Herio Capital Breaks $20 Million in Funded Deals

March 9, 2016 It might feel like 1997, but in early 2016 Herio Capital has surpassed $20 million in funding since inception. Co-founded by Sherif Hassan, the company’s chief executive, Herio launched only one year ago. Hassan was one of OnDeck’s first employees who stayed with the company all the way up until just before they went public.

It might feel like 1997, but in early 2016 Herio Capital has surpassed $20 million in funding since inception. Co-founded by Sherif Hassan, the company’s chief executive, Herio launched only one year ago. Hassan was one of OnDeck’s first employees who stayed with the company all the way up until just before they went public.

Today, Hassan does not appear to be regretting that choice. “We have lots to be grateful for and even more to be excited about in 2016,” he said.

The company’s chief product officer and co-founder, Patrick Janson, summed up their vision like this, “When we started Herio, we saw a huge opportunity to improve upon the software that currently supports the marketplace lending industry.”

The Herio team will be attending the LendIt Conference in San Francisco next month.

“Reaching the $20 million funding milestone is a testament to the execution, creativity, and diligence of everyone at Herio. We are grateful to our team and our loyal industry partners. We are excited about the advancements our industry will make in the next period as we continue to design the future of credit,” concluded Hassan.

Yellowstone Capital Welcomed to New Office Location By City Mayor

March 8, 2016 It’s a change of scenery, insiders at Fundry subsidiary Yellowstone Capital say about their new office.

It’s a change of scenery, insiders at Fundry subsidiary Yellowstone Capital say about their new office.

The company has officially relocated from 160 Pearl Street in Manhattan to 1 Evertrust Plaza in Jersey City. On their first day in the new location, Jersey City Mayor Steven Fulop made an appearance and posed for a photo with company executives Isaac Stern and Jeff Reece to celebrate their arrival. Aside from outgrowing the NYC office that they operated from for years, Yellowstone was wooed to the State by the New Jersey Economic Development Authority to create jobs in the area in exchange for a tax incentive. The hundreds of employees they bring with them to the neighborhood now will also serve to stimulate Jersey City’s burgeoning economy.

The company originated close to half a billion dollars in funding for small businesses in 2015.

Just one stop from the Path Train’s World Trade Center station, Yellowstone’s new office environment makes it feel as if the company has been transported a million miles away. deBanked was given a tour of the new space, which at 25,000 square feet, was easy to get lost in. One employee said the upgrade from their previous location felt so immense, that it felt like they had moved to Japan.

Just one stop from the Path Train’s World Trade Center station, Yellowstone’s new office environment makes it feel as if the company has been transported a million miles away. deBanked was given a tour of the new space, which at 25,000 square feet, was easy to get lost in. One employee said the upgrade from their previous location felt so immense, that it felt like they had moved to Japan.

A clear view of NYC’s Freedom Tower from many of the floor’s windows assures them that they are not that far.

Merchant Cash Advances Costly But Not Opportunistic, Fed Study Finds

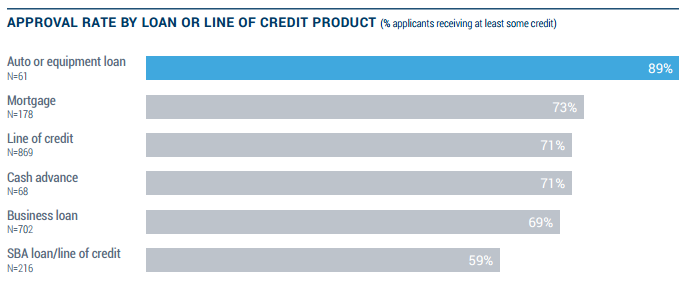

March 6, 2016Only 71% of business owners that apply for a merchant cash advance actually get approved for them.

Equipment loans, commercial mortgages, and company vehicle loans all have higher approval rates than merchant cash advances, a comprehensive Federal Reserve study revealed. Lines of credit were approved just as often as merchant cash advances. Right behind them were business loans and SBA loans at approval rates of 69% and 59% respectively.

The statistics disprove the theory that merchant cash advance companies don’t underwrite or that they are doing so recklessly at the expense of their small business customers.

Only 7% of small businesses have ever even applied for a merchant cash advance.

The propensity to apply for a merchant cash advance ranked higher among businesses less than two years old and those seeking less than $100,000.

Notably, small businesses reported being much less satisfied with online lenders than banks, but overwhelmingly cited cost as the reason behind it. Big banks scored worse on transparency than online lenders among dissatisfied borrowers.

