How Syndication Has Made Millions for Partners

April 3, 2015 “How Syndication Has Made Millions for Partners” is a subtitle I borrowed from Strategic Funding Source’s print periodical, The Business Strategist. In the article penned by Ben Johnston, the company’s Chief Strategy Officer, the story how of syndication made its way into the merchant cash advance industry is explained in detail.

“How Syndication Has Made Millions for Partners” is a subtitle I borrowed from Strategic Funding Source’s print periodical, The Business Strategist. In the article penned by Ben Johnston, the company’s Chief Strategy Officer, the story how of syndication made its way into the merchant cash advance industry is explained in detail.

Of notable mention is that Strategic has had over 200 syndicate partners co-invest over $260 million of their own money into funded deals. That’s more than a quarter billion dollars from syndicates.

Their platform, which was the first one to operate on scalable level, provides same day payments to syndicates and access to detailed reports on a daily basis.

“Peer-to-peer lending and crowdfunding have become hot topics in the financial industry,” the article concludes. “But Strategic Funding Source has been crowdfunding with its own peers for years.”

A Return to the Fundamentals? (At Transact 15)

April 3, 2015 The Transact ’15 conference opened to a record crowd and there was no shortage of merchant cash advance players in attendance. Those facts were to be expected. And if you walked in and poked your head around, you might not have noticed anything to be different. Payment processors touted the latest mobile technology and at every turn security systems were being offered to prevent catastrophic breaches of cardholder data.

The Transact ’15 conference opened to a record crowd and there was no shortage of merchant cash advance players in attendance. Those facts were to be expected. And if you walked in and poked your head around, you might not have noticed anything to be different. Payment processors touted the latest mobile technology and at every turn security systems were being offered to prevent catastrophic breaches of cardholder data.

Everything looked normal… except the merchant cash advance companies.

Back to the fundamentals

Early on Wednesday, April 1st, CAN Capital kicked off a product announcement by raffling off free Apple watches. CAN’s new product is called TrakLoan, a revolutionary new loan program that allows merchants to repay via a split percentage of their credit card sales instead of fixed ACH.

April Fools?

The described advantage of TrackLoan is that there is no fixed term and that merchants only pay back at the pace that they generate card sales. Wait, Where have I heard of this before?

After slapping myself across the face a few times to make sure I hadn’t teleported to the year 2005, the rip in the space time continuum grew more apparent at the after parties.

Card processors Integrity Payment Systems, North American Bancard and Priority Payment systems are still among the hottest names in town for splits. The veteran MCA ISOs and funders are still boarding hoards of merchant accounts with them every month and are therefore building multi-million dollar residual portfolios in the process. It makes one wonder why so many people have turned their back on split-deals for the ACH methodology.

Years ago, merchant cash advance was a sideshow value-add that could be used to acquire what really mattered and what was reliably profitable, merchant accounts. Not everyone has forgotten that however.

Over at Strategic Funding Source, Vice President Hellen McQuain is heading up a new merchant services division. In The Business Strategist, an SFS periodical, McQuain speaks the native tongue of the payments industry: EMV, PCI, NFC, etc.. Few, if any, of today’s new entrants in merchant cash advance could identify what those acronyms stand for, let alone explain the current climate of adoption.

Over at Strategic Funding Source, Vice President Hellen McQuain is heading up a new merchant services division. In The Business Strategist, an SFS periodical, McQuain speaks the native tongue of the payments industry: EMV, PCI, NFC, etc.. Few, if any, of today’s new entrants in merchant cash advance could identify what those acronyms stand for, let alone explain the current climate of adoption.

So, is it time to get back to the basics?

Over the last six months, I have heard more gripes from funders about how to align a broker’s interest with theirs, other than by offering the opportunity to syndicate of course. The question comes down to, how can you get a broker to care about the outcome of a deal?

The answer should be obvious. Pay half the commission upfront and the other half as part of an ongoing performance residual. That gives the broker a stake in the outcome without having to syndicate. This is not a novel idea. This was how the entire industry operated from 2005 to 2011.

Might brokers resist such a compensation plan today in an upfront-only world? Maybe. But the greatest resistance I sense from funders, especially new ones, is that automated residual payments are too complicated for their current accounting systems.

That of course begs another question. How can this possibly be? Despite the rapid growth in technology, there is an entire segment of the industry that is ill-equipped to handle transactions that were commonplace and scalable five years ago.

