Are Lawsuits the New UCCs?

December 5, 2017 Back when merchant cash advance funders first began to file UCCs, competitors immediately began to look them up and turn them into leads. The practice became so widespread that MCA funders began filing under pseudonyms to throw people off the scent. But soon, competitors began to figure out who the pseudonyms belonged to and the game continued. Funders tried other methods like having the UCC service providers themselves be named as the secured parties. Eventually, competitors realized that although they couldn’t figure out who the true secured party was on these, they could at least reasonably identify the named debtor as having obtained funding. Eventually some funders gave up and stopped filing UCCs altogether.

Back when merchant cash advance funders first began to file UCCs, competitors immediately began to look them up and turn them into leads. The practice became so widespread that MCA funders began filing under pseudonyms to throw people off the scent. But soon, competitors began to figure out who the pseudonyms belonged to and the game continued. Funders tried other methods like having the UCC service providers themselves be named as the secured parties. Eventually, competitors realized that although they couldn’t figure out who the true secured party was on these, they could at least reasonably identify the named debtor as having obtained funding. Eventually some funders gave up and stopped filing UCCs altogether.

These days, a new breed of public records detectives are harvesting the NY state court records for lawsuits against merchants in default. Though they don’t always wait until a merchant has already been sued, the public dockets make it easy for them to obtain all the details they need to pitch services such as debt settlement and legal aid.

An unfortunate consequence of that is that these so called advocates may not have the merchants’ interests at heart and they can greatly complicate communication between the parties.

See previous coverage:

- 4th Alleged Co-conspirator in Fake Debt Settlement Company Arrested

- ISOs Alleged to Be Partners in Debt Settlement “Scam” in Explosive Lawsuit

- Is The End Near For This Debt Settlement Firm?

- A Tale of “Debt Restructuring”?

The practice of trolling the dockets is becoming so popular that a similar trend may be cropping up, funders filing lawsuits under obscure entity names. While it’s too early to tell if debt settlement lead hunters could get so aggressive as to actually make it untenable to file a lawsuit or a confession of judgment, it is something to keep an eye on. Unlike a UCC, which may only reveal a description of the secured interest and the merchant’s name, the dockets may reveal the actual contract itself, all of the terms, what platform it was funded on, how much remains outstanding, etc. There’s vastly more than could ever be gleaned from a UCC. The downside, of course, is that it suggests a merchant breached a contract and may not be an ideal candidate for additional funding. But to a debt settlement firm (unsavory or not), that might just be the prospect they’re looking for.

Are lawsuits the new UCCs? Time will tell.

Yellowstone Capital Funds $100 Million Over Last 60 Days

December 1, 2017An email circulated by Jersey City-based Yellowstone Capital yesterday, confirmed that the company had originated $50 million in deals for the month of November. The figured tied the record set in the previous month, bringing the 60-day total to $100 million.

Two sales representatives ended up in a tie for top performer of the month, each originating $4.65 million. Juan Monegro, whom deBanked interviewed almost two years ago, was right behind them at $4.55 million.

ISO Roadmap For 2018

November 26, 2017ISOs, as you finish out a wild year of funding, we’ve put together a roadmap to prepare you for a very successful 2018!

1. Educate yourself. Litigation in the MCA industry skyrocketed in 2017. That means as a salesperson you’re  more accountable than ever to communicate the products and services you sell in a succinct and truthful manner. Case in point, MCAs are offered by funders, not lenders. Using lending-related terminology at any point during the sales process for non-lending products can open yourself up to both legal or regulatory consequences, even if you’re just an employee. As these fundamentals apply to industry veterans as well as newcomers, your top priority in the new year should be to get a certificate in Merchant Cash Advance Basics.

more accountable than ever to communicate the products and services you sell in a succinct and truthful manner. Case in point, MCAs are offered by funders, not lenders. Using lending-related terminology at any point during the sales process for non-lending products can open yourself up to both legal or regulatory consequences, even if you’re just an employee. As these fundamentals apply to industry veterans as well as newcomers, your top priority in the new year should be to get a certificate in Merchant Cash Advance Basics.

