Sean Murray is the President and Chief Editor of deBanked and the founder of the Broker Fair Conference. Connect with me on LinkedIn or follow me on twitter. You can view all future deBanked events here.

Articles by Sean Murray

deBanked Visits Local Commercial Finance Brokerage – Horizon Funding Group

October 22, 2020deBanked reporter Johny Fernandez visited the storefront office of Horizon Funding Group, a commercial finance brokerage located in Brooklyn. The company is owned by brothers James and John Celifarco.

The FTC’s Power to “Wipe Out” is Under Siege

October 9, 2020 As the FTC contemplates how to “wipe out” entire industries, federal courts around the country have recently ruled that the regulator can’t accomplish such a goal under Section 13(b) of the FTC act. That’s the statute the FTC relied on to bring its most recent actions against merchant cash advance companies. It might not have bite.

As the FTC contemplates how to “wipe out” entire industries, federal courts around the country have recently ruled that the regulator can’t accomplish such a goal under Section 13(b) of the FTC act. That’s the statute the FTC relied on to bring its most recent actions against merchant cash advance companies. It might not have bite.

Under 13(b), the FTC is empowered to bring a lawsuit to obtain an injunction against unlawful activity that is currently occurring or is about to occur. It’s powerful, but very limited. However, for the last several decades, the FTC, with the help of federal courts, has interpreted the statute to mean that it can also force the defendants to “disgorge” with illegally obtained funds.

That’s how the FTC wiped out Scott Tucker and his payday lending empire. In a lawsuit the FTC brought against his companies under 13(b) in 2012, the Court entered a judgment of $1.3 billion against him.

Not so fast, modern legal analysis says. Tucker’s case is being brought before the Supreme Court of the United States to settle once and for all what 13(b) allows for and what it doesn’t.

The momentum does not weigh in the FTC’s favor.

On September 30, the Third Circuit ruled in FTC v AbbVie that the FTC is not entitled to seek disgorgement under 13(b). The Seventh Circuit arrived at a similar conclusion last year in FTC v Credit Bureau Center.

In an interview with NBC, FTC Commissioner Rohit Chopra said in August “We’ve started suing some [merchant cash advance companies] and I’m looking for a systemic solution that makes sure they can all be wiped out before they do more damage.”

As the FTC attempts to be more proactive in the area of small business finance, it will be important to monitor what the Supreme Court ultimately decides it can actually accomplish.

LendingClub Formally Ends “Peer” Aspect of Its Business, Proceeding With Radius Bank Acquisition

October 7, 2020 LendingClub is finally ending the “peer-to-peer” aspect of its platform for good. Earlier today, the company announced that it would cease offering and selling Member Payment Dependent Notes effective December 31st.

LendingClub is finally ending the “peer-to-peer” aspect of its platform for good. Earlier today, the company announced that it would cease offering and selling Member Payment Dependent Notes effective December 31st.

“Ceasing the Retail Notes program will allow LendingClub to redeploy capital and improve platform efficiency, enabling the company to help even more members as LendingClub progresses towards closing the Merger and becoming a bank holding company,” the company said in an official statement. “All Retail Notes outstanding as of the date the Retail Note program is ceased will be unaffected by the cessation of the program. Accordingly, with respect to such outstanding Retail Notes, LendingClub will continue servicing the corresponding member loans and information regarding such Retail Notes will remain viewable in the applicable Retail Note investor accounts.”

LendingClub rose to fame with its peer-to-peer model nearly a decade ago, but using retail investors to fund loans has been eroding over time. ‘Peers’ Are Almost Gone From Lending Club’s Funding Mix was the title of a February 2019 deBanked story that highlighted this trend, for example.

LendingClub rose to fame with its peer-to-peer model nearly a decade ago, but using retail investors to fund loans has been eroding over time. ‘Peers’ Are Almost Gone From Lending Club’s Funding Mix was the title of a February 2019 deBanked story that highlighted this trend, for example.

Meanwhile, the focus on Radius Bank is a reminder that the announcement made nearly 8 months ago is still a work-in-progress.

