Dollar, at least for the pool of notes that earned the grade.

Across the entire offering, dubbed 2015-C, there are also notes with a BBB grade. Altogether, the portfolio contains a weighted-average credit score of 777 and a weighted-average borrower income of $143,132. This isn’t exactly a group of poor struggling borrowers.

100% of the loans were refinanced from another lender so they had a prior track record of making payments.

“Refinancing Loan borrowers have already graduated, have proven well-documented incomes and have stronger credit profiles as compared with typical newly originated student loans,” the DBRS report states. “Further, such borrowers have demonstrated an ability to gain employment and repay their student loan debt.”

And yet a large portion of borrowers have a variable rate loan, with the average balance on those being $74,315. It’s a recipe that could shake the system years down the road.

A AAA rating is an eye-opening assessment even with the quality of borrowers. The final maturity dates for those notes are in August, 2035, a full two decades from now. SoFi has only been in business for four years.

Technologists and scientists say to trust in the data, but there’s got to be credibility afforded to the noise coming from millennials over the last few years. That message, at least the one that I’ve heard, has been that student loans are ruining lives.

Breaking news stories about predatory colleges feed into this narrative. Just last month, the NYT alluded that as many as 350,000 students were scammed by Corinthian Colleges. “Corinthian was a longtime target for federal and state regulators, with a host of investigations and lawsuits charging falsified placement rates, deceptive marketing and predatory recruiting, targeting the most vulnerable low-income students,” the NYT stated.

A Corinthian College graduate would probably not qualify to be a SoFi borrower. 3.5% of borrowers in 2015-C graduated from NYU and 2.5% from Columbia. 59% have an MBA, law, or medical degree.

If the DBRS report makes anything absolutely clear, it’s that these are the types of borrowers you’d bring home to meet your parents.

The irony is not lost however that Lee Siegel, the NYT author that encouraged kids to default on student loans like he did, is a graduate of Columbia.

Perhaps for that reason, competing ratings agency Moody’s graded the senior notes only AA2, two notches below what they consider perfect.

Yesterday I would’ve told you that I would never consider student loans as an investment, but now I’m not so sure.

The data and the review by the ratings agencies definitely conflict with what I hear from real life borrowers and their attitudes about student loan debt.

What are your thoughts?

Federal Government Wants Your Thoughts About Online Lending

July 19, 2015 Whether you’re a funder, lender, broker, or platform, the U.S. Treasury Department deserves to hear your input.

Whether you’re a funder, lender, broker, or platform, the U.S. Treasury Department deserves to hear your input.

Only July 16th, the Treasury announced that it was seeking public comment on various business models and products offered by online marketplace lenders to small businesses and consumers. One stated purpose of this is to study “how the financial regulatory framework should evolve to support the safe growth of the industry.”

The comment period is only open for six weeks.

Over the last year, many funders and brokers have voiced their opinions on best practices, ethics, and standards. Some want regulation to curb what they believe to be immoral behavior and others just want clarity where the laws are obscure, illogical, or even in conflict with themselves.

In at least one recent case, a merchant cash advance company CEO wrote about the complexity of dealing with an endless amount of state laws. In Lift the Fog, Give us Regulation, Merchant Cash and Capital CEO Stephen Sheinbaum wrote, “It is also better, at least for the financial services industry, if the central government is the one to craft the regulation instead of getting one rule from each of the 50 state governments.”

Meanwhile the Consumer Financial Protection Bureau (CFPB) will eventually start to enforce the amendments to the Equal Credit Opportunity Act, which technically already became the law under Section 1071 of the Dodd Frank Act. As part of that, underwriters of business loans and merchant cash advance alike may no longer be allowed to meet applicants, speak with them on the phone, examine their driver’s licenses, review their social media profiles, or even ask what their business model is or how they market themselves.

One has to look at any opportunity afforded by a government agency to share input before future regulations are implemented then as a duty. It might not matter, but you should do it anyway, just like voting.

