Industry News

OnDeck Repurchased 3.2M Shares, Reports $8.7M Q3 Profit

October 24, 2019 OnDeck announced this morning that it has repurchased 3.2M of its own shares for $11M since making its buyback announcement on July 29th. The company intends to repurchase another $39M worth.

OnDeck announced this morning that it has repurchased 3.2M of its own shares for $11M since making its buyback announcement on July 29th. The company intends to repurchase another $39M worth.

OnDeck was profitable in Q3, reporting a net income of $8.7M on originations of $629M. Although that was an increase over the previous quarter, the year-over-year decline was said to be a reflection of “tightening underwriting criteria and market dynamics.”

The average term loan was for $56,000 with an average maturity of 13 months. The company’s line of credit program is growing and now accounts for 21% of the company’s total loans and finance receivables at quarter-end, up 15% from last year.

“OnDeck expects the current operating environment to extend into 2020 with increased profitability,” their quarterly report said.

Avi Wernick and Boris Kalendarev Move to RDM Capital Funding

September 23, 2019 Avi Wernick and Boris Kalendarev are joining RDM Capital Funding as the new Director of Partnerships and Strategy and CFO/COO, respectively.

Avi Wernick and Boris Kalendarev are joining RDM Capital Funding as the new Director of Partnerships and Strategy and CFO/COO, respectively.

The move comes after a fruitful year for the company, with it securing a $7.5 million credit facility from Charleston Capital, an amount that it has since extended; upping its funding originations from $300-500,000 per month at the beginning of 2018 to over $2.5 million currently; and witnessing 300% growth over the previous 12 months.

Wernick is moving from BlueVine, where he was a Business Development Manager. Seeking to develop and create new opportunities for RDM, as well as ensure the stability of these prospects, Wernick says that he’s bringing with him the skills and lessons learned at the New Jersey-based funding company, believing that how he will operate in RDM will serve as a “nod to his time and the guys at BlueVine.”

Prior to this, Wernick had done consulting work for Morgan Stanley in the early 2010s. Saying that he “wasn’t enthralled by” the world of institutional finance, he moved to RDM during its launch year, 2015, before starting at BlueVine in February 2018. Speaking of his homecoming to RDM, Wernick notes that he is excited to return to the “blend of ideas” that he says is integral to RDM’s approach towards operations and culture.

Kalendarev echoes this, saying that himself, Wernick, and Reuven Mirlis, RDM’s CEO, have been friends outside of business for years and that he enjoys the overlap of his personal and professional connections. “It’s something we arrived at gradually, it wasn’t like, ‘hey, we’re all working in finance, let’s pool our efforts.’”

Coming from Santander, where he was a Vice President, Kalendarev will be focusing on the operations of RDM. Having been a Financial Advisor for Wachovia Securities during the early years of college, as well as beginning his time at Santander during the days of his senior year, Kalendarev has been in finance for over ten years. On his departure from the Spanish bank he said that it “was a very hard role to leave,” but that he savored the risk which came with building a less established financial entity, saying that “you’re more aligned with it, you’ve got skin in the game.”

On the pair joining, Mirlis had to say, “We’re very, very excited for both Avi and Boris. They have an immense amount of value and they’re going to be an integral part of our group going forward. We’re extremely excited to have them on board and to see what’s to come going forward.”

When asked about what exactly may come in the future for RDM, Mirlis noted he plans to reach 300% growth for a second year in a row.

On the topic of the recent COJ bill, the new hires were optimistic, with Kalendarev remarking that RDM stopped using the contracts over eight months ago and that he thinks “it’s good for the space.” “It’ll be a challenge for these companies who tried to get rich quick and take short cuts and not build a sustainable operation,” said Wernick. “You know regulation is a scary thing.”

Stripe Ventures Into Merchant Cash Advance Financing

September 6, 2019 Stripe, a payments firm lauded as the world’s most valuable private fintech company (at $22.5B), has officially launched a merchant cash advance product.

Stripe, a payments firm lauded as the world’s most valuable private fintech company (at $22.5B), has officially launched a merchant cash advance product.

Dozens of news outlets have announced that the company is providing loans, but that’s not all, deBanked has learned. Both loans and merchant cash advances are available.

The company’s FAQ page originally explained the “Capital” product as a merchant cash advance but it’s since been updated to reflect that they offer access to both merchant cash advances and loans. An official Stripe spokesperson also clarified that an offer could be an MCA or a loan. The updated FAQ says that funding terms would be available in the customer dashboard, in the funding contract, and that which one a customer qualifies for depends on the specifics of their business.

Stripe merchant account customers can find out if they’re eligible for funding in their dashboard. If they’re not, they can still send Stripe a note through the dashboard to signal that they’re interested, say how much they’re looking for, and select what they plan to do with the funds. Stripe says they will not review your credit report and that all offers are based solely on Stripe transaction history.

