Sean Murray is the President and Chief Editor of deBanked and the founder of the Broker Fair Conference. Connect with me on LinkedIn or follow me on twitter. You can view all future deBanked events here.

Articles by Sean Murray

Will Marketplace Lending Revert Back to Peer-to-Peer Lending?

March 28, 2016 Institutional investors wanted higher yields on Prosper’s latest bond offering, an entire five percentage points higher, according to the WSJ. This wasn’t necessarily brought on by performance either. Instead the once voracious appetite for all things online lending is being tempered by uncertainty.

Institutional investors wanted higher yields on Prosper’s latest bond offering, an entire five percentage points higher, according to the WSJ. This wasn’t necessarily brought on by performance either. Instead the once voracious appetite for all things online lending is being tempered by uncertainty.

Bain Capital Ventures partner Matt Harris told the WSJ that online lenders will need to replace the easy hedge fund money by “longer-term capital.” Normally, that would include traditional bank lines and credit facilities, but moving that direction could irreversibly sever the ties with their peer-to-peer roots and image.

Peer-to-peer (p2p) lenders embraced Wall Street’s easy money to scale, rationalizing to the peers on which they were founded that this was all necessary to change the status quo. The road to the sharing economy utopia required hobnobbing with the very institutions they were set on disrupting, they said. The P2p term wasn’t compatible with this narrative so it was replaced with “marketplace lending,” which helped it retain its Silicon Valley feel and gave it the range to argue that hedge funds and peers were virtually the same thing since they were both buyers in a new-age marketplace.

But early this year, something started to happen. Loan originators like SoFi (which was never peer-to-peer) could not sell loans fast enough. One solution they came up with was to launch their own hedge fund to buy their own loans. SoFi CEO Mike Cagney said, “In normal environments, we wouldn’t have brought a deal into the market, but we have to lend. This is the problem with our space.”

But blaming financial institutions for pulling back credit is a scenario that has played out thousands of times in history. One only need watch The Big Short to connect why it’s dangerous for a lender to depend on the institutional credit markets. That’s where the peer-to-peer model was supposed to come in, a new way for a new day without Wall Street to prevent these problems.

But it’s not too late to go back. Lending Club for example, has capped their wholesale channel (the institutional portion) at 50%. They’ve kept more than 100,000 retail investors and intend to grow that even larger. “We’ve always been more exposed to retail, and I think we want to keep it that way,” said Lending Club CEO Renaud Laplanche to the Financial Times. “We’ll probably see that as a competitive advantage, as a source of stability and predictability, particularly in an economic downturn,” he added.

Prosper meanwhile has depended almost entirely on the institutional channel, an astounding 92% of their loans were sold to that category of investors. It’s a far cry from the slogan that appeared on their website back in 2007. “People-to-people lending. It’s an old idea that’s new again,” it said. Today it says, “We connect people looking to borrow money with investors.” Those investors are predominantly Wall Street.

But what to do when Wall Street will one day no longer be interested? It’s not too late to go back in time.

“Borrow money from people just like you,” said Prosper’s website nine years ago. People just like you might not suddenly decide they want five percentage points more. Peer-to-Peer implied a human aspect to the marketplace, that empathy played a role in a world where Wall Street had always been stone cold.

Will the industry revert back to the people? Or will ideas such as starting your own hedge fund to buy your own loans rule the day?

Why Square Ditched Their Merchant Cash Advance Program

March 27, 2016 Square did $400 million in merchant cash advances last year. Now they are no longer even offering them. To fill the void, they’ve partnered up with Celtic Bank to issue a unique kind of merchant loan, one in which borrowers have a fixed term to repay but make their payments daily by diverting a percentage of every transaction they process to Square.

Square did $400 million in merchant cash advances last year. Now they are no longer even offering them. To fill the void, they’ve partnered up with Celtic Bank to issue a unique kind of merchant loan, one in which borrowers have a fixed term to repay but make their payments daily by diverting a percentage of every transaction they process to Square.