“In connection with and in furtherance of the Merger, LendingClub has been in regular contact with federal banking regulators and, on September 25, 2020, filed an FR Y-3 application with the Federal Reserve to become a bank holding company,” the company said. “LendingClub plans to offer a full suite of products as a bank. This includes a high-yield savings account that will be initially exclusively available to its existing retail investors and will offer a compelling interest rate, as well as other products that take advantage of the marketplace to allow its customers to both pay less when borrowing and earn more when saving.”

Radius Bank was the subject of a major deBanked Magazine story in 2017 titled Tech Banks: Will Fintech Dethrone Traditional Banking?

Yellowstone Capital Moves to Dismiss FTC Lawsuit

October 3, 2020 Newly revealed in court documents filed on Friday is that the recent FTC lawsuit against Yellowstone Capital culminated after a 2-year inquiry. What may have been a surprise to the Yellowstone defendants is how the FTC brought its case or that it ultimately even decided to bring one at all. A motion to dismiss has been filed.

Newly revealed in court documents filed on Friday is that the recent FTC lawsuit against Yellowstone Capital culminated after a 2-year inquiry. What may have been a surprise to the Yellowstone defendants is how the FTC brought its case or that it ultimately even decided to bring one at all. A motion to dismiss has been filed.

Specifically, counsel for Yellowstone references in its papers that in the preceding years, Yellowstone had already complied with FTC discovery requests that amounted to the production of “24,000 pages of documents, more than 1,400 audio recordings, and responses to numerous interrogatories and follow-up inquiries.”

Following that, the FTC filed suit on August 3, 2020, alleging Misrepresentations Regarding Collateral and Personal Guarantees, Misrepresentations Regarding Financing Amount, and Unfair Unauthorized Withdrawals. In it, it relies heavily on alleged materials dating as far back as five years ago to make its case.

This is fatal to the FTC’s suit, the defendants contend, because the FTC laid out its claims under a very specific statute of the FTC Act, Section 13(b), which can only be brought in federal court if they believe a defendant “is violating, or is about to violate” this area of the law. Past conduct, they say, even if it were true, is not applicable. No acts in 2020 or even from 2019 are alleged with any particularity, nor is it said that any might be happening or will happen.

Some of the purported web pages, ads, or contracts that the FTC refers to no longer exist, have long since been replaced, were taken out of context, or could not even be identified as to where or whom they even originated from, defendants say.

Some of the purported web pages, ads, or contracts that the FTC refers to no longer exist, have long since been replaced, were taken out of context, or could not even be identified as to where or whom they even originated from, defendants say.

Defendants make further arguments for dismissal, one of which takes issue with alleged quotes or comments made by anonymous merchant customers. “The Complaint does not indicate, for instance, if these unidentified customers had breached their MCA agreements or otherwise incurred additional fees beyond the Purchased Amount that were due and owing to Yellowstone under their respective agreements.”

Deprived of all context and specifics, the complaint is loaded with elements that look bad but fall well short of the necessary legal burden, defendants essentially argue.

“The FTC has overextended itself in this litigation,” defendants say in their papers.

They further raise concern that it arises from a possible personal agenda rather than a legally-founded one. Reference is made to an NBC interview in which FTC Commissioner Rohit Chopra told the interviewer that “We’ve started suing some [merchant cash advance companies] and I’m looking for a systemic solution that makes sure they can all be wiped out before they do more damage.”

Chopra had also issued an official statement regarding Yellowstone in which he expounded almost entirely on legal questions that were not even raised in the lawsuit itself but create the impression that they are.

Yellowstone has asked for a stay of discovery pending the outcome of the motion to dismiss.

You can read Yellowstone’s full motion to dismiss here.

The FTC’s interest in this area of finance has been known for some time.

Another Attorney Charged Criminally in 1 Global Capital Saga

September 29, 2020 Andrew Dale Ledbetter, a veteran securities attorney who once co-authored a book called How Wall Street Rips You Off – and what you can do to defend yourself, now stands accused of ripping investors off.

Andrew Dale Ledbetter, a veteran securities attorney who once co-authored a book called How Wall Street Rips You Off – and what you can do to defend yourself, now stands accused of ripping investors off.

Ledbetter was criminally charged on Tuesday by the US Attorney’s office in South Florida for his alleged role in the 1 Global Capital Securities fraud case. Ledbetter was formally accused of Conspiracy to Commit Wire Fraud and Securities Fraud. He was simultaneously hit with civil charges by the Securities and Exchange Commission.