The findings are not surprising. 35% of small businesses said that speed of the decision process was a factor influencing where they applied. 37% said ease of the application process was a factor and 40% said the perceived chance of being funded played a role.

In these areas, online lenders walloped small and large banks. More than 50% of dissatisfied bank borrowers fingered a difficult application process as a reason and more than 40% said it was the long wait for a credit decision.

The results fall in line with expectations, that speed and ease often come at a cost. However, merchant cash advance companies do not appear to be approving applicants just to opportunistically charge a high fee. The approval rates are in line with other types of financial products, and are even less likely to be approved than a mortgage.

PayPal’s Merchant Cash Advance Program Grows, Performance Improves

February 27, 2016The PayPal Working Capital program has advanced more than $1 billion to small businesses since inception. Rooted in merchant cash advance methodology since PayPal withholds a percentage of each transaction until receiving payment in full, they are not actually buying future receivables. Rather, they originate loans through WebBank, the same Utah-chartered industrial bank that OnDeck uses. But OnDeck’s payments are fixed and PayPal’s are tied to sales activity.

PayPal’s loans therefore don’t have a fixed term but they evaluate historical sales activity and use that to project a loan payoff usually within 9 to 12 months. According to their Q4 2015 earnings report, their 2015 results performed just as well if not better than their 2014 results.

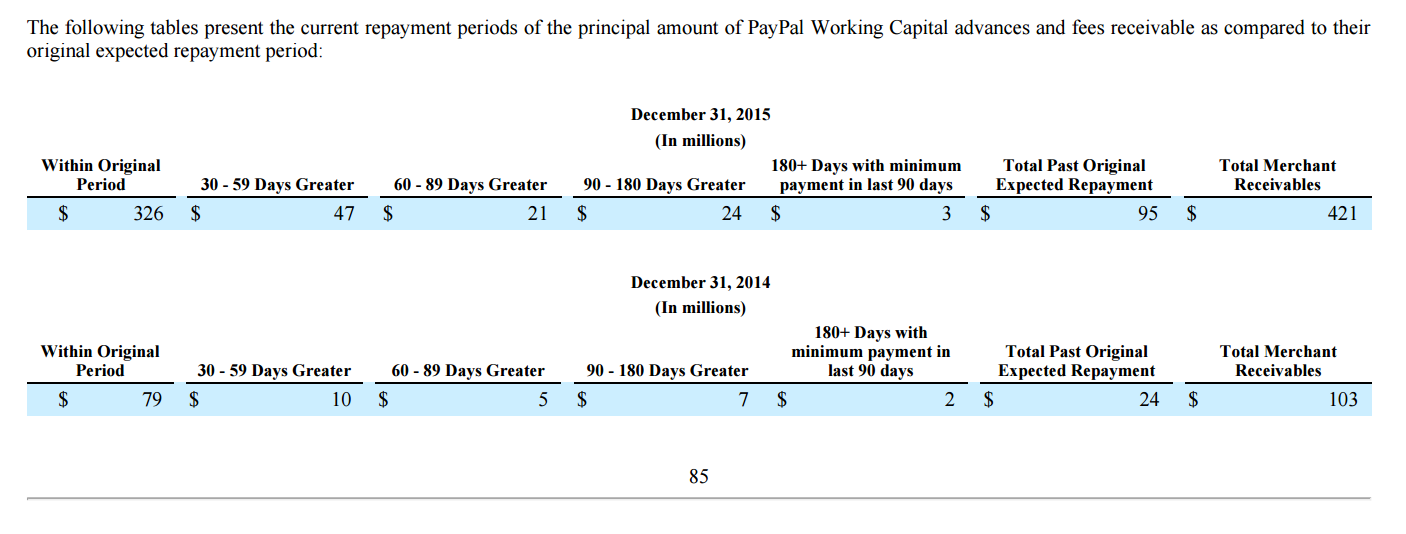

$421 million was outstanding at the end of 2015 compared to $103 million at the end of 2014. 77% of the $421 million was on pace to pay off within 30 days of their planned projections. 11.16% was on pace to finish 30-59 days beyond them. PayPal broke it down by dollars in their earnings report.

