Crowdfunding

How Ireland’s Spark Crowdfunding Got its Start

October 5, 2019 “We’ve not invented anything new,” Chris Burge, CEO of Spark Crowdfunding, tells me. “We saw the rise of crowdfunding in Europe, the states, and the world and we thought, ‘well why doesn’t Ireland have one?’”

“We’ve not invented anything new,” Chris Burge, CEO of Spark Crowdfunding, tells me. “We saw the rise of crowdfunding in Europe, the states, and the world and we thought, ‘well why doesn’t Ireland have one?’”

We’re in the lobby of a Dublin hotel drinking coffee, right around the corner from Spark’s offices on South William Street. There are at least three other professional meetings going on over variations of hot drinks, the room serving as a haven from the uniquely cold-yet-clammy weather outside.

Burge tells me about how he came to be in alternative finance. An engineer by trade, Burge entered the field after both him and his business partner had found the traditional process of investing to be wanting. “Both of us had invested in the past and had found it cumbersome, long-winded, and expensive,” leading them to explore more accessible, less unwieldy options.

Thus, from such a hole in the market sprung Spark Crowdfunding. Offering equity investment options from as low as €100, Burge sought to streamline the investment by offering it via an online platform from which members can view pitch videos, pitch decks, and detailed documents.

Established in early 2018, the company saw its first big success in August of that year with Fleet, an Irish business that allows cars owners to rent their vehicles to the public from their driveways as well as gas stations. Asking for €275,000, Fleet received this and more, with the total amount invested reaching €385,000.

Established in early 2018, the company saw its first big success in August of that year with Fleet, an Irish business that allows cars owners to rent their vehicles to the public from their driveways as well as gas stations. Asking for €275,000, Fleet received this and more, with the total amount invested reaching €385,000.

Allowing for choice when deciding which investors to choose from and how much to take from who, Burge says that flexibility is key to their platform and likens it to Dragons’ Den with much more than five potential investors.

And with bank loans for small businesses becoming increasingly more difficult to access, Spark is positioned similarly to crowdfunding in the US. “Where a company would have previously gone to Allied Irish Bank or Bank of Ireland to borrow €100,000 in order to get their business off the ground, they’re now finding it very difficult and nigh impossible as well to get these loans, so we found that a lot of companies are coming to us to do this.” In addition to such an investment, startups in Ireland may receive extra funding from Enterprise Ireland, a government organization that provides aid to indigenous businesses and will match investments up to a point so long as the company meets certain requirements.

Accompany this with the lack of regulation in the crowdfunding space in Ireland and it would appear that the industry is set to expand.

And on the topic of expansion, Burge is keeping most of his cards to himself. “We know that Ireland is a small country compared to the rest of Europe, or compared to the rest of the world, so there’s a limited amount of stuff that we can do here, and so do we want to grow? Yes. Are we going to go to the states? Probably not. But the rest of Europe? Yes, absolutely. Have we picked out a few countries? Yes, we have.”

Crowdfunding Legal Limit Too Low for Intended Beneficiaries

July 25, 2018 Regulation Crowdfunding (Reg CF), a regulation that grew out of the Jumpstart Our Business Startups (JOBS) Act of 2012, was designed to allow non-accredited investors to invest relatively small amounts in startups. But the regulation seems not to be serving its purpose, according to people in the fintech investment community.

Regulation Crowdfunding (Reg CF), a regulation that grew out of the Jumpstart Our Business Startups (JOBS) Act of 2012, was designed to allow non-accredited investors to invest relatively small amounts in startups. But the regulation seems not to be serving its purpose, according to people in the fintech investment community.

Why is this? Because the maximum amount that can be raised in a single year under Reg CF is limited to $1,070,000.

“I’ve had clients consider [using] Reg CF, but when they see that they can only raise $1 million, they say it’s not worth the trouble,” said James P. Dowd, CEO of North Capital, a Salt Lake City-based broker-dealer that helps private companies raise money.

“I’m not anti-regulation at all, but if the reward is not there, people won’t go through the trouble,” Dowd said. “Let’s have regulations that are appropriate for the need.”

Dowd said that a small startup seeking funding for a series A round is typically looking to raise around $10 million. The $1.07 million cap for Reg CF is therefore inadequate. A startup’s other options for raising money under the JOBS Act include regulations D, S and A+. Dowd said that Reg D is the most common. It involves very little paperwork and is less expensive compared to other options. Reg S applies only to offshore investors and Reg A+ makes sense only if the startup is looking to raise $20 million or more because this option is costly to file.

All of these options require that investors be accredited, which translates to investors being wealthy. (Accredited investors must have a net worth of at least $1,000,000, excluding the value of one’s primary residence). On the other hand, if an entrepreneur opts to raise money through a Reg CF, investors need not be accredited, although there are still restrictions on how much they can invest, given their income.

Reg CF allows entrepreneurs to access a wider pool of investors. And Dowd, along with others in the investment community, believe that the current $1.07 million annual cap should be raised to as high as $20 million to satisfy the need of entrepreneurs who are looking to raise more money.

“The infrastructure for the crowdfunding industry has been tested and is ready to expand,” said Douglas S. Ellenoff, partner at Ellenoff Grossman & Schole who is an expert on crowdfunding.

Ellenoff said that there was much fear among regulators following the 2012 JOBS Act that crowdfunding would be ripe for fraud. But the fraud didn’t happen. He believes in raising the Reg CF cap to allow the crowdfunding industry to mature. And he believes that once the cap is raised, more substantial companies will start to use crowdfunding which further legitimate it as a valid way of raising money.

North Capital was founded by Dowd in 2008 and provides an array of financial advisory services to its clients. In addition to its Salt Lake City headquarters, it also has offices in Benicia, California and McAllen, Texas.

Equity Crowdfunding to Masses Slow Out of the Gate, But Pickup Expected

February 25, 2017

After a lackluster start, spectators are betting on more promising times ahead for equity crowdfunding to the masses.

Although it’s been talked about for years, it wasn’t until last May that the general public could buy shares of their favorite companies through equity crowdfunding. Before then, only accredited investors could be part of the crowd.

The new crowdfunding regulation, known as Reg CF, has been talked about for several years as a potential game-changer for small businesses seeking growth capital. But so far, it hasn’t gotten the fast-track reception that some industry watchers had hoped for. Between inception and January 16 of this year, 75 companies have run successful equity crowdfunding campaigns, raising $19.2 million, according to statistics compiled by Wefunder, an online funding portal for equity crowdfunding.

Even so, industry watchers aren’t discouraged, saying it takes time for any new product to catch on and to gain traction.

