Business Lending

deBanked Nov/Dec Teaser

December 1, 2015The November/December issue of deBanked Magazine should go out in the mail at the end of this week. In the meantime, can you guess who is on the front cover of this issue?! Here’s your clue:

Jared Weitz, the CEO of United Capital Source, was on the cover of the previous September/October issue.

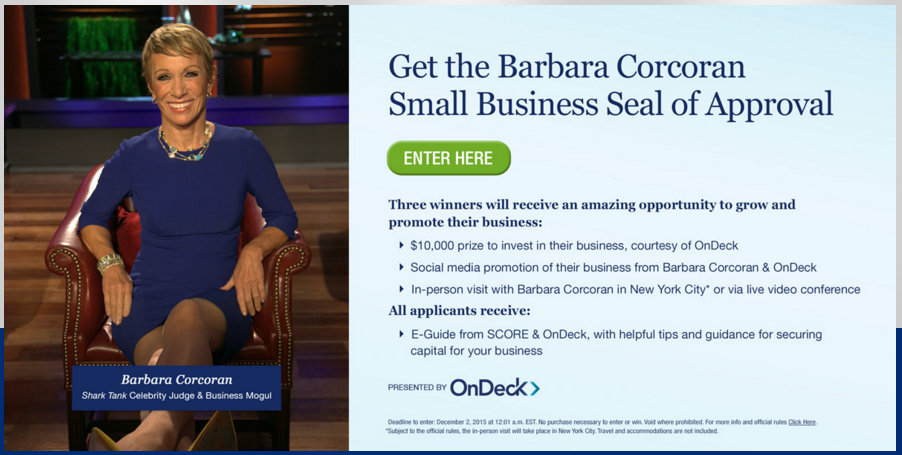

Shark Tank’s Barbara Corcoran Teams Up With OnDeck for Small Business Contest

November 29, 2015 Barbara Corcoran, co-founder of The Corcoran Group and famous Shark Tank investor, has teamed up with small business lender OnDeck to support entrepreneurs through a contest. Three winners will be chosen for a $10,000 prize and they’ll also get to meet Barbara Corcoran.

Barbara Corcoran, co-founder of The Corcoran Group and famous Shark Tank investor, has teamed up with small business lender OnDeck to support entrepreneurs through a contest. Three winners will be chosen for a $10,000 prize and they’ll also get to meet Barbara Corcoran.

Contest applicants are asked to enter what they would spend the $10,000 on to grow their business. The deadline to enter is December 2nd, 2015.

The partnership is significant because it marks yet another time that a Shark has crossed paths with online business lenders. Just one year ago, Kevin O’Leary became a spokesperson for IOU Financial.

I'm thrilled to announce a new partnership between O'Leary Financial & @IOUCentralInc this morning! http://t.co/ECJl1K5ZUC #smallbusiness

— Kevin O'Leary (@kevinolearytv) October 2, 2014

Also around that time, Kevin Harrington, an original Shark Tank investor before Mark Cuban or Lori Greiner, co-founded his own small business lending marketplace, Ventury Capital. Straight out of the OnDeck or merchant cash advance playbook, Ventury’s FAQ says their system “deducts a fixed, daily payment directly from your business bank account each business day.”

Watch Kevin Harrington explain his company here:

Of course there was the time that a merchant cash advance company (Total Merchant Resources) actually went on Shark Tank and pitched the sharks…

It seems that the show and the real world have a lot in common.

Will the Wild West of alternative lending stay that way?

November 24, 2015Comments on the regulatory future of alternative lending were included in a joint report prepared by Lendio and Dealstruck:

Blake hopes that governing agencies will offer reasonable policies that will encourage best-in-class business practices (to weed out the bad actors) without damaging the innovation and growth in the industry. Furthermore, Lendio highly recommends that any new or additional regulations come from the Federal level, rather than through a state-by-state patchwork of laws that will impose inconsistent and costly regulations on the online lenders.