2. Source your own leads. Sneaking deals out the backdoor or being on the receiving end of ill-gotten leads may yield a couple bucks but it may ultimately come at the expense of your reputation and career. It could also be against the law. The surefire way to become a legitimate top performer in the industry is to generate your own deals. How else do you expect to build a book of business that’s truly yours and relationships with clients that are built on trust and integrity? Need help getting started? Check out this list of lead sources!

3. Participate in industry events. In 2018, it will pay to truly  know who you’re working with. Sending your deal off to some random person you’ve never met claiming to be a funder or lender is a great way to increase the odds that your deal and potential commission will disappear. Fortunately in the coming year, there are great opportunities to network with industry colleagues. Here’s a link to one deBanked hosted this past August at Marine Park Golf Course in Brooklyn. If you’re a sales rep in the South Florida area, you should attend deBanked’s FREE cocktail networking event in South Beach on January 25, 2018. And if you want to better your skills, discuss the issues, and connect with the industry, you should register for Broker Fair 2018 right now! Check out the list of companies that have signed on to sponsor it already. Broker Fair 2018 is the number one don’t-miss event of the coming year.

know who you’re working with. Sending your deal off to some random person you’ve never met claiming to be a funder or lender is a great way to increase the odds that your deal and potential commission will disappear. Fortunately in the coming year, there are great opportunities to network with industry colleagues. Here’s a link to one deBanked hosted this past August at Marine Park Golf Course in Brooklyn. If you’re a sales rep in the South Florida area, you should attend deBanked’s FREE cocktail networking event in South Beach on January 25, 2018. And if you want to better your skills, discuss the issues, and connect with the industry, you should register for Broker Fair 2018 right now! Check out the list of companies that have signed on to sponsor it already. Broker Fair 2018 is the number one don’t-miss event of the coming year.

4. Keep up on the news. Keep up on  developments taking place across the entire alternative finance spectrum. The best part about deBanked magazine is that it’s free to subscribe. We publish six issues a year. Copies can be mailed to your home or office in print free of charge. Magazine content is typically distributed in print before it ever comes online so don’t miss out. Make sure the next deBanked magazine will be coming your way in 2018!

developments taking place across the entire alternative finance spectrum. The best part about deBanked magazine is that it’s free to subscribe. We publish six issues a year. Copies can be mailed to your home or office in print free of charge. Magazine content is typically distributed in print before it ever comes online so don’t miss out. Make sure the next deBanked magazine will be coming your way in 2018!

5. Choose your partners wisely. In the same way that it’s probably not a good idea to send your deal off to a random funder that cold called you, using old-fashioned methods like Google to discover who’s who can be onerous. That’s why we’ve segmented our sponsor directory by business type so that you can narrow down the right partner to fit your needs fast. While it’s true that these companies pay to advertise here, it’s an excellent starting point. So check out our list of sponsors!

Canadian Merchants Show An Appetite For Capital

November 25, 2017In Canada, the average deal size for a merchant is anywhere between $20,000 and $30,000 in funding, depending on who you ask. That’s why when one startup recently funded a $300,000 CAD advance from its balance sheet to a Canadian merchant, the deal turned some heads. While it’s unclear whether this amount could be indicative of a trend unfolding at our neighbors to the North, Canadian small businesses are preparing for some changes in the industry landscape in 2018.