While today’s systems are impressive, there are times when it seems like yesterday’s advanced technology was lost in a great flood, along with all the scientific texts documenting how to build the powerful machines.

To add to this, some of today’s edgy ideas are not new. A monthly payment loan for example is not an innovative idea. Weekly payments might acquire the merchant that wouldn’t do daily payments. And monthly payments might get the merchant that wouldn’t do weekly payments. These stretched out programs might make you popular with merchant cash advance brokers that are used to selling daily payment products, but they’re in no way new. It’s a return to the basics.

In 2015 we may apparently be going full circle.

A Peek Inside Yellowstone Capital

April 1, 2015When the banks say ‘no,’ alternative financing companies are saying ‘yes,’ sometimes. While costs may run high, there is still a limit on risk that a lender like OnDeck Capital and their competitors can accept.

In January of 2011, Kabbage stated their approval rate on volume-eligible applicants was only 55%. In February of this year, they said it’s about 80%. And a year ago, CAN Capital CEO Dan DeMeo told Forbes their approval rate was almost 70%. Similarly, a Biz2Credit report estimated the approval rate for alternative lenders in 2014 to be around 64% on average.

This indicates that approximately 20% – 35% of small businesses are being declined yet again. These are America’s exiles and they don’t fit into the neat little underwriting boxes that alternative lenders have crafted. Being declined by an alternative lender does not necessarily mean the business isn’t healthy or viable, but rather it could be because they exhibit some characteristic that today’s risk algorithms disqualify. Volatile sales activity, short time in business, poor credit, and atypical SIC codes are just a few of the reasons that a business could be rejected by a lender like OnDeck.

Consequently, an entire Plan C market has sprung up to service the small businesses that have been cast aside by the algorithms. And it’s huge. At the center of it all is Yellowstone Capital, a New York City-based merchant cash advance provider that has carved out its own niche. Founded in 2009, Yellowstone was one of a handful of pioneers that introduced ACH payments to an industry that relied entirely on split-processing.

Yellowstone does not publish their annual funding volume, but according to insiders not authorized to speak on the record, the numbers dwarf many industry behemoths including Square Capital, a company that funded more than $100 million in the last twelve months. And there’s some interesting changes happening there behind the scenes.

Yellowstone does not publish their annual funding volume, but according to insiders not authorized to speak on the record, the numbers dwarf many industry behemoths including Square Capital, a company that funded more than $100 million in the last twelve months. And there’s some interesting changes happening there behind the scenes.

Last year, Yellowstone gave up an equity stake to a New York-based hedge fund in exchange for capital. Just recently however, Yellowstone CEO Isaac Stern led a management buyout to reportedly better position themselves for growth.

As part of the arrangement led by Stern and backed by a private family office, the hedge fund has been bought out and Stern is the only remaining company co-founder to retain an equity stake.

Additionally, private equity turnaround expert Jeff Reece has come on as President. Reece is a former Director of Cogent Partners, a boutique, private equity-focused investment bank and advisory firm.

Josh Karp is remaining the company’s Chief Operating Officer.

Jake Weiser is staying on as General Counsel.

Above all, the changes are more than just a few new faces in management. Yellowstone has already rented an additional floor at 160 Pearl Street, bringing the total floors they occupy there now to three.

Above all, the changes are more than just a few new faces in management. Yellowstone has already rented an additional floor at 160 Pearl Street, bringing the total floors they occupy there now to three.

Notably, the company has endured some negative press in the past of which they are well aware, but they have no shortage of supporters. I contacted two ISOs that claim to have worked with them and asked for their opinion on the Yellowstone experience.

Len Gelman of Allied Capital Corp couldn’t say enough good things about his account manager there, “He fights for every deal I submit, no matter how small or how difficult it may be to get done,” said Gelman. “He always takes my calls and responds to my emails and texts no matter how late it may be.”

And Arty Bujan of Cardinal Equity said, “Working with Yellowstone opened a door of business for me that really wouldn’t have existed without their unique approach to funding what some may call less desirable merchants.”

With a new management team and strong capital backing, Stern and Reece appear to be laying the groundwork to scale.

According to company insiders, Yellowstone is also working to expand their box beyond just high risk businesses and plan to service the middle market risk class. That would in effect also make them a Plan B option.

Their new underwriting depth could spare business owners from that second ‘no.’

