Loans

What is ‘Lending as a Service?’

September 3, 2020I‘ve heard of SaaS, but now there’s LaaS, Lending as a Service. I recently spoke with Timothy Li, CEO of Alchemy, a fintech infrastructure company that offers that and more. You can check it out below!

Checkout in the time of COVID

August 10, 2020 Point-of-sale (POS) lenders, also referred to as buy-now-pay-later (BNPL) firms, allow shoppers to break up their individual purchases into installments, often without interest. By adding BNPL as an option at checkout or further upstream in the purchase process, the consumer’s buying power is increased and they are often less likely to abandon their checkout cart. It is a win / win for all stakeholders.

Point-of-sale (POS) lenders, also referred to as buy-now-pay-later (BNPL) firms, allow shoppers to break up their individual purchases into installments, often without interest. By adding BNPL as an option at checkout or further upstream in the purchase process, the consumer’s buying power is increased and they are often less likely to abandon their checkout cart. It is a win / win for all stakeholders.

For these reasons, POS lending is one of the fastest growing segments in unsecured credit, with volume increasing at 40 percent year-over-year. COVID has further accelerated the demand for credit options at checkout.

According to McKinsey, annual growth is expected to jump to 150 percent thanks to an explosion in online shopping and government subsidy programs boosting retail sales. In Canada, firms such as Uplift, Paays, and PayBright are all seeing merchant demand skyrocket for their services, with the latter onboarding over 250 merchants per month.

K-Ching!

POS lenders are able to subsidize APRs by charging the merchant a fee of 4-6 percent of the purchase price. This is on average 2 percent more than the fees charged by credit cards companies. Despite the larger fee, BNPL is very attractive for retailers for a number of reasons. By providing point of sale financing retailers see:

- 30% increase in basket size

- 25% reduction in cart abandonment

- 20% increase in repeat traffic

With installment payments as an alternative, credit cards have seen a decrease in popularity among young shoppers, particularly on smaller ticket items under $500. There are a number of reasons why:

1. Clunky signup experience. Signing up for a credit card at checkout requires lots of paper, personal information, signatures and significant patience – antithetical to the one-tap checkout shoppers are accustomed to. Alternatively, BNPL approval is instant at checkout. 75% of merchants even advertise POS financing far before the register, at the beginning of the customer journey which can increase conversion by two to three times.

2. Challenge to qualify. 19 percent of consumers ages 22 to 30 lacked the credit history to be approved for credit cards in the first place. Many BNPL products do not perform credit checks, and those that do use alternative data sources to underwrite thin-file borrowers.

3. High APRs. With their parent’s household debt in their rear view mirror, many younger shoppers have an aversion to carrying revolving credit balances. Millennials on average carry two fewer cards than their parents. Psychologically, $1000 on your credit card looks scarier than four installments of $250 over time.

4. Customer confusion. Inactivity fees, late fees, over-the-limit fees, cash advance fees, are all poorly understood and masked within dense monthly statements. BNPL offers an elegant digital first experience and straightforward reporting.

The Supporting Cast

Today POS lenders are competing in a land grab for merchant partnership. But for FIs and fintechs who have yet to plant their flags, there are still ways of participating in the BNPL boom.

- Banks. Banks have largely participated indirectly in the BNPL sector, by providing portfolio financing to fintechs or by offering installment options for larger ticket items within their existing credit card programs. Wayne Pommen, CEO of PayBright, sees more bank and fintech collaboration in the next few years: “I predict more buying and partnering, Banks are too far behind to build this themselves.” Marcus Pay, the recently launched retail banking arm of Goldman Sachs is the only group to directly compete in the POS financing ring, with JetBlue as their launch partner.

- Platforms. E-commerce enablers that power millions of independent merchants are piling in to embed POS financing within their platforms. Marketplaces Ebay and Etsy have partnered with Afterpay and Klarna, while the digital infrastructure whale Shopify has an agreement with Affirm.