The new product will not disrupt the separate integration with Funding Circle, according to a statement provided to Digital Transactions. Stripe customers can still apply to Funding Circle by connecting their Stripe account. Funding Circle offers term loans that range from six months to five years.

Stripe’s MCA product is currently only available in the US, but the company’s founders, Patrick and John Collison, brothers, hail from an unlikely place, rural Ireland. The company handles tens of billions of dollars in payments a year across 34 countries.

Like other recent entrants into the small business funding space, Stripe’s advantage is its ability to tap into its existing customer base. Other payments companies such as PayPal and Square, for example, were among the top four largest originators (for which public data is available) of alternative small business funding in 2018.

Note: This article has been updated to reflect the changes made on Stripe’s website as well as an additional clarification from the company.

IOU Financial Originates $38.5M in Q2

August 26, 2019IOU Financial originated $38.5M in loans in Q2, up from $32.8M the quarter before. The company said that the figure was actually a 31.8% increase over Q2 2018.

In a press release, IOU CEO Phil Marleau said, “IOU delivered strong loan origination and revenue growth in the second quarter of 2019 and continued to post positive earnings. We remain committed to our strategy of profitable growth which continues to deliver consistent and favorable results since its implementation.”

IOU is traded on the Toronto Stock Exchange and has a market cap of $19.3M.

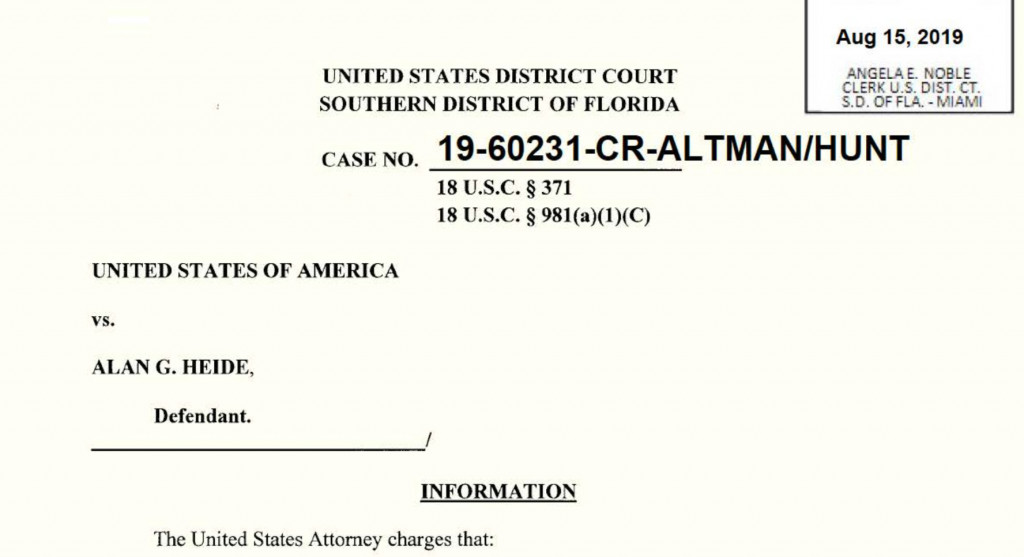

Alan Heide, CFO Of 1 Global Capital, Hit With Criminal Charge & SEC Violations

August 15, 2019

Update: Alan Heide has pleaded guilty to one count of conspiracy to commit securities fraud.

The former CFO of 1 Global Capital, Alan Heide, was stacked with bad news on Thursday. The US Attorney’s Office for the Southern District of Florida lodged criminal charges against him at the same time the Securities & Exchange Commission announced a civil suit for defrauding retail investors.

Heide was criminally charged with conspiracy to commit securities fraud.

According to the criminal complaint:

It was a purpose of the conspiracy for the defendant and his conspirators to use false and fraudulent statements to investors concerning the operation and profitability of 1 Global, so that investors would provide funds to 1 Global, and continue to make false statements to investors thereafter so that investors would not seek to withdraw funds from 1 Global, all so that the conspirators could misappropriate investors’ funds for their personal use and enjoyment.

He is facing a maximum of 5 years in prison.

1 Global Capital CEO Carl Ruderman, who recently consented to judgment with the SEC, has not been charged criminally to-date. However, he is mentioned throughout the pleading against Heide as “Individual #1 who acted as the CEO of 1 Global.”

Civil charges were simultaneously lodged by the SEC.