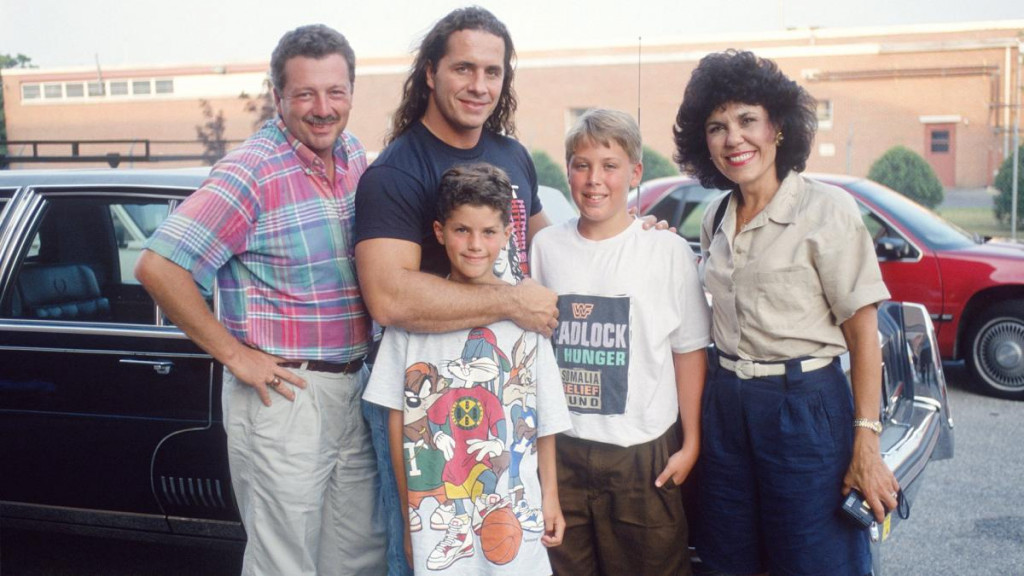

SharpShooter Funding, whose name depicts the famous wrestling move of the WWE’s Bret “The Hitman” Hart, was behind the $300,000 deal with an Eastern Canadian grocer.

If you’re wondering how a merchant funder and WWE legend became partners, chalk it up to a combination of fate and timing. Paul Pitcher, SharpShooter Funding managing partner, has been Hart’s biggest fan since he was a kid. Pitcher got the opportunity to meet his hero when was just 10 years old. It was then that the green shoots of friendship formed, and today the WWE’s Hart is acting commissioner of SharpShooter Funding, having helped to launch the business.

Canadian Merchant Landscape

To get a taste of the Canadian merchant financing landscape, consider that the three top Canadian funders deploy $20 million and $25 million per month combined, explained David Gens, president and chief executive of Merchant Advance Capital, which is included among the top three funders. That’s up from a range of $15 million to $20 million earlier this year.

And while a $300,000 advance may not seem like something to write home about for U.S. funders, it’s a big deal in the Canadian market. The culture among small businesses in the Great White North is different and more conservative than their US counterparts.

“It’s a function of the size of the merchant,” Gens explained. “The typical single-location storefront merchant is going to qualify for $30,000 to $50,000. It takes a larger and more established business, whether it’s a multi-location merchant or a business that is in the B-to-B space, a manufacturer, distributor or wholesaler to be large enough to qualify for large financing.”

Meanwhile there are some changes to small business taxation that are coming down the pike that may influence demand for credit, Gens noted, though the precise shape any changes to the tax law will take remains unclear.

“They will reduce the small business taxation rate on the face of it. But for businesses where they hold cash or need to hold cash, it’s a gray zone as to whether or not they will be able to hold financial assets in those businesses. The government is going after companies that are holding investments. But there’s a gray line as to what is a holding company that is holding an investment and an operating company holding a buffer because of seasonality or cyclical demand. We have yet to see what the rules end up being exactly,” Gens said.

Anatomy of the Deal

In the case of SharpShooter Funding, the grocer merchant originally came to the funder for less than $300,000 but qualified for more, bringing the funder’s tally for a single day’s deals to more than $500,000.

“We never thought we’d hit this milestone in the Canadian market. But the file was right, and the timing was great,” Pitcher told deBanked. Now that they’ve gotten a taste of it, SharpShooter Funding hopes to do more deals of this nature. “For a small funder like us to double the size of a big funder was a big moment for us, especially in the Canadian market,” Pitcher said.

Merchant Advance Capital’s Gens said his company is prepared to take on the risk for deals at even a higher threshold. “Our average is $35,000 to $40,000, and the largest deal we’ve ever done was $600,000. I don’t want to steal their thunder, but there have been larger deals,” said Gens. “A few funders may syndicate when deals get that big, but it’s not an inconceivable size.”