- Cards. Traditional credit card companies who have the most to lose from BNPL are getting ahead of the trend in several ways. Visa took a controlling stake in Klarna in 2007. More recently they launched Visa Installments, a developer tool for issuers in the Visa network to pilot branded installment products. Though Visa Installments stretches the definition of BNPL, David Fry, CEO of travel financing startup Paays does not mind the ambiguity. “I am not religious about the distinction between cards and installments. What we care about is what the customer is looking for, and what they have to pay to get access to that product”.

POS Lending has the potential to transform consumer lending as it’s evolution is inextricably tied to the growth of e-commerce. It is all about understanding the needs of the shopper and their digital journey. POS lenders are making it increasingly easy for merchants to streamline the buyer path to purchase.

The State of Securitizations in Alternative Lending

July 6, 2020Over the last few months, “securitizations” were frequently cited as a reference point for the health of a small business lender or alternative finance provider. Given the vague information and inferences that circulated, I decided to schedule a chat with Methodical Management co-founder Gunes Kulaligil to get his perspective. Our discussion on the state of securitizations in alternative lending below:

Forgiven Debts: The Hidden Tax Time Bomb That Could Kick Small Businesses While They’re Down

May 12, 2020 Small businesses that stay out of bankruptcy but have some portion or all of their debts forgiven (excluding PPP debt) are in for a rude awakening come tax time next year. In a variety of circumstances, cancelled debt can be classified as taxable income for the debtor per the IRS. This, according to a new tax study titled Did The IRS Forget Non-PPP Debt? authored by Grassi & Co, a leading accounting and business firm based in New York, that was produced in collaboration with deBanked.

Small businesses that stay out of bankruptcy but have some portion or all of their debts forgiven (excluding PPP debt) are in for a rude awakening come tax time next year. In a variety of circumstances, cancelled debt can be classified as taxable income for the debtor per the IRS. This, according to a new tax study titled Did The IRS Forget Non-PPP Debt? authored by Grassi & Co, a leading accounting and business firm based in New York, that was produced in collaboration with deBanked.

At face value, it would appear that taxpayers who have non-PPP debt canceled, forgiven or discharged during the COVID-19 crisis and do not meet any of the specific exclusions mentioned in the report, would be subject to tax on the cancelled debt as income.

This tax treatment, which pre-existed COVID-19, could be devastating in this era where the prevalence of debt forgiveness is likely to reach unprecedented levels.

In many cases this year, debt cancellation will be the direct result of government mandated shutdowns that were of no fault of the businesses themselves. Should they refrain from filing for bankruptcy and successfully negotiate a cancellation of some debt, it seems quite disastrous that the same government that shut them down might deliver a second blow by taxing the acts that enabled the businesses to survive.

In many cases this year, debt cancellation will be the direct result of government mandated shutdowns that were of no fault of the businesses themselves. Should they refrain from filing for bankruptcy and successfully negotiate a cancellation of some debt, it seems quite disastrous that the same government that shut them down might deliver a second blow by taxing the acts that enabled the businesses to survive.

One must also consider that a lender may just cancel some or all of a portion of a debt without any direct action of the debtor, with the end result being the same, a potential tax bill to the business on the cancelled portion.

It’s important to understand the various exclusions to the IRS guidelines that govern cancelled debt. The full report can be ACCESSED HERE.

The Story Behind The #BrokersAreBetter Super Bowl Commercial

February 7, 2020 Watching the Super Bowl, you may have seen a number of oddities: the resurrection of a peanut as an infant, the tattooed inside of a popular rapper’s head, Google’s plea to be the hub for all your elderly relatives’ memories, and, on top of it all, a cheeky spar between mortgage lenders.

Watching the Super Bowl, you may have seen a number of oddities: the resurrection of a peanut as an infant, the tattooed inside of a popular rapper’s head, Google’s plea to be the hub for all your elderly relatives’ memories, and, on top of it all, a cheeky spar between mortgage lenders.