But we’ve broken it down into percentages below:

| Total outstanding balance | Within Projections | 30-59 days greater | 60-89 days greater | 90-180 days greater |

| $421 million | 77.43% | 11.16% | 4.99% | 5.70% |

| Total outstanding balance | Within Projections | 30-59 days greater | 60-89 days greater | 90-180 days greater |

| $103 million | 76.70% | 9.71% | 4.85% | 6.80% |

PayPal borrowers cannot simply stop accepting PayPal payments in order to avoid loan repayment. They are required to pay at least 10% of their total loan amount (loan + the fixed fee) every 90 days so that they make consistent repayment progress regardless of their sales volume. Notably, their website warns, “If you do not meet the requirements in the above policies and your loan goes into Default status, your entire loan balance could become due and limits could be placed on your PayPal account.” For businesses that depend on PayPal sales, that is certainly a downside worth avoiding.

Steal A Deal, Go To Jail – MCA Broker Takes Fight Over Backdoored Deals To Law Enforcement

February 22, 2016 A suspicion over stolen deals has led to the arrest of a sales agent, deBanked has learned.

A suspicion over stolen deals has led to the arrest of a sales agent, deBanked has learned.

It’s yet another case of a deal slipping out the back door, one that resulted in handcuffs, according to multiple sources familiar with the matter. deBanked obtained evidence of the arrest, which happened earlier this month, and confirmed the identity of the individual charged.

A sales agent’s ill-fated meeting with law enforcement began when an MCA brokerage suspected their hard-fought applications were being rerouted to a third party by way of a New York based funding company they usually submit to, according to one source. To confirm these suspicions, they submitted at least one funding application that was tagged with a specially designated phone number that they possessed. The tactic would allow them to do a clean trace on their deal by seeing who called upon that number, multiple sources confirmed.

Sure enough, someone other than the funding company reached back out to them, not knowing it was a trap. Unfortunately, that call wasn’t conclusive enough to connect it to the funder, according to one source. The sales agent attempting to snatch the deal wasn’t employed by the funder and the funder wasn’t sure how the sales agent was getting the deal in the first place. Somehow this guy was getting data he wasn’t supposed to be getting and the funder wanted nothing more than to make sure their integrity remained intact, a source said.

The victimized brokerage set their sights on the rogue sales agent and together with the cooperation of the local police department, apparently staged a sting operation. The rogue agent allegedly attempted to sell the stolen deal data to an undercover cop who was assisting with the case.

The suspect was charged with criminal possession of computer related material, a Class E felony, and released on recognizance three days later, according to arrest records obtained by deBanked. The penalty for such a crime can earn an offender up to 4 years in prison.

The funding company and brokerage are reportedly both relieved to have gotten to the bottom of the issue. Notably, in this case of deals slipping out the back door, it was the alleged recipient of the stolen deals that was charged. The hole that allowed him to get those deals in the first place has apparently resolved itself, sources said.

In the September/October 2015 issue of deBanked Magazine, interviewed MCA brokers agreed that the industry should police itself when it comes to backdooring. One brokerage, although not one that was named in that article, apparently took that advice literally when they enlisted the police to assist them.

All the sources to this story agreed that the arrest should serve as a warning. Backdooring deals has to stop, they concurred.

—

The name of the accused and the names of the sources in this story were kept anonymous because it’s an ongoing criminal matter. The suspect is innocent until proven guilty.

Loan Brokers or Self Origination? Here’s What Experts Say

February 22, 2016 Last year belonged to the brokers in alternative finance — with a phone and a few leads pulled up online, anyone could sell a loan. With seemingly no barriers to entry, alternative lending attracted auto and insurance salesmen fleeing their jobs to cash in on the gold rush in an economy which was coming out of the shadows of distrust for big banks. And it found quick ascension to grow into a trillion dollar market.

Last year belonged to the brokers in alternative finance — with a phone and a few leads pulled up online, anyone could sell a loan. With seemingly no barriers to entry, alternative lending attracted auto and insurance salesmen fleeing their jobs to cash in on the gold rush in an economy which was coming out of the shadows of distrust for big banks. And it found quick ascension to grow into a trillion dollar market.

But a year on, as the dust has settled, we asked industry veterans what it means to remain successful in this business and what is the key to sustainability — is it in going for the ISO/broker channel to find deals or originating your own.

Here’s what they had to say

Don’t Break the Broker

Tom Abramov of MFS Global voted for the ISO/broker channel and said that that’s how the company strictly does deals, working with brokers who have a track record as a part of their recruitment system. The six year old company that started as an broker shop now focuses only on funding with products that are a mix of merchant cash advances and lines of credit.