“Equity crowdfunding is in its infancy. It’s got to be a toddler before it can be a teenager, and it’s got to be a teenager before it can be grown up. I think in three to five years, equity crowdfunding will be all grown up,” says Kendall Almerico, a partner with the law firm DiMuroGinsberg in Washington, who represents numerous clients in Jobs Act-related offerings.

A YEAR OF TRIAL AND ERROR

Some industry watchers had hoped equity crowdfunding to the general public would take off immediately, on the heels of successful rewards-based crowdfunding sites like Kickstarter and Indiegogo. Consider that since Kickstarter launched on April 28, 2009, 12 million people have backed a project, $2.8 billion has been pledged, and 118,362 projects have been successfully funded, according to company statistics from Jan. 16.

People looked at Kickstarter’s accomplishments and projected that from day one, equity crowdfunding to the public would be an immediate success, Almerico explains.

Instead, Almerico says 2016 was a year of trial and error, in which companies seeking equity funding tested out the market and learned the process. Initially, there were several funding failures, where companies set fundraising goals that were too lofty and came away with nothing. Other companies have been hesitant to dip their toes into a market that’s still very new and unchartered.

“I’m not surprised that it has taken a little bit of time for companies to raise money this way,” Almerico says.

However, industry participants say that every success story encourages others and the market will continue to build on itself.

“We are very optimistic that 2017 will be the year it goes more mainstream in the U.S,” says Nick Tommarello, founder and chief executive of Wefunder, who expects crowdfunding levels in 2017 to reach three to four times what they were at the end of 2016.

WADING THROUGH UNCHARTERED TERRITORY

Certainly, Reg CF is still very new in practice. On October 30, 2015, the Securities and Exchange Commission adopted final rules to permit companies to offer and sell securities through equity crowdfunding for non-accredited investors. But it wasn’t until May 16, 2016 that this new type of investing actually became permissible.

Companies that want to raise money from the general public have to do it through a funding portal that is registered with the SEC. As of mid-January, there were 21 funding portals, according to a listing on Finra’s website. The bulk of the funding thus far has come through the portals Wefunder, StartEngine and NextSeed, according to statistics compiled by Wefunder. Indiegogo, best known as a leader in perks-based crowdfunding, has also gotten a fair amount of business. Indiegogo launched an equity crowdfunding portal late last year through a joint venture with MicroVentures, an online investment bank.

There are significant rules when it comes to members of the general public investing in equity deals; how much you can invest per year depends on your net worth or income. Everyone can invest at least $2,000, and no one may invest more than $100,000 per year, according to SEC rules.

Meanwhile, companies are limited to raising $1 million in a 12-month period using Reg CF. Also, they must raise enough to hit their funding target or the fundraising round is a bust. They can, however, use other avenues to raise money simultaneously, such as through accredited investors or venture capitalists. This can be an advantage for companies because it allows them to tap their customer base—a great marketing and customer-retention tool—and yet still seek growth financing from investors with deeper pockets.

Over time, as equity crowdfunding gains traction, Almerico predicts the SEC and Congress will revisit some of the regulations and tinker with the laws to make them even more user friendly. And that too, will help crowdfunding gain ground with investors and companies, he says.

For instance, under current rules, a company can’t market its offering until it goes live, at which point additional marketing restrictions set in. Congress and the SEC will likely change some of these restrictions to make the rules more similar to Regulation A, which covers offerings of larger sizes, Almerico says.

A CONSUMER-FACING PROPOSITION

For the most part, companies that are consumer-facing as opposed to B2B will have the most luck with equity crowdfunding. For one thing, consumer-facing companies often have an easier time explaining their story to the public. Also, there’s real benefit for consumer based businesses to get their customers to sink money not only into a company’s product, but behind the scenes as well. Thus far companies that have sought funding under Reg CF run the gamut from breweries to tech startups, Wefunder data shows.

When it comes to equity crowding, investment levels tend to be small. Wefunder stats shows that 31 percent of investments made through its own platform are $100 and 76 percent of investments are under $500. “The whole point is to have lots of investors investing small amounts of money and together they add up,” Tommarello explains.

One of Wefunder’s largest offerings was Hops and Grain Brewing, a microbrewery based in Austin, Texas. The company is one of three businesses to raise $1 million on Wefunder, and more than 70 percent of the money came from its own customers, according to Tommarello. “Equity crowdfunding allows customers an opportunity to back things they really care about and it’s great marketing for the company too,” he says.

Another company, Snapwire Media Inc., a start-up in Santa Barbara, California, also believes in the power of the crowd to raise funds and gain marketing traction. Chad Newell, the company’s chief executive, says Snapwire wasn’t at a point where it felt ready to solicit venture capital money, but felt confident that its users, who were already passionate about its services, would become their biggest advocates.

The company, which connects a new generation of photographers with businesses and brands that need on-demand creative imagery, was launched in 2014. It previously raised $2 million from accredited investors before raising $179,065 from the general public on the funding portal StartEngine. In December 2016, the company launched a campaign to raise additional funds on Wefunder.

“Because we had a strong community and such a large one, we felt it was a good way to raise funds. Why not raise it from the people that care about the product the most?” Newell says.

OVERCOMING THE HURDLES OF NEWNESS

Because equity crowdfunding to the general public is so new, there’s still a lot of uncertainty about how the process works—both among companies looking to raise money and potential investors.

“The biggest hurdle today is that equity crowdfunding is still underground versus rewards-based crowdfunding,” says Howard Marks, co-founder and chief executive of the online portal StartEngine. “It’s tiny. It’s small. It’s nothing. It’s not even a dot in the grand scheme of things,” he says.

At this point, many people still don’t realize they can invest, or how to invest. He likens equity crowdfunding to index funds or junk bonds that were once completely unknown products. Over the years, however, they gained broad acceptance and are now widely used investment vehicles. “Every time there’s a new financial product that comes out, it takes time,” he says.

At this point, many people still don’t realize they can invest, or how to invest. He likens equity crowdfunding to index funds or junk bonds that were once completely unknown products. Over the years, however, they gained broad acceptance and are now widely used investment vehicles. “Every time there’s a new financial product that comes out, it takes time,” he says.

In December, five new companies used StartEngine for equity crowdfunding. In January, he expects there to be more than 10. By the middle of next year, he predicts there could be 20 a month, and in two years from now he’s hopeful to be doing about 500 equity deals a month.

“Within five years, our plan is to have 5,000 companies on the platform,” he says. “The demand for capital is pretty large.”

