Sean Murray is the President and Chief Editor of deBanked and the founder of the Broker Fair Conference. Connect with me on LinkedIn or follow me on twitter. You can view all future deBanked events here.

Articles by Sean Murray

Confidence in MCA and Online SMB Lending Industry Ticks Up

September 26, 2017The latest industry CEO survey conducted by Bryant Park Capital and deBanked showed that confidence in the continued success of the SMB lending/MCA industry is coming back. Confidence had a hit a low of 73.8% in Q1 of this year, the lowest point since the survey started in 2015. In Q3, the number jumped up to 81.3%.

Confidence in being able to access capital at a reasonable cost to grow ticked up only slightly to 79.9%, up from its lowest point in Q1 this year at 78.7%.

The first quarter of 2016 holds the confidence record since the surveying began. Coincidentally, that period is widely considered to be the peak of the online lending bubble. An April 2016 blog post published during that year’s annual LendIt Conference declared an end to the euphoria.

While respondents to the most recent survey were not asked to explain their confidence level, factors like a steady regulatory climate and some recent competition-reducing consolidation likely played a role in the boost.

Bizfi Survives, Thanks to World Business Lenders Asset Purchase Deal

September 22, 2017 The Bizfi marketplace is slated to live on, according to Stephen Sheinbaum who joined World Business Lenders (WBL) as a managing director in July. On Wednesday, WBL purchased several assets from Bizfi including the brand, the marketplace, the Next Level Funding renewal book, and other related pieces of the company, he says. Sheinbaum founded Bizfi (then Merchant Cash and Capital) in 2005.

The Bizfi marketplace is slated to live on, according to Stephen Sheinbaum who joined World Business Lenders (WBL) as a managing director in July. On Wednesday, WBL purchased several assets from Bizfi including the brand, the marketplace, the Next Level Funding renewal book, and other related pieces of the company, he says. Sheinbaum founded Bizfi (then Merchant Cash and Capital) in 2005.

WBL, a Jersey City-headquartered small business lender will also be a lender on the platform.

Other key Bizfi personnel have joined WBL including former Managing Director of Renewals John BellaVia, VP of Sales Michael Caronna, and Sales Manager Ryan Bressler.

The asset purchase does not affect the deal forged with Credibly to service the $250 million portfolio, Sheinbaum explains, which is separate.

While lesser known among the mainstream fintech media, WBL has been a stalwart player in the non-bank lending industry for years. Their ambitions and size became more apparent when deBanked attended their invite-only annual shareholder meeting at the Waldorf Astoria in NYC in 2015. The company went on to open a massive office in Jersey City in July 2016 that was attended by Jersey City Deputy Mayor Marcos Vigil, Councilwoman Candice Osborne, Archbishop David Billings and Mitchell Rudin, the CEO of Mack-Cali. At the ceremonial ribbon cutting, WBL CEO Doug Naidus said that he wanted to build a company that lasts, one that he can look back on and be proud of.

Now with the Bizfi brand and marketplace in tow, the company is uniquely positioned.

“[It’s a] game changer here,” Sheinbaum said. “2.0 here we come!”

C-level Credit Exec Leaves Lending Club for Affirm

September 21, 2017Lending Club’s Chief Credit Officer and Interim General Manager, Sandeep Bhandari, has joined fintech lender Affirm, according to Affirm CEO Max Levchin. Levchin posted the following on LinkedIn:

I am excited to announce and welcome Sandeep Bhandari to Affirm, Inc. as Chief Strategy and Risk Officer (CSRO).

Sandeep joins us from Lending Club where he was the Chief Credit Officer (CCO). Prior to Lending Club, he was at Capital One for many years, where he was Assistant Chief Credit Officer at Capital One Bank (Credit Risk Management) and Venture Partner (Capital One Ventures). Prior to that Sandeep held a variety of roles requiring expertise in strategy, credit risk management, marketing, product development, and underwriting across several lines of business including consumer and small business credit card, auto lending, and mortgage and home equity lending.