Below are the questions, the Treasury wants you to answer (or Click to view on Treasury.gov):

1. There are many different models for online marketplace lending including platform lenders (also referred to as “peer-to-peer”), balance sheet lenders, and bank-affiliated lenders. In what ways should policymakers be thinking about market segmentation; and in what ways do different models raise different policy or regulatory concerns?

2. What role are electronic data sources playing in enabling marketplace lending? For instance, how do they affect traditionally manual processes or evaluation of identity, fraud, and credit risk for lenders? Are there new opportunities or risks arising from these data-based processes relative to those used in traditional lending?

3. How are online marketplace lenders designing their business models and products for different borrower segments, such as:

• Small business and consumer borrowers;

• Subprime borrowers;

• Borrowers who are “unscoreable” or have no or thin files;

Depending on borrower needs (e.g., new small businesses, mature small businesses, consumers seeking to consolidate existing debt, consumers seeking to take out new credit) and other segmentations?

4. Is marketplace lending expanding access to credit to historically underserved market segments?

5. Describe the customer acquisition process for online marketplace lenders. What kinds of marketing channels are used to reach new customers? What kinds of partnerships do online marketplace lenders have with traditional financial institutions, community development financial institutions (CDFIs), or other types of businesses to reach new customers?

6. How are borrowers assessed for their creditworthiness and repayment ability? How accurate are these models in predicting credit risk? How does the assessment of small 10 business borrowers differ from consumer borrowers? Does the borrower’s stated use of proceeds affect underwriting for the loan?

7. Describe whether and how marketplace lending relies on services or relationships provided by traditional lending institutions or insured depository institutions. What steps have been taken toward regulatory compliance with the new lending model by the various industry participants throughout the lending process? What issues are raised with online marketplace lending across state lines?

8. Describe how marketplace lenders manage operational practices such as loan servicing, fraud detection, credit reporting, and collections. How are these practices handled differently than by traditional lending institutions? What, if anything, do marketplace lenders outsource to third party service providers? Are there provisions for back-up services?

9. What roles, if any, can the federal government play to facilitate positive innovation in lending, such as making it easier for borrowers to share their own government-held data with lenders? What are the competitive advantages and, if any, disadvantages for nonbanks and banks to participate in and grow in this market segment? How can policymakers address any disadvantages for each? How might changes in the credit environment affect online marketplace lenders?

10. Under the different models of marketplace lending, to what extent, if any, should platform or “peer-to-peer” lenders be required to have “skin in the game” for the loans they originate or underwrite in order to align interests with investors who have acquired debt of the marketplace lenders through the platforms? Under the different models, is there pooling of loans that raise issues of alignment with investors in the lenders’ debt obligations? How would the concept of risk retention apply in a non securitization context for the different entities in the distribution chain, including those in which there is no pooling of loans? Should this concept of “risk retention” be the same for other types of syndicated or participated loans?

11. Marketplace lending potentially offers significant benefits and value to borrowers, but what harms might online marketplace lending also present to consumers and small businesses? What privacy considerations, cybersecurity threats, consumer protection concerns, and other related risks might arise out of online marketplace lending? Do existing statutory and regulatory regimes adequately address these issues in the context of online marketplace lending?

12. What factors do investors consider when: (i) investing in notes funding loans being made through online marketplace lenders, (ii) doing business with particular entities, or (iii) determining the characteristics of the notes investors are willing to purchase? What are the operational arrangements? What are the various methods through which investors may finance online platform assets, including purchase of securities, and what are the advantages and disadvantages of using them? Who are the end investors? How prevalent is the use of financial leverage for investors? How is leverage typically obtained and deployed?

13. What is the current availability of secondary liquidity for loan assets originated in this manner? What are the advantages and disadvantages of an active secondary market? Describe the efforts to develop such a market, including any hurdles (regulatory or otherwise). Is this market likely to grow and what advantages and disadvantages might a larger securitization market, including derivatives and benchmarks, present?

14. What are other key trends and issues that policymakers should be monitoring as this market continues to develop?

The Treasury asks that you include your name, company name, address, job title, email address, and phone #. You can submit your responses on http://www.regulations.gov/. Just click on the tab that says “Are you new to the site?”