“We don’t look at FICO scores or SIC codes, we only look at cash flows of businesses,” said Abramov. “I want to see if I give a someone a dollar whether they can turn it into two.”

Abramov added that his firm offers brokers 20 percent commission and their default rates are sub 5 percent.

The advantages of scoring deals through a broker channel can be alluring. It involves no overhead, no staff that needs compensation, motivation and incentives, and makes use of the existing broker-merchant relationships.

Jordan Feinstein of NuLook Capital said that his firm works with brokers exclusively and the model has helped them respond to merchants faster. “We do not have a sales team speaking to merchants directly, that’s in conflict with our model,” said Feinstein. “We decided that the best way to grow is to build relationships to avoid the overhead, compliance, training and manpower that a sales team would require,” he said.

Building a Hybrid Model

There are some others who want to make the best of both the models and work with brokers while originating and funding their own deals. Forward Financing which uses a hybrid model has strategic partnerships with some brokers while still originating their own deals. “We have a hybrid model because our goal is to have a program for any type of business and work with companies across the spectrum of risk,” said Justin Bakes, CEO of Forward Financing. “While our priority is to self originate, it is essential to create and maintain partnerships in this business,” he said.

The Original Origination

While the allure of a lean business is certainly attractive, there are some who are in the industry to build a bigger business and create value by making it robust — Jared Weitz of United Capital Source is one of them. “There is a big market for both analytical process as well as sales process. It’s important to go after your strength,” said Jared Weitz, founder and CEO of United Capital Source. “When you originate and fund your own deals, you’re in a rewarding position and in control of how merchants get treated.”

Industry Trends

Speaking of the industry in general, these experts agreed that the business was undergoing a change with new entrants coming in and experimenting with better services and technologies.

“Last year was the year of brokers but we are still missing the education with merchants. Some brokers are interested while some are not,” said Abramov.

“I notice a clear difference between the old and the new in terms of technology and pricing model,” said Bakes.

“New funders are coming in with different products and terms with increased competition in the ISO market,” said Feinstein.

“Marketing is getting more expensive and only the ones who can afford to pay can play,” said Weitz.

‘Year of the Broker’ Gives Way to ‘Year of the Reduced Commission’

February 21, 2016 Many brokers just starting out in the alternative funding space may be in for a rude awakening. It’s not that the ‘Year of the Broker’ is over, per se, but 2016 certainly represents a new chapter for newbies—one in which getting rich quick and succeeding over the long-haul will be much more difficult.

Many brokers just starting out in the alternative funding space may be in for a rude awakening. It’s not that the ‘Year of the Broker’ is over, per se, but 2016 certainly represents a new chapter for newbies—one in which getting rich quick and succeeding over the long-haul will be much more difficult.

“It’s the ‘Year of the Leader’ now. Fresh brokers coming into our space will have to work harder to set themselves apart, and it will be harder for many of them to make the money they once did,” says Amanda Kingsley, chief executive of Sendto, a Palm Bay, Florida-based firm that assists companies in the alternative finance industry with referral marketing and operational growth programs.

Funders today remain hungry for deals and are still paying relatively high rates to bring in new business. Yet there are several competitive realities putting a damper on a new broker’s earnings power.

“A few years ago, individual brokers could be making $20,000 or even $40,000 a month. Now those numbers are much more difficult to reach unless brokers have a unique lead generation method or their own money to participate in the deals,” says Zachary Ramirez, a vice president and branch manager in the Orange, California office of World Business Lenders, a New York-based lender.

Most funders today allow brokers to charge merchants between 8 and 12 points above the buy rate, with some allowing as high as 15 to 20 points, according to industry participants. But to win business amid a flurry of competition, brokers are being forced to take a lower cut on many deals. Not only are there more brokers to compete with, but merchants are also savvier—and more price-conscious—about alternative funding products than they were several years ago.

For higher quality deals, there’s another force at play driving down what sales reps can earn. That’s because a handful of large funders are instituting caps on what brokers can charge top-quality merchants. “They want to make sure that the price that’s charged to the merchant is fair,” says Stephen Sheinbaum, founder of Bizfi, a New York-based funder that has not instituted these caps.

Together, these competitive realities mean that sales reps, on average, are making much less than they did a few years ago. For example, on high quality deals, brokers might only be able to make 3 to 8 points per deal on average. For lower quality deals, on the other hand, brokers might make as much as 15 to 20 points.