Both agencies say that Ledbetter reaped nearly $3 million in referral fees from 1 Global Capital in exchange for raising nearly $100 million from investors, mostly retirees, all while making knowingly false statements and misrepresentations about the investments. For instance, they say that he knew the investments were securities but claimed they weren’t anyway. Similar circumstances brought down Florida attorney Jan Douglas Atlas last year. Ledbetter had been compensating Atlas on the side as part of the alleged scheme.

Ledbetter is the 4th individual to be criminally charged in connection with the 1 Global Capital case. The other three: Atlas, Alan G. Heide, and Steven Schwartz, have all already pled guilty.

Following Nine Lawsuits, OnDeck Discloses Supplementary Details Behind Planned Enova Merger

September 28, 2020

After OnDeck announced its planned merger with Enova, it was sued nine different times (See here and here) by shareholders that accused the company’s Board of Directors that they had failed to disclose material information about the deal.

OnDeck formally responded on Monday, September 28th, wherein they disclosed that plaintiffs in all of those actions had agreed to dismiss their claims in light of the release of this supplemental information:

The Company and Enova believe that the claims asserted in the Actions are without merit and that no supplemental disclosures are required under applicable law. However, in an effort to put the claims that were or could have been asserted to rest, to avoid nuisance, minimize costs and avoid potential transaction delays, and without admitting any liability or wrongdoing, the Company has determined to voluntarily supplement the Proxy Statement/Prospectus as described in this Current Report on Form 8-K to address claims asserted in the Actions, and the plaintiffs in the Actions have agreed to voluntarily dismiss the Actions in light of, among other things, this supplemental disclosure. Nothing in this Current Report on Form 8-K shall be deemed an admission of the legal necessity or materiality of any of the disclosures set forth herein. To the contrary, the Company and the other defendants specifically deny all allegations in the Actions that any additional disclosure was or is required and expressly maintain that, to the extent applicable, they have complied with their respective legal obligations.

OnDeck first re-explained its background situation leading up to the Enova deal:

Starting in April 2020, OnDeck management commenced a review of potential financing options to secure additional liquidity and potentially replace the Corporate Line Facility and began contacting potential sources of alternative financing, including mezzanine debt. OnDeck contacted, or was contacted by, more than ten potential sources of mezzanine or alternative financing, and received pricing indications from four sources. The interest rates offered by those alternative financing sources ranged from 1-month LIBOR plus 900 basis points to 1,700 basis points (in addition to an upfront fee) and all but one required a significantly dilutive equity component. The one proposal that did not include an equity component was at an interest rate of 1-month LIBOR plus 1,400 basis points to 1,700 basis points. Based on the initial term sheets proposed, OnDeck engaged in negotiations with each of the four potential sources of alternative financing. As these negotiations progressed and COVID-19’s impact on the macro economy and OnDeck’s loan portfolio intensified, two of the four potential sources of alternative financing ceased to actively participate in negotiations. Discussions with the final two potential sources of alternative financing remained ongoing through the time that OnDeck and Enova entered into the merger agreement. Throughout the Process, OnDeck management reported the status of such negotiations on a frequent and ongoing basis to the OnDeck Board for its deliberation in the context of OnDeck’s standalone plan, and the OnDeck Board considered the significant uncertainty of being able to reach agreement on alternative financing in its decision to enter into the merger agreement.

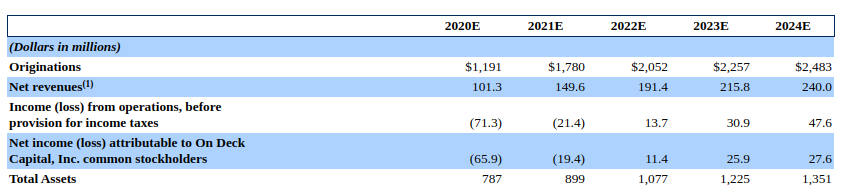

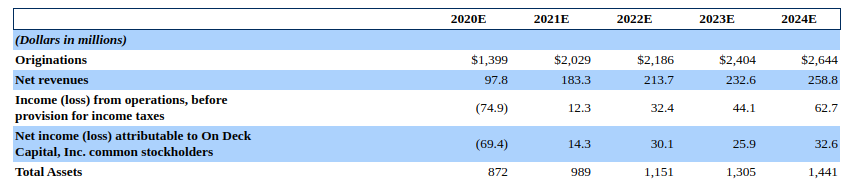

Of particular contention in the deal were OnDeck’s financial projections, prepared to estimate OnDeck’s trajectory as an independent entity. Shareholders complained that there were two sets of books and that they only got to see one. The other set, dubbed Scenario 1, had been used to shop OnDeck around to other suitors. OnDeck published both sets in their supplemental materials on Monday.

