Sean Murray is the President and Chief Editor of deBanked and the founder of the Broker Fair Conference. Connect with me on LinkedIn or follow me on twitter. You can view all future deBanked events here.

Articles by Sean Murray

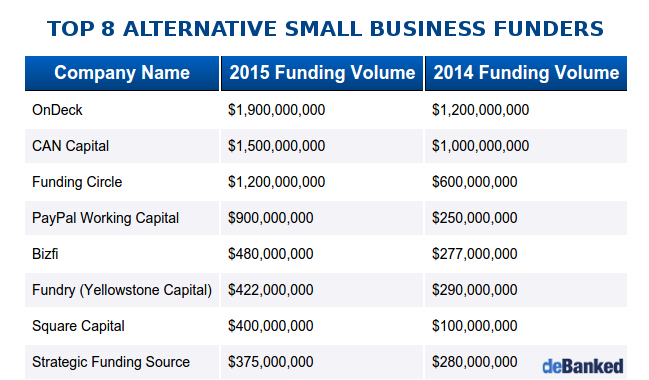

The Top 8 Small Business Funders

March 13, 2016Whether they do loans or merchant cash advances, here are the top 8 alternative small business funders:

This list originally appeared in a story about Square’s Q4 Earnings and has been republished individually here in case anyone missed it. The figures were either disclosed to deBanked directly or are a best estimate based on publicly available materials. This list is not comprehensive and in instances where no reliable data could be obtained, the company was just omitted. A larger list will appear in deBanked’s March/April Magazine issue so make sure you subscribe if you haven’t already.

Bank Strikes Back Against Online Lenders – Offers 5 Minute Business Loans

March 12, 2016Online lenders have new competition, a 198-year-old bank based in Boston, Eastern Bank. Worried that technology would leave them in the dust, Eastern has invested millions in an application and underwriting system that can fund merchants up to $100,000 in 5 minutes. “The 55 requests for information on the old form have been replaced by eight,” according to the WSJ.

Rates range from 6.99% to 9.99% and it’s only available to existing customers. However a new customer only need open a checking account to become immediately eligible for it. One out of the 36 original borrowers on this program has already become delinquent on their loan, a statistic mostly within their expectations, the WSJ reports.

Eastern makes no mention of their speedy capabilities on their website, which still has the old paper application available for download.

Notably, former NFL player Doug Flutie, Eastern Bank’s spokesman for over 10 years, is scheduled to appear on the upcoming season of Dancing With the Stars.

“Me, Too” Lenders Something to Worry About, Says Former OnDeck Investor

March 11, 2016 Lending Club, SoFi and OnDeck will endure, wrote Matt Harris, a former OnDeck board member and investor, and current Managing Director for Bain Capital Ventures. In a blog post that approached 4,000 words, Harris admits that he has not invested in a single lender since OnDeck.

Lending Club, SoFi and OnDeck will endure, wrote Matt Harris, a former OnDeck board member and investor, and current Managing Director for Bain Capital Ventures. In a blog post that approached 4,000 words, Harris admits that he has not invested in a single lender since OnDeck.

“It is still possible, though I believe increasingly unlikely, that marketplace lending will be a durable innovation,” he wrote. He bases that on the assumption that origination platforms with no skin in the game are not sustainable over the long term and that what really made companies like Lending Club special is that it has “scale, a brand in the capital markets for producing high quality assets, and an unbelievable management team.”

All of the other perceived advantages don’t make sense, he argues. The average cost of funds for a bank “is 0.06%, assuming they fund their loans using deposits. OnDeck’s funding costs for its assets averages 5.3%. Lending Club has paid a median return to its asset purchasers of 7.4%.” Banks have lower operating costs as well. “I’ll point out that most of the bank expenses they highlight are fixed expenses like branches and compliance, which makes that expense burden irrelevant to the profitability of the marginal loan,” he wrote.

Even on technology, Harris says banks spend less, and on big data credit scoring, he says a lot of the factors marketplace lenders might find useful in predicting performance cannot be used legally because they end up correlating with a protected class such as race, whether it’s directly or indirectly.

“Things are going to get harder before they get easier,” Harris wrote, though he thinks companies like OnDeck and Lending Club are positioned to last. Everyone else who copied their model is in shaky territory. And yet through it all, he is optimistic. “For the first time in a decade, I’m feeling like it’s a great time to be starting a lending company,” he said.

Square’s Merchant Cash Advance Program Now Among Biggest in the World

March 10, 2016Square originated more than $400 million worth of merchant cash advances advances in 2015, according to their Q4 earnings report. Their average deal size was just shy of $6,000. The result is a 300% increase year-over-year and makes them one of the largest players in that industry worldwide.