So far, the changing economic tide hasn’t discouraged new sales reps from jumping in. In fact, the market is still hot for new brokers who continue to pour into the market at a torrid pace, buoyed by rampant media attention and aggressive advertising by funders and large brokerage houses. “I think it’s even worse now,” says John Tucker, a solo broker since 2009 who also blogs for DeBanked. “They’re signing up anybody with a heartbeat and a pulse.”

Clinging to Misperceptions

Despite the overcrowding issue, industry watchers expect new brokers will continue to flood in as alternative funding continues to gain traction. Many of these new brokers, however, won’t be around very long. That’s because many of them are coming into the space, especially from other sales-oriented jobs, thinking it’s easier than it is. “I think many people are going to come into the space, fail and leave bloodied and bruised,” says Ramirez of World Business Lenders.

Indeed, there are many new brokers who are still holding on to outdated notions about the business. Some are primed to think that they can easily make 10 points on a $100,000 deal and if they do that once a month, they have the potential to make $120,000 a year. “It’s just not as easy as it’s promoted to be,” says Tucker, who owns 1st Capital Loans in Troy, Michigan. Even Tucker, a seasoned broker, frequently has trouble connecting with merchants nowadays because they are inundated with sales pitches. They’ll hang up on him as soon as he makes it clear he’s a broker because they are getting so many calls from competitors, he says.

William Ramos, owner of Right Away Funding in Phoenix, Arizona, recently worked with a new broker who was convinced he was going to make $5,000 a week from the get-go. Ramos tried to manage his expectations by explaining he’d first have to learn the business and be persistent if he hoped to make that kind of money.

Ramos says the broker took his advice by asking lots of questions and working hard over the next six months. He’s not making what he had originally hoped, but he is up to about $5,000 a month, says Ramos, the former president of Staten Island, New York-based Supreme Capital Group, which he sold in 2015 to open a new firm.

Ramos says the broker took his advice by asking lots of questions and working hard over the next six months. He’s not making what he had originally hoped, but he is up to about $5,000 a month, says Ramos, the former president of Staten Island, New York-based Supreme Capital Group, which he sold in 2015 to open a new firm.

In talking to new brokers, Nathan Abadi president of Excel Capital Management in New York, a lender and MCA funder, also sees a lot of misconceptions about what they think they can make and how easy it will be. It becomes problematic when the reality doesn’t match up with their expectations. For instance, he recently hired a used car salesman who worked for his company for about two months before they parted ways. The broker thought that because he had sold so many cars in the past, he could easily apply that to alternative funding. But he didn’t want to take the time to thoroughly learn about the new product set. He was just trying to ink deals based on cost, which is no longer a viable strategy, Abadi explains. “Customers know what the rates are. They’re not just applying with one person,” Abadi says.

The first month, the new broker closed a $175,000 deal based on a lead he was given and with Abadi doing the bulk of the legwork. After that, the broker got a few more deals, but he couldn’t do it on his own without significant support from the firm. A big problem was that he didn’t understand the math behind the deals he was pitching. “If merchants ask you a question and you can’t answer it properly, you’re done. The deal’s over. Not enough people are taking the time to understand the market as a whole,” says Abadi, whose firm is in the process of hiring new brokers for its internal sales force.

Edward Siegel, founder and chief executive of Fundzio LLC, a funding company in Fort Lauderdale, Florida, says he still sees plenty of new brokers who come into the business believing they can easily close a deal for $50,000, make 10 points and sustain that type of income. “The market has changed. The cost of capital has gotten a lot lower for the customer, and since there are more brokers in the marketplace they are willing to take a lesser amount just to get the deal to the finish line,” he says.

A lot of brokers come into the industry all gung ho and then flounder when they see how hard it really is. Siegel says he’s seen them submit deals for a few months and then realize they were living a pipe dream and leave the industry. “It’s not easy, especially in a competitive marketplace, especially when 10 other brokers might be knocking on that same guy’s door,” he says.

Nearing the breaking point

Andrew Reiser, chairman and chief executive of Strategic Funding Source, a New York-based funder, says that many brokers are operating under a false sense of security. “We’re in a strong economy in our space largely because of lack of other available sources of capital from larger institutions. When a market is very forgiving, mistakes are easily absorbed and swept under the carpet.”

He believes it’s going to get even harder for brokers over time, likening the situation with brokers today to that of stockbrokers a few decades ago. People used to be inundated with calls from stockbrokers at firms of all sizes about this stock or that one. Now many small brokerage houses have disappeared and larger firms have moved away from cold calling. Instead they are focused on money management and proving their prowess as specialists.

