Expansion Capital Group Crosses $50 Million Milestone

August 27, 2015 Move over New York and Silicon Valley, Expansion Capital Group (ECG), a young Sioux Falls, South Dakota-based business lender is quickly rising up the ranks. Founded just two years ago, a company representative has confirmed to deBanked that they’ve already funded more than $50 million to small businesses nationwide.

Move over New York and Silicon Valley, Expansion Capital Group (ECG), a young Sioux Falls, South Dakota-based business lender is quickly rising up the ranks. Founded just two years ago, a company representative has confirmed to deBanked that they’ve already funded more than $50 million to small businesses nationwide.

While South Dakota might be better known as the home state of Mount Rushmore, they have made a name for themselves in an industry largely centered around New York, California, and South Florida.

Jay Larson, ECG’s COO, shared with deBanked, “We are definitely excited to cross the $50 million deployment milestone. First and foremost, we’d like to thank all of our industry partners for all their help and support in getting us here. Second, this is only the beginning of ECG’s journey [and] as such we’re looking forward to reaching the $100M milestone in a much shorter period of time.”

On the industry leaderboard, ECG is not that far behind competitors that have been in the industry for much longer. Credibly, for example, has reportedly funded more than $140 million since inception but that’s spread out over a period of more than four years.

Business Financial Services Acquires Entrust Merchant Solutions

August 26, 2015 A representative for Coral Springs, FL-based Business Financial Services (BFS) has confirmed that the company has acquired Entrust Merchant Solutions. Entrust is a well established and widely known NY-based ISO/broker shop that was founded in 2007. As part of the deal, Entrust CEO Ilya Fridman will remain with the company and for the time being, the Entrust name will not change. They are now a part of the BFS family of companies however.

A representative for Coral Springs, FL-based Business Financial Services (BFS) has confirmed that the company has acquired Entrust Merchant Solutions. Entrust is a well established and widely known NY-based ISO/broker shop that was founded in 2007. As part of the deal, Entrust CEO Ilya Fridman will remain with the company and for the time being, the Entrust name will not change. They are now a part of the BFS family of companies however.

The news comes on the heels of a major milestone. Just a month ago, BFS announced that they had funded more than $1 Billion since inception, earning them a spot as one of the industry’s largest players.

The Entrust acquisition is representative of an M&A trend taking place in the industry. Below is a list of some of the more recent ones:

- Enova International acquired The Business Backer (for $27 million)

- Merchants Capital Access acquired Reliant Funding

- Capital Z Partners acquired Pearl Capital

- World Business Lenders acquired the business loan operations of Plan B Growth (and has made 11 acquisitions total over the past 12 months)

Prior to the deal, Entrust was an ISO for BFS. Over the last few days though, some insiders speculated that the relationship had suddenly grown even tighter. It turns out they were right.

Federal Reserve Publishes Results of Alternative Lending Focus Groups

August 26, 2015 Alternative lenders have a lot of work to do!

Alternative lenders have a lot of work to do!

In a study conducted by the Federal Reserve which included focus groups moderated by the Nielsen Company, small business owners that had not heard of online lenders or had not used them, expressed extreme skepticism about their legitimacy. Among the negative responses were words such as shady, scam, identity theft, high APRs, ridiculous, wild west and unregulated, among others.

The focus groups, while small, had to meet a minimum criteria to be eligible:

- Have 2 to 20 employees

- Have annual revenues between $200,000 and $2 million

- Be the financial decision maker

- Not be a new business

Only 44 people participated.

There were both bright and dark spots in the findings, with one of the bright spots being that people’s attitudes became more positive about online lenders once they started to actually navigate the websites of several big industry players.

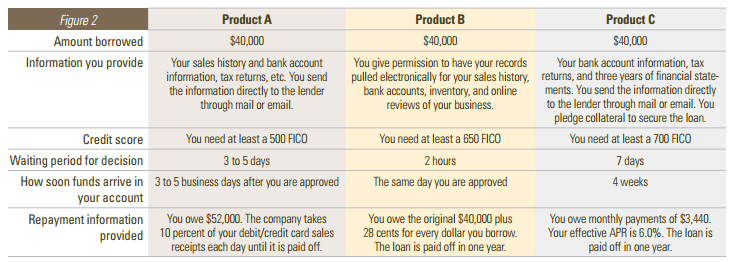

While the extent of the research is significant for any lender trying to get into the mind of a small business owner, there was a section in particular that warrants closer attention. In a mock comparison, participants were asked to compare three unnamed financial products, with one supposedly representing the characteristics of a merchant cash advance based on future credit card sales, another on a daily debit business loan, and the last a traditional bank loan.