Quicken Loans, the Detroit-based mortgage provider, had an ad that featured Hawaiian actor Jason Momoa reveal his ‘true’ self, all while explaining the values of Quicken’s Rocket Mortgage product. Par for the course with Super Bowl ads, until United Wholesale Mortgage’s advert aired. Throwing shade at it its competitor with the line: “Playing with rockets is great when you’re a kid, but when it’s time to get a mortgage, you quickly realize a rocket is complicated and expensive,” United promoted its FindAMortgageBroker.com website, which points potential customers towards a host of brokers local to themselves, before closing its ad with the #brokersarebetter hashtag.

Speaking to The Detroit News about the joke, United CEO Mat Ishbia said: “I don’t think we attacked (Rocket Mortgage); we had fun with it … I think it’s going to grow their business just like it’s going to grow ours. I think (Quicken founder) Dan Gilbert and (CEO) Jay Farmer are going to laugh when they see it. They won’t like it enough to chip in with the cost. The reality is we’re friendly competitors.”

Being a wholesale lender, United gains customers exclusively from its brokers, where as Quicken engages with both brokers and its own marketing efforts. In a call with deBanked, United’s Chief Marketing Officer, Sarah DeCiantis, explained that this was one of the main motivators behind the ad. Noting that for local, independent brokers it can be a struggle to compete with behemoth retail lenders, DeCiantis said that the ad was an answer to the question of ‘How do we allow them to get out there?’ “Retail are amazing at marketing and customer retention, so we try to do what we can to put [independent brokers] on the same playing field because they don’t have the same budget.”

And with only 30 seconds to express this, the challenge was on — not to mention how such ads are estimated to cost $5.6 million. “So much thought goes into every frame, every second,” remarked DeCiantis, who said she was proud of the final product. “We’ve gotten over 75,000 searches on the website just in the first few days after the ad.”

The high profile decision to purchase Super Bowl air time comes during what looks like will be a big year for United, with it planning to add an additional 3,000 employees to its already 5,000-strong staff in its Pontiac headquarters. Despite this, according to Ishbia the focus is still on the local: “If a consumer goes through an independent mortgage broker it will be faster, easier and more affordable than going through a retail lender or mega bank.” From his point of view, it just makes more sense to go independent, it isn’t rocket science.

Lender Ranking Website Accused By FTC Of Misleading Rankings

February 6, 2020 LendEDU, a Hoboken-based company that lists and ranks loan providers, came under fire this week after the FTC filed a complaint detailing how LendEDU charged businesses for higher positions in its rankings of lenders and promoted fake testimonials. Providing ratings for student loan refinancing, personal loans, and mortgage lenders, it is the first of these loan types that is in the spotlight.

LendEDU, a Hoboken-based company that lists and ranks loan providers, came under fire this week after the FTC filed a complaint detailing how LendEDU charged businesses for higher positions in its rankings of lenders and promoted fake testimonials. Providing ratings for student loan refinancing, personal loans, and mortgage lenders, it is the first of these loan types that is in the spotlight.

While LendEDU initially denied that it received any compensation for its lists, saying, “ratings are comparatively objective and not influenced by compensation in anyway” and that “research, news, ratings, and assessments are scrutinized using strict editorial integrity,” this assertion was disproved by the FTC’s investigation.

Emails were discovered which featured CEO Nathaniel Matherson and Vice President of Products Alexander Coleman discussing with a business the pricing per click to hold the #1 spot on the best student loan refinancing company list, as well as what sort of traffic could be expected at this ranking. Accompanying this was a contract between LendEDU and a student loan refinancing company, revealing that in return for compensation the company would drop “[n]o lower than position three” in the rankings. It was also found that if businesses who were already in the rankings refused to pay for the clicks they received, they would drop down in the list.

The testimonials that featured prominently on LendEDU’s homepage, which noted alleged consumers’ names, colleges, and years of graduation, were found to be wholly false, with the people portrayed in them being nonexistent.

And the reviews of LendEDU that were found on Trustpilot and subsequently posted to the company’s own website, were also shown to be fake. Of the 126 reviews, 123 were found to be 5-stars; and only 11 were proven to be from customers (this was confirmed as the emails matched those used by customers), the other 115 were deigned to be written by friends, family members, and associates of LendEDU members, as well as by LendEDU employee’s themselves under false names.

