Business Lending

Small Biz Feel Better About Economy But Still Won’t Borrow

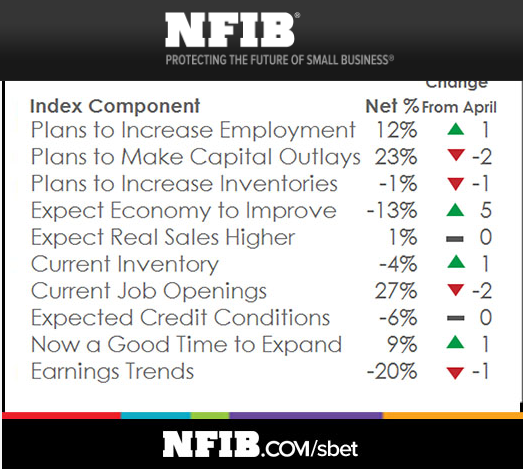

June 14, 2016The nation’s small businesses are cautiously optimistic about the economy and the National Federation of Independent Business’s Index of Business Optimism testified showing a marginal rise in May.

While merchants are still nervous about sales and remain hesitant to make big capital expenditures or stock inventory, they are still looking to expand, hire more and generally expect the economy to improve.

But much to lenders’ displeasure, 31 percent reported that their credit needs were met and 52 percent said they didn’t plan on getting a loan as businesses controlled spending on capital goods. The percent of owners planning to spend on capital fell 2 points to 23 percent and the average rate paid on short term maturity loans fell by 40 basis points to 5.3 percent.

The index survey that 700 business owners participated in, rose a negligible 0.2 points to the previous reading of 93.8 last month.

While 56 percent of the respondents said they were planning to ramp up hiring, 48 percent reported a talent crunch for the positions they were trying to fill. Thirteen percent of owners cited the difficulty of finding qualified workers as their most important business problem.

Weak sales were also among the top concerns for small businesses in the country for 14 percent of the respondents, which hurt inventory and capital expenditure. The number of owners wanting to stock up on inventory was low. “These weak inventory investment readings are consistent with the rather poor performance of consumer spending in the first quarter, leaving owners with excessive stocks and no incentive to add to them,” the report said.

Industry Goes Par for the Course

June 13, 2016Two companies in the industry are sponsoring golfers in this year’s U.S. Open, Mike Van Sickle via Expansion Capital Group (ECG) and Billy Horschel via Lenders Marketing.

Back in February, ECG SVP Steve Beveridge said, “we are excited to announce our partnership with Mike as a member of the ECG team. His motivation, drive, and dedication represent the same core values that ECG admires in our business clients who are pursuing their own individual dreams.” (Below: Van Sickle in an Expansion Capital Group shirt)

Van Sickle is ranked 1,297th in the world.

Horschel by contrast is ranked 55th in the world. Lenders Marketing, a lead generation company, also sponsored Michael McCabe last year during the PGA Tour Barracuda Championship in Reno, Nevada. (Below: McCabe in the green hat and Justin Benton of Lenders Marketing behind him to the left with the glasses over a white hat)

As Its Peer Winds Down, Able Lending Commits $5 million to Dallas Companies

June 13, 2016Small business lender Able Lending will pump in $5 million to fund companies in the Dallas-Forth Worth area in the wake of its peer running out of business.

Able calls itself “lowest cost non-bank lender” to small businesses and lends up to $1 million to businesses at any stage. Able offers better rates to entrepreneurs who raise funds from Backers – or family, friends and “fans” who fund as much as 10 percent of most Able loans. The company claims that its borrowers save $31,000 on loans between $25,000 and $1 million.

“DFW is an important market for Able. Our $5 million-dollar commitment to DFW solidifies that Able is ready to fund more deserving small businesses,” said Evan Baehr, president and cofounder of Able which began in Dallas last year to fund nearly $2 million to companies in the area.

Last week (June 5th), personal lender Vouch Financial which follows a similar family-and-friend strategy announced that it was shutting down. The three year old firm based out of San Francisco made personal loans based on what it called a ‘vouching network’ or sponsors, which secures the loan.

The Wall Street Journal reported that Vouch’s investors decided to stop backing the firm as demand for loans retreated as it struggled to compete with bigger rivals.