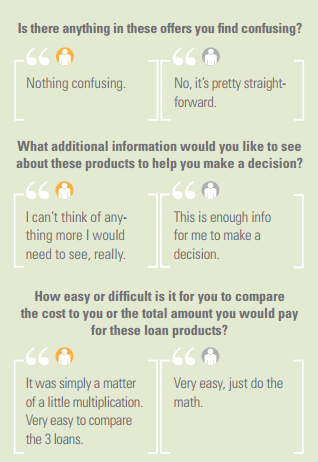

Respondents generally reported that they understood these offers and were not confused by them.

Unfortunately, the researchers assigned some gut-wrenching characteristics to the structure of the product alleged to represent merchant cash advances (Product A).

The offer was a loan of $40,000 to pay back $52,000 in future credit card sales via a 10% processing split and participants were asked to guess the interest rate over one year. The question received all kinds of confused answers such as 5%, 9.8%, 15%, and others that made little sense.

The offer was a loan of $40,000 to pay back $52,000 in future credit card sales via a 10% processing split and participants were asked to guess the interest rate over one year. The question received all kinds of confused answers such as 5%, 9.8%, 15%, and others that made little sense.

Since the researchers presented the theoretical product as a loan, not a sale, they have potentially tainted the inferred conclusions about the transparency of future receivable transactions. Given the strong authority associated with the Federal Reserve and Nielsen, there is a troubling implication that the findings about a hypothetical loan could be used as a basis to make future regulatory decisions about unrelated products like receivable purchases.

Ironically, the diversity of wrong answers to the interest rate question could lead one to this conclusion though, that APRs wouldn’t necessarily be a transparency cure.

If business owners don’t understand what Annual Percentage Rates represent, then it might not be a very good medium to make comparisons. This argument is actually reinforced by the study’s own research since two of the three products were presented without the confusion of interest rates and “participants initially reported the three were easy to compare and that they had all the information they needed to make a borrowing decision.”

In regards to the traditional bank loan, one business owner is actually quoted as saying, “I am not sure what they mean by my ‘effective APR.'”

While value can be gleaned from the results of such a small sample size of 44 business owners, it’s obvious that the researchers influenced the participants answers on how they assessed the cost of merchant cash advances in particular.

- A transaction typically structured as a sale was presented to participants as a loan.

- A predetermined time frame of 1 year was provided to participants when they were asked about interest rates even though purchase transactions have no time frame.

The merchant cash advance product presented in the focus groups has just about no similarities to the purchase transactions that exist in real life.

What are your thoughts on this report and particularly the way merchant cash advance is framed in it? You can download the full report, including the focus group questionnaire here.

Are Your Sales Methods Wimpy?

August 24, 2015 Do you remember Wimpy? Some of you probably don’t but those who do remember Wimpy, remember him as being a silent scam artist who promised the famous phrase, “I will gladly pay you Tuesday for a Hamburger today.” He never adhered to that promise. I never ascribed cartoons to real life but we can learn a few things from Wimpy and how we understand business relationships.

Do you remember Wimpy? Some of you probably don’t but those who do remember Wimpy, remember him as being a silent scam artist who promised the famous phrase, “I will gladly pay you Tuesday for a Hamburger today.” He never adhered to that promise. I never ascribed cartoons to real life but we can learn a few things from Wimpy and how we understand business relationships.

Back in the day, there was something called Trust. It was a little thing that was swapped like currency with the people that you interacted with on a daily basis. Today, trust has been traded for the Internet and now we have nothing to stand on. We must work harder to build relationships in any capacity and at the end of the day, you might still question if a developing level of trust is reciprocal.

Take trust and mix it with a sales position in 2015 and you have disaster. The countless nos you must endure to get to the few yeses and the pressure to close those yeses is exacerbated by the fear that a Wimpy or the Internet will come and take them away.

While reading Personal Touch Makes Big Difference in Small-Business Loans on the WSJ this morning, I immediately got a little upset. This is such a “Duh Article.” A “Duh Article” is one of those articles that are true, but so true in the fact that you end up saying, “Duh, I know that!” and wonder why such basic teachings become important when they are finally backed up by a case study. Did anyone really not think that personal relationships help? Or that Wimpy, the borrower you didn’t know, would not really pay you on Tuesday when you relied on just his word? It goes both ways.

