Legal Briefs

Two Commercial Finance Consultants Charged By SEC in Ponzi Scheme

August 22, 2018Two commercial finance consultants were charged by the SEC earlier this week for their alleged role in soliciting investors to place their savings into mortgage-backed securities issued by Woodbridge Group of Companies, LLC, a company revealed to be a $1.2 billion ponzi scheme.

Barry Kornfeld and Ferne Kornfeld of Parkland, Florida, allegedly earned $3.7 million in commissions by selling unregistered securities to more than 500 investors. Barry Kornfeld was already barred by the SEC for previous securities violations, the complaint states. The Kornfelds taught a “conservative retirement, income planning and social security” class at Florida Atlantic University, where the investments were pitched, the SEC says.

FEK Enterprises, Inc. DBA First Financial Tax Group, the company the Kornfeld’s operated, is also named in the complaint.

Their LinkedIn profiles, however, currently list them as the owners of Value Capital Funding, a small business financing broker in Boca Raton, FL.

Merchant Cash Advance Company Wins in Bankruptcy Court After Judge Rules It’s an Ordinary Part of Business

August 21, 2018 Last week, a bankruptcy judge in the Northern District of Illinois ruled that a merchant had used so many merchant cash advances that it had become a normal part of their business.

Last week, a bankruptcy judge in the Northern District of Illinois ruled that a merchant had used so many merchant cash advances that it had become a normal part of their business.

At issue was Network Salon Services, a business founded in 2004 that was brought back from the brink of insolvency in January 2013 by a merchant cash advance. That advance, coupled with dozens of advances from more than 14 MCA companies over the following 3 and a half years would keep Network Salon on life support until it finally failed for good.

At the end, Network Salon had just $200 to its name and nearly $4 million in outstanding future receivables due to MCA companies.

After the Chapter 7 proceedings commenced, the bankruptcy trustee came knocking on the doors of several MCA companies to give back the funds it believed had been fraudulently transferred and obtained through criminally usurious means.

One of those companies, NY-based LG Funding, pushed back hard, and on August 15th the judge ruled in LG’s favor. In a carefully considered decision, The Honorable Jacqueline Cox said that an exception applied to LG Funding. Unlike a normal creditor where certain property obtained leading up to a bankruptcy becomes returnable to the trustee, Network Salon relied on MCAs in its normal course of business for years and thus the transfers of funds to LG Funding was the ordinary course of business not subject to return.

So ordinary was it in fact that Network Salon used MCAs to make payments on other MCAs, going so far that at one point one of its bank accounts showed no deposit activity for a month except for deposits from MCA companies and online lenders.

Ultimately it didn’t matter if LG Funding was actually debiting the deposits made by rival companies rather than the actual proceeds of sales, Judge Cox opined, because this deviation from the contract was not fraudulent and both parties benefited from it.

The usury arguments, as usual, failed, because New York courts (The state governing LG Funding’s contracts) have already determined that MCA transactions are not loans and therefore can’t be usurious.

“The Trustee has failed to meet her burden to establish by a preponderance of the evidence that the transfers were preferential or constructively fraudulent and therefore subject to avoidance,” The judge ordered. “LG Funding has succeeded in establishing that the transfers were made in the ordinary course of business, defeating the Trustee’s 547(b) preference claim. The constructive fraudulent conveyance claim fails because Network Salon received reasonably equivalent value in the transactions in issue. Judgment will be entered in favor of Defendant LG Funding on all counts.”

This post is an oversimplified explanation. Download the 24-page decision HERE for the full facts and details.

World Global Financing Bankruptcy Converted to Chapter 7

August 9, 2018Florida-based World Global Financing (WGF), who filed for Chapter 11 in May, has been ordered into liquidation following their failure to abide by the settlement agreement with Eaglewood SPV I LP.

Eaglewood’s claim on WGF comprised 98% of all creditor claims.

WGF agreed to settle with Eaglewood for $2.95 million, but WGF failed to make payments in the specified timeframe. That inevitably allowed Eaglewood to convert the bankruptcy to Chapter 7 and to simultaneously file a $6.5 million Confession of Judgment against WGF.

Details Emerge in Florida Lawsuit Against Corporate Debt Advisors

August 9, 2018 A debt settlement company being sued by Itria Ventures in Miami-Dade County, FL was asked to prove its claim that it has managed over $1.5 billion in total debt, court records show. That company, Corporate Debt Advisors (CDA), advertises that it provides debt relief for small business owners.