But why make this change? After all, Square reported that its merchant cash advances typically tended to cycle through to completion in approximately nine months despite there being no fixed term. Their loans will have terms of 18 months, almost ensuring that money will turn over slower, not faster.

Todd Baker, the managing principal of Broadmoor Consulting LLC, says it’s a P/E play. That’s because as part of the change, Square will not be keeping the bulk of the loans on their balance sheet. Instead, they’ll be bundled together and sold to institutional investors. That positions them to be an originator or marketplace dependent on fee income instead of a lender. “Banks and lenders trade at 12x-15x p/e while tech trades at infinity,” Baker said.

Square likely encountered trouble trying to bundle up merchant cash advances because their legal standing across states is not as defined. Celtic Bank-issued-loans however are considered to be rather protected under federal preemption laws established under the Federal Deposit Insurance Act.

But that’s not the whole story either

Online lenders were widely criticized in the wake of the San Bernardino attacks after it was learned the terrorists obtained a loan from Prosper. “The issue may end up being whether marketplace lenders are too easy of a source of cash to finance terrorist attacks,” said Guggenheim Partners analyst Jaret Seiberg in a research letter back in December.

Square’s merchant cash advance program had very little underwriting. The focus was almost entirely on a merchant’s historical sales activity. No credit check was required, nor did applicants have to supply a photo ID or financial statements. This one-click process may have played a major role in originating $400 million in merchant cash advances in 2015, but it probably raised red flags with regulators.

Notably, the new Square Capital application page makes light of this issue. “To help the government fight the funding of terrorism and money laundering activities, Federal law requires all financial institutions to obtain verify and record information that identifies each person who opens an account,” it says. “What this means for you: When you open an account, we will ask for your name, address, date of birth, and other information that will allow us to identify you. We may also ask to see your driver’s license and other identifying documents.”

There’s easy and then there’s too easy. For Square, $400 million a year in merchant cash advances may have been proof of concept for demand but also proof that it was time to slow it down just one notch and make sure they aren’t being reckless.

Few would be impressed by one-click no-underwriting funding if it meant money flowed into the coffers of terrorists even once. Similarly, institutional investors would not be too happy if it was deemed that all of the California merchant cash advances in a bundle they bought were subject to a class action lawsuit. Square can now focus on what they are known for, technology, and perhaps improve their market cap.

By moving away from merchant cash advances, Square has killed at least three birds with one stone. Long live the bank charter model.

Square Swaps Out Merchant Cash Advances for Business Loans

March 25, 2016 Square’s merchant cash advance program is already among the biggest in the world, but they’ve got even bigger plans, or maybe just different ones.

Square’s merchant cash advance program is already among the biggest in the world, but they’ve got even bigger plans, or maybe just different ones.

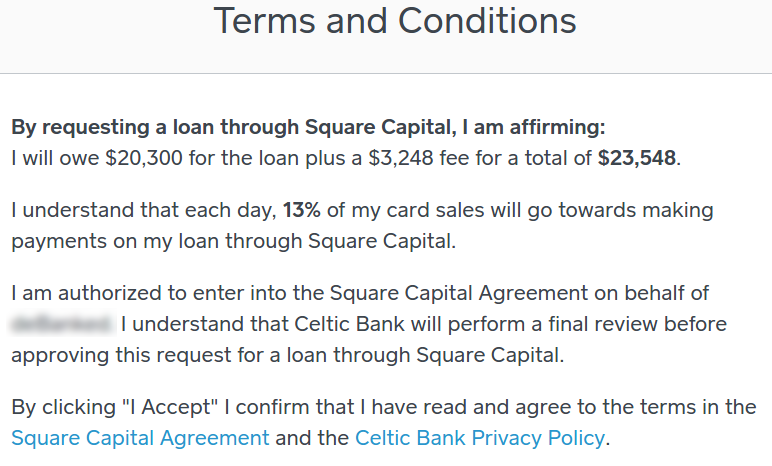

The company announced on Thursday that they will now be offering true business loans as well through a partnership with Celtic Bank, an industrial bank chartered by the State of Utah. The WSJ reports that loan payments will also be made via a split of future credit card sale activity but with the caveat of there ultimately being a fixed term. This is coincidentally how PayPal’s loan product works.