Below are a few ways to avoid the Wimpy traits of sales when building a relationship between you and a business owner:

#1 Rule of Sales Relationships: What are you even selling?

You are selling money so it shouldn’t be that hard right? WRONG. Even though everyone could use an influx of capital, you have two factors that impact your sales in the MCA Industry. PRICE and PROMINENCE.

- Price: We are already slandered for putting a hefty price tag on advances and even if you say, “We offer factor rates as low as a 1.08!”, How many 1.08 deals do you really close?

- Prominence: Names, Logos, and Promises. Characterization plays a big part in what you represent. With so many MCA Entities popping up, how do you set yourself apart?

You have to offset the two factors by building the relationship and creating an understanding.

Example: Imagine you are selling a line of ketchup to every hamburger shop in the U.S.

Do they already have ketchup? They will eventually need to reorder. So where do they get it now? Are they content with this outlet or have they never thought to seek out an alternative? This is the same “question scenario” you have to answer when selling. Note: Replace Ketchup with Capital.

- Do they need capital now?

- Will they need more capital soon?

- How do they get capital when they need it?

- How can I deliver all of the above and be their new preferred choice?

If the answer to the first question is no, that’s okay, move on to the next question. You are more likely to close double the sales when you answer the second and third one. Either way, one of those will have an answer.

#2 Rule of Sales Relationships: Understand the Market you are Targeting

Who is your target market and do you understand them? This is one of those situations where I feel offering a factor to a manufacturing company that is based on invoices is just plain dumb. There are many alternative financing options that are more mainstream than you think and it all boils down to the top 3 things:

- Industry: Do you understand the industry you are selling to? You will connect better with your merchant if you understand the inner workings, schedule, and the ways they obtain their receivables. Their Industry is their passion. If you don’t connect with their passion (unless there is a dire need for emergency capital) you will not be taken seriously or remembered. Ask yourself, “how can I demonstrate an understanding of the way the business makes money or works with different vendors to get paid?”

- Credit: Don’t promise a low rate to a business that you know has a credit score below 600. Research the different tier programs PROVIDED to you by most Direct Funders. Categorize your tier sales structure and request examples of similar past funded industries from the Funders you work with.

- NEED:If they do need capital now, what is it for? This is a great conversation starter. Whether it’s a seasonal need, equipment-related, or plain ol’ working capital, probe the conversation by finding out their goals so you can better represent the merchant and fit them to a better funding program.

#3 Rule of Sales Relationships: The Follow up

This may go far beyond the basic sales guidelines, but categorize your prospects!

Example: Say you have a book of restaurants that you have connected with before and you know they are going to start gearing up for the holidays. Let them know you UNDERSTAND this time of year and how you can assist! Personalize the need of capital with something they base their business on. This is where direct marketing comes into play. If you remind them of who you are and that you are to assist them to manage the most stressful money making times of the year, they will think of you as their go-to when they NEED it.

Some deBanked Swag to Go With Your Magazine

August 24, 2015Some lucky funders and ISOs will receive a Dunkin’ Donuts gift card along with their deBanked magazine shipment thanks to Lenders Marketing, a trigger lead company specializing in merchant cash advance and business loan leads. The gift cards are in limited supply and recipients are being selected at random.

A similar swag lottery took place with deBanked’s May/June issue where dozens of recipients received a Starbucks gift card with their magazines. Those were also courtesy of Lenders Marketing.

And in related news, pictured below in the green Lenders Marketing hat is professional golfer Michael McCabe during the PGA Tour Barracuda Championship in Reno, Nevada. Behind him to his left in the white hat with sunglasses is Justin Benton of Lenders Marketing.

Will You be at Lend360?

August 20, 2015This year’s Lend360 conference in Atlanta, GA is shaping up to be one of the industry’s biggest events. A welcome respite for some from the typical trek out to New York, San Francisco, and Las Vegas, the show is being hosted in the same neighborhood as industry leaders CAN Capital and Kabbage.

Just take a look at the speaker lineup so far:

You can register here. Hope to see you there!

deBanked Photo of the Day

August 18, 2015This photo of the Central Diligence Group team was recently posted to our forum. By the look of their reading material, it appears they are thoroughly deBanking.