At this point, Wefunder is the largest platform for Reg CF offerings in terms of dollars funded, successful offerings and number of investors.

According to data through January 16, forty-six of the seventy-one companies that listed on its platform, or 65 percent, had successful offerings, meaning they reached their investment goals.

Some funding portals have felt the pangs of being new to the industry and are trying to get their bearings to compete more effectively.

Vincent Petrescu, chief executive of truCrowd Inc, a funding portal based in Chicago, says his company got registered in May 2016 and spent the rest of the year learning the lay of the land. Ultimately, truCrowd decided it would be better off specializing in a few verticals than going after all types of companies. Its plan now is to focus on the cannabis industry and the HR space.

“I think that the potential is huge. There are lots of good companies out there that need capital,” he says.

THE SNOWBALL EFFECT

Wefunder data shows that investors who buy into one deal tend to do another deal shortly after, so it’s a compounding effect, Tommarello says. “It’s a snowball rolling down a hill. We’re developing a whole new class of mini angel investors,” he says.

In terms of future growth, Petrescu of truCrowd says the biggest hurdle for the industry is exposure. Lots of people still don’t know about it, and they are still in the mindset that it’s illegal because it was for so long.

He says he’s not too concerned, though, because the UK had a similar experience when equity crowdfunding to the general public first started there a few years back. As soon as the success stories start to become more publicized and people see the returns that are possible, he predicts interest will grow. “The potential is there. No doubt about it,” he says.

For companies that are giving more thought to equity crowdfunding, it may help to seek out advice from others that have already traveled this road. Newell of Snapwire says he gets calls every week from company founders to ask about his experience with equity crowdfunding and to discuss in further detail whether it might be the right option for them.

Newell tells companies that ask him about equity crowdfunding that it’s an effective way to raise funds, with certain caveats. For instance, you really have to understand the rules of what you’re allowed to do and what you can’t do because there are many more restrictions when marketing to the general public versus accredited investors. You also have to be good at marketing—or hire a company to do it on your behalf—and have a sizable group of users that you think will want to invest in your future.

“It’s been a great source of capital for Snapwire because of our passionate community. I caution any company that doesn’t have a large community to be careful about spending time and resources and have realistic expectations,” he says.

He also says companies should have realistic fundraising goals since it is unusual—at least at this juncture—to raise a million dollars from small investors through equity crowdfunding. It’s more realistic to expect to raise $200,000 to $500,000, he says.

“I think everyone gets attracted to the top number. But that’s not necessarily what happens. Equity crowdfunding should be complementary to any funding strategy. By itself, it’s not some magic bullet,” he says.

Meet the Lending Platform With 0% Interest (Kiva)

January 6, 2016 Chany of Angela’s Boutique in Philadelphia, PA needs $5,000 to help purchase new signage and lighting to improve her storefront. She’s been turned down by banks even though she’s been in business for more than five years. 61 participants have already contributed to her loan thanks to a marketplace lending platform, which puts her very close to her goal. If it funds, all of the participants will get back their principal from her payments over the next 24 months and NO interest.

Chany of Angela’s Boutique in Philadelphia, PA needs $5,000 to help purchase new signage and lighting to improve her storefront. She’s been turned down by banks even though she’s been in business for more than five years. 61 participants have already contributed to her loan thanks to a marketplace lending platform, which puts her very close to her goal. If it funds, all of the participants will get back their principal from her payments over the next 24 months and NO interest.

Meet Kiva Zip, the anti-Lending Club because the borrowers are far from anonymous and the yield delivered to investors is negative due to inflation.

Angela’s Boutique, which is a real prospect on the Kiva Zip platform, includes a picture of the owner, her bio, endorsements, and comments from supporters.

According to Jessica Feingold, Kiva’s East Coast Manager of Development, “Kiva is the world’s first and largest crowdfunding platform for social good with a mission to connect people through lending to alleviate poverty and expand economic opportunity.”

And just like Lending Club, contributions as small as $25 are accepted. Obviously structured as a non-profit, “Kiva and its growing global community of 1.2 million lenders has crowdfunded more than $775 million in microloans to over 1.7 million entrepreneurs in 83 countries, all the while maintaining a 98% repayment rate,” according to Feingold.

Normally thought of as an overseas endeavor, Feingold said that “in 2011, Kiva launched Kiva Zip, a pilot program in the US that provides 0% interest crowdfunded loans to small business entrepreneurs.” Their underlying purpose and target market sounds very much like those being served by for-profit alternative lenders. “Kiva doesn’t require a minimum FICO score, collateral, or a minimum operations period for the business,” Feingold said.

Since inception they’ve made loans to over 1,800 borrowers in 47 days states, Peru, and Guam.

Notably, Lending Club promises borrowers that their “identity will at all times remain confidential and not be disclosed to anyone,” according to their website. Kiva by contrast is looking to “instill empathy” in their lenders. “We want to show that whether in East New York or Uganda, underserved entrepreneurs are credit-worthy, and will pay you back,” Feingold said. “All of these features on the Kiva websites enhance our ability to do so.”

While there is definitely a certain allure about being able to see the borrower for yourself, the concept seems to fly in the face of Dodd-Frank’s Section 1071 which stipulated that lenders are prohibited from knowing the sex and gender of business loan applicants. While the CFPB is not currently enforcing the law until the rules can be clarified, Democratic members of Congress have been pushing them to take action.

While there is definitely a certain allure about being able to see the borrower for yourself, the concept seems to fly in the face of Dodd-Frank’s Section 1071 which stipulated that lenders are prohibited from knowing the sex and gender of business loan applicants. While the CFPB is not currently enforcing the law until the rules can be clarified, Democratic members of Congress have been pushing them to take action.

According to the law, no loan underwriter or other officer or employee of a financial institution, or any affiliate of a financial institution, involved in making any determination concerning an application for credit shall have access to any information provided by the applicant about whether or not the business is women-owned or minority owned.

As small businesses often celebrate the heritage of their founders, and at times that can be the entire reason customers buy from them in the first place, the law has presumably put the small business lending world in an awkward position (and that’s why the law should be repealed). Non-profits like Kiva have embraced the very things that make a small business bankable outside of a credit score, like the owner, their background, and their story.

Borrowers on the Kiva Zip platform don’t raise all the money from strangers though. Their credit-worthiness is based on their ability to recruit friends and family to fund a small portion of their loan. The other lenders though of course may make their decisions based on the numbers or entirely on the perceived cultural, racial, or gender values of the borrower, all of the things that the CFPB is attempting to eradicate in the for-profit arena.

