Opinion

Did UCC Lead Generators Overload NY State’s System?

April 4, 2017 In the small business finance industry, New York State is known as one of the friendliest places to conduct a UCC search. You can not only search by debtor, but also by secured party, and get just about everything you need to create a list of prospects for free.

In the small business finance industry, New York State is known as one of the friendliest places to conduct a UCC search. You can not only search by debtor, but also by secured party, and get just about everything you need to create a list of prospects for free.

But the State’s website isn’t exactly a pillar of technological achievement. Indeed, the UCC Lien Search welcome page makes clear that searchers will need to be using Netscape Navigator 4.0 or higher and that version 3.0 of Internet Explorer or lower is not supported. Those browser iterations were released in 1997 and 1996 respectively, before some in the business finance industry were even born.

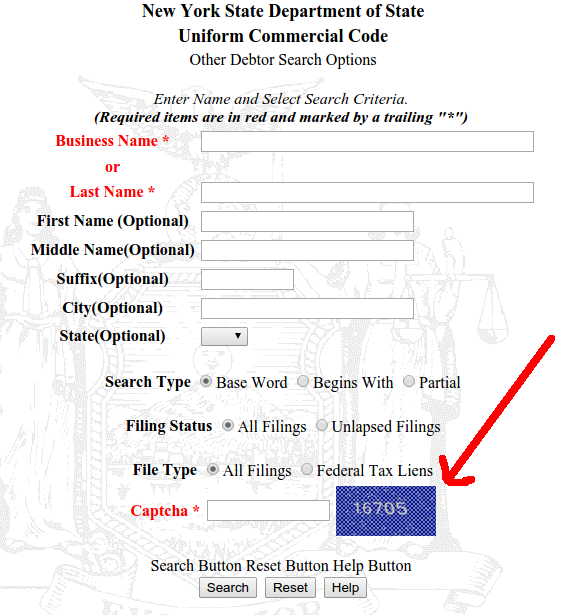

And the online system built for Windows 3.1 users didn’t seem to be doing so well over the last few months. Routine manual searches that I occasionally conduct were leading to error messages and crash pages instead of results. Were UCC lead generators querying the system to death?

Last week, New York took the entire UCC system down for “maintenance” and when it finally came back up, a tool to combat automated queries had been installed.

Curiously, this has only been implemented for secured party searches and other debtor search options. Standard debtor search options remains unchanged.

As Captchas are designed to thwart automated queries, could this be a sign that lead generators were crashing the system?

To check it out yourself, it’s best to be using Windows 95 or higher. Typewriters and Etch-A-Sketch users may experience performance issues.

Funding Circle’s New $100 Million Funding Round is a Surprise, But it’s Really Not

January 13, 2017The alternative small business lender that is arguably offering the longest terms with the lowest rates has secured a $100 Million Series F Round, according to an announcement on Wednesday.

With the round led by Accel, the strong sign of confidence contradicts the sentiment felt by many in the US about their business model. In the last few months, several of Funding Circle’s US competitors have suspended operations, shut their doors, or integrated into other companies. Most of the questions we’ve received lately have centered around “who’s next to fall?” not “who’s next to raise $100 million?”

So what’s going on here?

Imagine in an alternate universe that the US government was using Funding Circle’s platform to fund millions of dollars to small businesses, that the US Treasury Secretary was publicly cheering them on, and that they sat on Capitol Hill drawing up new laws that would regulate their industry in a way that would help them succeed, would you bet on them to win?

That alternate universe exists and it’s called the United Kingdom. It’s also Funding Circle’s primary market. Just last week the UK government lent Funding Circle another £40 million on top of the previous £60 million to lend to small businesses amid credit concerns related to Brexit and it’s only one example of how cozy government relations are over there.

That alternate universe exists and it’s called the United Kingdom. It’s also Funding Circle’s primary market. Just last week the UK government lent Funding Circle another £40 million on top of the previous £60 million to lend to small businesses amid credit concerns related to Brexit and it’s only one example of how cozy government relations are over there.

Chancellor of the Exchequer (the US Treasury Secretary equivalent), Philip Hammond, said: “Funding Circle has become a real success story for British Fintech and news that it has attracted £80 million (US $100 mil) of investment is further evidence of the growing importance of this industry. This is another vote of confidence in a UK firm that plays an important role in our economy – helping businesses to grow and create jobs.”

And in a TV interview with Bloomberg, Funding Circle co-founder James Meekings said that the company is working with the government to help draft the regulations that they would have to abide by. Sounds like a nice arrangement.