Transact 15 in San Francisco

March 29, 2015 I’ll be at Transact ’15 this week in San Francisco. It used to be the only national show that the entirety of the merchant cash advance industry attended. That’s not necessarily the case anymore but it’s still a must-attend event for funders.

I’ll be at Transact ’15 this week in San Francisco. It used to be the only national show that the entirety of the merchant cash advance industry attended. That’s not necessarily the case anymore but it’s still a must-attend event for funders.

Click here for my photo blog of last year’s Transact conference.

To view the events I’ll be at this year, check out our schedule.

I will of course be keeping a live blog of the conference on the website and collecting photos, news, and interviews for use in the next issue of deBanked magazine. If you’d like to arrange a meeting, email me at sean@debanked.com.

See you in Cali!

The #payments industry will all be at Moscone in San Francisco Tuesday for http://t.co/dV0KxGwXmR – largest show in ETA's 25 year history!

— Jason Oxman (@joxman) March 27, 2015

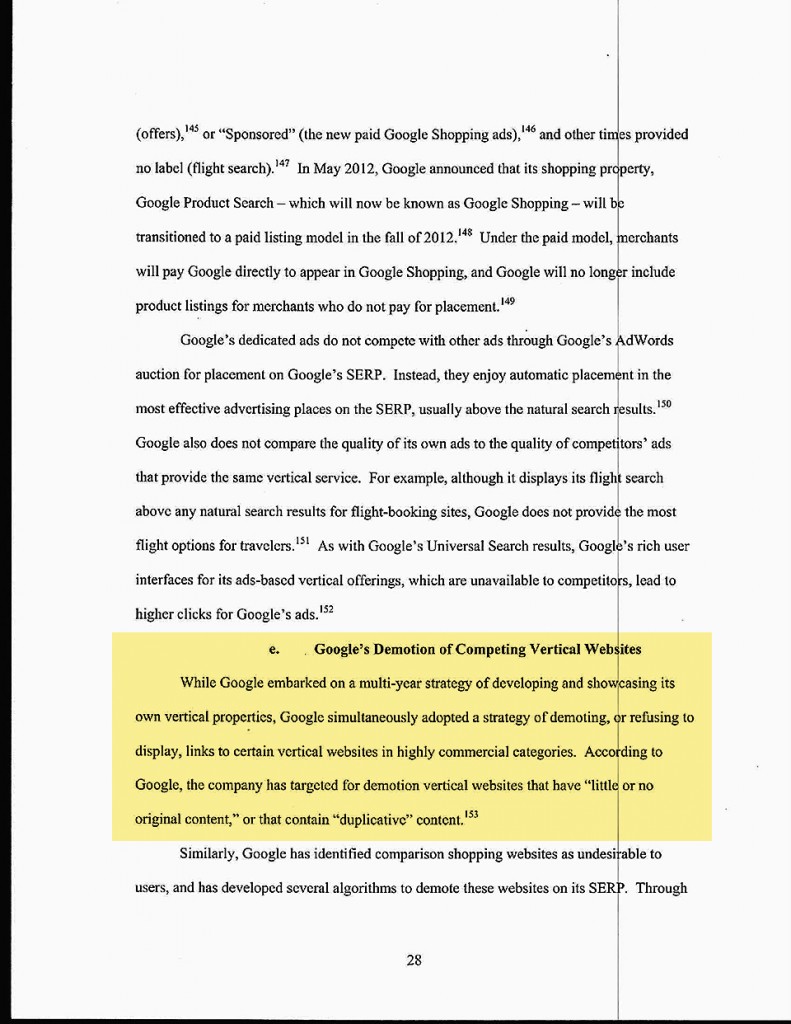

Search Engine Lead Generation Is Probably Rigged

March 21, 2015 Hoping to do some nifty SEO to boost your site to the top of search results for valuable keywords? Don’t bother. In August, 2014, I presented six signs that alternative lending is rigged, at least as far as search was concerned.

Hoping to do some nifty SEO to boost your site to the top of search results for valuable keywords? Don’t bother. In August, 2014, I presented six signs that alternative lending is rigged, at least as far as search was concerned.

Two days ago, the Wall Street Journal ran a story that exposed a confidential FTC report on Google. The article opens with, “Officials at the Federal Trade Commission concluded in 2012 that Google Inc. used anticompetitive tactics and abused its monopoly power in ways that harmed Internet users and rivals, a far harsher analysis of Google’s business than was previously known.”

The conclusion? Google indeed skewed search results to favor its own services.