OnDeck, which similarly has Canadian operations, lends up to $250,000 CAD in Canada. OnDeck has extended more than $7 billion in online loans across 70,000-plus customers across the United States, Canada and Australia.

As for SharpShooter Funding, Pitcher said the funder has been on the sidelines for larger deals because they don’t want to grow too fast. He’s been turned off by other funders doing deals within a couple of months of launching and then being forced to close their doors.

“Our capital has always been strong. It’s not that we can’t afford to lend larger amounts. It’s because we want to make sure we’re doing it right from the start,” Pitcher said, adding that SharpShooter Funding has only had its doors open in Canada since June 2015, though its corresponding U.S. business, First Down Funding, has been around since 2012. “It’s been a work in progress, and I love every day of it! We’re only getting started, and I am 100% excited for the future,” he said.

The Canadian grocer reached out to SharpShooter Funding in response to Google advertising. The affiliation with the Bret Hart association didn’t hurt. Pitcher explained there is a seasonality tied to the merchant’s business, evidenced by a couple of months or more each year in which revenue is spotty, that made the grocer unattractive for banks to fund. “That’s why those sized deals are difficult to put out and banks won’t put out, because of seasonality,” Pitcher said.

SharpShooter Funding was not deterred by that. “We were really able to gain in-depth trust and visibility into this merchant from the first call to the last call. There was never a problem with him mixing up stories. Just the honest truth. From his references to his landlord, everyone involved made it clear he was here to work with us and not to play games,” Pitcher said.

Pitcher was impressed by the business owner’s work ethic. “He’s a roll-up-your-sleeves entrepreneur who didn’t borrow $1 million from his father. No bank loans. Six years ago, he rolled up his sleeves and made it work. Now he’s in a situation where banks won’t lend to him. But we will,” he said.

The merchant’s bank statements also made sense to the funder given their consistency, predictability and transparency. “Whenever we ask for finances from someone and that merchant can get them to us in an organized fashion in less than an hour, it speaks wonders. It means they’re honest and ready to play ball. And that’s what we want,” Pitcher exclaimed.

The merchant plans to use the capital for an expansion into a new food product line. If he pays off the advance early the funder will lower the rate.

Take a Break From Funding This Thanksgiving

November 21, 2017This Thanksgiving…

Step back from the daily grind

Those merchants eager for your cold calls can wait

There’s no need to start worrying about next year just yet

It’s Thanksgiving

So hug an underwriter

Kiss a broker

Think about your favorite merchant

And pay no attention to the algorithms automating your job

Give thanks

Because nobody wants to hear you recap your holiday like this

Or this

Or this

Enjoy the Holiday!

You should also check out our 2016 Thanksgiving Day post and 2012 Thanksgiving Day post.

The Bad Broker And Merchant Due Diligence

November 15, 2017 There may be a rogue broker on the loose. The scam involves a fraudulent Letter of Intent (LOI) falsely claiming to be that of a major funder designed to resemble the real McCoy. Events like this place a spotlight on the risks associated with this market and is a reminder that not all small businesses are armed with the right information.

There may be a rogue broker on the loose. The scam involves a fraudulent Letter of Intent (LOI) falsely claiming to be that of a major funder designed to resemble the real McCoy. Events like this place a spotlight on the risks associated with this market and is a reminder that not all small businesses are armed with the right information.

deBanked was contacted by a victim of the fraud, Noah Grayson, managing director and founder of Encino, Calif.-based South End Capital. Grayson said the real victims are the merchants who get taken advantage of by these scams. In this case it was a New York-based small business owner who took on too many MCAs.

Grayson is quick to point out the MCAs were not at fault and each may have even thought they were the first position funder since it all unfolded so quickly. “They’re just trying to do business and provide financing to businesses, and they got burned as well. They’re going to take some degree of financial loss because of this and maybe more,” Grayson said.

False Pretenses

When Grayson reviewed an email that he received from the borrower, which included a copy of the LOI, he knew immediately that it was fraudulent and the borrower had been misled. “It was a fraudulent LOI and we had no record of the borrower or the brokers who provided it in our system,” Grayson exclaimed.