– Brock Blake, Lendio CEO

Thoughtful regulation to ensure operators are performing with honesty and transparency is a good thing. And good players are stepping up to the plate to take a proactive stance regarding fair and transparent lending practices, executed ethically and with integrity. Fortunately for the small business lending market, the key lenders and marketplaces in the industry have used a blueprint of best practices that were established and implemented in the consumer lending space. It’s fascinating to think about how much room they have left to grow.

– Ethan Sentura, Dealstruck CEO

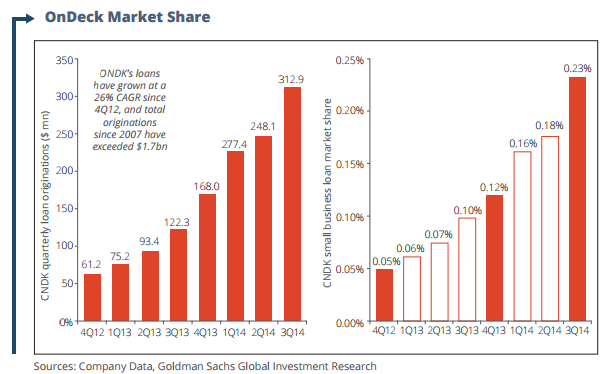

The report compiles other interesting pieces of data such as OnDeck’s share of the entire business loan market, which stood at less than a quarter of 1% just 1 year ago.

You can view Lendio and Dealstruck’s full report here.

What Makes a Good Loan Broker? Is it How Much You Fund?

November 18, 2015What Makes A Good Broker?

Through the plethora of recruiting ads by brokerages, funders and lenders, trying to draw people into the space through promises of lucrative paydays with minimal work, one has to stop and wonder, who are the actual good brokers? What do they look like, sound like, and dress like? How is their personality? How is their work ethic? How can you spot them in a crowd?

Through the plethora of recruiting ads by brokerages, funders and lenders, trying to draw people into the space through promises of lucrative paydays with minimal work, one has to stop and wonder, who are the actual good brokers? What do they look like, sound like, and dress like? How is their personality? How is their work ethic? How can you spot them in a crowd?

There are a number of things that make a good broker, a good broker, but for the sake of this discussion, I wanted to begin with expectations and measurements of funding volumes.

LIMITING THE MEASUREMENT

A broker can have a good month, a good quarter, and even a good year, so to truly judge the quality of a broker’s work, I believe you have to start the measurement over at least a 24 month time period. This would smooth out things that usually plague sales professionals such as down times, seasonal periods, stall periods, dry spells, artificial market boom and bust periods.

One won’t even be able to complete this measurement on most brokers entering the space, as most of them will be out of the industry within 3 – 6 months. I believe that success in our industry is mainly due to having leveraged resources that give you a competitive advantage, rather than actual superior “selling” capabilities. 20% of brokers will have these resources and 80% will not.

MEASUREMENT TIERS

From my research, these are the measuring tiers that can be utilized to gauge the quality of a broker over at least a 24 month time period. These numbers include both new and renewal funding volumes. With renewal merchants, even though you are dealing with the same client, they still require a new underwriting process with new offers being generated, thus requiring a new sales process or another “close.” As renewals are the lifeblood of our industry, many brokers have a plan in place to build a renewal portfolio and “sit back”, thus we shouldn’t only factor in new deals to this measurement.

- $300,000 plus a month in funding average: The Superstar Broker Level

- $150,000 to $250,000 a month in funding average: The Good Broker Level

- $75,000 to $125,000 a month in funding average: The Average Broker Level

- $25,000 to $50,000 a month in funding average: The Rookie Broker Level

If you have been a broker for at least 24 months, what is your current standing? If you are currently at the Rookie Agent level or the Average Agent level, what do you think you can do to get to the Good Agent level or the Superstar Agent level?

NOT ALL BROKERS ARE EQUAL IN TERMS OF OPERATIONAL STRUCTURE

These measurement tiers are only for individual brokers and not for total funding volumes completed by an entire office of brokers.