We are excited for Sandeep to join us for our next phase of rapid growth and to help us fulfill our mission of delivering honest financial products that improve lives.

The move comes on the heels of Lending Club announcing their “most advanced and predictive credit model ever.” Bhandari was responsible for credit strategy and overall credit risk management at Lending Club and presumably would’ve overseen that.

Talkative investors on the LendAcademy forum were not immediately sold on Lending Club’s new system, however. Some users bemoaned that Lending Club is ignoring common sense in favor of data. In one instance, the CEO of PeerCube referenced an interest rate anomaly alleged to be discovered in Lending Club’s pricing as “Data-driven but knowledge-unaware.”

Affirm and Lending Club differ. Whereas Lending Club targets the credit card refinancing market, Affirm helps consumers finance purchases. Last month, Affirm and Walmart were reportedly in talks to offer financing to consumers.

CFPB’s Small Business Lending RFI is Now Closed

September 18, 2017The window to share your two cents on the CFPB’s quest to collect data on small business lending has closed. The extended deadline to respond to the RFI was September 14th.

The agency received 2,668 comments, 650 of which you can read online. Most responses that deBanked reviewed asked the CFPB to exempt certain businesses such as community banks from the law. Others denounced the CFPB’s objective as misguided or poorly thought-out from the get-go.

Nevertheless, Section 1071 of the 2009 Wall Street Reform and Consumer Protection Act directed the CFPB to collect data on small business lending presumably to determine if women and minorities are treated differently.

Some observers expected this initiative to be derailed when Richard Cordray, the Director of the CFPB, resigned to campaign for Governor of Ohio. However, the governor’s race is now in full swing and he has yet to resign, and could now possibly remain in his position until it expires next year.

The implementation of any resulting rule from the RFI would likely not take place until some time in the 2020s, sources contend.

The Top Small Business Funders By Revenue

September 14, 2017Thanks to the Inc 5000 list on private companies and earnings statements from public companies, we’ve been able to compile rankings of alternative small business financing companies by revenue. Companies that haven’t published their figures are not ranked.

| SMB Funding Company | 2016 Revenue | 2015 Revenue | Notes |

| Square | $1,700,000,000 | $1,267,000,000 | Went public November 2015 |

| OnDeck | $291,300,000 | $254,700,000 | Went public December 2014 |

| Kabbage | $171,800,000 | $97,500,000 | Received $1.25B+ valuation in Aug 2017 |

| Swift Capital | $88,600,000 | $51,400,000 | Acquired by PayPal in Aug 2017 |

| National Funding | $75,700,000 | $59,100,000 | |

| Reliant Funding | $51,900,000 | $11,300,000 | Acquired by PE firm in 2014 |

| Fora Financial | $41,600,000 | $34,000,000 | Acquired by PE firm in October 2015 |

| Forward Financing | $28,300,000 | ||

| IOU Financial | $17,400,000 | $12,000,000 | Went public through reverse merger in 2011 |

| Gibraltar Business Capital | $16,000,000 | ||

| United Capital Source | $8,500,000 | ||

| SnapCap | $7,700,000 | ||

| Lighter Capital | $6,400,000 | $4,400,000 | |

| Fast Capital 360 | $6,300,000 | ||

| US Business Funding | $5,800,000 | ||

| Cashbloom | $5,400,000 | $4,800,000 | |

| Fund&Grow | $4,100,000 | ||

| Priority Funding Solutions | $2,600,000 | ||

| StreetShares | $647,119 | $239,593 |

Companies who were published in the 2016 Inc 5000 list but not the 2017 list:

| Company | 2015 Revenue | Notes |

| CAN Capital | $213,400,000 | Ceased funding operations in December 2016, resumed July 2017 |

