Loans

LendUp Stops Making New Loans

July 10, 2021 LendUp, a fintech lender that hoped to disrupt the payday loan industry, is no longer making new loans. A note posted on its website said “We are currently not offering loans to new customers.”

LendUp, a fintech lender that hoped to disrupt the payday loan industry, is no longer making new loans. A note posted on its website said “We are currently not offering loans to new customers.”

When deBanked sat down with the now former CEO Sasha Orloff in 2017, he said that their product was simply cheaper and more flexible.

“The easiest person to convince that we’re a better product is an existing payday user because it’s slightly cheaper at the beginning, it gets much cheaper over time,” he said then. “It has a lot more flexibility.”

But for all the bells and whistles, their still relatively high rates generated a target on their back with regulators.

In 2016, for example, the CFPB said “[LendUp] did not give consumers the opportunity to build credit and provide access to cheaper loans, as it claimed to consumers it would.”

Balancing the messaging with the reality seemd a difficult task.

Orloff stepped down in January 2019, but in less than two years the CFPB took a second crack at LendUp for allegedly violating the Military Lending Act.

In January of this year, LendUp settled the charges, agreeing to pay $300,000 in redress to consumers and to pay a $950,000 civil money penalty.

As recently as April, LendUp’s website was still offering loans with a promoted APR of 400%.

Loan Fraudsters Resorting to AI Generated Faces

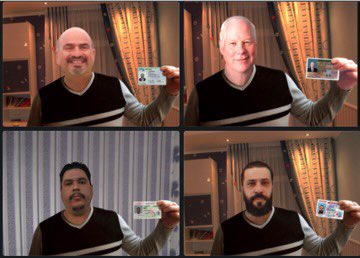

April 27, 2021 According to a sneak peek posted by Lendio CEO Brock Blake, fraudsters are stopping at nothing to game the government’s emergency loan system.

According to a sneak peek posted by Lendio CEO Brock Blake, fraudsters are stopping at nothing to game the government’s emergency loan system.

“Wanna glimpse into what lenders are experiencing with attempted fraudulent applications?” Blake wrote in a tweet. “Here are four ‘applicants’ seeking a loan.”

Four pictures showing computer-generated “business owners” all have the same sweater, but different heads. People are using AI tech to create randomized, just barely discernible pics of borrowers holding IDs beside them to beat new compliance measures.

It’s like a techno arms race between an automated scanning system that looks for fakes versus an automated fake ID and person generator that tries to make passable fakes.

After a year of PPP and EIDL success stories and fraud concerns, funders are still beating back scam artists. During a recent U.S. Senate hearing, SBA Inspector General Mike Ware said his office had secured $2.1 billion in fraudulently claimed PPP and EIDL loans.

In related news, the SBA announced the $28.6 billion Restaurant Revitalization Fund applications would open on Monday, May 3. Fraudsters start your fake restaurant owner generators.

Wanna glimpse into what lenders are experiencing with attempted fraudulent applications?

Here are 4 different “applicants” seeking a #ppploan. pic.twitter.com/kdbLmNGlvt

— Brock Blake (@BrockBlake) April 26, 2021

Can’t Wait For An Inheritance? Someone Will Fund You

April 19, 2021 Another twist on purchasing receivables is making its way into the mainstream in the form of an Inheritance Cash Advance.

Another twist on purchasing receivables is making its way into the mainstream in the form of an Inheritance Cash Advance.

For some, the aftermath of losing a loved one can turn into a long drawn out legal process and delay the transfer of rightfully owed inheritance in the process. Probate funders fix the problem, paying cash upfront, purchasing the future receivable of a will. The small industry is remarkably similar to the merchant cash advance world and uses the same terminology. “Inheritance Cash Advances are not loans,” one website says, “with an Inheritance Cash Advance, we send immediate cash to heirs in exchange for an assignment of a fixed dollar amount of their eventual inheritance.”

David Horton, a University of California-Davis law professor who delved into 1,119 probate agreements in the San Francisco area as part of a UPenn Study, said of the product “in almost all cases, with rare exceptions, the lender not only gets their advance back but also gets a huge markup.”

Interestingly, this type of funding is most popular in California, where some of the most complicated estate laws in the country make inheriting a hassle. But a less than flattering industry profile in Consumer Reports says that such companies “earn millions offering cash advances to heirs, with effective interest rates as high as 490 percent.”