According to the SEC’s complaint:

Although 1 Global promised investors profits from its short-term merchant cash advances to businesses, the company used substantial investor funds for other purposes, including paying operating expenses and funding Ruderman’s lavish lifestyle. The SEC alleges that Heide, a certified public accountant, for nine months regularly signed investors’ monthly account statements that he knew overstated the value of their accounts and falsely represented that 1 Global had an independent auditor that had endorsed the company’s method of calculating investor returns.

According to an SEC statement, Heide agreed to settle the SEC’s charges as to liability, without admitting or denying the allegations, and agreed to be subject to an injunction, with the court to determine the penalty amount at a later date.

1 Global Capital filed for bankruptcy last year after investigations by the SEC and US Attorney’s Office hampered their ability to raise capital. Ruderman’s recent settlement with the SEC put him on the hook for $50 million to repay investors.

LendingPoint Places Seventeenth on Inc. 5000

August 14, 2019 Today Inc. 5000 released is 2019 list of the fastest growing private companies in America, featuring alternative finance company LendingPoint in seventeenth place after it witnessed a three-year revenue growth of 9,265%. LendingPoint offers consumer loans of up $25,000 and provides financing to merchants, service providers, and medical institutions via its LendingPoint Merchant Solutions program.

Today Inc. 5000 released is 2019 list of the fastest growing private companies in America, featuring alternative finance company LendingPoint in seventeenth place after it witnessed a three-year revenue growth of 9,265%. LendingPoint offers consumer loans of up $25,000 and provides financing to merchants, service providers, and medical institutions via its LendingPoint Merchant Solutions program.

This is the Atlanta-based business’s debut on the list and it comes after LendingPoint had a strong twelve months, with it being on track to reach $100 million per month in loan originations by the end of 2019 as well as it being the year the company turned profitable. On top of these, LendingPoint also has plans to expand its operations by hiring an additional 100 people, bringing its Atlanta HQ up to nearly 300 staff members.

In a press release, LendingPoint CEO Tom Burnside claimed that “Our platform saw more originations in 2018 than in 2015, 2016 and 2017 combined [sic], and at the same time our credit performance improved allowing us to facilitate more financing for consumers online and at the point of sale.”

Such growth is attributed by Burnside to LendingPoint’s use of technology. “We started by using data and technology to provide access to credit to underserved [sic], expanded to providing financing options at the point of sale to virtually everyone, and are now working on ways to integrate financing and payments with loyalty using blockchain to protect PII and enhance customer experience.” Such technology makes use of over 10,000 alternative data points, while also using FICO as a weighted factor of their analysis, to determine an applicant’s approval.

“We spend a lot of time cross-tabularizing the data points,” said Mark Lorimer, LendingPoint’s Chief Communications and Public Affairs Officer, when asked about the company’s approach to tech. Confronted by vast amounts of data, Lorimer noted how LendingPoint makes use of its technology to determine the value of different variables, “it really is a matter of taking the data and turning it into information.”

On the subject of LendingPoint’s placement on the Inc 5000, Lorimer told deBanked that the company was “not really surprised” by the news. According to him, his colleagues had been keeping an eye on the performance of those companies who previously placed on the list and were aware of what was required to appear on it, while his CEO has a more exuberant take on it: “It has been quite a ride for the last three years, and we’ve only scratched the surface.”

Funding Circle Originated $377M of US Loans in First Two Quarters of 2019

August 8, 2019Funding Circle originated $377M of loans in the US in the first six months of 2019, according to their latest public report. The company said that “growth was proactively controlled” and that they tightened higher risk band lending and increased prices. They’ve now loaned more than $2B cumulatively in the US since inception and their growth is being led by “new borrowers” that are being lured away from traditional lenders.

Funding Circle still lags behind PayPal, OnDeck, Kabbage, Square Capital, and Amazon in the US in loan origination volume, according to the deBanked small business finance rankings. Its closest competitors by volume are BlueVine, National Funding, and Kapitus.

Funding Circle Co-Founder & Managing Director James Meekings to Step Down

August 8, 2019 Funding Circle’s lackluster business performance has led to a casualty. Co-founder James Meekings, who serves as Managing Director of the UK Business (the company’s primary market), will be transitioning to a non-executive role on the UK board in Q3. He will no longer be MD, the company announced.

Funding Circle’s lackluster business performance has led to a casualty. Co-founder James Meekings, who serves as Managing Director of the UK Business (the company’s primary market), will be transitioning to a non-executive role on the UK board in Q3. He will no longer be MD, the company announced.

Lisa Jacobs, Funding Circle’s Chief Strategy Officer, will take over leadership of the UK business, the company subsequently disclosed.

Funding Circle went public less than 1 year ago on the London Stock Exchange. Since then the share price has plummeted by 75%.

The company has been busy trying to correct course through various maneuvers, one of which has been to cut CEO Samir Desai’s annual compensation.