The 160 page report that the WSJ draws its analysis from was not supposed to be made public. Only a handful of pages are presented on the WSJ’s website in their entirety. Below are two of them:

Though I cannot find the specific comment anymore on LinkedIn, one of the responses I received on my August post regarding Google’s search results came from a former Google employee. They informed me that my suspicion was preposterous and that Google would never ever manipulate results.

While I made no effort to assert my evidence as anything more than circumstantial, the outright dominance of Google-owned lending companies for high value lending keywords was impossible to ignore. The WSJ story adds fuel to this fire.

Admittedly, the WSJ story doesn’t mention lending, nor do I think lending keywords were a subject of the FTC report (There are 156 pages the WSJ didn’t share). What I think is compelling here is a conclusion that Google did indeed manipulate results and penalized competitors to favor its own financial goals.

Despite the findings, the FTC ultimately did not bring any action against Google.

Is the game rigged? I feel a little bit better about saying, yes. Don’t put all your eggs in the SEO basket.

Merchant Cash and Capital Hits a Billion Dollars

March 18, 2015I was there. In August 2006, a little startup in College Point, Queens hired its third and fourth employees. One of them was me. The company’s CEO Steve Sheinbaum hired us to be underwriters of a financial product that at that point didn’t really have a name. It would later become referred to as a merchant cash advance.

The company grew fast, almost too fast. By December of 2006, half of the company was working out of temporary offices in the Empire State Building. And when that no longer made sense, we leased a floor at 450 Park Avenue South in mid-2007 where Merchant Cash and Capital still has its headquarters today.

Fast forward to 2008, I was the most senior risk manager of the firm. As the Director of Underwriting, my direct reports were two underwriting managers. Below them were three or four team leaders. And below them were entry-level underwriters and their administrative assistants. I oversaw what was arguably the most important department leading up to the financial crisis. I really believe the hard work of all the underwriters and the seriousness of which they took their job is a huge contributing factor to why MCC survived when many of their competitors did not.

It is great to see them hit the milestone of $1 billion in funding. Congratulations.

The Unofficial Origin of Merchant Cash Advance (In Honor of St. Patrick’s Day)

March 16, 2015 In the late 1790s, two brave pioneers trekked across the North American continent in search of a bank loan alternative. A particularly harsh winter almost managed to dash their dreams, but they pressed on. “For the free market! For funding!” they cheered. Their optimism stood in stark contrast to the cold rugged landscape through which they traveled.

In the late 1790s, two brave pioneers trekked across the North American continent in search of a bank loan alternative. A particularly harsh winter almost managed to dash their dreams, but they pressed on. “For the free market! For funding!” they cheered. Their optimism stood in stark contrast to the cold rugged landscape through which they traveled.

They weren’t the only two who sought change, but they were the catalyst. One of them was Sam Smith, an owner of Ye Olde Bar and Restaurant. His partner was John Stacker. John was the more wild and unpredictable of the two. They had always brewed their own ale but their customers had grown tired of the taste and were turning to local moonshiners.

Eager to win back their customers, Sam reached out to the distributor of a major lager but was told he could only make purchases in bulk. It would cost them $10, nearly the amount his bar would earn in a month. He was confident that if he raised the cash, he could sell it to their customers for far more than they paid for it and come out ahead. Sam knew there was only one place in town to borrow a hefty sum of $10, First American Bank and Trust. It wasn’t a national chain, but rather quite literally the first national bank and the only one that anyone could trust.

“A business loan for $10?” the bankers laughed. “Absolutely not!”

And so Sam realized that if it was capital they sought, they’d have to get it from someone out in the great beyond. John agreed, kind of. He didn’t want to settle for someone. He hoped to enlist the help of everyone.

After packing their bags and saying their farewells, the two partners set off on a 900-mile journey.

Their wagon fell apart about halfway there. When it could no longer be patched up, they continued on horseback. When the horses died, they walked. When their legs gave out, they crawled and when their knees gave out they did the worm.

Their wagon fell apart about halfway there. When it could no longer be patched up, they continued on horseback. When the horses died, they walked. When their legs gave out, they crawled and when their knees gave out they did the worm.

With barely any energy left and ready to give up, they came upon a charming red brick building in the middle of a desert. A sign was posted outside that said “Ye Olde Barter Shop. Trade Inside.” If for no other reason than to rest, they made their way toward the door.