I didn’t ask Kiva any questions about Dodd Frank or Section 1071, but many people might empathize with their empathy approach as a way to fund small businesses that otherwise don’t qualify for bank loans. Its reminiscent of the subjective underwriting that a lot of alternative lenders and merchant cash advance companies employ to get deals done that banks won’t touch.

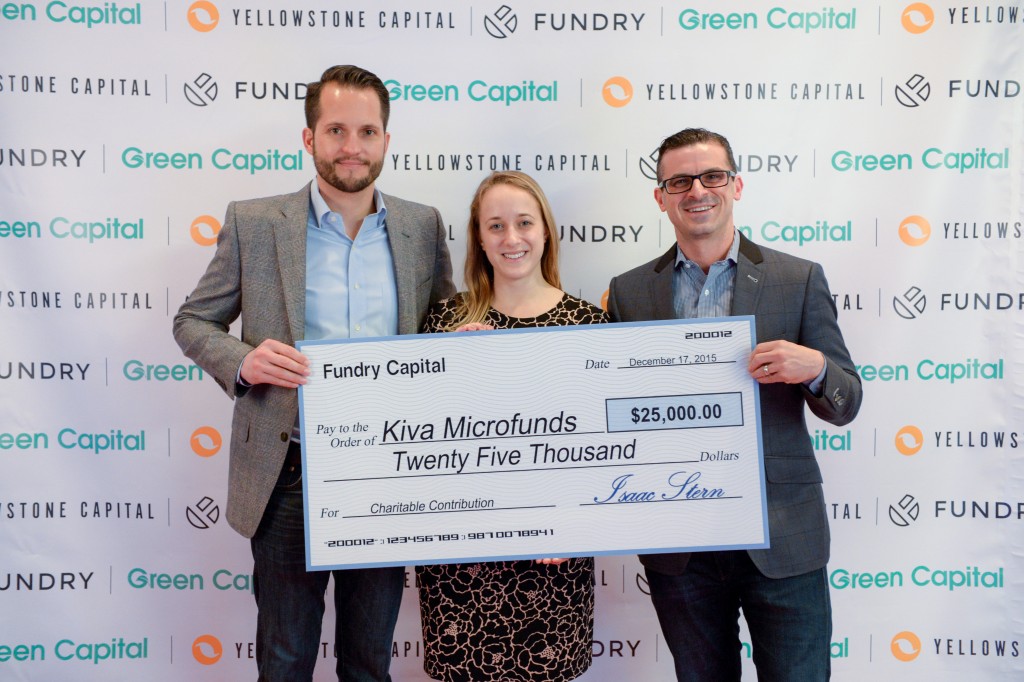

Not so coincidentally, Fundry, Yellowstone Capital’s parent company, donated $25,000 to Kiva just last month to support their cause.

Kiva’s Feingold (pictured at center above) said in regards to that, “Kiva is thrilled to receive a grant from Fundry to further our work to make credit more affordable.”

LendIt Conference: The State of Alternative Business Lending

May 6, 2014 Have you heard? Banks aren’t lending. Nobody at LendIt seems to mind though. Ron Suber, the President of Prosper Marketplace, said earlier today that banks are not the competition. That’s an interesting theory to digest when contemplating the future of alternative lending. If banks are not the competition, then who is everyone at LendIt competing against? I think the obvious answer is each other, but much deeper than that, the competition is the traditional mindset of borrowers.

Have you heard? Banks aren’t lending. Nobody at LendIt seems to mind though. Ron Suber, the President of Prosper Marketplace, said earlier today that banks are not the competition. That’s an interesting theory to digest when contemplating the future of alternative lending. If banks are not the competition, then who is everyone at LendIt competing against? I think the obvious answer is each other, but much deeper than that, the competition is the traditional mindset of borrowers.

The biggest challenge the wider alternative lending industry faces is awareness and understanding. Those happen to also be two of Suber’s three edicts for growth. The third is education. Just because alternatives are available today doesn’t mean that potential borrowers know about them or feel comfortable enough to use them. Today we are competing against the old way of thinking.

Revolution?

Other products in the new “share economy” have encountered a similar struggle. Several presenters today cited Uber as having revolutionized the way people use taxis. “A long time ago, people used to stand on corners and hold out their hand to get a cab, but that’s all changed,” was the oft-paraphrased proof that age-old industries were falling like dominoes. But as a New York City resident, I hadn’t quite noticed a change at all. Hailing cabs off the street is still very much the norm. It is only by sheer coincidence that I used Uber for the very first time to travel to JFK airport on my way to this conference.

I first encountered Uber a year ago when an acquaintance dazzled me with his ability to summon a car using an app on his phone. It was then that I became aware, but I did not understand how it worked. It took me 12 months to get comfortable enough to try it myself, and the experience was okay I guess if you discount the fact that my driver went through the E-ZPass lane without actually having an E-ZPass. Needless to say, that led to a major holdup that caused me to almost miss my flight.

If it took me a year to get past the confusion of hailing a cab from my phone, I can only imagine what potential borrowers must think when told they can raise money from their peers, the crowd, or a lender that requires payments to be made every single day.

Perhaps most telling about the awareness challenge, is that many people I’ve spoken to at LendIt had never heard of a 16 year old product known as merchant cash advance. That speaks volumes about how much more work merchant cash companies still have to do in order to gain mainstream awareness.

Even those fully aware were not entirely certain about how to define the product. In the Online Lending Institutional Investors Panel, merchant cash advance was briefly discussed as a topic but it was almost entirely spoken in the context of being something that OnDeck Capital does. That would come as disheartening news to OnDeck since they have spent considerable resources in positioning themselves as anything but a merchant cash advance company. Confusion over what somebody is or isn’t will probably increase especially as alternative lenders from different industries start to compete for the same clients.

Funding businesses instead of people

Brendan Ross, the President of Direct Lending Investments, and the moderator of the Short Term Business Lending panel pointed out that a dentist could pursue two different loan options and get completely different results. With excellent credit a dentist could expect to land a 3-5 year personal loan at 7-8% APR on a P2P platform. If he were to apply for the loan using his dental practice though, he could expect to incur costs over 25% and get nothing longer than 2 years.

Ross, who was a very active moderator, subscribes to the belief that businesses are overpaying for credit. Unlike the consumer loan space, there hasn’t been price compression. The cost of business capital remains high, perhaps higher than what is necessary to turn a reasonable profit. Ross argued that the padded cost serves as a hedge against defaults and economic downturns. “The asset class works even when the collection process doesn’t,” Ross said. “The model works with no legal recovery.”

Building on that premise, Ross asked the panelists if an increase in defaults were simply the cost of doing business towards automating the underwriting process.