But also understand that other variables might be at play for an individual broker as well, such as the fact that he might be a sub-broker to a large brokerage house that feeds him warm leads all day, and his job is just to come in, sit down and focus only on the selling/closing part of the process. Or, he might be a part of a funder’s inside sales team and similar to the sub-broker, he gets warm leads fed to him all day to where he just needs to come in, sit down and focus only on selling/closing.

If you are currently in the sub-broker or inside sales team setup, it’s understandable if you are in The Superstar Broker level as you have more leveraged resources, less responsibilities and more time to dedicate solely to your selling/closing process.

But if you are operating as a One Man Show, like I was, then (in my opinion) it would mean a lot more to consistently perform at either The Superstar Broker level or The Good Broker level, considering all of the administrative/operational tasks that you solely have to juggle on your own.

MY ONE MAN SHOW PERFORMANCE

As my office currently goes through restructuring, during my time of selling the product from late November 2009 until September 2015 (70 months), I averaged $200,000 a month in new and renewal funding volume. This would place me at The Good Broker level.

There were surely months when I funded at The Superstar Broker level of over $300,000 with even some months getting at or near $1 million, but those were not my consistent averages throughout the 5 years and 10 months (70 months) that I sold the product. During the 70 month time period operating as a One Man Show, I had to juggle many administrative/operational aspects including but not limited to:

- Completing my own secondary and primary market research

- Designing my own business plan, ROI formulas, and completing my own trend analysis

- Coming up with innovative ways to creatively and profitably finance my office

- Building business related credit

- Setting up my funder network and keeping up on their underwriting criterion

- Setting up agreements with warm data suppliers and other vendors

- Designing and running my own website

- Setting up and managing my own direct and in-direct marketing campaigns

- Running through my daily calls to warm data (averaged about 150 a day)

- Managing and following up with my sales pipeline

- Managing and following up with my current deals in underwriting

- Managing and following up with my renewal portfolio

- Managing legal aspects such as contracts, LLC requirements, keeping up on marketing laws, etc.

- Managing accounting, insurance and tax related aspects

- Managing retirement account aspects

On the side, I built a merchant processing portfolio on track to process close to $200 million.

To top everything off, I also managed to complete four college degrees (MBA and three bachelor’s degrees) during this hectic and stressful time period as well.

YOU MIGHT HAVE BETTER OPERATIONAL LUXURIES THAN I DID

If you have the luxury of being a sub-broker or a part of an inside sales team, with having a team of people to do a good chunk of the administrative/operational tasks listed above (that I had to manage on my own), then as mentioned, you stand a great chance of getting to and staying in The Superstar Broker level of performance in terms of funding volumes.

You want to just bring to the table a solid work ethic and professional competency, always with the passion, desire and ability to learn. You also want to be very efficient in time management. I believe that time management is a “skill” that must be honed and managed. As the English brewer Charles Buxton said: “You will never find time for anything. If you want time, you must make it.”