You can also submit by mail:

To: Laura Temel,

Attention: Marketplace Lending RFI,

U.S. Department of the Treasury, 1500

Pennsylvania Avenue NW., Room 1325

Washington, DC 20220

If you have questions, email marketplace_lending@treasury.gov or call 202-622-1083.

Do Bank Statements Matter in Lending? Business Lenders and Consumer Lenders Disagree

July 16, 2015Bank statements. Those in consumer lending argue they’re all but irrelevant because FICO and credit reports do the job of predicting risk just fine, but over in today’s small business lending environment, there’s an entirely different sentiment; Reveal your recent banking history or be declined.

After having bought nearly $60,000 worth of consumer notes on Lending Club and Prosper combined, there’s something I’ve seen a lot of, bounced ACHs.

Lending Club doesn’t reveal borrower bank data to their investors. Sure, anyone can see the credit report, the income level, zip code, and job title, but the borrower could have negative $10,000 in the bank and be living off overdraft protection on day 1 and an investor would never know it.

Lending Club doesn’t reveal borrower bank data to their investors. Sure, anyone can see the credit report, the income level, zip code, and job title, but the borrower could have negative $10,000 in the bank and be living off overdraft protection on day 1 and an investor would never know it.

For all the fanfare surrounding online marketplace consumer lending, access to borrower banking history is oddly absent.

“Welcome to consumer lending, where the rules are different because the game is too,” replied a user to my comment on a peer-to-peer lending forum.

Veteran consumer lenders assumed I was a lost newbie who knew nothing about lending. “I have a feeling if you ask to crawl someone’s bank account, they’ll just go elsewhere,” one user said. “Seems that’d only work on subprime borrowers who have limited bargaining power.”

“I’m assuming you may be new to lending,” he continued. “Making a loan based on deposit balances is rarely a good idea.”

My initial question to them was that without bank statements, how could they ascertain if a borrower’s finances were actually in order at least at the time the loan was issued? It’s really easy to access someone’s banking history for the last 90 days by using common tools like Yodlee or Microbilt, I argued.

Some people sympathized with my logic but others believed requesting bank data would be suicide in today’s competitive environment. And still more wondered if there might be consumer protection laws that prevented lenders from seeing a loan applicant’s banking records (which sounded ridiculous).

A Credit Card Issuer’s Take

Those questions led me to interview an underwriting manager at one of the nation’s largest credit card issuers who would only speak on the condition of total anonymity, including the bank’s name. There, he oversees a department of people that manually assess credit card applicants. There is no algorithmic approval process. In his department, humans underwrite each application, conduct phone interviews with the prospective borrowers, and request additional documents if they feel it’s warranted.

Requesting bank statements is a regular part of the job, explained the manager. “We require proof of income for any line over 25k,” he added. “It’s the main thing we ask for along with proof of address.”

Requesting these documents keeps them compliant with the Bank Secrecy Act, he explained, but the bank statements in particular are their first choice in verifying somebody’s income, even more than pay stubs. And their underwriters aren’t oblivious zombies, he noted. If an applicant has no money in the bank, they’ll decline it.

Requesting these documents keeps them compliant with the Bank Secrecy Act, he explained, but the bank statements in particular are their first choice in verifying somebody’s income, even more than pay stubs. And their underwriters aren’t oblivious zombies, he noted. If an applicant has no money in the bank, they’ll decline it.

“The Adverse Action reason [for that] would be ‘sufficiently obligated’,” he stated. “That’s when their bank account shows they can not take on any additional financial obligations.”

The manager shared however that he believed there is a very strong correlation between what’s on the credit report and what to expect in the bank statements. Generally speaking, good credit will show a healthy banking situation, he explained. They’re rarely taken by surprise. Overall, the credit reports and phone interviews are enough for them to feel comfortable and the bank statements are really just there to check off a compliance box.