The WSJ makes it seem as if both products will run alongside each other, but a Square merchant revealed to deBanked that all of the language on Square Capital’s application portal has changed from advances to loans. Even the promotional materials have changed to reflect that it may take more than just an automated review of historical credit card sales activity to get approved and funded. Also, all Square loans are subject to credit approval, whereas no credit check was required for merchant cash advances. Applicants may be required to produce a photo ID and other documents for further verification. North Dakota businesses are prohibited from borrowing altogether.

Square’s loans require that merchants process at least $10,000 or more a year. Borrowers must pay at least 1/18th of their initial loan balance every 60 days. PayPal by comparison requires that their borrowers pay down 10% of their loan amount every 90 days.

A Square merchant was not able to locate any mention of the merchant cash advance program. It’s all loans now.

Did Square really just add business loans to their arsenal or have they traded MCAs for the bank charter lending model?

Update: 3/25 2:54 PM Square confirmed that they have indeed replaced their merchant cash advance program with the loan program.

Our Square Capital program is transitioning from merchant cash advances to flexible loans. https://t.co/oUyRtNgVSS pic.twitter.com/ELXC7ayJyU

— Square (@Square) March 25, 2016

Plot Twist: Obama Administration to Comment on Madden v Midland

March 22, 2016

The U.S. Supreme Court wants to know what the Obama administration thinks of the Madden v Midland case.

The potential impact of Madden v Midland on marketplace lending was finally starting to fade away until the U.S. Supreme Court made an unexpected move yesterday. “The Solicitor General is invited to file a brief in this case expressing the views of the United States,” the docket states. At issue is the scope of preemption under the National Bank Act (i.e. can you buy a loan issued by a nationally chartered bank that legally circumvented state usury laws at the time it was originated and still enforce the interest rate?)

The Solicitor General is responsible for arguing cases on behalf of the U.S. government in the U.S. Supreme Court. The position is appointed by the President and confirmed by the Senate. That seat is currently filled by Donald B. Verrilli, Jr., an Obama appointee and the man credited with saving Obamacare. He was the attorney that helped persuade the Supreme Court to treat the individual mandate of the Patient Protection and Affordable Care Act as a tax and not as an exercise of Congress’s power under the Commerce Clause.

Any brief filed is bound to become politically significant since the Obama Administration is on its way out. Therefore any views it expresses in the next few months may not be the same views of the next administration scheduled to be sworn in ten months from now.

Madden v Midland will have no bearing on merchant cash advances and little if any bearing on commercial marketplace lenders. That’s because most not only work with state chartered banks instead of nationally chartered banks, but also face more favorable state usury laws since they do not lend to consumers.

Lending Club Performance Data Has Obvious Errors, Investors Say

March 20, 2016There’s something wrong with the returns Lending Club is dangling in front of investors, some diligent note buyers say. And the numbers are so far off, that it’s being chalked up as a bug, instead of something nefarious.

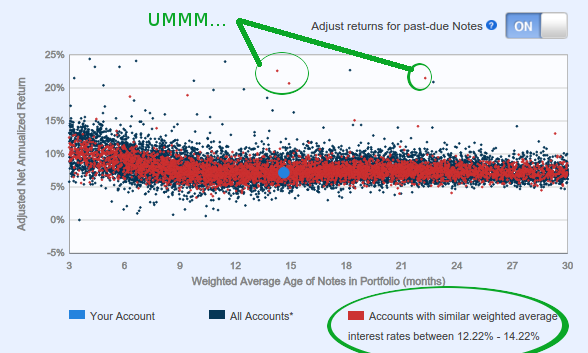

On the “Understanding Your Returns” page, investors can view how their portfolio stacks up against all others on the platform with the same weighted average interest rate. Most investors will end up somewhere in the middle, but a few are outperforming the rest with seemingly impossible results.