All this is coming after LendEDU landed in hot water following a controversy in 2018 that saw Matherson admit to working with others to create a fictitious expert on student loans, named Drew Cloud, who would give interviews and comments to publications, creating a pro-student loan refinancing discourse. According to Matherson, Cloud “was created as a way to connect with our readers (ex. people struggling to repay student debt) and give us the technical ability to post content to the WordPress website.” Cloud was even given a pixelated face and backstory that extended into high school, imbuing him with a passion for journalism even in his teenage years. Neither Matherson’s comments on Cloud nor his fictional biography do anything to explain how or why his creators decided to give him a name that is quite clearly fake.

LendEDU promptly agreed to settle the charges and pay $350,000 while not admitting or denying the allegations. The public has 30 days to comment on the settlement prior to it becoming final.

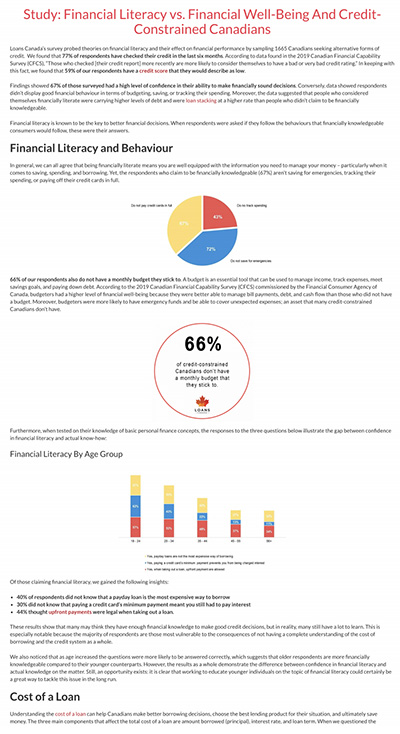

Study Claims Canadian Market Needs to Improve Financial Literacy

January 24, 2020 This week Loans Canada, a lead generation company, released a study documenting the disparities between perceived financial literacy and actual financial well-being. Surveying 1,665 Canadians, the report asserts that those individuals who claim to have a firm grasp of their financial situation may in fact be out of touch.

This week Loans Canada, a lead generation company, released a study documenting the disparities between perceived financial literacy and actual financial well-being. Surveying 1,665 Canadians, the report asserts that those individuals who claim to have a firm grasp of their financial situation may in fact be out of touch.

This being highlighted by major misunderstandings about how to budget for the future as well as a lack of education regarding loan repayments. 72% of the respondents said that they did not save for emergencies, 43% did not track their spending, and 66% do not stick to a monthly budget. Such budgetary omissions outline the potential for a large portion of the Canadian market to be in trouble should unforeseen expenses arise, and the fact that two thirds of the market aren’t even drawing up budgets is a cause for concern.

Such factors are made worse by the community’s seeming misinterpretations of loan terms. With 40% of the survey stating that they didn’t know payday loans were one of the most expensive ways to borrow money, 30% not understanding that paying the minimum amount of a credit card charge still meant you had to pay interest, and just over half of those surveyed were not able to identify the factors which affect the cost of loans, there appears to be a problem surrounding financial literacy and education of individuals regarding loans.

As well as these issues, there is the case of stacking loans, with the study indicating that the practice is not fully understood by Canadians and that the two top reasons for taking on multiple loans are for emergency costs (25%) and making ends meet (43%). Interestingly, the respondents who claimed to have the most confidence in their capacity to make financially sound decisions are more likely to be individuals who stack loans, leading them, inevitably, to have similar or more debt than those surveyed who said they were not confident in their financial decision-making ability.

Altogether, the study paints the picture of Canada as a market in need of further education. While financial literacy isn’t in crisis, the report points towards vulnerable sectors, such as such as those individuals with poor knowledge of loans and interest rates, as well as budgeting, are groups that need to develop a better understanding.

Apple Card Under Investigation by State Financial Regulator

November 14, 2019 Apple and Goldman Sachs came under fire this week after numerous users of the Apple Card, a joint venture by the two companies, took to social media claiming that the algorithm used to determine credit limits discriminated against women.