A debt settlement company being sued by Itria Ventures in Miami-Dade County, FL was asked to prove its claim that it has managed over $1.5 billion in total debt, court records show. That company, Corporate Debt Advisors (CDA), advertises that it provides debt relief for small business owners.

CDA responded to Itria’s request on June 29th with information relating to just two employees, Tony Shea and John Philbin, who combined through their previous experience have purportedly managed $1,584,000,000 of debt.

Not mentioned in their response is that each individual is prohibited from engaging in debt settlement services with Florida consumers where Corporate Debt Advisors is located.

According to the Office of the Attorney General, both Shea and Philbin previously and independently settled with the State after being investigated for running questionable debt settlement businesses. (See here and here)

In the lawsuit filed against CDA by Itria, it’s alleged that CDA is advising merchants to commit fraud by moving money owed to Itria to a new secret hidden bank account at a local bank in Florida where it will be out of reach from Itria.

This is not the first time Corporate Debt Advisors has been sued. In early July, a competitor to Itria, High Speed Capital, petitioned a New York court to turn over funds it believes CDA has in its possession for unlawful budget planning services rendered to a Florida-based business.

Notorious Tampa Bay Loan Broker Likely Headed Back to Jail

July 27, 2018 Tampa Bay loan broker Victor Clavizzao pleaded guilty this week to one count of wire fraud, which could land him in prison for up to 20 years. This would not be his first time behind bars. In 2009, a federal judge sentenced him to five years for conspiring to fraudulently obtain nearly $6 million in mortgage loans.

Tampa Bay loan broker Victor Clavizzao pleaded guilty this week to one count of wire fraud, which could land him in prison for up to 20 years. This would not be his first time behind bars. In 2009, a federal judge sentenced him to five years for conspiring to fraudulently obtain nearly $6 million in mortgage loans.

This time, Clavizzao, 55, cheated a church congregation out of $16,350 that they had set aside to build a new church. According to a Tampa Bay Times story, shortly after leaving prison in 2014, Clavizzao was still on probation when he created Key Business Loans. Around the same time, he met husband and wife, Sam and Minnie Wright. Minnie Wright is the pastor of the Tampa Bay-area New Testament Outreach Holiness Church #2, and she asked Clavizzao if his company would be able to make a loan to their church.

According to the Tampa Bay Times story, Clavizzao said “Absolutely.”

Clavizzao, who used the named Victor Thomas, ingratiated himself with the Wrights and other church congregants and told them that not only could he help them obtain a $650,000 loan, he could also handle the purchase of the plot of land along with other details. The church gave Clavizzao a series of initial payments – for an architect and for an environment inspection of the land – and when the Wrights started getting suspicious, Clavizzao disappeared.

Last year, suspected of defrauding the Wrights and others, Clavizzao told Tampa Bay Times in a phone interview that his business, Key Business Loans, was completely legitimate.

“Knock yourself out, I’m not doing anything wrong,” he said, acknowledging that he discloses his criminal history to prospective borrowers. “Any person who has a problem about my past can choose to do business with me or not do business.”

In July of 2014, Clavizzao presented the Wrights with a “Proposal Letter for Guaranteed Business Purchase Loan” from Key Capital Commercial Funding, a New York City-based company he said he had ties with. The proposal outlined the terms of a 15-year, $650,000 loan at 5.1 percent interest. The Wrights signed it. However, what the Wrights did not know at the time was that there was no Key Capital Commercial Funding in New York City, or anywhere else.

In part because of persistent reporting on Clavizzao from Susan Taylor Martin at Tampa Bay Times, the Wrights were able to learn more about Clavizzao’s criminal past and the FBI got involved.

After Clavizzao’s recent guilty plea, he is currently out on bond pending his sentencing. A date has not been set.

JTT Funding STILL Impersonating Rival Funding Company, Court Docs Allege

July 26, 2018 A Court-ordered injunction hasn’t prevented New York ISO JTT Funding from continuing to pretend to be Accel Capital, a new motion filed in New York County this week argues. In May, JTT Funding failed to appear in court to defend itself against claims it was impersonating Accel Capital when contracting with merchants. After reviewing the evidence, the judge ordered JTT to stop using the name, logo and likeness of Accel.