The UK is still their biggest market but part of their $100 million funding round will be used to further develop their US business, Meekings said on Bloomberg. To date, the company has raised $375 million. Less than two years ago, their private market valuation was $1 billion, more than twice OnDeck’s current market cap. Funding Circle’s valuation in this round was not disclosed.

Funding Circle’s global loan volume these days rivals OnDeck’s. £400 million was lent by Funding Circle in Q4 versus $613 million lent by OnDeck in Q3, setting up the possibility that the former could surpass the latter in volume this year.

Funding Circle’s publicly traded SME Income Fund has also held up pretty well over the last year:

Shortly after announcing their funding round, a trade group they co-founded in the US, the Marketplace Lending Association, welcomed 11 new members. Might Funding Circle eventually gain the same favor in the US that they’ve nurtured in the UK? Would you bet on them?

Merchant Cash Advance’s David and Goliath End an Era

January 5, 2017 Before there was Capify and CAN Capital, there was AmeriMerchant and AdvanceMe. Those are the original names of the two industry rivals whose history goes back more than 10 years. When I started working for an MCA company in 2006, I was taught two things, that AdvanceMe claimed to have a patent on merchant cash advance’s core feature and that AmeriMerchant’s CEO was leading the charge to have it invalidated. Back then, AdvanceMe had sued AmeriMerchant and several other companies for violating its automated payment patent and it was the biggest threat to the industry’s future at the time.

Before there was Capify and CAN Capital, there was AmeriMerchant and AdvanceMe. Those are the original names of the two industry rivals whose history goes back more than 10 years. When I started working for an MCA company in 2006, I was taught two things, that AdvanceMe claimed to have a patent on merchant cash advance’s core feature and that AmeriMerchant’s CEO was leading the charge to have it invalidated. Back then, AdvanceMe had sued AmeriMerchant and several other companies for violating its automated payment patent and it was the biggest threat to the industry’s future at the time.

A real life David and Goliath saga, it was only fitting that AmeriMerchant’s CEO was actually named David. His last name Goldin, he went on to win the lawsuit in such a big way, the story was featured in the New York Times. At that time in 2007, the Times quotes Goldin as saying, “It’s a victory against patent trolls. This has changed the landscape. The days of coming up with an obvious idea and patenting it and using legal extortion are over.”

With the patent invalidated, numerous entrepreneurs felt the coast was clear to start a merchant cash advance company, thus paving the way to become an industry that now originates more than $10 billion a year in funding to small businesses. AdvanceMe was a Goliath in that it held a virtual monopoly on MCA in the late 90s and early 2000s. They had such a huge head start on everyone, that they were still the largest MCA company in the US in 2014 (if you don’t count OnDeck which only does loans).

That era is coming to a close. AdvanceMe, today CAN Capital, suspended funding in late November of 2016 after internal issues were discovered, which resulted in mass layoffs and executive departures. And AmeriMerchant, today Capify, announced it is integrating its US operations with another industry rival, Strategic Funding Source (SFS), who will be managing all of their US customers going forward.

That era is coming to a close. AdvanceMe, today CAN Capital, suspended funding in late November of 2016 after internal issues were discovered, which resulted in mass layoffs and executive departures. And AmeriMerchant, today Capify, announced it is integrating its US operations with another industry rival, Strategic Funding Source (SFS), who will be managing all of their US customers going forward.

While CAN Capital’s ultimate fate is still yet to be determined, the end of Capify’s US presence is an M&A event, the first one of 2017. An insider at SFS said on a call that Capify’s international operations were not part of the deal in any way. Goldin will continue to run his company’s other offices such as Capify UK like normal. In the US however, more than twenty of Capify’s employees are being transitioned to work as SFS employees and to work from SFS’s office.

In the transaction’s announcement, Goldin is quoted as saying “we are very pleased to have put together a deal with Strategic Funding that will provide our customers a future source of important capital. As a company that shares our values of providing simple, transparent and responsible access to capital for small and mid-sized businesses, it was a logical transition.”

SFS, founded in 2006, and today one of the largest MCA funders in the nation, is a worthy successor. In a way, the more things in this industry change, the more things stay the same. As a testament to that, the antagonist of the 2007 NY Times story is Glenn Goldman, then the CEO of AdvanceMe and today the head of Credibly, another MCA competitor that also underwent a name change.

At the time, Goldman wrote to the Times, saying, “Although we feel vindicated that the court found clear infringement of our patent by each of the defendants, we respectfully disagree with the court’s findings on validity.”