New Funder Doing 12-Month Deals With Weekly Payments (Guess Who)

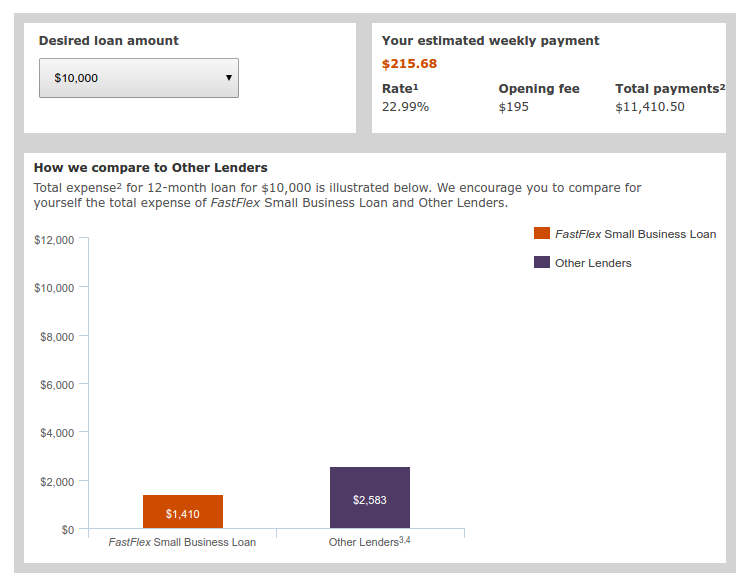

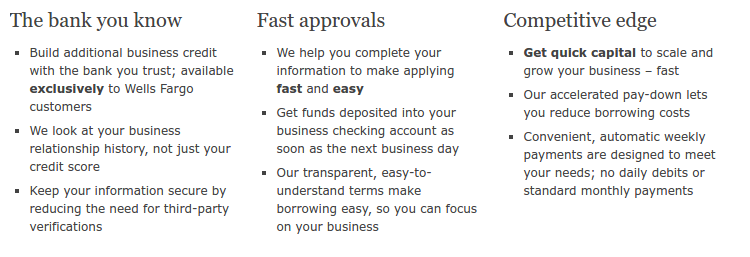

June 3, 2016 Merchants doing at least $4,100 a month in gross deposits are eligible for funding on a 12-month term with weekly ACH debit payments, a new funder revealed. Interest rates start as low as 13.99% but the max funding size is only $35,000. Underwriting decisions can be made instantly online with funds available the next day. “We consider your existing business checking history — not just your credit score,” they advertise.

Merchants doing at least $4,100 a month in gross deposits are eligible for funding on a 12-month term with weekly ACH debit payments, a new funder revealed. Interest rates start as low as 13.99% but the max funding size is only $35,000. Underwriting decisions can be made instantly online with funds available the next day. “We consider your existing business checking history — not just your credit score,” they advertise.

The name of the funder? Wells Fargo Bank.

The caveat is that applicants must have banked with Wells Fargo for at least 1 year to be eligible. The upside is that little documentation is required to apply outside of the application. The loan is unsecured and the closing fee is only $195. Dubbed FastFlex, the product is clearly meant to compete against online business lenders because well, they mention CAN Capital, OnDeck, and Kabbage in the footnotes on their loan calculator page.

Using their loan calculator, Wells Fargo estimated a 10k loan on a 1.14 over twelve months with weekly ACH payments.

Wells Fargo’s marketing message sounds awfully familiar:

Next day funding, not just your credit score, weekly payments…

Wells Fargo is not alone in their attempts to attack online lenders. Discover Bank for example, is targeting Lending Club directly. By going after the same borrower profile and offering better terms, Discover hopes to cut into Lending Club’s newfound market share.

Unsurprisingly, it is the non-bank prime lenders that will feel the growing bank threat the most. Companies offering small business loans or merchant cash advances to small businesses with damaged credit or complex situations are unlikely to find their target customer pool become bankable any time soon.

Fora Financial Secures $53 Million Credit Facility

May 19, 2016

New York-based small business lender Fora Financial closed a $52.5 million senior revolving credit facility with a group of financial institutions led by AloStar Capital Finance that includes BankUnited, Customer’s Bank and First Tennessee Bank.