As it turns out, the borrower was tricked by the fake LOI that sought to leverage the reputation of South End Capital’s brand to coerce him into taking out $260,000 of MCAs from four separate funders. They did it under the false pretense that South End Capital would then consolidate those positions in 10 days and extend as much as $900,000 more in working capital to grow the business.

To be clear, South End Capital does offer a genuine MCA consolidation loan program. Grayson had never agreed to consolidate the business owner’s MCA positions, however, or provide an additional $900,000. That part was fabricated. This left the merchant holding the bag for more than a quarter of a million dollars in MCAs, placing his business, which has been successful since the 1960s, on the brink of bankruptcy protection in the interim because of the crippling weekly payments.

Fraud Prevention

Andi McNeal, research director at the Association of Certified Fraud Examiners, or ACFE, said she has seen this before, only on the consumer side of the industry. “Loan consolidation fraud for credit card debt is very common in the consumer space, and it’s not surprising to know that similar schemes are popping up in the small business space, too,” she said.

She went onto explain that because a small business is typically run by a small management team who typically aren’t trained in fraud prevention, they often adopt the same mindset as they do in personal finances. They don’t always have the necessary checks and balances in place, which can place them at risk of being victimized by such schemes.

“Sometimes they’re not savvy enough to detect those types of scams coming at them,” she noted. “Certainly, big businesses can fall prey to this, but it’s less common.”

Staying on Defense

The recent saga unfolded over a period of six weeks. Meanwhile Grayson has outlined some red flags for small businesses to watch out for to prevent becoming the next victim to a new fraud.

“If what you’re being told seems suspicious or doesn’t make sense, question it. Ask questions and get more information,” said Grayson.

Another rule of thumb is to stick to the document in front of them. Again, this may just be a case of a few bad apples spoiling the bunch, but sometimes brokers tell small businesses something contrary to what appears in front of them on the official document. “The LOI spells it out,” said Grayson, adding that when in doubt the borrower should defer to the document.

The merchant should also take it upon themselves to call the lender whose name is on the LOI to verify its authenticity before signing it or providing any upfront fees.

“In this case, it was a fraudulent document and it didn’t help out the borrower but calling us to confirm it initially would have. Most of the time, looking at what’s written out on paper from the verified source will help and getting a verbal or email confirmation from the actual lender, certainly will,” Grayson said.

Another defensive step merchants can take is to simply review the website of the brokers and funders and look for names, press releases and past closings, details which Grayson noted were all missing from the broker in question’s site.

“Anybody can say they make loans and provide financing. They could tomorrow put up a website for a couple bucks and say they’re a lender and start taking applications. But just because there’s a website doesn’t mean they’re legitimate,” Grayson said.

He’s suggesting merchants check out the names of the principals and employees on the site. Google is their friend to check for any history of loans closing. Look for closing announcements and any complaints tied to the entity in question. Call the Secretary of State Department and inquire about any complaints.

At the end of the day, it comes down to the merchant doing their homework. “A lot is on him. He should have done more research, absolutely. But anybody can be coerced or tricked if the right things are said,” said Grayson.

If a merchant does find themselves in a situation where they fall victim to a fraud, there are steps they should take. McNeal said that while each situation is unique, a good first step is always going to be to reach out to a trusted legal counsel.

“They can help guide you through the process of what the options are. Do you have recourse? Does the situation call for insurance to help cover the losses? They also can advise on which law enforcement or government agencies are the most helpful – should the case be referred to the local authorities or do they need to bring in the FBI,” the ACFE’s McNeal advised.

More Pervasive

Grayson’s fear is that this is not an isolated incident. He has reason to be cynical, as this was the second incident this year resembling the most recent situation that they have experienced.

The first incident was relayed to South End Capital by a handful of borrowers about one specific MCA broker. No fraudulent documents were ever recovered, but the borrowers recalled the harrowing details of the incident

“Per the multiple borrowers, the broker used our real LOIs and lied to borrowers about how to interpret them to coerce tens of thousands of dollars in upfront fees from them. For example, for an LOI we issued for our SBA loan program that listed what SBA guarantee fees would be due at closing, he would convince them that that fee was his and they needed to pay it to him upfront to proceed,” Grayson explained.