Ironically, ACH is now the main payment mechanism for merchant cash advances, not split-processing, rendering the patent battle that took place a decade ago practically moot. It’s the end of an era.

My Three Year Anniversary of Investing on Lending Club’s Platform

January 3, 2017 It’s been three long years since the first month that I ever bought a Lending Club note and to commemorate the event, I decided to go back and see what I did and share what I’ve learned since then.

It’s been three long years since the first month that I ever bought a Lending Club note and to commemorate the event, I decided to go back and see what I did and share what I’ve learned since then.

In January 2014, I attempted to buy ten $25 notes for a total of $250, all of which were A and B-grade with 36 month maturities. Here’s what happened:

- Four of them paid off early

- Four of them are current and are just about to mature

- Two of the loans ended up not getting funded

So I actually only ended up getting $200 worth of notes and the results were great. But I didn’t stop there. I went on to buy more than $85,000 worth of Lending Club notes over the next two and a half years. The last note I ever bought was on June 8, 2016. If you’re wondering if I’ve made money, I have so far, but that still assumes a doomsday event doesn’t happen with the rest of my outstanding notes that will mature over the next few years.

Here are a few things I learned since the day I first started:

Reinvesting isn’t guaranteed

There is no guarantee that a similar new note will be available to replace one that just paid off. In the immediate post-Laplanche era, there were very few notes on the retail platform to buy and sometimes even none at all. Any number of major events could cause a situation like this to happen on a marketplace lending platform so you need to be prepared to manage idle cash should there be few or no suitable replacement notes.

Early payoffs can be very bad

This is related to reinvesting but can be bad all on its own. Lending Club charges retail investors a 1% penalty on outstanding principal whenever a borrower pays off their loan early (so long as the loan is 12 months old). Few people seem to be aware of this and it really makes no sense. Consider that as a retail investor you not only lose the interest you would make for the rest of the life of the loan on a good paying borrower, but you also get hit with a penalty on top of it even though you as the investor had nothing to do with the borrower’s decision. That sucks a lot. And potentially even worse, but plausible, what if there were no identical notes available to replace the ones lost to an early payoff? You lose three times.

Other platforms and banks are working against you

Banks like Discover and Goldman Sachs are actively working to steal Lending Club’s borrowers. And when they are successful, loans get paid off early, which hurts your investments. I’ve had nearly 1,000 of my borrowers pay off early on Lending Club for some reason or another already, so this is a major phenomenon.

Diversification isn’t just about the letter grades

Don’t put all your money in 1 note, but also don’t put all your money on 1 platform. Lending Club is still just a single company so you should only invest a small percentage of your investable assets on it. I have placed smaller experimental amounts on other platforms such as Prosper, StreetShares and Colonial Funding Network (Strategic Funding Source.) And yet, the bulk of my personal investments are actually in more traditional assets.

Holes in transparency

One of Lending Club’s biggest draws has been its transparency with investors but there’s still a lot of information that is withheld. When a borrower pays off early, investors aren’t told why or how it happened. Are borrowers really refinancing a credit card or are they taking the money and going to Vegas for the weekend? Investors don’t know and the true use of funds isn’t verified. Is the borrower broke? Lending Club focuses on a borrower’s credit profile, not on how much cash the borrower has in the bank, which could be $0 or negative. I’ve encountered plenty of investors that have argued that a borrower’s cash flow history is a non-factor or a burden on approval speed, but coming from a commercial financing background, I am still shocked that a consumer’s historical cash flow plays no role in getting a three-to-five year loan.

When a borrower stops paying, don’t expect to know why

A common theme in the collections notes of delinquent borrowers is the dreaded “Called. No answer,” line which can repeat for days, weeks, or months on end. Some borrowers will just stop paying and then never answer Lending Club’s calls again or they’ll ask that they “cease and desist” from making future calls. Was it financial hardship? You won’t always get the satisfaction of knowing, making it truly a numbers game.

This is a speculative investment

The value of your portfolio might not have volatile swings, but there are numerous risk factors that can impact performance. Only invest a small percentage of your investable assets.

It’s a nice investment option to have

Investing in notes backed by consumer loans is a great yield opportunity for retail investors in a low savings account rate environment. Despite the risks, retail investors don’t have many alternatives to earn a decent return outside of the stock market. Hopefully marketplace lending platforms don’t completely move away from retail investors.

Is Marketplace Lending Really Just Westworld?

December 5, 2016

If you haven’t watched HBO’s new flagship TV show Westworld, my analogy may have some broad spoilers so you might want to look away. Also, you should start watching the show.