The flawed chart, which I could duplicate myself, shows investors supposedly making over 20% annual returns on seasoned portfolios where the weighted average interest rate of notes is between 12.22% and 14.22%. But how can an overall return be so much greater than the interest rates that make up the portfolio? They can’t be. But Lending Club’s chart tells a different tale.

With projected defaults, the adjusted returns should be lower than the weighted average interest rate, certainly not much higher and definitely not double.

On the Lend Academy forum where this was noticed, at least one investor said they emailed Lending Club on March 18th to alert them to the impossible performance data.

For now, the page that is meant to help investors understand their returns, is doing anything but.

Update 3/22: Lending Club has reportedly told an investor asking about this discrepancy that it is indeed a bug and will be fixed.

Update 3/24: This has mostly been fixed

Merchant Cash Advances Not Governed by Truth in Lending Act, Fed Says

March 16, 2016 Ellyn Terry, an Economic Policy Analysis Specialist at the Federal Reserve Bank of Atlanta, wrote on the Fed’s blog that merchant cash advances are not governed by the Truth in Lending Act.

Ellyn Terry, an Economic Policy Analysis Specialist at the Federal Reserve Bank of Atlanta, wrote on the Fed’s blog that merchant cash advances are not governed by the Truth in Lending Act.

“Because an MCA is structured as a commercial transaction instead of a loan, it is regulated by the Uniform Commercial Code in each state instead of by banking laws such as the Truth in Lending Act,” wrote Fed analyst Ellyn Terry on March 15th. “Consequently, the provider does not have to follow all of the regulations and documentation requirements (such as displaying an APR) associated with making loans.”

While Terry applies some incorrect characteristics to describe the nature of the parties in a future receivable purchase transaction (by calling them a lender and borrower instead of a buyer and seller), she was able to broadly describe the nature of MCAs.

“MCAs have been around for decades, but their popularity has risen in the wake of the financial crisis,” she wrote. “Typically a lump-sum payment in exchange for a portion of future credit card sales, the terms of MCAs can be enticing because repayment seems easier than paying off a structured business loan that requires a fixed monthly payment.”

Retail Investors Can Invest In Business Loans – Thanks To StreetShares Regulatory Approval

March 16, 2016 If not being an accredited investor has kept you on the sidelines of marketplace lending, you’ll soon be able to invest in business loans on the StreetShares platform, thanks to a special regulatory approval by the SEC. While you’re not going to the earn the yields you’d get with merchant cash advance (MCA) syndication, StreetShares makes loans for as short as three months. The available products are 3, 6, 12, 18, 24 & 36 month term loans, according to their website, which are desirable lengths for investors used to MCA. The Funding Circle platform by contrast, requires investors be accredited and loan terms range from 1 to 5 years. If you aren’t eligible to invest through Funding Circle, well that is what will make StreetShares different.

If not being an accredited investor has kept you on the sidelines of marketplace lending, you’ll soon be able to invest in business loans on the StreetShares platform, thanks to a special regulatory approval by the SEC. While you’re not going to the earn the yields you’d get with merchant cash advance (MCA) syndication, StreetShares makes loans for as short as three months. The available products are 3, 6, 12, 18, 24 & 36 month term loans, according to their website, which are desirable lengths for investors used to MCA. The Funding Circle platform by contrast, requires investors be accredited and loan terms range from 1 to 5 years. If you aren’t eligible to invest through Funding Circle, well that is what will make StreetShares different.