Stephen Sheinbaum, the CEO of Merchant Cash and Capital argued that just the opposite had occurred, that automation had led to a decrease in defaults. Others on the panel confirmed a similar outcome, though Rob Frohwein of Kabbage admitted they could potentially weather higher defaults through automation by offsetting it against decreased infrastructure costs.

Noah Breslow of OnDeck echoed something similar to Frohwein in the Small Business Term Lending Panel. He asked this question, “Do underwriters add value or not?” and followed up by saying that 30% of their deals were still manually underwritten, usually the deals that are larger.

Is full automation right around the corner?

The debate between humans and computers in risk analysis is a featured segment in the third issue of DailyFunder that is being mailed out this week, but there is another angle that is seldom discussed, whether or not customers want automation. Breslow said today that, “if customers want full automation, we are prepared to deliver it.” They’ve learned over time that “many customers want someone to talk to at some point in the transaction.” Rohit Arora, the CEO of biz2credit expressed much of the same in a recent interview with DailyFunder’s Managing Editor Michael Giusti.

The only dissenting voice was Gary Chodes, the CEO of Raiseworks who seemed to be of the belief that human involvement in underwriting was nothing short of ridiculous. He stated that, “if you look back over the last 20 years, the loss rates on business loans under 24 months has been really low.” To him, that data seemed to be proof enough that complete automation could and should be achieved, though he admitted to performing back-end checks such as landlord verifications. They currently have no physical underwriters however.

Is there a transparency problem?

Tom Green, a VP of LendingClub shared an interesting tale. While trying to convince potential borrowers to ditch a merchant cash advance in favor of a LendingClub business loan, they get pushback on the cost of their money. The reason being? Some borrowers think they’ve already got a great deal or at least a better deal than what LendingClub is offering. The problem stems from the borrower’s belief that the holdback percentage set up in their future revenue sale (the most common way a merchant cash advance is set up) is the APR.

Merchant Cash Advance Companies pay cash upfront in return for a specified amount of a businesses’s future sales. They collect these sales by withholding a percentage of each credit card transaction or bank account deposit until the agreement is satisfied in full. On a dollar for dollar basis, the cost of these programs typically range from 20%-49%, but on an APR basis, substantially higher. The holdback % is not even a factor in the APR. Green said they’ve learned that some small business owners are not sophisticated when it comes to finance.

Merchant Cash Advance Companies pay cash upfront in return for a specified amount of a businesses’s future sales. They collect these sales by withholding a percentage of each credit card transaction or bank account deposit until the agreement is satisfied in full. On a dollar for dollar basis, the cost of these programs typically range from 20%-49%, but on an APR basis, substantially higher. The holdback % is not even a factor in the APR. Green said they’ve learned that some small business owners are not sophisticated when it comes to finance.

Ethan Senturia, the co-founder of Dealstruck would probably agree. Earlier today he said, “you need to speak the borrower’s language.” Some understand APR, some don’t. “Dealstruck offers more than just APR comparisons to borrowers,” Senturia said. “Whatever helps them understand.”

When the OnDeck Capital model and merchant cash advance model were questioned as possibly being bad for borrowers, Tom Green was quick to clarify. “There are different capital needs that small businesses have,” he said. And “there is a trade-off between the length of the term and the risk.”

OnDeck Capital’s clients are not entrepreneurs born yesterday. “The typical customer has been in business for 10 years,” Breslow said. Their deals are “structured to protect through daily and weekly payments in addition to the interest rates we charge,” something he reminded everyone was “not single digits.”

Still, transparency issues remain in business lending. Sam Hodges, the Managing Director of Funding Circle explained that when he was previously a small business owner, there were hardly any lenders willing to provide him with an amortization schedule. Ashees Jain, a managing partner of Blue Elephant Capital Management admitted he would find it hard to justify the high rates of merchant cash advance if asked by a regulator, so he’d rather not invest in that market. When it comes to those types of transactions, they “don’t want to have to explain themselves” at some point in the future.

Scott Ryles, the managing member of Echelon Capital Strategies, LLC commented on OnDeck capital’s model as unbelievable. “The arbitrage is huge,” Ryles said. And Eric Thurber the managing director of Three Bridge Wealth Advisors believes that alternative business lenders are at odds with themselves. “They always talk about their risk management,” Thurber said, but he feels that players in that industry are concerned with how much market share they have. That conflicts with risk management in his opinion.

They pay or they don’t

At the end of the day Ashees Jain said as far as unsecured loans go, “borrowers pay or they don’t.” The recovery process on secured loans can be 12-18 months Jain said, a statistic cited by Brendan Ross earlier in the day.

It’s clear at LendIt that there are a lot of products available, but Ryles summed it up nicely. In the consumer space, all the volume is in the 36 month installment loans, he reckoned. For businesses it’s merchant cash advance. “It’s an awareness thing,” Ethan Senturia said in regards to getting businesses to use alternative lending sources.

It is indeed. Awareness, education, and understanding…

Merchant Cash Advance Syndication: Crowdfunding?

March 28, 2014 You might not have known this, but one of the most lucrative opportunities in merchant cash advance is the ability to participate in deals. It’s a phenomenon Paul A. Rianda, Esq addressed in DailyFunder’s March/April issue with his piece, So You Want to Participate?

You might not have known this, but one of the most lucrative opportunities in merchant cash advance is the ability to participate in deals. It’s a phenomenon Paul A. Rianda, Esq addressed in DailyFunder’s March/April issue with his piece, So You Want to Participate?

Syndication is industry jargon of course. You probably know the concept by its sexier pop culture name, crowdfunding. For all the shadowy rumors and misinformation that circulates out there about merchant cash advance companies, they’re similar to the trendy financial tech companies that have become darlings of the mainstream media.

Did you know that many merchant cash advances are crowdfunded? To date, no online marketplace has been able to gain traction in the public domain aside from perhaps FundersCloud, so crowdfunding in this industry happens almost entirely behind the scenes. There is so much crowdfunding taking place that it’s becoming something of a novelty for one party to bear 100% of the risk in a merchant cash advance transaction. Big broker shops chip in their own funds as do underwriters, account reps, specialty finance firms, hedge funds, lenders, and even friends and family members of the aforementioned.

Merchant cash advance companies find themselves playing the role of servicer quite often, which is coincidentally the model that Lending Club is built on. A $25,000 advance to an auto repair shop could be collectively funded by 10 parties, but serviced by only 1. Each participant is referred to as a syndicate. This is not quite the same system as peer-to-peer lending because syndicates are not random strangers. Syndication is typically only open to businesses, and most often ones that are familiar with the transaction such as the company brokering the deal itself.