In a world controlled by banks, people can visit a world where the hosts looks like banks but aren’t. They’re non-banks with bank-like attributes run off of advanced programming. You can borrow from them, pay them back, invest in them and securitize their loans. They seem real indeed, but the real banks are the chartered ones that pull their strings and script their stories.

In this real life version of Westworld, might the proposed OCC charter be the maze?

A rose is a rose is a rose.

The Season Finale of Alternative Lending Has Everything You’d Expect

November 17, 2016

This month kicked off what appears to be the first segment of the 2016 two-part season finale of alternative lending. So far, it has everything you’d expect, a main character gets killed off, another simply won’t be returning next season, a wedding, a scandal and even a cliffhanger!

So in that precise order, here’s what you missed:

A main character’s surprising death

Crowdfund Insider reported on Wednesday that Dealstruck, a small business lender, had ceased lending operations. An email sent to Dealstruck has not yet been returned, but Crowdfund Insider’s story includes a quote from Dealstruck’s CEO saying that the company is no longer originating new loans.

The company initially arrived on the scene to much fanfare. A writeup in techcrunch last year said that they had raised $8.3 million in venture financing and secured a $50 million credit facility.

Guess who won’t be back next season

Aaron Vermut is stepping down as Prosper Marketplace’s CEO. He is being replaced by company CFO David Kimball. Vermut’s father, Stephan Vermut is also stepping down as executive chairman.

A wedding between an old character and a new one

Peerform, which was founded in 2011, has been acquired by Versara Lending. Versara, an unfamiliar name, appears to be related to NYC-based Strategic Financial Solutions, a debt relief company headed by Ryan Sasson. Peerform CEO Mikael Rapaport has updated his LinkedIn profile to reflect a new role at both Versara and Strategic.

Scandal! The fake business loan negotiator from upstate New York has been arrested

His name is Sergiy Bezrukov, but the world may know him by another name (or three), John Butler, Thomas Paris or Christopher Riley. After terrorizing the MCA and business lending industry for almost a year, he now sits in prison awaiting trial.

Cliffhanger

Oh, so you thought Prosper would file their 10-Q on Tuesday? You were wrong. The company instead informed the SEC that they would be filing their report late, leaving loan investors wondering if there may be more to the recent executive departures.

Stay tuned!

If this were really a TV show, you’d probably think it jumped the shark when the country elected a President that pledged to dismantle Dodd-Frank while potentially defanging the CFPB. But that is precisely what has happened. “The Dodd-Frank economy does not work for working people,” the President-Elect’s website states. “Bureaucratic red tape and Washington mandates are not the answer. The Financial Services Policy Implementation team will be working to dismantle the Dodd-Frank Act and replace it with new policies to encourage economic growth and job creation.”

If anything, this is all the more reason that you should be tuning in and following the industry in 2017.

The Art of The ‘Thiel’ – With Fintech Leader On Trump’s Transition Team, Alternative Lenders Could Benefit

November 13, 2016

Peter Thiel is famous for a lot of things, co-founding PayPal, backing Hulk Hogan’s lawsuit against Gawker and being a billionaire venture capitalist, just to name a few. Accustomed to shaking up Silicon Valley with his investments and antics, these days Thiel stands to impart his wisdom on another region, Washington DC. That’s because last week he became part of the Executive Committee of President-Elect Trump’s transition team.

After speaking at the 2016 Republican National Convention and donating $1.25 million towards Trump’s election efforts, his allegiance to the campaign should come as no surprise. His support is said to be genuine too, and that’s perhaps because the two have relied on similar rhetoric to make their points.

“Competition is For Losers”

Who said that quote? If you thought Donald Trump, you’re wrong, but you wouldn’t be blamed for thinking that given that so much of Trump’s mantra was focused on America “winning.” Competition is For Losers is the title of a 2014 Wall Street Journal essay penned by Thiel, that argued a perfectly competitive marketplace, an economic utopia, is flawed. “In business, equilibrium means stasis, and stasis means death,” he wrote. Entrepreneurs should instead strive for a monopoly, to win, he explained.

Winning is certainly something Thiel has done a lot of, making him a role model of the Trump credo.

“I think they should be described as terrorists, not as writers or reporters.”

Who said that quote? If you thought Donald Trump, you’re wrong, but you wouldn’t be blamed for thinking that given Trump’s hostility towards the media. Thiel said that in 2009 about Gawker reporters, and he bottled up that disdain and unleashed it in the form of financial support for Hulk Hogan against Gawker in a lawsuit years later, the force of which crippled Gawker and put the company into bankruptcy. It’s a revenge narrative that sounds oddly Trumpesque.