Apple and Goldman Sachs came under fire this week after numerous users of the Apple Card, a joint venture by the two companies, took to social media claiming that the algorithm used to determine credit limits discriminated against women.

It began when Danish tech entrepreneur and racecar driver David Heinemeier Hansson wrote up an expletive-laden teardown of the card and the companies behind it after he discovered that he had access to twenty times more credit than his wife, despite the couple having filed joint tax returns. Following the twitter thread’s viral surge, other men came forward with similar stories, some noting that their wives had better credit scores than themselves.

Upon dealing with Apple’s customer service, who gave Hansson’s wife a “VIP bump” to her credit limit, raising it to match her husband’s, the entrepreneur lamented the giant’s response to his questions about the decision-making process behind Apple Card.

“Apple has handed the customer experience and their reputation as an inclusive organization over to a biased, sexist algorithm it does not understand, cannot reason with, and is unable to control,” Hansson wrote after being told by two Apple representatives that they were unable to explain the reasoning behind the inequity other than say that “it was just the algorithm.” Hansson went on later to criticize the implementations of algorithms that incorporate “biased historical training data, faulty but uncorrectable inputs, programming errors, or malicious intent” as a whole, pointing to Amazon’s recent use of an algorithmic hiring tool that taught itself to favor men.

And in a surprise twist, Apple Co-founder Steve Wozniak weighed in, saying, “The same thing happened to us. I got 10x the credit limit. We have no separate bank or credit card accounts or any separate assets. Hard to get to a human for a correction though. It’s big tech in 2019.”

Over the weekend word came from the New York Department of Financial Services that it would be investigating the practices behind the Apple Card to determine whether or not such an algorithm discriminates on the basis of sex, which is prohibited by state law in New York. This is the second such investigation recently, with the NYDFS announcing last week an investigation into the healthcare company UnitedHealth Group and its use of an algorithm that allegedly led to white patients receiving better care than black patients.

“Financial service companies are responsible for ensuring the algorithms they use do not even unintentionally discriminate against protected groups,” wrote NYDFS Superintendent Linda Lacewell in a blog post that explained the decision to investigate and called for those who believed they were affected unfairly by Apple Card to reach out. “[T]his is not just about looking into one algorithm – DFS wants to work with the tech community to make sure consumers nationwide can have confidence that the algorithms that increasingly impact their ability to access financial services do not discriminate and instead treat all individuals equally and fairly no matter their sex, color of skin, or sexual orientation.”

In their response, the Goldman Sachs Bank Support twitter account posted a note listing various factors that come into consideration when determining a person’s credit limit, asserting that they “have not and will not make decisions based on factors like gender.”

And it would appear that this is correct, at least in the literal sense, as the application process for the Apple Card does not include any questions relating to gender.

Bruce Updin of Zest AI, a company that provides machine learning software for underwriters, said of the controversy that “there’s bias in all lending models, even human lenders … race, gender, and age are built into the system. It can show up just due to the nature of the credit scoring system as FICO scores at the end of the scale can correlate to race.”

Explaining that there are connections between identity and information many humans might never perceive without machine-learning algorithms, like Nevada license plates being an indicator of the likelihood of someone’s race, Updin asserts that such links need to be weighed, balanced, and supervised by those in the banks. For Updin, transparency and explainability are the real problems here rather than the algorithms themselves.

Software exists that can pinpoint which variables are producing results that, for example, skew to prefer women over men, and can remove such factors and run the tests again, probing for differences. The trouble arises when banks find themselves unable to communicate such details for whatever reason, be it an inherent misunderstanding of their own programs or an unwillingness to explain why some of their models prefer certain groups over others.

It’s really a case of “giving up a little bit of accuracy for a lot of fairness” when choosing to remove variables that are proxies for gender, race, age, or a variety of other identifying features, according to Updin. “It’s just a lot of math, it’s not magic. The more you automate the tools, the easier it is.

“I’m convinced in 5-10 years every bank will be using machine-learning for underwriting … we don’t need to throw out the baby with the bathwater.”

{kind=link}