Meanwhile, those that speculated requesting bank data would be a death knell competitively might want to talk to Kabbage’s sister company, Karrot. Karrot already crawls bank accounts as part of their consumer loan application program and competes with Lending Club, Prosper, and Avant. Considering Kabbage has funded more than half a billion dollars worth of business loans using this very methodology, it’s safe to say that applicants aren’t flocking to competitors in droves over the perceived injustice or inconvenience of filling out three additional fields on a web application to share their transaction history.

Bounced Payments

Kabbage CEO Rob Frohwein offered these comments last year about their underwriting, “A critical aspect of consumer lending is determining the appropriate amount of a payment to collect so that an account doesn’t become overdrawn. Our intelligence accurately predicts how much of a payment to request via ACH so consumers avoid the cost and headache associated with non-sufficient funds.”

I thought about those statements when I noticed that thirty-six of my Lending Club notes carried a Grace Period status the other day. These are borrowers whose payments just recently bounced. Some are only three or four months into a five-year loan. Worse, there are those that are saying they have no money whatsoever to make a payment. How can this be when they just practically got approved?

To the consumer crowd it’s business as usual. “If you got their bank account, you still wouldn’t be able to predict who will default. You can’t predict defaults on any individual borrower,” argued one veteran on a forum.

But it’s not all about the lender’s tolerance for risk. ACH rejects can have consequences that affect a lender’s ability to debit accounts in the future.

“Ultimately, regulatory thresholds set by NACHA will continue to become more and more critical of returns,” said Moe Abusaad of ACH Processing Co, an ACH processor based in Plano, TX. “I think it’s safe to say that there is a positive correlation in considering statements as a component of the underwriting process to the rate of returns incurred,” he added.

And while it’s true that bank data can’t make predictions perfectly on its own, nobody in small business lending or merchant cash advance would consider an approval without it.

Bank Statements or Bust

“There is no substitute for banking information when reviewing a client for approval,” said Andrew Hernandez, a co-founder of Central Diligence Group, a risk management firm that allows business lenders and merchant cash advance companies to outsource their underwriting.

“Money moves fast through these businesses and every business is unique, so a lot more variables come into play than just having to account for the timely monthly payments of credit cards, cars, and mortgages as you find in the consumer world,” he added. “A FICO score along with other information presented in a credit report provide a detailed, historical snapshot of a client’s creditworthiness in consumer lending, and while these are great complementary tools for us to use in our underwriting process, I believe that banking data paints us a picture of its own which is absolutely essential in assessing the risk of a B2B transaction in our space.”

Those underwriting business loan deals have reported seeing applicants with open personal loans from Lending Club, which shows that the exact same borrowers are being underwritten in two different ways.

But Julio Izaguirre, another co-founder of Central Diligence Group added that, “banking transactions are essential in gauging the cash flow of the business by looking at recent and up-to-date bank volume, but it is even more important with businesses that lack historical data and cannot provide financials or other documentation to show and prove their track record.”

Translation: A lack of credit history and formal financial statements can be overcome thanks to in-depth analysis of bank account data.

“When our underwriters look at a bank statement you can get a better understanding of the business cash flow, operational cost and how the owner manages his business,” said Heather Francis, CEO of Gainesville, FL-based Elevate Funding. “The credit score is like a person’s blood pressure reading,” she continued. “It indicates there may be an issue but until lab work is pulled and analyzed you don’t know what that issue is. The bank statement is that lab work and it can tell you more about the issues behind the scenes than a credit score can.”

Greg DeMinco, a Managing Partner of Americas Business Capital based in Cherry Hill, NJ would probably agree. “FICO isn’t everything,” he shared. “Bank statements can tell a great story especially if there is upward momentum month after month, and more importantly a high ratio of deposits to requests for the advance.”

Meanwhile, the manager of the credit card issuer was surprised to hear about the high value placed on bank statements in business lending. I offered him the example of an applicant with good credit that was consistently negative in the bank because of a reliance on overdraft protection as a way to make sure all the bills were being paid. “That’s the craziest thing I ever heard,” he commented.