While there are likely more contrasts between the two men than similarities like these, both share a special penchant for winning. And more to the point, in a Trump presidency, Thiel may have his ear.

That should be welcome news to fintech and alternative lenders, given Thiel’s strong financial interest in that sector. Small business lender OnDeck has already experienced a 43% increase in its stock price since Trump was announced the winner. Enova, which bought merchant cash advance firm The Business Backer, is up 13%. That’s no doubt in part a result of Trump’s campaign promises to put a moratorium on financial regulations and recent pledge to dismantle the Dodd-Frank Act.

But with Thiel, his ties to alternative lending and fintech were made evident when he gave the keynote speech at LendIt earlier this year in San Francisco, in which he colorfully reiterated his theory about competition being a losing endeavor. “If you want to compete like crazy, you should just leave the conference and try to open a restaurant in San Francisco,” he said.

Thiel participated in SoFi’s $80 Million Series C round and Avant’s $225 million Series D round. “There are a lot of banks in the United States, but not enough access to credit,” he said in an announcement for the latter at the time.

He also participated in ZestFinance’s Series C round and both OnDeck’s D and E rounds.

And more recently, his VC fund, Founder’s Fund, led the $100 million Series D round of Affirm. The fund has also invested in Able Lending, BitPay and Upstart.

Last month, Phin Upham, a principal of Thiel Capital, another of Thiel’s investment firms, dismissed Goldman Sachs’ recent attempt to cash in on tech-based lending. “I wonder if Goldman will actually be able to keep up, because this is not a mature industry, everything changes sometimes within months.”

The NY Times reported that Thiel will not be moving to Washington and may not have a formal role in the administration, but that he will have a voice.

“A page in the book of history has turned, and there is an opening to think about some of our problems from a new perspective,” the Times reported Thiel saying. “I’ll try to help the president in any way I can.”

If truly given the opportunity to do so, Thiel’s influence could be a boon to fintech and the larger economy as a whole.

At the Money2020 conference last month, Trump was largely and quite openly derided by industry leaders. They may soon be changing their tune.

Other members of the Executive Committee of the transition team include:

- Congressman Lou Barletta

- Congresswoman Marsha Blackburn

- Florida Attorney General Pam Bondi

- Congressman Chris Collins

- Jared Kushner

- Congressman Tom Marino

- Rebekah Mercer

- Steven Mnuchin

- Congressman Devin Nunesv

- Anthony Scaramucci

- Donald Trump Jr.

- Eric Trump

- Ivanka Trump

- RNC Chairman Reince Priebus

- Trump Campaign CEO Stephen K. Bannon

It is quite possible that we may soon be making fintech ‘Great Again’

Make Funding Great Again – Triumphant Trump Trumps Clinton In Big Upset

November 9, 2016

The signs were there, surveys showed, at least a few that deBanked made reference to back in August. Small business owners felt Trump had their best interests at heart by a 2 to 1 margin over those who felt that about Clinton, according to a Capify survey.

Taxes ranked among their biggest concerns, with 20% of business owners ranking taxes as the single most important problem facing their business, according to a survey conducted by the National Federation of Independent Business. And Trump was in tune to that.

“Under my plan, no American company will pay more than 15% of their business income in taxes,” Trump said in Detroit on August 8th. He’s also proposed a moratorium on new financial regulations.

But up on the hill, the chatter over the last few months among the political establishment, including republicans, has been one of uncertainty. No one has been able to ascertain for sure what Trump’s positions would actually be or what agenda he’d actually set. And this wildcard status is probably what helped him win the election in the first place.

On his website however, Trump says that “we will no longer regulate our companies and our jobs out of existence,” and that he’ll “issue a temporary moratorium on new agency regulations that are not compelled by Congress or public safety in order to give our American companies the certainty they need to reinvest in our community, get cash off of the sidelines, start hiring again, and expanding businesses.”

That may be good news for the fintech industry which has grown increasingly concerned and preoccupied with potential regulatory changes. One potential conflict could arise with the CFPB, however, which has argued that its own executive branch authority operates outside the scope of the President of the United States.

In October, the United States Court of Appeals for the District of Columbia Circuit, ruled that the CFPB’s power structure violated Article II of the Constitution.

It’s too early to tell what Trump will really do and we’ll likely learn more about his goals over the next few months. Until then, prepare to Make The Industry Great Again…