“You can’t be all things to all people serving a market this size,” he says.

Survival Strategies

Kingsley of Sendto says she receives many questions from new brokers about how to compete effectively, and it’s not an easy answer. Having a niche product, though, can help. “If you can learn how a particular industry works along with appropriate deal placement, you can develop a really good client base. It helps when presenting your clients to funding companies and you will build a more professional relationship,” she says.

Tucker, the broker with 1st Capital Loans, notes that UCCs and Aged Leads are outdated marketing tactics and says most new brokers don’t have enough industry knowledge to critically think to create new strategies for survival. “All they will end up doing is burning through the little capital that they do have and be out of the business within 12 to 18 months,” he says.

Tucker, the broker with 1st Capital Loans, notes that UCCs and Aged Leads are outdated marketing tactics and says most new brokers don’t have enough industry knowledge to critically think to create new strategies for survival. “All they will end up doing is burning through the little capital that they do have and be out of the business within 12 to 18 months,” he says.

Having good training is critical for new brokers to survive, according to Mike Andriello, president of Cushion Capital Corporation in Poughkeepsie, New York. “I think that if brokers focus on the nature of the industry, actually pick the business owners’ minds and learn their business as best as they can, they will have a lot of success. It’s not all about making the biggest commissions; it’s about having the biggest client book,” he says.

Ramirez of World Business Lenders believes brokers can do better for themselves long-term by syndicating because it’s a way to make more money. “I don’t think it’s a long-term strategy if a broker’s not participating in his own deals,” he says.

Granted, some funders make it easier for brokers to participate than others do, but Ramirez believes brokers should seize opportunities to earn interest income over the life of the loan. So, for instance, on a $100,000 loan, instead of earning a $20,000 commission upfront, a broker might be able to apply that money to the deal and earn $26,000 or $28,000 over the life of the loan.

Granted, some funders make it easier for brokers to participate than others do, but Ramirez believes brokers should seize opportunities to earn interest income over the life of the loan. So, for instance, on a $100,000 loan, instead of earning a $20,000 commission upfront, a broker might be able to apply that money to the deal and earn $26,000 or $28,000 over the life of the loan.

Of course, this strategy won’t work well for brokers living paycheck to paycheck. “But if you don’t need the commissions right away, you can roll the commissions into deals and increase your earnings exponentially,” he says. “Because of rising acquisition costs and decreased commission averages per deal, being forced to participate, or syndicate, is the natural evolution.”

Gearing for the Future

To be sure, industry watchers believe there is still ample opportunity for new brokers with drive and ambition to enter the space. “Successful brokers will always have a place in the ecosystem,” says Sheinbaum of Bizfi.

But there’s a general consensus that from now on these brokers will have to work harder than they have in the past to thrive. Says Andriello of Cushion Capital: “2016 will be the year of who was smart enough and made the right business moves to stay progressing and growing. It will also be the year a lot of funders and brokerage firms close shop.”

Over time, the changing economic reality will continue to set in. While it will be harder for individual brokers, it’s best for the industry when new sales reps understand the realities of the market and how to compete effectively. “You want the smartest people in the space. The more well-educated they are about the products and the processes, the better off everyone is,” Sheinbaum says.

Despite everything, it’s still a great time to be getting into the industry, provided you have the right mindset and proper resources behind you, according to Ramos of Right Away Funding. “If you’re just coming in and you just want to collect your weekly check, now’s not a good time to be a broker. It’s a great time for people who are hungry, motivated and determined to make something out of it.”

Did BFS Capital Trade Going Public for a Bigger Credit Line?

February 4, 2016 BFS Capital secured a $165 million credit line through Wells Fargo Capital Finance with an additional increase of up to $250 million. This agreement extends the former line of $135 million and will help the Florida based small business lender to service merchants in North America.

BFS Capital secured a $165 million credit line through Wells Fargo Capital Finance with an additional increase of up to $250 million. This agreement extends the former line of $135 million and will help the Florida based small business lender to service merchants in North America.

The company had an eventful 2015 — In July last year, it funded $1 billion worth of deals and acquired New York-based financial services firm Entrust Merchant Solutions in August. It also rebranded itself from Business Financial Services Inc.

Interestingly enough, as deBanked reported in September last year, the company filed for an IPO and submitted a draft registration statement on Form S-1 with the Securities and Exchange Commission (the “SEC”) relating to the proposed initial public offering of its common stock.