RANKINGS

| Company Name | 2015 Funding Volume | 2014 Funding Volume |

| OnDeck | $1,900,000,000 | $1,200,000,000 |

| CAN Capital | $1,500,000,000 | $1,000,000,000 |

| Funding Circle | $1,200,000,000 | $600,000,000 |

| PayPal Working Capital | $900,000,000 | $250,000,000 |

| Bizfi | $480,000,000 | $277,000,000 |

| Fundry (Yellowstone Capital) | $422,000,000 | $290,000,000 |

| Square Capital | $400,000,000 | $100,000,000 |

| Strategic Funding Source | $375,000,000 | $280,000,000 |

A much longer list will be available in deBanked’s March/April 2016 Magazine Issue. SUBSCRIBE FREE to make sure you obtain a copy.

Marketplace Lending Investors: Enjoy Redlining While it Lasts

March 9, 2016 For investors, geographic discrimination in marketplace lending is not only a possibility, it’s a privilege and a joy

For investors, geographic discrimination in marketplace lending is not only a possibility, it’s a privilege and a joy

Two years ago, LendingMemo’s Simon Cunningham openly boasted about his exclusion of Florida borrowers from his marketplace lending strategy. In, The Joy of Redlining: Why I Never Lend Money to Florida, Cunningham wrote “folks from Florida are less likely, in a statistically significant way, to pay back their p2p loans. So I have never loaned a dollar to people in Florida, and have gone on to earn a higher net return on my peer to peer investment than 90% of p2p lenders.”

And he could openly say that because so long as the lenders are the ones making the loans, it’s within his right to buy pieces of the ones he wants in a secondary market. If Lending Club themselves were to underwrite that way however, well then they could potentially be accused of discriminatory redlining.

Lending Club used to offer rather precise geographic data to investors such as the actual city of the borrower, but that has since changed to only include the first 3 digits of the zip code. Racial and gender identity are obviously not disclosed.

NSR Invest, a marketplace lending investment-advisory firm, told the WSJ that about about 16% of people who buy loans from online marketplaces use a borrower’s state to make lending decisions. Some investors however are simply ignoring states like Vermont, New York and Connecticut because of a peculiar court ruling with jurisdiction over those three states.

Investors might not be able to redline forever, its foretold. According to the WSJ, the CFPB is reviewing this practice. “The agency said it aims to ensure that companies aren’t incorporating potentially discriminatory factors into marketing or underwriting.” Jo Ann Barefoot, a former advisor to the CFPB, said that “it may be unclear whether the investors in marketplace loans would have liability,” adding that the practice is in the regulatory gray space.

—

Full disclosure: I currently exclude borrowers from 11 states in my marketplace lending strategy, including Florida.

SoFi Starts Hedge Fund – And It’s Weird

March 8, 2016 With investor interest waning, SoFi’s solution to sell more loans is to launch their own hedge fund to buy them. Are they hypocrites?

With investor interest waning, SoFi’s solution to sell more loans is to launch their own hedge fund to buy them. Are they hypocrites?

Why stop at a dating app when you could also launch a hedge fund?

According to the WSJ, SoFi needs to be able to sell more loans so that they can continue to grow, but investors just aren’t buying them fast enough. A new hedge fund launched last month solely for the purpose of solving this problem has already raised $15 million. It has “a real chance to solve the balance-sheet problems facing the industry,” said SoFi CEO Mike Cagney to the WSJ. Called the SoFi Credit Opportunities Fund, Cagney believes it could grow to manage $1 billion and be used to buy loans from other lenders, not just SoFi.

News of the hedge fund arrives on the heels of a leaked rumor that the company was exploring the formation of a REIT to keep up with its burgeoning mortgage business, which it also does alongside student lending. Just a few months ago, SoFi was reportedly originating more than $50 million a month in mortgages.

Cagney’s choice of words in the WSJ interview seem to depart with his previously held beliefs on the capital markets. “In normal environments, we wouldn’t have brought a deal into the market, but we have to lend. This is the problem with our space,” he said. Emphasis mine.

In Cagney’s August 2015 Op-ed for American Banker, he said “The beauty of marketplaces is real-time information feedback. If there are too many buyers, the loan rates are too high. If there aren’t enough, they are too low.”

In practice, SoFi’s reaction to there not being enough buyers has been to start their own hedge fund to continue originating loans at a fever pitch. Absent a buyer, they’ll simply become their own buyer.

“If there is no buyer, MPLs simply stop lending — they won’t start originating underwater loans,” Cagney wrote back then.

Broadmoor Consulting’s Managing Principal Todd Baker warned of this exact scenario, ironically in an Op-ed battle with Mike Cagney. “An MPL has to keep issuing loans to survive. It can’t slow down lending and slash operating costs to stay afloat while collecting cash from existing loans, like a traditional finance company, because it doesn’t own any loans,” he wrote.

And although SoFi’s survival is not currently at stake, SoFi is indeed not slowing down.

Cagney and Baker actually faced off in person last November at the Marketplace Lending and Investing Conference in NYC. There, Cagney told the crowd that “the beauty of marketplace lending is we’re balance sheet light.” But just a few months later, he’s claiming the industry has “balance-sheet problems,” as in there’s not enough money floating around to buy the loans they want to generate regardless of demand.