Behind the counter of the establishment was a dapper old man with silver hair. He spoke with a brogue and was quite possibly of Irish heritage. “Come to trade have ya lads?” He had a warm inviting smile and it caused the two friends to feign an interest, even though they had nothing to trade.

After some pleasant small talk, the Irishman asked what they were looking for. “We need money for our small business,” Sam responded. “Aye lad, well I’m not a banker ya know, but I might be able to work out a trade.”

After some pleasant small talk, the Irishman asked what they were looking for. “We need money for our small business,” Sam responded. “Aye lad, well I’m not a banker ya know, but I might be able to work out a trade.”

Uninterested in anything other than money, they felt their time was being wasted and they turned to say their goodbyes. But the Irishman’s infectious voice called to them with an interesting offer. “I’ll trade ya lads. I will give you this $10 you seek, but in return you will give me $12 of your future sales. Tis’ a barter I just came up with.”

Sam was immediately interested, but had questions. “When do you need the $12 back by?” he asked. Before the Irishman could respond, Sam began to pick up on something he hadn’t before. What was a beautiful building doing in the middle of the desert? Why would an Irishman be bartering out here and wouldn’t the fact that his FICO score was below 680 be a deal breaker?

The entire experience almost seemed…magic, which made him even more receptive to the response he was about to get.

“The $12 is not due by any time. For every ten pennies you earn from your customers, take one and put it in a jar. When the amount in the jar reaches $12, you can bring it to me. As long as your bar is as consistent as you say and there’s no reason for me to believe that your business will close, I would like to invest this $10 for you to buy this fine lager. However lad, no lager is as fine as the true lager itself. I do hope this lager is Guinness.”

The Irishman continued but Sam was already sold. The stars had aligned. It was unsecured, it was fast, it was magic. As long as Sam could prove that they had no real problems with the tax man, they would receive $10.

“We should do this with every barter shop in the country at the same time!” John exclaimed. Sam just glared at him.

“We should do this with every barter shop in the country at the same time!” John exclaimed. Sam just glared at him.

After the Irishman pulled their credit, ran a UCC search, and examined their bank statements, they got funded. It was just that simple.

And so the end of the story is different depending on who you ask, though every version of it has a few common elements. Sam and John’s bar thrived and the townspeople loved them for it. John Stacker opened a separate bar that was all his own and he bartered his future sales all the way up to 12th position.

Other merchants began to tap into this kind of financing by trading their future sales in exchange for cash upfront. First American Bank and Trust was unperturbed and instead focused on how to charge people for holding their money, withdrawing their money, breathing and existing. Their goal was to one day become too big to fail, blow up, and then never lend to small businesses ever again.

And as for the barter shop run by the Irishman? Legend has it that they’re currently paying 14 points to brokers and gearing up for an IPO. They’ve also rebranded themselves in the public eye as a tech company. Private Equity is now all over them.

Happy St. Patrick’s Day. It’s okay to have some fun every now and then. 🙂

Brokers, Ferraris, Stacking and More

March 10, 2015 Not yet signed up to receive deBanked’s print magazine? You can subscribe to receive it FREE here. This upcoming issue covers a lot of ground!

Not yet signed up to receive deBanked’s print magazine? You can subscribe to receive it FREE here. This upcoming issue covers a lot of ground!

Some sneak peeks and commentary:

* I interviewed the president of a Ferrari-driving MCA brokerage who started off as a telemarketer that lived in his car.

* A CPA firm and Law firm submitted interesting takes on different industry practices.

* As much as I wanted to cool off on the topic of stacking for a while, those interviewed by our journalists couldn’t stop talking about it. It is apparently unavoidable and inescapable. Whether you stack or you don’t it’s one of the first nuggets to pop up in any conversation about short term business financing. Coincidentally, I had the privilege of being in the room with some industry leaders a few weeks ago and a discussion about stacking inevitably dominated the debate.

* There’s lot of new brokers in the space and not just human middlemen, but platforms that are really just technology-based brokers. We investigated what’s driving the new brokers and how to handle them. Separately, we interviewed a technology company that automates loan picks so that retail lenders don’t have to.

There’s more of course. You’ll just have to subscribe and wait for it to arrive in the mail. They’ll be sent out at the end of this month.

And if you plan on going to the LendIt Conference in NYC, use coupon code: deBankedVIP to get 25% off the ticket price. All attendees will get a copy of the magazine in their swag bag. I hope to see you there.