Fintech

The Merchant’s Paying, The Bank Statements Were Fraudulent: Talking With MoneyThumb

September 16, 2025Small funders trying to tackle fraudulent submissions with no tools stand almost no chance in today’s environment. A recent survey conducted by both MoneyThumb and deBanked, for example, found that small funders experience fraud in 11.8% of applications on average, more than double the rate of larger funders. In the past, detecting altered documents such as bank statements, was best managed by experienced underwriters, but now with technology and AI in the palm of everyone’s hands, today’s fraud is often imperceptible to the naked eye.

“If you go back to 2020 when we created this [Thumbprint technology], I would say about 80 to 85% of bank statements that were fraudulent we would look at and say, ‘there’s the fraud,'” said Ryan Campbell, CEO of MoneyThumb. “Now it’s sub-5% that I can identify just with the human eye, and so technology has just absolutely created an environment where people can create fraud in a way that they never could.”

Thumbprint is MoneyThumb’s patented fraud detection tool. It can bolt into any industry CRM. Historically, an immediate default was the first clue that a fraudulent app had slipped through the cracks, but even accounts in good standing may not be what they seem.

“[What] we’ve seen is people take a smaller loan, then a slightly larger loan, and then the big one, the third loan—default,” said Campbell.

Bank statements that are otherwise in perfect order may have had their transaction descriptions edited so that loan deposits from third parties look like revenue or round-trip payments with the owner’s personal account are reclassified to look like daily sales. For fraud like this, the numbers are real, the statements are real, but what’s revenue and not revenue is obfuscated. And when the deal is approved based on the misleading metrics the scammers can actually stick around to pay for a while to convince the underwriters that they’re worthy of more.

Bank statements that are otherwise in perfect order may have had their transaction descriptions edited so that loan deposits from third parties look like revenue or round-trip payments with the owner’s personal account are reclassified to look like daily sales. For fraud like this, the numbers are real, the statements are real, but what’s revenue and not revenue is obfuscated. And when the deal is approved based on the misleading metrics the scammers can actually stick around to pay for a while to convince the underwriters that they’re worthy of more.

“We’ve run quite a few portfolio analyses for our funders, and so we’ll review all of the statements that they have, all of the funded deals that they’ve done, and many are surprised to find out that they actually have fraudulent paying accounts on their books,” Campbell said.

Since the rate of fraudulent applications is so material, catching the fraud as early as possible is paramount. This saves cost on underwriting, reduces time spent on deals that won’t move forward, and spares referral partners the pain of a deal getting killed at the finish line for an uncurable problem.

“As soon as it comes in, rather than wasting time on ‘are we collecting this? Are we extending offers?’ because think, it’s not just the fraud,” said Campbell. “Even if you can catch the fraud at the very end, somehow it’s not the catching part, it’s the fact that your staff is working a fraudulent deal for some matter of days. And Thumbprint just says, ‘get it out. It’s gone, done,’ and right at the beginning of the process.”

From the CERN Large Hadron Collider to Funding Working Capital Loans to SMBs

August 20, 2025When deBanked stumbled upon a scoop that DoorDash had begun offering merchant cash advances in late 2021, the tech and financing team behind it had not been on anyone’s radar. That company was Parafin which at the time appeared to be a startup comprised of former Robinhood engineers. But the backstory is a bit more wild because its CEO and Co-founder Sahill Poddar previously worked on getting his PhD by discovering the Higgs boson particle at CERN’s Large Hadron Collider. His credentials include a Doctorate (summa cum laude) in Particle Physics at European Council for Nuclear Research (CERN), Geneva, Switzerland and before that he was a Visiting Researcher for the Max-Planck Institute for Nuclear Physics in Germany. But today, at Parafin, his company makes $10 billion in funding offers to small businesses EACH DAY. The company has now funded more than 30,000 businesses since inception.

Turner Novak at The Peel secured Poddar as a guest on how Parafin came to be and it’s a must watch.

Adding Event Connections to DailyFunder

August 12, 2025MY BIG PET PEEVES WITH “EVENT APPS” ARE:

1. 95% of users stop using them after the event is over.

2. Most are white labeled from a third party with no customizable solutions.

3. They are generally zero-sum in that everyone can see you’re going or no one can. People want to choose their own visibility.

4. If a boss buys 10 tickets under their name for their team, it makes it hard for the individual team members to be able to access the app because their info isn’t in the system.