In the immediate aftermath of the ’08-’09 financial crisis, some merchant cash advance companies became very mistrusting of brokers and deal pipelines were going nowhere. Underwriters had a list of solid rebuttals for deals they weren’t comfortable with. “If you want us to approve this deal so bad, why don’t you fund it yourself!,” underwriters would say. Such language was intended to put a broker’s objections over a declined deal to bed. But with all the money being spent to originate these deals, it wasn’t long until brokers stumbled upon a solution to put anxious merchant cash advance companies at ease. “Fund it myself? I’d love to, but I just can’t put up ALL of the cash.”

And so some brokers started off by reinvesting their commissions into the deals they made happen. That earned them a nice return, which in turn got reinvested into additional deals. Fast forward a few years later and deals are being parceled out by the truckload to brokers, underwriters, investors, lenders, and friends. There’s a lot of money to be made in commissions but anybody who’s anybody in this business has a syndication portfolio. The appetite for it is heavy. Wealthy individuals and investors spend their days cold calling merchant cash advance companies, brokers, and even me, trying to get their money into these deals. They know the ROI is high and they want in.

That’s the interesting twist about crowdfunding in the merchant cash advance industry. You can’t get in on it unless you know somebody. There are no online exchanges for anonymous investors to sign up and pay in. It requires back door meetings, contracts, and typically advice from sound legal counsel. A certain level of business acumen and financial prowess are needed to be considered. These transactions are fraught with risk.

That’s the interesting twist about crowdfunding in the merchant cash advance industry. You can’t get in on it unless you know somebody. There are no online exchanges for anonymous investors to sign up and pay in. It requires back door meetings, contracts, and typically advice from sound legal counsel. A certain level of business acumen and financial prowess are needed to be considered. These transactions are fraught with risk.

In Lending Club’s peer-to-peer model, investors can participate in a “note” with an investment as small as $25. This is a world apart from merchant cash advance where it is commonplace to contribute a minimum of $500 per deal but can range up to well over $100,000.

Lending Club defines diversification as the possession of more than 100 notes. At $25 a pop, an investor would only need to spend $2,500. With merchant cash advance, 100 deals could be $50,000 or $10,000,000. By that measure, syndication is crowdfunding at the grownup’s table, a table that doesn’t care about sexy labels to appease silicon valley, only yield.

Strange merchant cash advance jargon keeps the industry shrouded in mystery. Did you know that split-funding and split-processing are terms often used interchangeably? Or that they have a different meaning than splitting? Or that the split refers to something else entirely?

Do you know what a holdback is or a withhold? How about a stack, a 2nd, a grasshopper, an ISO, an ACH deal, a junk, a reup, a batch, a residual, a purchase price, a factor rate, or a UCC lead?

Paul Rianda did a great job detailing the risks of syndication, but there is one thing he left unsaid, and that’s if you’re going to participate in merchant cash advances, you better be able to keep up with the conversation.

At face value, syndication is nothing more than crowdfunding. But if your reup blows up because some random UCC hunting ISO stacked an ACH on top of your split while junking him hard and upping the factor with a shorter turn, you just might curse the hopper that ignored your holdback and did a 2nd. And on that note, perhaps it’s better that the industry refrain from adopting mainstream terminology. We wouldn’t want everybody to think this business is easy. Because it’s not.

One factor to consider is the actual product being crowdfunded. In equity crowfunding, participants pool funds together to buy shares of a business. In crowdlending, participants pool funds together to make a loan. But in merchant cash advance syndication, participants pool capital to purchase future revenues of a business. An assessment is made to predict the pace of future income and a discounted price is paid to the business owner upfront. That purchase price is commonly known as the advance amount.

Syndication has more in common with equity crowdfunding than crowdlending. If you buy future revenues and the business fails, then your purchase becomes worthless. There is typically no recourse against the business owner personally unless they purposely interfere with the revenue stream and breach the agreement. Sound a bit complicated? It is, but crowdfunding in this space is prevalent nonetheless. To get in on it, you need to know someone, and to do it intelligently, you better know what the risks are.

If you want to sit at the grownup’s table and syndicate, consult with an attorney first. There’s a reason this industry hasn’t adopted sexy labels. It isn’t like anything else.

Merchant Cash Advance Term Used Before Congress

December 18, 2013 I’d like to think that the term, merchant cash advance, is mainstream enough that a congressman would know what it was. I have no idea if that’s the case though. What I do know is that Renaud Laplanche, the CEO of Lending Club gave testimony before the Committee on Small Business of the United States House of Representatives on December 5, 2013.

I’d like to think that the term, merchant cash advance, is mainstream enough that a congressman would know what it was. I have no idea if that’s the case though. What I do know is that Renaud Laplanche, the CEO of Lending Club gave testimony before the Committee on Small Business of the United States House of Representatives on December 5, 2013.

Watch:

In it, he argued that small businesses have insufficient access to capital and that the situation is getting worse. We knew that already. However, he went on to explain that alternative sources such as merchant cash advance companies are the fastest growing segment of the SMB loan market, but issued caution that some of them are not as transparent about their costs as they could be.

The big takeaway here is that he didn’t say they are charging too much, but rather that some business owners may not understand the true cost. I often defend the high costs charged in the merchant cash advance industry, but I’ll acknowledge that historically there have been a few companies that have been weak in the disclosure department. That said, the industry as a whole has matured a lot and there is a lot less confusion about how these financial products work.

Typically in the context Laplanche used, transparency is code for “please put a big box on your contract that states the specific Annual Percentage Rate” of the deal. That’s good advice for a lender and in many cases the law, but for transactions that explicitly are not loans, filling in a number to make people feel good would be a mistake and probably jeopardize the sale transaction itself. If I went to Best Buy and paid $2,000 in advance for a $3,000 Sony big screen TV that would be shipped to me in 3 months when it comes out, should I have to disclose to Best Buy that the 50% discount for pre-ordering 3 months in advance is equivalent to them paying 200% APR?

This is what happened: I advanced them $2,000 in return for a $3,000 piece of merchandise at a later date.

I got a discount on my purchase and they got cash upfront to use as they see fit. Follow me?

Now instead of buying a TV, I give Best Buy $2,000 today and in return am buying $3,000 worth of future proceeds they make from selling TVs. That’s buying future proceeds at a discounted price and paying for them today. As people buy TVs from the store, I’ll get a small % of each sale until I get the $3,000 I purchased. If a TV buying frenzy occurs, it could take me 6 months to get the $3,000 that I bought. But if the Sony models are defective and hardly anyone is buying TVs, it could take me 18 months until i get the $3,000 back.