But over in the peer-to-peer lending forum it didn’t sound so crazy at all. “Plenty of Americans are ‘broke’, in the sense that they have negative net worth, yet they’ll continue servicing their debts for… a long time… no matter what it takes,” shared one user.

The argument seems to come full circle, that business lending and consumer lending are just different.

But to Isaac Stern, the CEO of New York-based Yellowstone Capital, the bank statements are not just about financial health. “We are literally underwriting against fraud,” said Stern, who said his office regularly receives applications with doctored statements. “Logging in [to the banks] and verifying those statements are probably the most important part of the process,” he noted.

His logic goes that a consumer that is paid a salary has a predictable stream of income and so that information along with a credit report might be enough for a consumer lender, but business revenue is less predictable and can vary practically day-to-day.

“You can’t just look at a FICO score and say, ‘this is a good a business’,” Stern explained. “The story is in the bank statements.”

Lending Club Ends Q2 With Crisis Nobody Noticed

July 1, 2015 Lending Club investors are used to wonky stuff happening in the run up to a quarter’s end, but perhaps now since the company is public, making sure the numbers align with nice perfect trends that analysts expect is more important than ever. Either that or all hell really broke loose.

Lending Club investors are used to wonky stuff happening in the run up to a quarter’s end, but perhaps now since the company is public, making sure the numbers align with nice perfect trends that analysts expect is more important than ever. Either that or all hell really broke loose.

On the Lend Academy forum, where you can get a great glimpse of the front lines, chatter about a loan surge started on June 22nd and escalated from there.

“Huge # loans dumped in all of a sudden, and almost all allocated to fractional,” wrote veteran user Fred93. “Hard to fathom. My best guess is that this flow might be a result of having turned on some new source. Hard to guess why they are allocating them all to fractional.”

I personally noticed the increase too when I realized I didn’t have to fight robots and algorithms to get the loans I wanted. There were so many that I could pick them at my leisure.

Around this time, Anil Gupta of PeerCube pointed out that Lending Club’s Q2 loan volume had been about 10% lower than Q1’s, thus potentially putting the company in emergency mode to show growth.

But with all those loans piling up, something else happened. The loans weren’t actually issuing and conspiracy theories began to develop.

“I had nothing issued as well….with over 120 notes pending…lc playing end of quarter games,” wrote one user named kya.

Other users speculated that there was something more ominous than just games. There was a lot of discussion of the possibility that something had happened to the major institutional buyers that was causing almost all of the loans to be suddenly dumped off on retail investors, where there just wasn’t enough supply of capital to handle them.

And for a couple of days there, nothing appeared to be getting through. A handful of users reported that only 1% of purchased notes were actually becoming issued loans. The other 99% were in limbo. Everyone’s money appeared to be locked up.

But then suddenly on June 29th, the loan spigot turned off completely. “This would be a new quarter end behavior,” wrote a veteran user by the name of BruiserB. “Normally they keep placing notes on the platform for investors to buy, but they just hold up actually issuing the notes. This is the first time I have seen them stop even offering notes.”

Not that anyone really needed more notes since practically none of the previous ones they had recently bought had been issued. Everything was backlogged.

So was all the chaos just quarter-end volatility? Many did not think so. A member representing LendingAlpha.com thought the system might actually be breaking down. “What is happening now is highly unusual, as they typically push hard to find a large number of borrowers and at the same time their systems broke.”

Others started talking about a purported breakage too on June 30th, including the possibility that Lending Club’s Automated Investing option stopped functioning in the last week of the month.

LendingAlpha.com claims to have gotten a response from a Lending Club representative that admitted there were actual technical problems at play. “Their engineering team is communicating internally that the problem should be resolved by tomorrow (July 1, 2015), and the supply and demand imbalance should be back to normal by early July,” he posted on the Lend Academy forum.

All of the irregular activity prompted LendingRobot, a third party automated investing service to issue a notice to all of its users.

While chatter on Lend Academy’s forum surged about the strange events, it got literally no coverage by blogs or news media. Fortune and Bloomberg claimed that the sudden plummet in Lending Club’s stock price had to do with investors suddenly waking up to the risks of online lending.