5. There are generally no moderation capabilities to limit or stop abuse.

6. Redundancy.

We had a deBanked Events App (2018 – 2023 white labeled), a deBanked App (2015 – 2017 white labeled), and a DailyFunder App (2013 – 2017 white labeled), but we recently rebooted a DailyFunder App only.

Why DailyFunder? With 17,000+ members, 3 million+ annual page views, and an average session > 10 minutes, it seems the most logical starting point to tackle point 1 above, which is keeping a party going 24/7 instead of just a few days before an event and never again right after. We’ve moved development in-house, no more white labels. We can put events in there whether they’re affiliated with us or not. You can let people know if you’re going or not. You can dm other people that plan to go. You can follow up with them afterwards. You can see the sponsors. We can put video content in there like tech companies that demoed or the interviews on the red carpets. No, you won’t see the whole attendee list, but you’ll be able to see those that want other people to connect with them at each one. You can use your real name or be pseudonymous. We can remove fakers. You can post on the forum. You can see what people are saying. It doesn’t all end when the event ends. You can see news headlines from deBanked and other video content we choose to put on there.

This is a work-in-progress but currently live in the Apple App Store and Google Play Store. If you have ideas or suggestions, email them to webmaster@dailyfunder.com. There’s some bugs we’re aware of. You must have a DailyFunder account already to log in. The registration process is still only on the website but we’ll change that.

Some thoughts are being able to add events like a Title sponsor’s cocktail party, a related golf-outing, etc. People are always asking which company is having a party after an event or before.

So instead of having to go on the forum, facebook groups, linkedin, or the whatsapp chats to be like “yo, xyz is happening.” or “who’s going?” we can just add it in here and then everyone can see them in one place to communicate with each other about them if they want to.

Open to suggestions.

How Are Your Sales Calls Going? How One AI System Can Score Performance

July 21, 2025 The subjectivity era of evaluating sales reps is over. Sales calls can now be dissected down to every little nuance of why something went right or wrong, and it can be done at scale with no human bias. These interactions can also be aggregated to determine strengths, weaknesses, trends, compliance, confidence levels, and more, all thanks to AI and technology available right now.

The subjectivity era of evaluating sales reps is over. Sales calls can now be dissected down to every little nuance of why something went right or wrong, and it can be done at scale with no human bias. These interactions can also be aggregated to determine strengths, weaknesses, trends, compliance, confidence levels, and more, all thanks to AI and technology available right now.

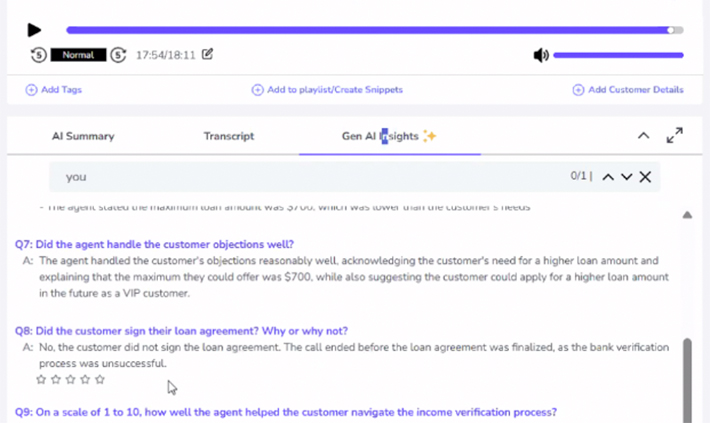

“The way [our] platform works is we integrate with the dialer,” says Atul Grover, Co-founder and VP of Sales for Enthu.AI. “Typically, what we have seen with our clients, the calls are automatically pushed within two or three minutes after the conversations are done.”

With Enthu, a company’s call recordings go through their AI system to be analyzed based on either their own scorecard, the client’s, or both. Whatever the outcome of the call, lost sale, closed deal, or neither, management receives a report to see how the rep performed. Did the rep try to build rapport? What were the objections? Did they handle objections well? Did the rep sound confident when answering difficult questions? Across hundreds or thousands of calls each week, any rep can get an unbiased report card of their strengths and weaknesses. These metrics can then be compared with peers, without the worry of human bias deciding the outcome. They can’t blame the boss for simply favoring another rep, for example.

Originally, when Enthu started, they focused mainly on keyword spotting for compliance purposes, evaluating whether or not reps were saying what they were supposed to across thousands of calls. But that had its limitations.

“That’s how we started our journey, using purely keyword spotting,” Grover says, “but the challenge over there is that you can’t basically expand or scale it. So that’s why we use our AI approach, where it’s primarily intent-based rather than keyword-based. So we look at the intent of all the conversations.”