The small business owner at the center of the scandal declined to comment, and it’s unclear whether they were the one to initiate the original communication with the broker or vice versa.

Former MCA Co-founder Meir Hurwitz Kicks Off New Venture With Kim Kardashian West

November 9, 2017I love how @screenshopit lets you find the exact designer looks you see people wearing online, plus suggests similar items at all price points! #ScreenShop_Ambassador https://t.co/TXZ23agVoT pic.twitter.com/nA8JBDVbU5

— Kim Kardashian West (@KimKardashian) November 7, 2017

An early innovator of the merchant cash advance industry has re-emerged on the business scene in a very different new venture focused on mobile shopping.

Meir Hurwitz, co-founder of Pearl Capital, the MCA company acquired in 2015 by Capital Z Partners Management LLC for as much as an estimated $60 million, is now the chief visionary officer of ScreenShop. The New York startup markets an app designed to enable users to shop for a specific item by uploading a screenshot of the item to the app.

Working on a mobile app is a longer shot than MCA and it doesn’t always pay off, but Hurwitz said Thursday he’s enjoyed learning the business after two years off and visiting 62 countries since selling Pearl Capital.

“It’s new and exciting for me, but I don’t get paid right away,” he said. “It’s something I haven’t done before — it’s kind of exciting for me.”

The app is the first developed by New York-based Craze Ltd. and publicly launched on Nov. 7 with celebrity Kim Kardashian West cited as an advisor. Craze employs 12 technical workers in Israel and five in New York, Hurwitz said.

Hurwitz started in MCA in 2006 and then launched Pearl Capital with partner Abe Zeines in 2010.

Pearl launched with $1 million and generated an $8 million profit in 2012. The following year, the company doubled its profit and reached origination volume of $100 million, Bloomberg reported in 2015. Hurwitz’s ScreenShop profile indicates that he’s a “three-time successful entrepreneur” and cites “over $500 million in funding capital.”

In addition to a real estate business in Puerto Rico, Hurwitz said he’s managing partner of New York-based GS Capital, a convertible debt company lending to small businesses. Zeines lists himself as the CIO of GS Capital, according to his online profile.

At ScreenShop, Molly Hurwitz (Meir’s sister) is listed as the co-creator and co-founder. CEO Mark Fishman was previously a risk manager for Pearl Capital.

The startup’s app, which is free, scans screenshots taken from any app or website on a mobile phone, converting them to similar items that can be bought for various prices. It plans to generate revenue by collecting a commission at the point of sale, Forbes reported.

“The results have been — we’re No. 5 on the app store category of fashion,” Meir Hurwitz said. “We’re just getting started.”

ISO Alleged to Have Forged a Confession of Judgment

November 6, 2017 Underwriters, keep your eyes on the notary stamps.

Underwriters, keep your eyes on the notary stamps.

A lawsuit filed in the New York Supreme Court last week by a merchant cash advance company against an ISO and several co-defendants, alleges that an ISO was partially responsible for damages when a merchant defaulted.

And they make a compelling argument. In this case where a Confession of Judgment (COJ) was required to approve the deal, the merchant, who defaulted within 30 days of being funded, claims to have never signed one, despite the ISO having delivered a signed one to the funder.

Well then who signed it?

Upon inspection, the notary stamp on the COJ belonged to a notary in Nassau County, NY, where the contract logically would’ve been notarized. But the merchant is based in Florida and claims to have been in Florida at the time the COJ was allegedly signed.

So who would’ve been in Nassau County that day?

According to the funder, it was the ISO, since the ISO is based on Long Island and the ISO is the one that delivered the signed COJ to them.

These are just the allegations at this point, of course, since the defendants have not even yet had a chance to respond.

The complaint, however, adds another twist, that after the ISO got the deal funded, they then referred it to a debt settlement company, who assisted the merchant in defaulting.

As you might imagine, the debt settlement company is a named co-defendant.

The case is filed under Index Number: 656692/2017 in the New York Supreme Court. You can view the entire complaint here.