This credit facility will take care of Fora’s financing for the next three years and allow for expansion of the facility to $75 million, tripling the lender’s current borrowing capacity. The eight year old company has financed $450 million to 9,500 businesses to date.

“This facility will provide us with flexible, low-cost financing that will enable us to continue on our growth trajectory while offering even more attractive and innovative solutions to thousands of small businesses in need of capital,” said Andrew Gutman, Chief Financial Officer at Fora Financial.

In October of last year, founders Jared Feldman and Dan Smith sold a major stake to PE firm Palladium Equity Partners LLC which helped capitalize their balance sheet. The Palladium deal marked a milestone in the development of Fora Financial, a company with roots that date back to when Smith and Feldman met while studying business management at Indiana University.

In a first, Bizfi crosses $144 million in Q1 funding

May 17, 2016

Thanks to the partnership with Western Independent Bank, Bizfi had a record Q1 to date with $144 milion in loan originations.

The New York-based fintech company funded 3,605 small businesses, a 49 percent increase from $96 million funded in Q1 last year, Bizfi said.

The partnership with Western Independent Bank in March this year opened up several markets in the midwest and west coast Alaska, Arizona, California, Colorado, Hawaii, Idaho, Montana, Nevada New Mexico, Oregon, Utah, Washington and Wyoming can benefit from this partnership. Referring to the partnership, Bizfi founder Stephen Sheinbaum said, “These types of relationships not only help to fuel Bizfi’s growth, they ensure the financial partner continues to maintain their customer relationships by providing their clients an alternative for the financing they need,”. “In 2016, we’re looking forward to further expanding our product set and partnering with more traditional financiers, enabling us to fund the growth of even more of America’s small businesses.”

Bizfi’s marketplace partners with lenders like OnDeck, Funding Circle and Kabbage and the company has so far funded 29,000 small businesses with $1.6 billion in capital since 2005.

The Direct “Lender” Test – For ISOs/Brokers

May 16, 2016

ISOs/Brokers: Unsure if the company you’re speaking with is a direct lender? There’s a few ways to immediately spot a faker. Fakers are often confused between loan products and sales of future receivables, an issue that will likely open them up to all kinds of legal liabilities. For this reason alone, you don’t want to end up working with the wrong company. In some states brokering a deal to an unlicensed lender could have severe consequences.

First, if anyone tells you they are a direct lender, a popular phrase these days, ask them how it is they lend. Do they comply with lending laws on a state-by-state basis or do they have a bank charter relationship? If a bank charter, ask them what bank. Verify it. If they have a lending license in a single state or multiple states, verify it. You can look up licensed California lenders here for example.

If they don’t know what you are talking about when you ask about chartered banks or state licensing, you should end the conversation.

If they’re supposedly only in the business of purchasing future revenues or receivables but call themselves a direct “lender,” you should run away as fast as you can. If a company buying future receivables believes they are indeed a lender, they and anyone working with them could face all sorts of penalties, up to and possibly including criminal charges. No amount of commission is worth this.

If a company is only in the business of buying future receivables (what some would call a true or traditional merchant cash advance), a more proper title would be a direct “funder.”

Keep in mind that a lender reliant on a bank charter relationship technically would not qualify as being a “direct lender” either since the bank itself would be the lender.

The differences between loans and sales will be taught in the industry’s upcoming online certification course. I highly recommend that newcomers sign up for it.

Expansion Capital Group Joins The $100 Million Club

May 13, 2016 Expansion Capital Group has officially lent its one hundred millionth dollar since inception. In an e-mail, the Sioux Falls, South Dakota-based lender said they’re proud of the small businesses they’ve helped along the way. And they’re helping them at increasing speed, records indicate. The company celebrated its $50 million milestone less than 9 months ago, which means they’re lending more than $50 million a year.

Expansion Capital Group has officially lent its one hundred millionth dollar since inception. In an e-mail, the Sioux Falls, South Dakota-based lender said they’re proud of the small businesses they’ve helped along the way. And they’re helping them at increasing speed, records indicate. The company celebrated its $50 million milestone less than 9 months ago, which means they’re lending more than $50 million a year.

In November, the company announced the closing of a $25 Million credit facility through Northlight Financial and Bastion Management to support their rapid growth.