And yet, industry advocates say that they are providing a needed service. “We are proud of the service we provide and the highest ethical way we conduct our business at IFC,” said Doug Lloyd, CEO of Inheritance Funding Company to Consumer Reports. “It is easy to understand why banks and other financial institutions are not in this business.”

His company has already advanced more than $200 million to customers. The following video is featured on their website:

Upstart Says Covid Had No Material Impact on Loan Performance, Believes All Loan Underwriting Will be Powered by AI in the Future

March 17, 2021 Yet another online consumer lender has reported that the Covid-era was good for business. Upstart, which went public in December, recorded $1M in profit in Q4 and $6M in profit for the year. Prosper Marketplace, an Upstart competitor, reported an $18.5M profit for 2020 just days earlier.

Yet another online consumer lender has reported that the Covid-era was good for business. Upstart, which went public in December, recorded $1M in profit in Q4 and $6M in profit for the year. Prosper Marketplace, an Upstart competitor, reported an $18.5M profit for 2020 just days earlier.

“Despite the COVID-19 pandemic, we delivered strong growth and profits in Q4 and for the full year 2020,” Upstart CEO Dave Girouard said in the company earnings announcement. “This combination is rare among FinTechs and demonstrates the growing advantages of AI-based lending.”

Upstart actually grew its revenue in 2020 by 42% over the previous year while keeping loan performance steady.

“We’re happy to report that the COVID-19 pandemic had no material impact on the returns that our bank partners and loan investors experienced this past year.”

The company is going full speed ahead on AI-based lending. “We believe virtually all lending will be powered by AI in the future, and we’re in the earliest stages of helping our bank partners successfully navigate that transformation.”

Keenly aware that AI is an overly used buzzword, the company reminded investors about what its AI can actually do.

Our AI models, like all AI systems, are fueled by incredible amounts of data and sophisticated software to interpret that data, while most lenders consider only a handful of variables as part of a lending decision, Upstart’s model considers more than 1,000 variables about each applicant. You can think of these as the columns in a spreadsheet. And as of December 31, 2020, our model was trained on more than 10.5 million unique repayment events.

These are like the rows in the spreadsheet. And we continually upgrade the machine learning software that interprets this data, enabling us to price the next loan on our platform just a bit more accurately. Upstart goes far beyond a singular AI model predicting default risk. We have discrete AI model that improve the entire lending process, including identity fraud, income misrepresentation, loan stacking, prepayment risk, fee optimization, and more.

But of course, our model that targets default risk is the centerpiece of our system. It predicts not just the likelihood that a loan will default, but when that default can be expected to happen.

Upstart also intends to bring that technology to auto lending. The company simultaneously announced that it had acquired Prodigy Software, Inc, a tech that’s been used to assist with selling more than $6B worth of cars.

“…2021, from our perspective with auto, is really a building year,” said Girouard, “And the acquisition of Prodigy, we certainly view as an accelerator toward the point of sale, the majority of the market that happens at the dealership.”

Prosper Marketplace Posts $18.5M Profit for 2020

March 15, 2021 Prosper Marketplace reported a $18.5M profit for 2020, up from a net loss of $13.7M in 2019, marking yet another online lender that successfully weathered Covid.

Prosper Marketplace reported a $18.5M profit for 2020, up from a net loss of $13.7M in 2019, marking yet another online lender that successfully weathered Covid.

In 2020, Prosper originated $1.5B in loans, $1.4B of which were originated through their Whole Loan Channel.

Like Lending Club, the company has long retreated from its peer-to-peer lending roots, but still operates a platform where individual retail investors can buy notes, whereas Lending Club terminated theirs completely.

Prosper generated $100 million in revenue in 2020 and had 353 full-time employees at year-end.

Prosper is not publicly traded but is required to file regular financial statements with the SEC because it sells notes to retail investors.

LendingClub Talks Earnings Post Radius-Bank Acquisition

March 11, 2021 “It’s really hard to imagine a better time to be launching a digital bank,” said LendingClub CEO Scott Sanborn on the company’s Q4 earnings call. “First up, we’ll be building on Radius’ multi-award winning online and mobile deposit offering to make it very easy for our customers to manage their lending, spending and savings in a holistic fashion.”

“It’s really hard to imagine a better time to be launching a digital bank,” said LendingClub CEO Scott Sanborn on the company’s Q4 earnings call. “First up, we’ll be building on Radius’ multi-award winning online and mobile deposit offering to make it very easy for our customers to manage their lending, spending and savings in a holistic fashion.”