In the first situation, if the TV never ships I get my $2,000 back. In the second situation if the TV sales never happen, I don’t get the 3 grand or the 2 grand. I’ll just have to live with whatever I got back up until the point the TV sales stopped, even if that number is a big fat ZERO.

Best Buy is worse off in the first situation, but critics pounce on the 2nd situation. APR, it’s not fair! Transparency, high rate, etc.

Imagine if every retailer that ever had a 30% off sale or half price sale one day woke up and realized the sale they had was too expensive and not transparent enough for them to understand what they were doing. If only consumers had given the cashiers a receipt of their own that explained that they would actually only be getting half the money because of their 50% off sale, then perhaps the store owners would have reconsidered the whole thing. 50% off over the course of 1 day?! My God, that’s practically like paying 18,250% interest!!!

To argue that a business owner might not understand what it means to sell something for a discount is like saying that a food critic has no idea what a mouth is used for.

I will acknowledge that issues could potentially occur if an unscrupulous company marketed their purchase of future sales as if it were a loan. That could lead to confusion as to what the withholding % represents and why it was not reported to credit bureaus. I’m all in favor of increasing the transparency of purchases as purchases and loans as loans, but let’s not go calling purchases, loans. Americans should understand what it means to buy something or sell something. Macy’s knows what they’re doing when they have a Black Friday Sale. They do a lot of business at less than retail price. They are happy with the result or disappointed with it. They’re business people engaged in business. End of the story.

In recent years, the term, merchant cash advance, has become synonymous with short term business financing, whether by way of selling future revenues or lending. When testimony was entered that many merchant cash advance providers charge annual percentage rates in excess of 40%, I do hope that Laplanche was speaking only about transactions that are actually loans. As for any fees outside of the core transaction, those should be clear as day for both purchases and loans. I think many companies are doing a good job with disclosure on that end already.

Part 2

The other case that Laplanche made was brilliant. Underwriting businesses is more expensive than it is to underwrite consumers. Consumer loan? Easy, check the FICO score and call it a day. That methodology doesn’t even come close to working with businesses. He stated:

These figures show that absolute loan performance is not the main issue of declining SMB loan issuances; we believe a larger part of the issue lies in high underwriting costs. SMBs are a heterogeneous group and therefore the underwriting and processing of these loans is not as cost efficient as underwriting consumers, a more homogenous population. Business loan underwriting requires an understanding of the business plan and financials and interviews with management that result in higher underwriting costs, which make smaller loans (under $1M and especially under $250k) less attractive to lenders.

Read the full transcript:

LendingClub CEO Renaud Laplanche Testimony For House Committee On Small Business

Merchant Cash Advance just echoed through the halls of Capitol Hill. And so it’s become just a little bit more mainstream, perhaps too maninstream.

Thoughts?

The Economics of Lending: Money vs. Goods and Services

May 21, 2013 If I were to offer you the choice between a free DVD with a retail value of $20 or a free $20 bill, which one would you take?

If I were to offer you the choice between a free DVD with a retail value of $20 or a free $20 bill, which one would you take?

Unless the DVD was something you were going to buy anyway or unless it was a rare item that is hard to find, you’d probably accept the cash. I would too, and that’s because I can turn around and exchange the $20 for anything I want. This isn’t to say that someone wouldn’t accept a DVD and give you something of value in return. You could probably do this but it would be a hassle compared to buying something with cash. Cash is the ultimate liquid asset. It has the same numerical value to all that evaluate it and it is acceptable everywhere.

If this is the case, then why do governments set limits on transactions that only involve cash vs. transactions that involve cash in exchange for a good or service? The reference I’m making here is to usury. Many states govern the interest that can be charged on a loan. This is done to protect borrowers but in doing so, they end up hurting them.

For example:

A manufacturer spends $100 to create a commercial refrigerator, but they sell it to a business for $1,000. That’s equates to a fee of 900%. Once the business books it as inventory, they will attempt to sell that refrigerator to a consumer for an even higher price to make a profit. While it’s a nice windfall for the manufacturer, it’s capitalism at its finest.

But what if the manufacturer lent the business $100 cash in exchange for $1,000 back? Does that change the transaction significantly? In our example above, the manufacturer gave the business an item worth $100 and got $1,000 cash in exchange. The business hopes to sell that item for more and turn a profit but a couple things could happen:

- Consumers might not be willing to pay more than $1,000 or anything at all for that model/make/color

- The refrigerator could get damaged and lose its value

If these scenarios were to occur, the business may try to liquidate the inventory for a lesser amount and take a loss, but doing that might not be easy. The refrigerator might have to be inspected and appraised before a buyer is confident to make the purchase. This problem doesn’t happen with cash. People don’t go out and appraise the value of a $100 bill to determine if it’s worth more or less than $100. The other possibility is that the business can’t liquidate it at all and they end up losing the entire $1,000 they spent.

What’s interesting is that if the business had accepted a $100 bill in exchange for paying $1,000 at a later date, that $100 bill wouldn’t have the real risk (discounting hyper-inflation) of becoming worthless tomorrow or becoming the object of a difficult liquidation.

So when faced with choices again… would you rather take a refrigerator someone spent $100 to make and try to sell it for more than $1,000 or would you rather someone give you $100 cash and you do whatever you want to try to turn that into more than a thousand bucks? On the one hand you have a refrigerator which might have a decent retail market and on the other hand you have cold hard cash that you can do anything with to try and make the necessary profit. You might choose refrigerator but you might choose the cash especially if you had a rock solid idea for that hundred bucks.

So when faced with choices again… would you rather take a refrigerator someone spent $100 to make and try to sell it for more than $1,000 or would you rather someone give you $100 cash and you do whatever you want to try to turn that into more than a thousand bucks? On the one hand you have a refrigerator which might have a decent retail market and on the other hand you have cold hard cash that you can do anything with to try and make the necessary profit. You might choose refrigerator but you might choose the cash especially if you had a rock solid idea for that hundred bucks.

If you’re an expert in your trade, you might be able to build your own higher-quality refrigerator for the same cost of $100 and be able to sell it for $2,000. Sure beats buying a crappy lower quality one and struggling to sell it for more than a thousand doesn’t it? Then you could pay the $1,000 owed and walk away with $1,000 in profit.

Sounds awesome except some states might deem the transaction illegal because to give a business $100 cash in exchange for $1,000 over a certain time period is usurious and predatory to the borrower. But selling a refrigerator valued at $100 to a business for $1,000 is okay, even if the business is never able to sell it.