Fortune’s Leena Rao seemed to rely on Compass Point Research & Trading analyst Michael Tarkan to form a thesis that long term regulatory concerns were suddenly putting pressure on the stock. “Tarkan further explained that Wall Street has realized that the stock price was overvalued considering the competitive and regulatory risks in the alternative lending space,” Rao wrote.

Meanwhile, veteran note buyers like user lascott were conversing about an unprecedented breakage that had led to long loan issuance delays and in all likelihood, unhappy borrowers.

It should be noted that several forum users also trade the stock. Might the hysteria and speculation that the institutional investors were all dead and backlogged loans were blowing up the system have caused some selling activity?

At the end of June when everyone’s finally starting to hit the beach, I doubt Wall Street suddenly woke up and thought, “Damn, this regulatory risk is scary as hell. Time to sell Lending Club.”

I don’t know why the stock is down exactly but it’s ironic to see news media offer broad market generalities while a crisis unfolds in a public forum.

What happened at Lending Club in the last week of Q2? Nobody really knows but it seems like everything’s getting back to normal now that we’ve started Q3. The institutional investors aren’t gone and backlogged loans are starting to issue.

Nothing to see here folks. What were you saying about regulatory risks again?

Tech-based Lenders Clobbered On Dose of Bad Economic News

June 29, 2015How would tech-based lenders fare in a slumping market? Not very well apparently…

OnDeck (ONDK) and Lending Club (LC) set new record lows earlier today amid bad news coming out of Greece and Puerto Rico. OnDeck is down almost 43% from its IPO price and down 61% from its all time high. It was down more than 8% today even though the Dow was only down 2%.

$ONDK was unaware that it focused on Greek loans…. interesting 8.6% drop.

— Mark Holder (@StoneFoxCapital) Jun. 29 at 05:48 PM

The downward trend was dissected in a post that was published just hours before today’s further fall.

Meanwhile Lending Club is in new territory, down 3% from its IPO price and down 50% from its high. So what are investors saying about this?

$LC hmm i really dunno what to say about this…

— mike pham (@mincogneto) Jun. 29 at 05:30 PM

That’s kind of the overall gut feeling. Many feel this company is being unfairly dragged down and yet it continues to fall. A mounting campaign by the Puerto Rican government to declare bankruptcy and a Greek debt disaster clobbered everything today including Lending Club. One tweeter came up with a great idea last week, bail out Greece with a loan from Lending Club…

If all else fails with the IMF #Greece should just apply on @LendingClub pic.twitter.com/RbtnMm5JaO

— World First USA (@WorldFirstUS) June 22, 2015

Last week no one was even talking about Puerto Rico. Now all of the sudden they’re in a “death spiral.”

Watch the death spiral coverage on CNN

The market’s tech lending darlings might’ve gotten pummeled like everyone else but the ease with which they drop should probably be a warning sign. Neither offshore dilemma stands to have any impact on their businesses. So what would happen if a relevant issue were to arise such as a domestic disaster, a sudden rise in unemployment, a recession, a financial crisis, skyrocketing fuel prices, a steep increase in the fed funds rate, or even something no one dares talk about like a legal ruling that could jeopardize the entire bank charter model?

It’s quite possible that both companies haven’t bottomed out just yet….

——–

Note: I have no equity positions in either company. I do own Lending Club notes however.

Tech-based Underwriting Shows Cracks?

June 21, 2015 A self proclaimed borrower of Lending Club and Prosper loans posted a tell-all on the Lend Academy forum earlier today and the allegations are alarming. Below is a summary of their experience:

A self proclaimed borrower of Lending Club and Prosper loans posted a tell-all on the Lend Academy forum earlier today and the allegations are alarming. Below is a summary of their experience:

- Stated that when times got tough, they resorted to lying about everything.

- Alleged the lenders don’t care about what they’re using the money for.

- Stated that after consolidating their debt, they immediately maxed out their revolving lines again.