The company reported a Q4 net loss of $26.7M on $75.9M in revenue and originated $912M in loans. Their status of being a bank, however, is only just beginning. CFO Tom Casey explained the following:

In addition to lowering our funding cost of deposits, our new marketplace bank will capture significant financial benefits from being a bank and having a marketplace. [….]For every $100 million of loans we originate, we generate about $4 million through an origination and servicing fee when we sell the loans in the marketplace. The vast majority of this fee-based revenue is realized immediately and without requiring a significant amount of capital. However, it is highly dependent on origination volume.

[…]

We can now bolster this revenue stream with bank revenue generated by loans held for investment on our balance sheet. As you can see on the left side of the page, every $100 million of loans we hold on the balance sheet should generate additional marginal profitability of approximately $12 million. And when you compare that to the $4 million in the marketplace, that’s 3 times more. And this recurring revenue is not dependent on originations in any given quarter.

LendingClub experienced unique success during the pandemic, stating that loan performance exceeded their expectations.

“Coming out of the pandemic,” Sanborn said, “the strength of our underwriting has now also been cycle-tested. Losses on loans issued pre-COVID are in line with our pre-pandemic expectations, and loans issued since the pandemic are some of our best-performing loans in recent years.”

Was That Loan Forgiven? The Tax Man Cometh

March 10, 2021 With tax season upon us, the events of 2020 will soon be reviewed and evaluated by everyone’s best friend, the IRS. Lenders that offered debt forgiveness might have done a favor to distressed borrowers in 2020, but a consequence of that courtesy is that the borrowers’ forgiven debt might be taxable.

With tax season upon us, the events of 2020 will soon be reviewed and evaluated by everyone’s best friend, the IRS. Lenders that offered debt forgiveness might have done a favor to distressed borrowers in 2020, but a consequence of that courtesy is that the borrowers’ forgiven debt might be taxable.

This is as good a time as ever to review a report prepared by Grassi Advisors & Accountants whether you are a lender that forgave debt or a borrower that had debt forgiven.

“This issue was noticed early last year,” said deBanked President Sean Murray, “but at the time everyone was so focused on PPP forgiveness, the EIDL program, and government stimulus, that I think the potential consequences of lenders forgiving non-PPP debt for their borrowers were lost in the shuffle. Imagine you’re a borrower that had $100,000 of non-PPP debt forgiven last year and you’re only now about to learn that the IRS may classify that as income. Or worse yet, you don’t even realize it and are told that later on during an audit.”

In May 2020, deBanked labelled this as a hidden tax time bomb that was set to detonate in 2021. And now here we are.

Methodical Ponders if The Roaring Twenties Are Around The Corner

March 9, 2021 When we last spoke with Gunes Kulaligil, a co-founder of Methodical Management, a valuation and advisory firm, several securitizations in the non-bank finance space had just hit early amortization triggers. That was in late June 2020.

When we last spoke with Gunes Kulaligil, a co-founder of Methodical Management, a valuation and advisory firm, several securitizations in the non-bank finance space had just hit early amortization triggers. That was in late June 2020.

Now that time has passed and the world stabilized, a publication put out by the firm on March 3rd ponders if we are on the verge of repeating the Roaring Twenties of a century ago.

“We have repeated a pandemic, and a hundred years ago the Roaring Twenties was a decade of economic growth and widespread prosperity, driven by recovery from wartime devastation and deferred spending… and we now see a tsunami of deferred spending waiting to be deployed,” the company wrote.

Although spreads for the majority of sectors are currently at the tight end of multi-year trading ranges, there are notable exceptions such as retail/hotel heavy CMBS, aircraft, private student loan subs, rental car and some franchise bonds. One thing to note is that even though spreads in most sectors have held up in the face of deteriorating performance due to the COVID freeze, most structural protections have worked as designed to insulate investors from losses.

“A positive perhaps unexpected consequence of COVID has been the higher savings rates seen than before the pandemic,” the report says. “To be clear, it is a K-shaped recovery and there continues to be distress especially for lower income borrowers, but nowhere near the projected levels pontificated after April 2020’s unemployment number of 14.8% was released. There may continue to be unintended consequences down the road but for now FICOs are up, savings are up, delinquencies are down and this trend is likely to continue as new stimulus packages that are in the works get rolled out.”