In the eyes of a state, it is okay for a business to pay a 900% markup for an illiquid asset but it is dangerous to pay a 900% markup for the most liquid asset of all. I don’t understand it. If the idea is to prevent lenders from poaching borrowers or borrowers from making bad business decisions, then why is it okay for someone to sell a product for a lot more than they paid for it? Is a manufacturer selling a $100 refrigerator to a business for $1,000 usurious?

Perhaps your answer would be that a business owner wouldn’t engage in such a transaction if he/she didn’t believe it could be sold for more, either because there is an established retail market or because of sufficient market research. That is a weak defense because businesses get stuck with inventory they can’t sell all the time. Whether the market changed or it was just a bad business decision, Americans attitude towards speculation on a good or service is one of total acceptance. But give a man a dollar and he can’t be trusted to earn back more than a few cents on it. A legislator might evaluate these potential returns on a $1 investment like this:

Turn it into $1.05? sure!

Turn it into $1.15 maybe…

Turn it into $2.00? Let’s make laws to prevent people from thinking that way!

In many states, if you borrow a dollar so you can make three but it cost you a dollar in interest to make this happen, it’s illegal. But if you pay a dollar for an old banana peel with the hope of selling it for $3, that’s a business transaction.

I could rehash examples over and over, but where I’m going with this is that there are things like credit history and risk criteria that prevent people from borrowing a dollar at a relatively low rate. Naturally, the more risky the borrower, the higher the cost. After a certain level though, the law intervenes. If the amount of risk warrants a very high rate of interest, more than what is allowed by law, the government would rather the borrower get nothing than allow the transactions to go through. It’s a very sad position the government takes on its citizens, that the borrower is not capable of generating the return they believe or that that they lack the intelligence to know what they’re engaging in and therefore the transaction should be stopped altogether. In a utopian society, saving people from themselves might seem fair and just, but in reality there are millions of people and businesses with less than stellar credit, disqualifying them from borrowing at all because to compensate for risk would require a rate of interest disallowed by law.

At this time last year, 53% of Americans had credit scores of 700 or better. 700 is that magic threshold and it means that 47% of Americans are going to have a hard time obtaining credit or won’t be able to get it at all. When the laws were written to protect borrowers, I highly doubt the legislators understood they would be locking out almost half the country.

It’s ironic then that in times of financial crisis, government points the finger at banks for keeping credit tight, when it is nearly impossibly to free it up because of how regulated it is.

Credit has been screwy the last few years because government intervention is wreaking havoc on the market. The maximum allowable interest rate on an SBA 7(a) loan maturing in less than 7 years is the Prime Rate + 2.25%. That would be 5.5% annually. FICO states that the odds of a borrower becoming delinquent on their loan (90 days or more behind) range from 15% to 87% if their score is less than 700.

Credit has been screwy the last few years because government intervention is wreaking havoc on the market. The maximum allowable interest rate on an SBA 7(a) loan maturing in less than 7 years is the Prime Rate + 2.25%. That would be 5.5% annually. FICO states that the odds of a borrower becoming delinquent on their loan (90 days or more behind) range from 15% to 87% if their score is less than 700.

How can you expect to make money if you can only charge a maximum of 5.5% when 47% of all Americans have a 15 to 87% chance of going delinquent or defaulting? You can’t and that’s why the Small Business Administration exists. In order to manipulate banks into making wildly unprofitable loans to businesses, the Federal Government via the SBA guarantees up to 85% of the losses banks are stuck with. It’s a bandaid solution to the broken market that usury laws create.

The SBA also empowers banks to crush private sector competition since many non-bank financial institutions do not participate in the SBA program and therefore need to charge vastly higher rates to compensate for risk.

But even the SBA has strict criteria on default coverage. Many borrowers do not meet the SBA’s criteria, leaving the bank unable to lend to them.

It is no surprise then that the end result of continued credit market dysfunction has led to non-bank financial institutions getting creative. If you can’t loan a man a buck in return for two, then buy 2 bucks worth of his future success in exchange for a buck today. That was the original basis behind Merchant Cash Advance financing and the concept is rooted in factoring. Americans accept the buy/sell arrangement in business no matter how much risk each party is taking and so if we start treating cash as an asset, of which there is nothing more liquid, then we’ve finally cured the disconnect of money versus product/service.

For those with heavy debt, critics point fingers at the lenders, disregarding the cash the borrower got as a seemingly empty asset with no value that disappeared over night, a trick they’ll conclude was all part of the lender’s plan to saddle the borrower with evil debt and interest charges.

Somewhere along the line, a few people stopped thinking about how they could turn a dollar into two and started thinking how they could use the dollar to pay for something they already got while worrying about the dollar and interest owed on it at a later date. As this psychology has taken root in our culture, people have painfully learned that the ability to borrow runs out and the reality of owing a lot of money interferes with the comfort of living the way they did before. Lenders have taken losses and legislators have enacted laws to prevent people from hurting themselves. It all comes back full circle as we wonder now why banks aren’t lending and people can’t get credit.

There are many solutions, some temporary, some long-term, some will help a little, and some will help a lot. All of the debates, arguments, and finger pointing don’t change the fact that no matter how much progress we make, there are people out there that are wondering how they can borrow a dollar today to pay for something they already got. Businesses borrow to pay for past due rent, pay off inventory, taxes, payroll, and equipment. There are instances when a cash infusion is appropriate because the business will bounce back and there are instances when a loan will prop an insolvent business up for a short while, only for it to finally fail because the profitability or cash-flow problems were never fixed.

In America we all understand the trading of goods and services for money, but when money is traded for money, we get confused. If you are willing to pay $1,000 for a refrigerator it cost someone else $100 to make with the belief that you could resell it for $2,000, then there is no reason why the manufacturer shouldn’t be able to borrow $100 and go direct to the consumer themselves. The $900 interest fee is justified. Let’s not forget that a competing lender will charge less to try and steal the borrower away. The market will takeover until the perfect balance is met between risk and reward. When we legislate away this natural process we cause dysfunction, creating the needs for bandaids like government guarantees to force a market into existence while disrupting all of the other ones.

Undo the regulations and inspire the masses to turn a dollar into two, a hundred, or a thousand! The possibilities are endless with cash. If you can’t think of a way to turn a healthy profit with the most liquid asset on Earth, then chances are your luck won’t be much better with selling refrigerators or anything else.

– Merchant Processing Resource

https://debanked.com

MPR.mobi on iPhone, iPad, and Android