Cagney and Baker actually faced off in person last November at the Marketplace Lending and Investing Conference in NYC. There, Cagney told the crowd that “the beauty of marketplace lending is we’re balance sheet light.” But just a few months later, he’s claiming the industry has “balance-sheet problems,” as in there’s not enough money floating around to buy the loans they want to generate regardless of demand.

Slowing down growth is apparently not a path that SoFi is looking to take. More loans originated means more fee income, and that’s ultimately the conflict of interest that Baker had pointed out.

Brendan Ross, who heads up a similar hedge fund that buys only business loans, expressed concern over the existence of an institutional buyer in the market that is connected to the seller. “You wouldn’t want to have SoFi advisers cherry-picking the best loans,” Ross said to the WSJ.

One thing is certain. SoFi’s “We’re Not a Bank” slogan says what they’re not, but these days it’s becoming harder to tell what exactly they ARE.

Yellowstone Capital Welcomed to New Office Location By City Mayor

March 8, 2016 It’s a change of scenery, insiders at Fundry subsidiary Yellowstone Capital say about their new office.

It’s a change of scenery, insiders at Fundry subsidiary Yellowstone Capital say about their new office.

The company has officially relocated from 160 Pearl Street in Manhattan to 1 Evertrust Plaza in Jersey City. On their first day in the new location, Jersey City Mayor Steven Fulop made an appearance and posed for a photo with company executives Isaac Stern and Jeff Reece to celebrate their arrival. Aside from outgrowing the NYC office that they operated from for years, Yellowstone was wooed to the State by the New Jersey Economic Development Authority to create jobs in the area in exchange for a tax incentive. The hundreds of employees they bring with them to the neighborhood now will also serve to stimulate Jersey City’s burgeoning economy.

The company originated close to half a billion dollars in funding for small businesses in 2015.

Just one stop from the Path Train’s World Trade Center station, Yellowstone’s new office environment makes it feel as if the company has been transported a million miles away. deBanked was given a tour of the new space, which at 25,000 square feet, was easy to get lost in. One employee said the upgrade from their previous location felt so immense, that it felt like they had moved to Japan.

Just one stop from the Path Train’s World Trade Center station, Yellowstone’s new office environment makes it feel as if the company has been transported a million miles away. deBanked was given a tour of the new space, which at 25,000 square feet, was easy to get lost in. One employee said the upgrade from their previous location felt so immense, that it felt like they had moved to Japan.

A clear view of NYC’s Freedom Tower from many of the floor’s windows assures them that they are not that far.

Cost of Online Lenders Takes Back Seat to Cost of Government Regulations

March 8, 2016 Study indicates that regulation and taxes are the chief problems, not borrowing costs.

Study indicates that regulation and taxes are the chief problems, not borrowing costs.

Small businesses are being smothered in the age of marketplace lending… by the government. According to the National Small Business Association’s (NSBA) most recent year-end annual report, regulatory burdens and federal taxes ranked among the most significant challenges to business survival.

The NSBA is a non-partisan small business organization with 65,000 members. In the survey they used to prepare their report, 33% of respondents said regulatory burdens were one of the most significant challenges to their future growth and survival. 24% cited federal taxes. The cost of health insurance benefits beat both of those with 36% of respondents choosing it.

Only 3% of those surveyed reported using an online lender or non-bank lender within the last 12 months. 43% used a bank loan, half of which came from a large bank. In another study, dissatisfied borrowers were slightly more likely to have transparency problems with big banks than online lenders.

Regulators might want to take notice of these statistics when considering future regulations for the commercial side of the marketplace lending industry. That’s because the cost of complying with any such regulations would likely increase the cost to borrowers, not reduce it.

Such was the case with Dodd-Frank and its impact on community banks. Speaking on behalf of the Independent Community Bankers of America last fall during a House Committee hearing, B. Doyle Mitchell Jr., the CEO of Industrial Bank, said that “Dodd Frank has only increased our costs.”

For bank loans in particular, 11% of respondents to the NSBA study that had taken a bank loan within the past 12 months said that the terms have become less favorable to their business. Only 4% reported the terms becoming more favorable.

When it came to the number one issue that small businesses believe that Congress and President Obama should address first, 15% said simplify the tax system, 9% said reduce the tax burden, 9% said rein-in the cost of health care reform, 8% said reduce the regulatory burden on businesses, and only 5% said increase small business access to capital.

Regulators mulling more regulation might want to consider what their constituents are actually saying, and that’s to roll back regulations, not come up with new ones. Online lenders might be expensive, but when asked what’s challenging their growth and survival, they barely even register, if they even register at all.

In a recent story by The Atlanta Journal-Constitution, Holly Wade, a representative of the National Federation of Independent Business, said “Our fear is that they will over-regulate [online lenders] out of existence or to the point that it’s no longer a benefit.”