Unlike the laborious process that Lending Club and Prosper took with the SEC to sell loan performance-dependent notes to unaccredited investors, StreetShares got a special approval under the JOBS Act’s Regulation A+. That only allows them to raise up to $50 million over a 12-month period so investing availability may be limited.

In a press release, the company specified that “repayment to investors is not tied to the performance of a particular underlying loan.” The LendAcademy blog is reporting that “StreetShares will provide a vehicle for investors to become diversified through some kind of fund” and that details should be revealed around the time of the LendIt Conference.

Though company CEO Mark Rockefeller of StreetShares might not remember this, we spoke during a lunch break at LendIt 2014 when his company was a brand new startup. At that time, he told me about his “veterans funding veterans” lending marketplace model where the costs would be much lower than what can be experienced in the merchant cash advance industry. Since then his company has won the 2015 #1 global Best Investment Award from Harvard Business School and is now the first small business lender to get approval under Regulation A+.

One other person that is trying to bring small business lending investing to the unaccredited investor community is hedge fund manager Brendan Ross. Ross’s Direct Lending Income Fund filed an N-2 with the SEC at the conclusion of last year to become a “40 Act fund,” a special investment company permitted under The Investment Company Act of 1940 that can accept investments from retail investors. In January, Ross explained to CNBC during an interview that the fund’s structure would be converted so that investors become shareholders in what would essentially be a lending business.

StreetShares plans to officially debut their new program at LendIt next month.

Google Culls Online Lenders – Pay or Else?

March 15, 2016Can you become one of the biggest or most successful online lenders without Google? A search layout update may be inadvertently culling the herd.

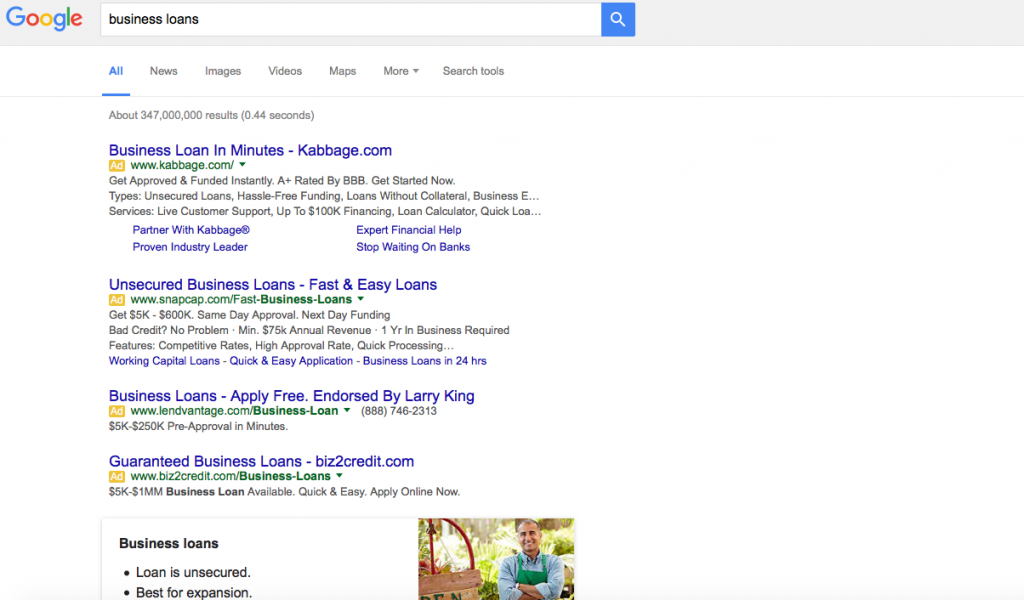

In late February, Google eliminated ads from the right side of the page while adding another layer to the top and bottom. When factoring in features like site links, the effects on organic search has been devastating. Non-paid links are now entirely below the fold for many commercial keywords, which means users may limit their selections entirely to ads. Here’s an example of a full screen browser window on a Macbook Air when searching for Business Loans:

Brad Geddes, a Google Adwords marketing author, expert and consultant, has said the Click-through rate (CTR) on this new 4th ad placement is skyrocketing. “Depending on the keyword, position 4 is going to have a 400%-1000% CTR increase,” he said on Webmaster world. And while side links and bottom links were never a huge factor anyway (less than 15% of click-throughs), Geddes believes a consequence of this change is that fewer ad slots means higher cost bids to rank on the 1st page. “Companies with thin margins are going to have a lot of words fall to page 2,” he wrote.