| Bizfi | $79,000,000 | Wound down |

| Quick Bridge Funding | $48,900,000 | |

| Capify | $37,900,000 | Wound down |

The Google Battle for Lending and SMB Finance Keywords

September 14, 2017The online lending battle is at least in part being fought online. Below is a chart of organic page 1 rankings in Google for some of the industry’s biggest players, banks, and the SBA. (Hat tip to Fundera and NerdWallet):

| Keywords | OnDeck | Kabbage | Fundera | Lending Club | NerdWallet | National Funding | Traditional Banks | SBA.gov |

| business loan | 1 | 9 | 3 | 5 | 4,7 | 6 | ||

| merchant cash advance | 2 | 3 | 4 | 8 | ||||

| working capital | 9 | 4 | ||||||

| commercial loan | 3 | 2,7 | ||||||

| small business loans | 2 | 3 | 5 | 7 | 1 | |||

| business line of credit | 3 | 2 | 11 | 1,4 | 6,7,8,9,10 | 5 | ||

| fast business loan | 1 | 4 | 2 | 5,6 | ||||

| business loan with bad credit | 7 | 1 | 2 | 3 |

The Top 10 Google Search Results for Merchant Cash Advance in February 2012 compared to now:

| February 2012 | September 2017 |

| MerchantCashinAdvance.com | Wikipedia |

| Yellowstone Capital | OnDeck |

| Entrust Cash Advance | Fundera |

| Merchants Capital Access | NerdWallet |

| Merchant Resources International | Businessloans.com |

| American Finance Solutions | Bond Street |

| Nations Advance | Capify |

| Bankcard Funding | National Funding |

| Rapid Capital Funding | CNN |

| Paramount Merchant Funding | CAN Capital |

The top result in 2012 is a great example of how much easier it was to game Google’s system back then. After achieving rank #1 for MCA and 300 other related keywords, MerchantCashInAdvance.com, which was just a lead generation site, sold for $75,000 in December 2011. The site was later clobbered by Google Penguin for black hat SEO and banished from visibility.

A major shift has obviously taken place over the last 5 and a half years. Is the search results game rigged to advance Google’s own interests? Three years ago I put forth my theory on that.

One thing that’s different between then and now is that Google now has 4 paid links above the organic search results as opposed to 3 and the paid links blend in more with the organic results. With the organic results pushed further down the page, they’re not as visible as they were five years ago.

Read my previous analyses on the industry’s search war over the years:

December 2015 Google Serves Low Blow to Merchant Cash Advance Seekers

March 2015 Google Culls Online Lenders – Pay or Else?

October 2014 Merchant Cash Advance SEO War Still Raging

August 2014 Six Signs Alternative Lending is Rigged: Do Lending Club and OnDeck have a helping hand?

October 2013 Google Penguin 2.1 takes swing at the MCA industry

August 2013 Your merchant cash advance press release may be hurting you

December 2012 Is Google your only web strategy?

July 2012 The other 93% [of leads]

April 2012 The SEO war continues

February 2012 The SEO War for Merchant Cash Advance: The first story on this topic

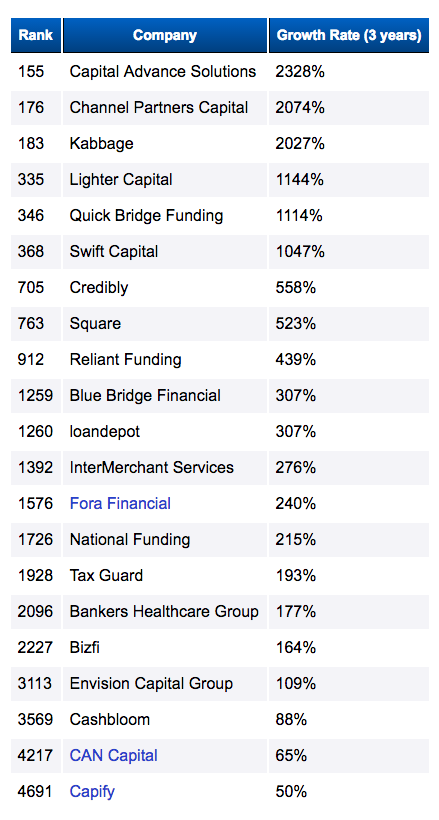

Where Alternative Finance Ranks on the Inc 5000 List

September 14, 2017Here’s where your peers rank on the Inc 5000 list for 2017:

| Ranking | Company Name | Growth | Revenue | Type |

| 15 | Forward Financing | 12,893.16% | $28.3M | MCA |

| 47 | Avant | 6,332.56% | $437.9M | Online Consumer Lender |

| 219 | OppLoans | 1,970.22% | $27.9M | Online Consumer Lender |

| 260 | US Business Funding | 1,657.42% | $5.8M | Business Lender |

| 361 | nCino | 1,217.53% | $2.4M | Software |

| 449 | Kabbage | 979.31% | $171.8M | Online Consumer Lender |

| 634 | Lighter Capital | 712.03% | $6.4M | Online Business Lender |

| 694 | Swift Capital | 652.08% | $88.6M | Business Lender |

| 789 | CloudMyBiz | 575.46% | $2.1M | IT Services |

| 1418 | loanDepot | 286.11% | $1.3B | Online Consumer Lender |

| 1439 | Nav | 281.98% | $2.7M | Online Lending Services |

| 1731 | United Capital Source | 224.85% | $8.5M | MCA |

| 1101 | ZestFinance | 165.99% | $77.4M | Online Lending Services |

| 2050 | National Funding | 184.74% | $75.7M | Online Business Lender |

| 2572 | Blue Bridge Financial | 136.73% | $6.6M | Online Business Lender |

| 2708 | Bankers Healthcare Group | 127.51% | $149.3M | Financial Services |

| 2714 | Tax Guard | 127.02% | $9.9M | Financial Services |

| 2728 | Fora Financial | 125.81% | $41.6M | Online Business Lender |

| 2890 | Reliant Funding | 121.61% | $51.9M | Online Business Lender |

| 4005 | Cashbloom | 70.47% | $5.4M | MCA |

| 4945 | Gibraltar Business Capital | 42.08% | $16M | MCA |

Compare that to last year’s list below:

Of the companies on the 2016 list, Capify and Bizfi were wound down while CAN Capital ceased operations but then later resumed them more than half a year later.

Bond Street Has Stopped Lending

September 13, 2017 NYC-based small business lender Bond Street has stopped making new loans, according to sources who worked with them. The Wall Street Journal published a similar report earlier today. In addition, the WSJ reported that Goldman Sachs is hiring 20 of Bond Street’s employees.

NYC-based small business lender Bond Street has stopped making new loans, according to sources who worked with them. The Wall Street Journal published a similar report earlier today. In addition, the WSJ reported that Goldman Sachs is hiring 20 of Bond Street’s employees.

Just seven months ago, Bond Street announced that they had closed a $300 million loan purchase agreement with Jefferies. The WSJ reported that an inability to raise additional equity is what threw a wrench in their future. The same situation happened to Bizfi just a few short months ago, who wound down after 10 years and shipped their portfolio off to rival Credibly to service.

Bond Street’s 1-3 year loans with APRs ranging from 8% – 25% were terms that many in the alternative business lending universe say is a fundamentally unprofitable model. The company now appears to be joining the ever growing purgatory of alternative small business finance companies. They join Dealstruck, Herio Capital, Bizfi, and Nulook Capital. CAN Capital was previously on that list but was recently restructured and revived.

Able Lending, another small business lender, denied that they were going out of business but admitted they were looking to be acquired.

Square is also reportedly in talks to hire Bond Street employees, the WSJ claims. When Bizfi closed, their employees were mainly picked up by rivals World Business Lenders, Strategic Funding, iPayment, 6th Avenue Capital, and others.