Central Diligence Group is an NYC-based MCA underwriting & consulting firm.

Thanks for sharing this!

Reactions to the Treasury RFI: Business Lenders and Merchant Cash Advance Companies Share Their Thoughts

August 13, 2015 The Treasury Department could get an earful from the alternative funding industry during a 45-day public comment period on online marketplace lending that began July 17.

The Treasury Department could get an earful from the alternative funding industry during a 45-day public comment period on online marketplace lending that began July 17.

Treasury emphasizes that it isn’t a regulator and its Request for Information, or RFI, isn’t a regulatory action. The department just wants to hear success stories and opinions on potential public policy issues, a Treasury spokesman said.

“There isn’t a lot of data available on this industry,” the spokesman noted. “The RFI allows us to gather information from the public.”

One portion of the public – alternative funding executives – may have a lot to say on the subject. At least some of the industry’s top players favor regulation or legislation that could clean up the industry and clarify conflicting directives.

“Personally, I’d be glad to see it on the federal level,” Stephen Sheinbaum, president and CEO of Merchant Cash and Capital, said of regulation. “We won’t have to deal with 50 individual states, which is more unruly.”

Others would prefer to see the industry regulate itself instead of having federal agencies issue dictates or having Congress pass laws.

“I would like to put in my two cents,” said Asaf Mengelgrein, owner and president of Fusion Capital, indicating he intended to respond to the RFI. “I see a need for better practices, but regulation should come internally.”

Whoever makes the rules, restrictions seem inevitable because of alternative funding’s prodigious growth, executives agreed. “Regulatory attention is a sign of an emerging industry,” said Marc Glazer, president and CEO of Business Financial Services.

Regulation should curb the practice of stacking loans or advances, which can burden merchants with more financial obligations than they can meet, Sheinbaum said. Stacking has proliferated even though ethical members of the industry avoid it, he said.

At the same time, disclosure statements should become more transparent so that merchants can easily identify how much they’re paying in fees and expenses, Sheinbaum maintained. Merchants should also be able to see how much they’re paying the different entities involved in the deal, he said.

“I’m not suggesting someone should make more or less, but transparency is a healthy thing and this industry could use a little more of it,” Sheinbaum said.

The alternative-funding industry could follow the example of the mortgage business, where more-standardized forms help consumers compare competing offers, Sheinbaum said. “That’s not the case in this industry, so that might help,” he maintained.

The alternative-funding industry could follow the example of the mortgage business, where more-standardized forms help consumers compare competing offers, Sheinbaum said. “That’s not the case in this industry, so that might help,” he maintained.

The industry should not emulate the credit card processing business, which uses complicated and dissimilar contracts to keep customers uniformed, Sheinbaum said. “It’s not so easy for a merchant to understand the effective cost of a transaction – and that’s by design,” he said.

Reviewing those issues could confuse among regulators who don’t understand the industry, Mengelgrein warned. Someone “on the outside looking in” might consider the industry’s fees and factor rates outrageously high, but that’s because they fail to understand the financial risk involved with lending to small businesses, he said.

Before imposing rules, regulators should also bear in mind that many small businesses could not survive without alternative funding, Mengelgrein continued. In recent years banks have failed to step up and help merchants in need of cash, and the alternative lending community has filled the gap.

Sheinbaum agreed. “I hope the regulators and legislators will make an earnest effort to understand all the good that folks in the alternative finance space provide for people,” he maintained. “It’s a critical role we play in keeping small businesses going, and small business is important to this country.”

The Small Business Finance Association could play a critical role in helping government understand the industry, Sheinbaum suggested. He noted that the trade group changed its name from the North American Merchant Advance Association because the industry is adding loans to its initial offering of merchant cash advances.

Whatever shape regulation takes, the industry should keep up with the new rules, Glazer cautioned. “As this industry evolves, we will work closely with our partners and our customers to ensure that everyone is informed about any new regulations and the potential impact that they may have on our business,” he said.

Meanwhile, Treasury’s efforts to comprehend the business are continuing. Its RFI contains 14 detailed questions that respondents could address.

The department held a forum on Aug. 5 called “Expanding Access to Credit through Online Marketplace Lenders.” The event included two panel discussions and roundtable discussions with Treasury staff.

Attendees numbered about 80 and included consumer advocates, representatives of nonprofit public policy organizations and members of the financial services industry, the department said.