A Court-ordered injunction hasn’t prevented New York ISO JTT Funding from continuing to pretend to be Accel Capital, a new motion filed in New York County this week argues. In May, JTT Funding failed to appear in court to defend itself against claims it was impersonating Accel Capital when contracting with merchants. After reviewing the evidence, the judge ordered JTT to stop using the name, logo and likeness of Accel.

Allegedly, JTT is undeterred and is continuing to represent itself as Accel Capital. When merchants deceived by the imposter accidentally reach out to the real company, they learn they’ve been duped. Accel attached contracts as evidence between merchants and the imposter that are dated after the injunction was issued, the docket shows. The phone # in the phony contracts belongs to JTT Funding, according to a Google search.

One of those contracts promises a merchant that they have been approved for $818,000 and in order to obtain the funding they need to first send a payment of $36,932.70 to the imposter.

JTT Funding is the same company that was alleged to have forged a Confession of Judgment last year. Like in the Accel case, JTT never appeared to defend itself.

The Accel Capital suit can be found in the New York Supreme Court under Index Number: 153447/2018

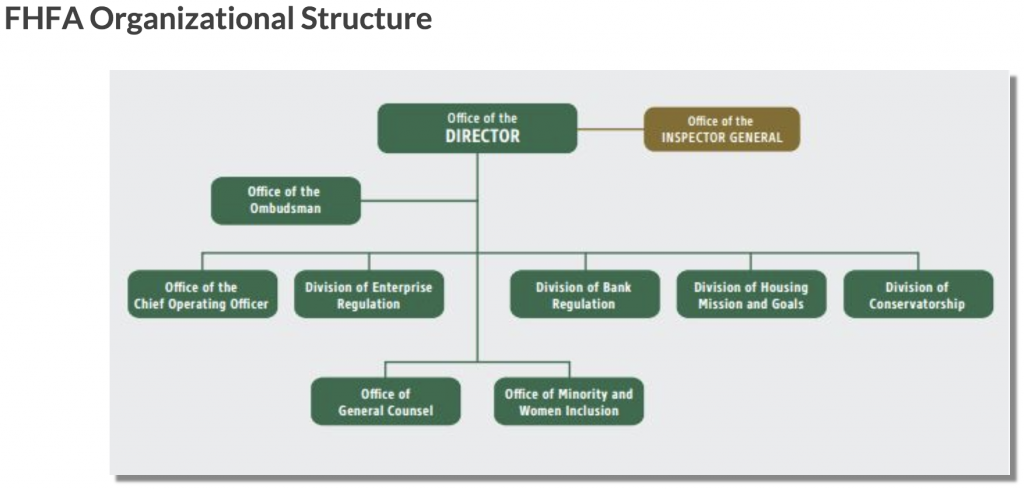

Like Bureau of Consumer Financial Protection, Court Declares FHFA Unconstitutional

July 19, 2018The Bureau of Consumer Financial Protection (Bureau), created largely by Democratic politicians in the wake of the 2008-10 financial crisis, has not been the most popular government agency under the current administration. That said, a June court decision declared that the agency itself is, in fact, not very democratic.

The controversial decision came from District Judge Loretta Preska of the New York’s Southern District who declared the Bureau to be unconstitutional based on its single directorship structure. (The current structure features a director who has full control over decisions with no requirement of a vote or a consensus from other colleagues or parties).

This week, the Court of Appeals for the Fifth Circuit made a ruling against the Federal Housing Finance Agency (FHFA) for the same reason – because it deemed the agency to be unconstitutional based on its single directorship structure.

The FHFA was established by the 2008 Housing and Economic Recovery Act to ensure that Fannie Mae, Freddie Mac and the Federal Home Loan Bank System are operating in a safe and sound manner so they can serve as a reliable source of liquidity and funding for housing finance and community investment.

The defense for this decision against the FHFA cites heavily from a 2016 ruling, written by Supreme Court Justice nominee Brett Kavanaugh, that asserts that the Bureau is unconstitutional in large part because the director cannot even be removed the president. Part of this week’s FHFA decision is as follows:

“Congress encased the FHFA in so many layers of insulation—by limiting the President’s power to remove and replace the FHFA’s leadership, exempting the Agency’s funding from the normal appropriations process, and establishing no formal mechanism for the Executive Branch to control the Agency’s activities—that the end ‘result is a[n] [Agency] that is not accountable to the President.’ The President has been ‘stripped of the power [the Supreme Court’s] precedents have preserved, and his ability to execute the laws—by holding his subordinates accountable for their conduct—[has been] impaired.'”