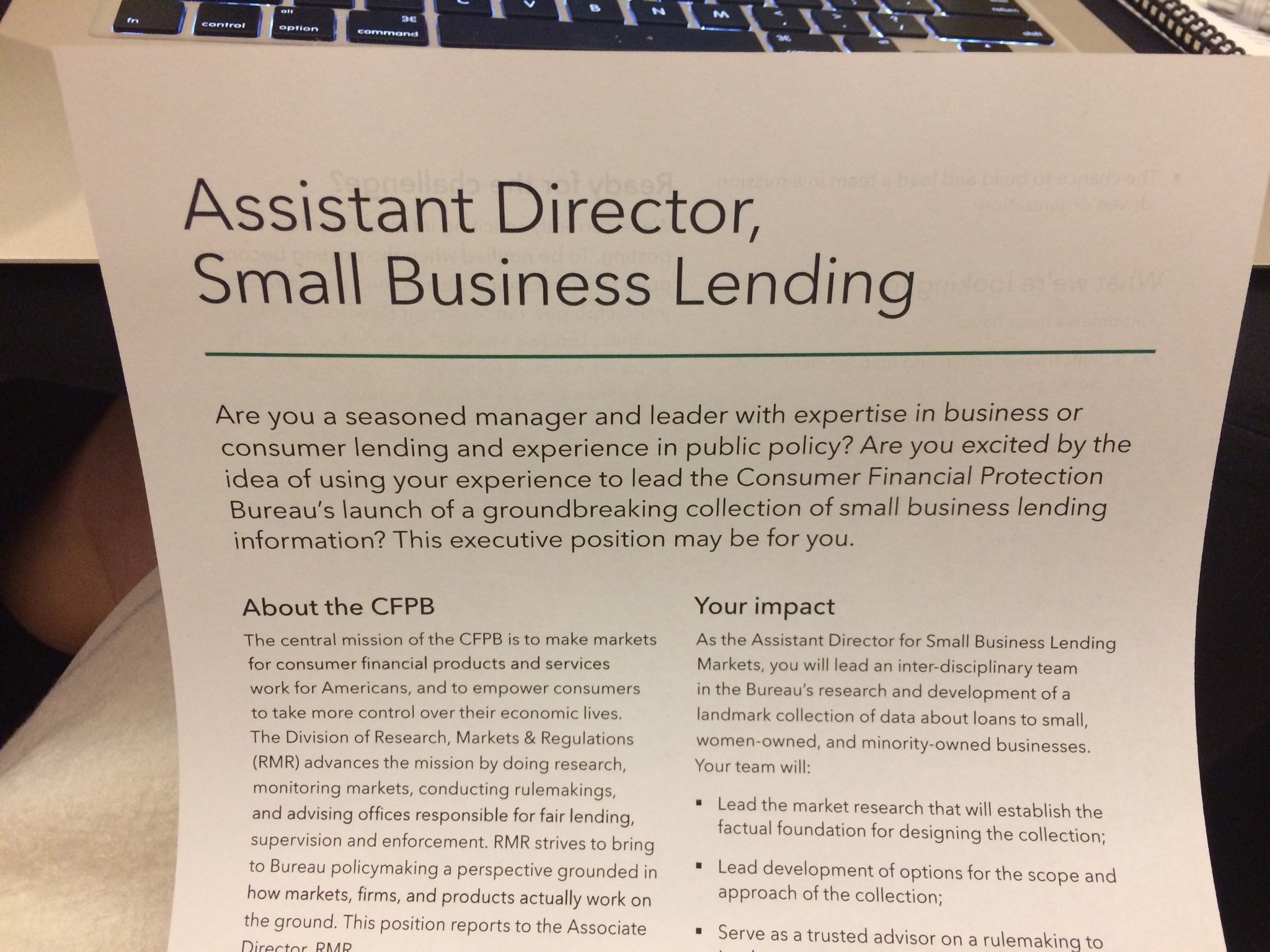

The Clock is Ticking: CFPB Blankets Small Business Banking Conference

November 17, 2015At the Small Business Banking conference in Nashville, the CFPB is making its presence known by peppering attendees with this handout:

While not surprising considering they have been advertising this position on LinkedIn, it shows a concerted effort to not only recruit, but also to subtly inform everyone that their involvement is just around the corner.

What is alarming is that the assistant director for small business lending is said to play a role in rulemaking. As you may not be aware, the CFPB has legislative power that can bypass Congress even though it’s part of the executive branch.

Would you like to play a proactive role to protect the industry, improve its reputation, and educate government policy makers? Now is the time to consider joining the Coalition for Responsible Business Finance.

Contact:

CRBF Executive Director Tom Sullivan

c/o Nelson Mullins Riley & Scarborough

101 Constitution Avenue, NW

Washington, DC 20001

(202) 905-2571

Learn more at: http://www.responsiblefinance.com/

Top Lawmakers Request Information About Online Small Business Lending

November 16, 2015 In the past two weeks, four ranking members of Congress have sent letters to the Treasury Department, SBA, SEC and CFPB requesting information about alternative small business lending. On November 3, Senators Jeff Merkley (D-OR), Sherrod Brown (D-OH) and Jeanne Shaheen (D-NH) sent a letter to the Treasury Department and the SBA requesting information about the impact of marketplace lending on small businesses. The Senators serve, respectively, as the ranking member of the Senate Subcommittee on Financial Institutions and Consumer Protection, the ranking member of the Senate Banking Committee, and the ranking member of the Senate Small Business Committee.