In summary: Fewer ad placements, higher costs per click, decreased likelihood of organic click-throughs.

And the online lending industry is already feeling the burn. Several funders and ISOs on the commercial side have told deBanked in confidence that the online lead gen battle has been lost or that they have been temporarily sidelined by the increase in costs. At least one funder is refocusing their efforts entirely on the ISO channel after a horrible experience with Pay-Per-Click.

And it’s not just the costs, it’s the quality of leads, they say. The searchers clicking their expensive ads and running up their bills sometimes literally meet none of the qualifications their ads stipulate. Yet many searchers click anyway, rendering the ads’ carefully scripted messages moot. One study might explain why that is. In it, users spent around .764 seconds considering the first paid search result and a total of only 4.5 seconds scanning the first five results. That’s not a whole lot of time to read each ad, digest them and consider whether or not there’s an appropriate fit.

And it’s not just the costs, it’s the quality of leads, they say. The searchers clicking their expensive ads and running up their bills sometimes literally meet none of the qualifications their ads stipulate. Yet many searchers click anyway, rendering the ads’ carefully scripted messages moot. One study might explain why that is. In it, users spent around .764 seconds considering the first paid search result and a total of only 4.5 seconds scanning the first five results. That’s not a whole lot of time to read each ad, digest them and consider whether or not there’s an appropriate fit.

On one industry forum, ISOs have reported that the cost of acquiring a merchant cash advance or business loan deal from Pay-Per-Click is ranging from $700 to $1,200. “PPC for premium keywords as high as $40 at times. Ugly. Real ugly,” one user wrote. Another user wrote, “It’s not just Adwords that is saturated. The whole market is saturated. Lenders and the onslaught of new brokers are making it tough. Lenders with programs like Funding Circle and Kabbage, and with all the advertising money in the world to burn and get direct traffic.” And still another believes that online ads are simply inviting the lowest hanging fruit. “Internet leads have the highest level of fraud,” said one sales manager.

Notably, many of the top 8 funders are only competing for a limited number of competitive keywords or may not even be running Adwords at all. PayPal and Square for example, focus only on their existing payment processing customers despite being “online lenders.”

It’s too early to tell what effects Google’s ad changes will have on the online lending industry, though a couple of companies who were paying just enough to extract clicks from side ads have indicated the change is for the worse and they have suspended their campaigns.

The natural alternative to paid search, organic search, is seldom discussed anymore as a realistic strategy these days, in part because the rankings might be rigged anyway.

One irony that’s pervasive in the online lending industry is that borrowers are being targeted offline where it’s potentially more affordable. In a discussion thread that garnered 76 posts last fall, ISOs and funders suggested that direct mail, referrals, UCCs, cold calling, radio and even going out and shaking hands, were pegged as “what’s next” for marketing. Pay-Per-Click was only mentioned once and only in the context of it being something that had long ago been made too expensive for small and mid-size companies.

The cost of making these things work might be why so many funders are hoping that brokers can figure it out. “We decided that the best way to grow is to build relationships to avoid the overhead, compliance, training and manpower that a sales team would require,” said Nulook Capital’s Jordan Feinstein in an interview with deBanked last month.

With Google becoming even more competitive now though, perhaps United Capital Source’s Jared Weitz summed it up best. “Marketing is getting more expensive and only the ones who can afford to pay can play,” Weitz said.