- Proclaimed that these types of loans are for people who are at the end of their rope just trying to survive.

- Alleged their revolving line utilization percentage was wrong because credit bureaus showed old revolving accounts as open even though they’ve actually been closed for years. In their case, the utilization stated 25% but in reality was 100%.

- Alleged their Debt-to-Income ratio was wrong. It looked more favorable than it actually was.

- Stated they stopped making payments and then filed bankruptcy six months later.

- Alleged Prosper never even filed a Proof of Claim with the bankruptcy court and therefore won’t be receiving anything.

Disturbingly, the borrower says they were able to get a second loan from each lender without their employment/income being re-verified.

“I guess I could have lost my job and you never would have known,” the author writes.

Suspiciously however, they go on to make an off-the-cuff recommendation that peer-to-peer marketplaces be required to invest their own money in the loans they issue.

“Why wouldn’t a company file a proof of claim?,” they questioned. “I have to assume because they have no incentive to do so. If the law was changed so these companies had to put up 10-20% of their own money, you may see them caring more about the investors.”

One has to wonder why an individual that successfully evaded a creditor after drowning in debt and filing bankruptcy would come on to lobby for a law that would encourage that creditor to do a better job collecting.

Regardless of us being able to confirm the borrower’s authenticity though, they did raise some good points.

Is it possible that a credit bureau could show accounts as open that are actually closed? Of course. A recently issued FTC report revealed that one in five consumers had an error on at least one of their three credit reports. But even worse, one in just four consumers identified errors on their credit reports that might affect their credit scores.

If 20% of reports are not perfect and 25% of consumers see material errors in their reports, then investors are working off of pretty shoddy data to make decisions.

Additionally, a common complaint by investors on the forum are loan amounts for debt consolidation that wildly exceed the borrower’s actual revolving debt. Could this be a sign that borrower intent is not validated?

And while I couldn’t confirm whether or not income and employment are re-verified on additional loans from the same lender, the implications of playing fast and loose the second time around are troublesome. Lending Club states that past performance is the predominant basis for another loan:

To qualify for a second loan, you’ll need to meet the current credit criteria for the second loan and have made either 6 or 12 consecutive on-time monthly payments on your existing Lending Club loan*, depending upon the size and term of the existing loan.

*Borrowers must have made 12 consecutive successful monthly payments if the original loan principal is $20k or more or the existing loan has a 60 month term, unless the loan has been paid down by 50% or more, in which case borrowers need only have made 6 consecutive monthly payments. Borrowers must have made 6 consecutive successful monthly payments if the original loan principal is less than $20k and the loan has a 36 month term.

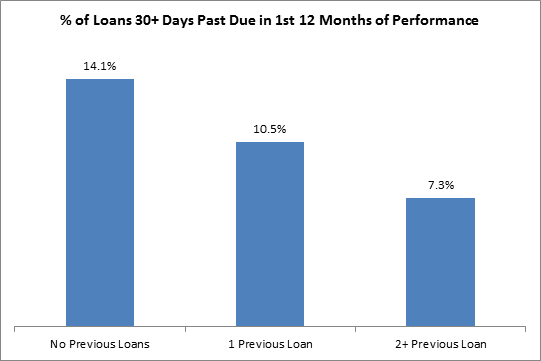

But while the defaulting borrower tells us to be afraid, historical data paints a different picture. Peer-to-peer lending guru Peter Renton has long touted repeat borrowers because of the stellar returns they produce.

And Orchard’s analysis of Prosper loans two years ago confirmed the same. The more loans a borrower took with Prosper, the less likely they were to become delinquent on their loan. This was only the case for the first 12 months of the loans, not in their entirety to maturity, which they didn’t examine at the time.

But while the statistics look good, the defaulting borrower is perhaps warning us that a lender’s guard comes down with positive past performance and is therefore vulnerable.

Whatever the case may be and whatever the author’s true intentions are, it is certainly alarming to read that a borrower lied, their credit information was inaccurate, they defaulted on the loan, and the lender made no effort to make a claim in the bankruptcy proceeding.