Rather than AI replacing sales reps, as some theorize might happen over time, it can be used to make them a whole lot better. And this is already being employed today. Enthu, for example, is currently being used in financial services, healthcare, home industries, property management, and more. Grover says clients are already using it to measure disparities in call performance and then using those insights to coach reps who score on the lower end.

“Our platform also offers the ability to create a playlist for the good recordings, which you can use to train your new agents,” Grover says. “So rather than training in general that’s like, ‘okay, this is our company product, this is our company offerings, you should talk like this,’ they can share those good recordings with the new agents so they can listen to how their good sales agents are doing, and then get trained on the real data.”

Recording calls and finding good ones is not a new capability, anyone can do that. But it’s the ability to identify certain call situations at scale that makes all the difference when trying to evaluate and coach. If a new objection is tripping up the team, management can pull every instance it has come up, calculate its frequency, and use that information to determine the best path forward. These are things that would typically rely on the “vibe and feel” of the sales floor, as reps relay information to the boss, who must then assess whether the trend is legitimate or just a statistical blip.

Independent analysis can also be critical when a company is evaluating a lead source or referral partner, especially if that partner is also expecting to be judged objectively. And when the lead source changes, the AI can be told in advance whether the calls are outbound or inbound, hot or cold, or how they differ from other types of calls the company handles. The resulting evaluations can then reflect those circumstances.

Success, in this way, can be gamified, allowing reps to strive for higher grades across all areas of a call and objectively compare themselves to colleagues in an emotion-free environment. The AI can score each call or aspect of a call on a scale from 1 to 10 and produce a summary score for each rep over a day, week, or month, unlocking new motivational challenges. An underperforming rep could be recognized for a top score in overcoming objections, for example, even if they didn’t close the most deals. Picture a Broker Battle, but the judge is an AI.

And it’s not just sales. Clients can also use the technology for compliance, to determine whether proper disclosures were made, correct terminology used, and whether the tone of the call remained positive.

And it’s not just sales. Clients can also use the technology for compliance, to determine whether proper disclosures were made, correct terminology used, and whether the tone of the call remained positive.

“It’s definitely going to be great help for the sales organization,” Grover says. “And if we talk about the lending industry, you talk about compliance and everything, or let’s say the collections department, because they want to make sure that their agents are not screwing up, because there’s legalities involved if they mess up anything. So that’s what our system will flag, where they are doing right or where they’re doing wrong.”

If a client wants to keep keyword spotting as part of the analysis, they can. Grover says pre-set words can be marked as zero-tolerance or flagged for management. The more data and calls the system analyzes, the better it gets.

Grover adds that even if a client isn’t ready to fully integrate Enthu, they can still use old call recordings to access analytics.

“We have some customers in that space where they don’t have a dialer but they still have the recording,” Grover says. “So our platform also allows to upload the recordings directly by the client itself, on the platform itself, where they can upload the calls manually, then you’re still going to get the same intelligence, same analytics, same scorecard mechanism, even if you upload it manually.”

Block: Potential JPM Bank Account Data Access Fees Will Have No Impact to Our ‘Borrow’ Model

July 17, 2025Borrow, short-term consumer loan program by Cash App, will not be affected by fees JPMorgan intends to charge fintechs for bank account data access. That’s because Block’s Cash App doesn’t even need the data.

“Across Block we’ve been deliberate in how we’ve built products, leveraging internal data when we can to deliver value to our customers,” the company said in response to the JPM announcement. “For example, to date: the vast majority of Borrow volume has been underwritten using only Cash App data and less than 1% of U.S. BNPL GMV is paid back via ACH. While we can’t comment on the future, historically, our fees paid to data aggregators have been de-minimis.”

Heron Makes Big Splash in Small Business Finance Industry

July 15, 2025 Heron, a startup using AI to automate workflows, just raised a $16M Series A round. Already a well-known brand in the small business finance industry, the funds will be used to grow their presence, expand into adjacent verticals, and grow their go-to market & and engineering teams.

Heron, a startup using AI to automate workflows, just raised a $16M Series A round. Already a well-known brand in the small business finance industry, the funds will be used to grow their presence, expand into adjacent verticals, and grow their go-to market & and engineering teams.

While Heron serves top tier clientele like insurance carriers and FDIC-insured banks, its technology can be utilized at almost any level.