In the past two weeks, four ranking members of Congress have sent letters to the Treasury Department, SBA, SEC and CFPB requesting information about alternative small business lending. On November 3, Senators Jeff Merkley (D-OR), Sherrod Brown (D-OH) and Jeanne Shaheen (D-NH) sent a letter to the Treasury Department and the SBA requesting information about the impact of marketplace lending on small businesses. The Senators serve, respectively, as the ranking member of the Senate Subcommittee on Financial Institutions and Consumer Protection, the ranking member of the Senate Banking Committee, and the ranking member of the Senate Small Business Committee.

In their letter, the Senators cited concerns of some observers about the regulatory framework governing the space:

Observers have questioned what the appropriate role of federal regulators should be in supervising non-bank companies providing small business capital. Government agencies such as the federal financial regulators, Small Business Administration (SBA), or the Federal Trade Commission may have a role to play, as well as state regulators. However, it is possible that ‘the current online marketplace for small business loans falls between the cracks for Federal regulators.’ As we saw during the crisis, financial markets that fall between the cracks may result in predatory lending, consumer abuse, or systemic issues.

And last Thursday, Nydia Velazquez (D-NY), ranking member on the House Committee on Small Business, sent a letter to the SEC and CFPB inquiring about small business lending marketplaces. Rep. Velazquez cited a 2011 GAO report discussing early developments in P2P lending. Rep. Velazquez noted that in the report the GAO had proposed two approaches for federal regulation of online lending: one SEC-centered and the other CFPB-centered. Rep. Velazquez requested the agencies to provide her with more information concerning their regulation of online lending marketplaces for small business borrowers.

The lawmakers also posed a number of specific questions to the agencies, such as:

- What are the most significant risks in the market?

- What authority exists for federal agencies to supervise and examine companies offering online small business loans?

- What impact is the market having on community banks?

- How do online business lenders fit in the broader financial regulatory framework?

- What disclosures are required in small business lending?

- What resources have your agencies devoted to the regulation of the online lending marketplaces?

- Do you believe that your agencies possess the necessary legal authorities to protect small business borrowers and retail investors as it relates to the online lending marketplace?

And most interesting:

8. What statutory changes, additional legal authorities, and resources are necessary to support your agencies’ role in the regulation of online lending as it relates to small business loans and extensions of credit?

The recent congressional interest is likely a result of the RFI issued by the Treasury Department regarding marketplace lending. It seems Capitol Hill is also interested in learning more about the topic and, specifically, how alternative small business finance products are currently being regulated.

CFPB Signals Alarming Interest in Small Business Lending

November 10, 2015 The Consumer Financial Protection Bureau posted an alarming job opportunity on LinkedIn last month for the position of Assistant Director for Small Business Lending Markets. Ominously self-labeled as an “Expression of Interest” rather than a job opening since the job is not currently open to applications yet, the CFPB has inadvertently revealed its own expression of interest in small business lending.

The Consumer Financial Protection Bureau posted an alarming job opportunity on LinkedIn last month for the position of Assistant Director for Small Business Lending Markets. Ominously self-labeled as an “Expression of Interest” rather than a job opening since the job is not currently open to applications yet, the CFPB has inadvertently revealed its own expression of interest in small business lending.

If there was any doubt that data collection required under Section 1071 of Dodd Frank was never going to happen, the CFPB also revealed that there will not only be a person responsible for small business lending, but in fact an entire team. And they won’t just be collecting data, but they’ll be monitoring it, analyzing it, interpreting it, and advising on rulemaking, according to the listing.

Candidates are being offered a once-in-a-career opportunity to make the market for small business finance fairer and more transparent.

So much for just collecting data, the CFPB apparently plans to directly insert itself into the fairness of transactions conducted between commercial entities.

Perhaps, we are not too far off from a world like this:

Check out my thoughts about the troubling narrative developing around small businesses in the Sept/Oct magazine issue of deBanked.