Is tech-based underwriting and the marketplace model showing cracks? You be the judge…

Lending Club Violated Securities Laws, Forced to File Rescission Offer

June 12, 2015Lending Club appears to have violated the securities laws of several states when it issued stock options as compensation between July 2012 and October 2014. According to an official Rescission Offer filed with the SEC on June 12th, Lending Club is offering to buy back both common stock shares and unexercised options to remedy their mistake. Combined, 40,469,837 shares of common stock are subject to the offer. Their reason for doing so is as follows:

We have issued shares of common stock or granted options to purchase shares to our current and former employees and consultants. From July 2012 through October 2014 (or during the periods specified on the addendum to this offering circular with respect to residents of certain states), the options we granted and shares issued upon exercise of the options may not have been exempt from the registration or qualification requirements under applicable securities laws.

The filing admits they violated the laws of at least 16 states and Puerto Rico.

For New York, it says, “We were required to apply for an exemption from the broker-dealer registration and securities issuance requirements with the State of New York to issue the shares and/or options to you without registration or qualification. Because of our failure to apply for an exemption, you have three years to seek a remedy for our failure to register.”

For New York, it says, “We were required to apply for an exemption from the broker-dealer registration and securities issuance requirements with the State of New York to issue the shares and/or options to you without registration or qualification. Because of our failure to apply for an exemption, you have three years to seek a remedy for our failure to register.”

For California, it says, “Certain options and shares issued pursuant to the 2007 Stock Incentive Plan may have been granted or issued in violation of the California Corporate Securities Law.”

The market price of the improperly issued shares amounts to $700 million. However, few if any shareholders subject to the rescission offer would likely accept it since it proposes buying back the shares at their original value + interest. Those values range from $0.06 to $8.94 per share. Lending Club closed today at $17.28, at double the highest proposed rescission offer price.

Indeed, no company officers are moving to accept the offer as it specifically states, “Seven of our officers and directors, who together hold 1,044,892 shares of common stock and options to purchase 11,081,780 shares of common stock, all of which shares are subject to this rescission offer, are eligible to participate in the rescission offer. We have been advised that these officers and directors do not intend to accept the rescission offer.”

Indeed, no company officers are moving to accept the offer as it specifically states, “Seven of our officers and directors, who together hold 1,044,892 shares of common stock and options to purchase 11,081,780 shares of common stock, all of which shares are subject to this rescission offer, are eligible to participate in the rescission offer. We have been advised that these officers and directors do not intend to accept the rescission offer.”

However, if the stock price were to drop by more than 50% between now and July 15th (the deadline to decide), the rescission offer would actually become in the money for a handful of investors. The odds of that happening are pretty slim.

Lending Club’s explanation for getting in this mess in the first place is as follows:

We became subject to the reporting obligations of section 15(d) of the Securities Exchange Act of 1934, as amended (Exchange Act) upon the effectiveness of our registration statement for our member payment dependent notes on Form S-1 on October 10, 2008. As a result, we were no longer entitled to rely on the qualification requirements pursuant to section 25102(o) of the California Corporate Securities Law. Because we could not rely on section 25102(o) of the California Corporate Securities Law, the options we granted and the shares issued upon exercise of these options during this period may have been issued in violation of California securities laws. In July 2014, we applied for a permit for qualification from the California DBO. In connection with the review of the permit application, the California DBO has required that we make this rescission offer to certain holders of any outstanding, unexercised options or shares of common stock issued upon exercise of stock options. Accordingly, we are making the rescission offer to the approximately 598 persons who received grants of options or purchased common stock upon exercises of options under the 2007 Stock Incentive Plan (except with respect to shares of our common stock which were subsequently sold by such persons at a price per share that exceeded the exercise price per share plus interest at the legal rate from the date of exercise, and therefore would exceed the amount of the rescission offer). If our rescission offer is accepted by all offerees, we could be required to make an aggregate payment to the holders of these options and shares of up to approximately $34.2 million, which includes statutory interest.