“Our technology is built to serve funders of all sizes from industry leaders like Bitty, Forward, Vox, and CFG to sub-five person shops originating hundreds of thousands of dollars a month,” the company told deBanked. “If a team is receiving 25 or more submission documents per day, Heron can deliver immediate value by automating their document intake and reducing manual review time. Our platform scales to meet volume, and we often see smaller, fast-moving teams who want to scale submissions and originations without scaling headcount benefit the most from Heron.”

Heron noticed that small business lenders were employing teams of underwriting analysts that spend hours on repetitive intake work and created a process to streamline it within seconds. Consequently, they’ve seen that improving efficiencies in this market has had a positive impact on the economy overall.

“At Heron, we believe that SMB lending is the backbone of the American economy — it powers everything from local restaurants to trucking fleets,” the company said. “But outdated, document-heavy processes slow things down. Heron helps lenders move faster and smarter, so they can get capital to the businesses that need it most.”

“Grok, Read My ISO Agreement”

July 14, 2025 Before having an attorney review an ISO agreement, consider having an intelligent LLM AI take a look at it and alert you to any immediate red flags. After all, some accusations of purported funder improprieties these days are actually rooted in actions well within the rights of the funder in the ISO agreements. D’oh! But if such agreements are too long or too legalese-sounding for you to make an immediate judgment, LLMs like ChatGPT-o3 or Grok4 or Claude or Gemini etc have become so adept at understanding a subject and communicating in a way that the user understands, that perhaps it’s worth having them take a look. (Maybe even at your existing agreements!)

Before having an attorney review an ISO agreement, consider having an intelligent LLM AI take a look at it and alert you to any immediate red flags. After all, some accusations of purported funder improprieties these days are actually rooted in actions well within the rights of the funder in the ISO agreements. D’oh! But if such agreements are too long or too legalese-sounding for you to make an immediate judgment, LLMs like ChatGPT-o3 or Grok4 or Claude or Gemini etc have become so adept at understanding a subject and communicating in a way that the user understands, that perhaps it’s worth having them take a look. (Maybe even at your existing agreements!)

For example, deBanked obtained a 15-page ISO agreement and asked Grok4 a bunch of casual questions. One of them was, “can this funder backdoor my deals?” Surprisingly, it named some weaknesses and loopholes that the broker should be aware of even if they were not easily exploitable. On the other hand, this ISO agreement already had some broker protections built in that the LLM pointed out, such as an in-house funding clause where the broker would be paid the commission if their submitted deal was funded by the funder’s in-house sales team within 30 days of the broker having submitted it. Did you know they had an in-house sales team?!?! Grok4 did!

Grok4 also gave me the heads up that there’s a 30-day clawback period and that my future renewal commissions would be forfeited if I were to be terminated for cause. Ironically, the LLM also gave me some unsolicited advice, telling me to diversify my funders and to watermark my docs “as per the new tool.” When I asked what tool it was even talking about, it specified Aquamark, which appeared on this site just a few months ago. Grok4 also said to use deBanked, lol. Thanks!

Recommendations to Protect Yourself

Operational Steps: Timestamp submissions, watermark docs (as per the new tool), and require written confirmations for all merchant interactions. Diversify funders.

Contract Tweaks: Negotiate for audit rights, higher breach penalties, or tech tracking of merchant contacts. Extend non-interference to 3-5 years (common in MCA).

Industry Tools: Join broker networks or use platforms like deBanked for alerts on shady funders.

Curious what your ISO agreements say? I used Grok4 for this experiment. Of course, you should actually be using a lawyer for a real assessment. Here’s a list of some to get you started.

CAFE’s Fall 2024 Accelerator Cohort a Success

November 25, 2024 deBanked attended and sponsored the final demo day of CAFE’s Fall 2024 Accelerator Cohort. CAFE, as previously profiled, is the non-profit Center for Advancing Financial Equity. The six members of the Cohort were Carvertise, GivingCredit, Kredit Academy, Odynn, Salus, and Prismm.

deBanked attended and sponsored the final demo day of CAFE’s Fall 2024 Accelerator Cohort. CAFE, as previously profiled, is the non-profit Center for Advancing Financial Equity. The six members of the Cohort were Carvertise, GivingCredit, Kredit Academy, Odynn, Salus, and Prismm.

As previously stated, the bi-annual accelerator aims to identify, support and grow extraordinary financial accelerated technologies and innovations. Hundreds of companies apply but only six get selected for each cohort.

The demo day took place inside the Fintech Innovation Hub, situated on University of Delaware’s STAR campus. It was a major success.

To learn more about CAFE, visit: https://ftcafe.org/