Mike Cagney vs. Todd Baker: The Debate at the Marketplace Lending and Investing Conference

November 6, 2015 “You’re big buyers of some of this paper until you’re not,” said Todd Baker, the managing principal of Broadmoor Consulting, LLC, to a crowd of institutional investors and bankers at the Marketplace Lending and Investing Conference in New York. Seated to his right was his debate adversary, SoFi CEO Mike Cagney, who offered many opposing viewpoints. You can’t choose to not run a business because you fear it could some day shut down, Cagney argued.

“You’re big buyers of some of this paper until you’re not,” said Todd Baker, the managing principal of Broadmoor Consulting, LLC, to a crowd of institutional investors and bankers at the Marketplace Lending and Investing Conference in New York. Seated to his right was his debate adversary, SoFi CEO Mike Cagney, who offered many opposing viewpoints. You can’t choose to not run a business because you fear it could some day shut down, Cagney argued.

The two opponents had battled before though Op-eds published in American Banker. “The hard truth is this: while MPLs [Marketplace Lenders] have introduced valuable innovation into financial services, they carry a fundamental flaw that threatens to undermine their business, destabilize financial markets and cause real economic hardship,” wrote Baker back on August 17th. The flaw he addressed is access to funding. Baker argued that if investors don’t want to buy loans, then the marketplace lender is dead because their existence relies on the transaction fees from loan originations.

Cagney responded directly two days later. “The scenario [Baker] describes can’t happen. It is true that an MPL needs a buyer to originate loans — without one, the marketplace needs to raise rates until a buyer emerges. If there is no buyer, MPLs simply stop lending — they won’t start originating underwater loans.”

That perhaps played partly to Baker’s argument because if indeed there was an absence of buyers then the marketplace lender stops originating loans… and would at least temporarily be dead or would at least not be generating revenue.

But during the live debate, Cagney cast the suggestion of there being no buyers aside. Companies like his are targeting large market segments, where there will theoretically always be demand at some price, not niche market segments that could dry up in a crisis. “The beauty of marketplace lending is we’re balance sheet light,” Cagney told the crowd while pointing out that banks get into trouble with lending because of how leveraged they are.

But during the live debate, Cagney cast the suggestion of there being no buyers aside. Companies like his are targeting large market segments, where there will theoretically always be demand at some price, not niche market segments that could dry up in a crisis. “The beauty of marketplace lending is we’re balance sheet light,” Cagney told the crowd while pointing out that banks get into trouble with lending because of how leveraged they are.

That viewpoint contrasted that of two Goldman Sachs VPs that told the same crowd earlier that marketplace lenders would eventually move towards keeping loans on their balance sheets.

SoFi is of course an exception to the mold of the average marketplace lender, which Baker made sure to point out. Most people in the room were aware of SoFi’s $4 billion private market valuation. It’s clear that Cagney knows what he’s doing, Baker said out of respect several times on stage. His comments were directed less at SoFi and more on marketplace lenders in general.

Baker worried that these loans were being classified as fixed income investments too soon. These loans are not backed by large corporations, he warned, but by consumers. They won’t act like fixed income investments forever, he said.

Cagney took the criticism in stride and basically chided Baker and those that share his concerns as being unwilling to pursue opportunities because they are simply afraid of change.

Someone knows where I am at all times, he jokingly warned the audience of bankers, in case any of them had planned to kidnap him and put an end to his disruptive endeavors.

SoFi’s brand is of being an anti-bank or a fixer of the broken banking system so Cagney no doubt expected doubters at a conference produced by American Banker’s parent company.

Baker told Cagney that he had a nice libertarian view that didn’t make sense over in the real world. Cagney gleefully accepted the label of libertarian and rejected the notion that the real world and the libertarian world weren’t one and the same.

The two agreed to cordially disagree and notably did not shake hands when the debate ended. Cagney, the anti-banker, appeared to win over a significant portion of the audience. To his credit, the conference was aptly named the Marketplace Lending and Investing conference, not the Traditional Banking Forever conference.

Both sides made valid arguments, but one thing is for certain, banking will never be the same.