The 2016 decision decreeing that the Bureau is unconstitutional is similar:

“Other than the President, the Director of the Bureau is the single most powerful official in the entire United States Government, at least when measured in terms of unilateral power. That is not an overstatement. What about the Speaker of the House, you might ask? The Speaker can pass legislation only if 218 Members agree. The Senate Majority Leader? The Leader needs 60 Senators to invoke cloture, and needs a majority of Senators (usually 51 Senators or 50 plus the Vice President) to approve a law or nomination. The Chief Justice? The Chief Justice must obtain four other Justices’ votes for his or her position to prevail…”

Clearly, some judges feel that the Bureau and the FHFA are unconstitutionally formed. Whether these agencies will change their structure in response to these decisions is unclear.

California Bill May Disadvantage Small Brokers

July 17, 2018A California State Assembly bill that carefully defines what a broker is, could significantly affect small, unlicensed brokers, according to Tom McCurnin, an attorney at Barton, Klugman and Oetting in Los Angeles.

Assembly bill 3207 enumerates the ways that the bill would depart from the current law. Most notably, the definition of a broker would be far more precise. The current California Licensing Law, which requires brokers to be licensed, defines a broker as “anyone who is engaged in the business of negotiating or performing any act as a broker in connection with loans made by a finance lender.”

Tom McCurnin – Barton, Klugman & Oetting LLP

Tom McCurnin – Barton, Klugman & Oetting LLP“It’s a circular definition,” McCurnin said. “It presently says that a broker is someone who is brokering transactions.”

Essentially, it defines a broker as a broker, leaving plenty of room for ambiguity.

“With respect to registering to conduct business in the state of California, we’ve got tons of brokers doing deals in California, but they’re not licenced here,” McCurnin said. “They do deals in California, but they’re located in Florida or New York or Michigan. They’re making money in the state of California. Why shouldn’t they pay their fair share of taxes?”

People can always evade the law and not get licenced. But the idea behind this bill is that by making the definition of a broker perfectly clear, it’s no longer possible for a broker to make an argument that they’re not really a broker. With the language in the bill, a broker would be in clear violation of the law if they don’t obtain a licence.

The new definition of a broker would be “anyone who, among other things, transmits confidential data about a prospective borrower to a finance lender with the expectation of compensation.” McCurnin notes that “expectation of compensation” is an important phrase, currently used to describe real estate brokers, because it states clearly that the broker intends to earn money from the consumer. The proposed definition in the bill continues to define a broker as someone who “participates in any loan negotiation between a finance lender and prospective borrower, participates in the preparation of loan documents, communicates lending decisions or inquiries to a borrower, or charges a fee to a prospective borrower for any services related to an application for a loan from a finance lender.”

This definition leaves little room for debate. So what does getting a California State broker licence entail? It requires that a broker have at least $25,000. Beyond this, McCurnin says it inquires primarily about three other things: 1) if you have a criminal record (fingerprints are required), 2) what type of loans you intend to broker (secured, unsecured, etc.), and 3) the size of the loans you intend to broker. There are different regulations for different loan sizes.

Being licensed requires being registered to conduct business in the state of California. And a registered business must pay taxes on earnings in the state. With this in mind, McCurnin said the passage of this bill could be a win for California in that it could result in more out-of-state brokers getting registered and paying taxes on their earnings in the state.

At the same time, should the bill pass, McCurnin thinks it would be a big loss for the small broker who is either unable to show $25,000 or who might have something unsavory to hide. But if the small broker working from his basement has enough capital and is willing to state what he intends to broker in California, then obtaining the license shouldn’t be a problem.

The bill passed in the state Assembly and is being reviewed in the Senate. An amendment to the bill was made on July 5. Another California bill of great significance to the alternative lending industry is SB-1235, which has passed in the state Senate and is being reviewed in the state Assembly. McCurnin said he believes that the broker bill will pass.

“California is a very liberal place,” McCurnin said. “It’s like another country.”