The difference is stark. Originally disclosed to shareholders was a projected cumulative net loss of $20.4 million through the end of 2024. The other set of projections, Scenario 1, state a cumulative net income of $33.5 million over the same time period, a difference of over $50 million.

The original predicted a 2021 net loss of $19.4 million while Scenario 1 predicted a net income of $14.3 million.

One reason offered for selecting the less optimistic of the two is that OnDeck’s management determined that loan originations were trending below both sets of projections as of July 12th. OnDeck announced the Enova deal about two weeks later.

Shareholders will cast their votes on the merger on October 7th. OnDeck’s Board “unanimously recommends” that they vote in favor of the proposed merger with Enova.

United Capital Source CEO Jared Weitz Discusses The State of Small Business Finance

September 24, 2020Jared Weitz, the CEO of United Capital Source, recently sat down (virtually) for an interview with me to discuss the state of small business finance. During it, Weitz makes an alarming prediction, that pandemic related events will lead to 50% of all restaurants permanently closing. You can watch our full talk below:

NYC Taxi Drivers Protest, deBanked Reporter Goes For a Ride

September 17, 2020 On Thursday, NYC taxi drivers shut down the Brooklyn Bridge to formally protest the financing costs tied to their taxi medallions, the certificate that allows them to operate in the five boroughs. Tensions over “Medallion loans” have been bubbling over since last year when it was revealed that many borrowers had signed a Confession of Judgment to obtain their loan, which basically waived their right to settle any disputes with their lender in court should they be unable to make the payments. Since then, COVID has completely devastated an already suffering industry…

On Thursday, NYC taxi drivers shut down the Brooklyn Bridge to formally protest the financing costs tied to their taxi medallions, the certificate that allows them to operate in the five boroughs. Tensions over “Medallion loans” have been bubbling over since last year when it was revealed that many borrowers had signed a Confession of Judgment to obtain their loan, which basically waived their right to settle any disputes with their lender in court should they be unable to make the payments. Since then, COVID has completely devastated an already suffering industry…

“Before it was good, we could make $100-$150 a day,” said Mohammad Ashref, a local Brooklyn taxi driver in a video interview with deBanked reporter Johny Fernandez. “Now it’s very hard to survive, we work very hard to make 60, 70, or $80 a day, but what can I do? I have to make a living. We have no other choice.”

Ashref technically drives a green cab, different from the yellow cabs that were protesting on the bridge in that they’re not permitted to accept street-hails throughout most of Manhattan. Green taxis also operate through a permit rather than a medallion, a still relatively new concept that was first rolled out in 2013 to facilitate ride-hailing in the outer boroughs where yellow cabs did not spend much time.

Ashref technically drives a green cab, different from the yellow cabs that were protesting on the bridge in that they’re not permitted to accept street-hails throughout most of Manhattan. Green taxis also operate through a permit rather than a medallion, a still relatively new concept that was first rolled out in 2013 to facilitate ride-hailing in the outer boroughs where yellow cabs did not spend much time.

In the interview with Fernandez, Ashref pointed out that the success of the taxi business is intertwined with the restaurant industry. Many riders in the boroughs depend on cabs to take them to restaurants or night clubs, but with the complete ban on indoor dining still in effect within city limits, that need has mostly dried up.

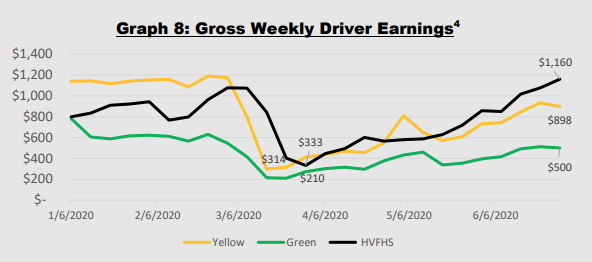

According to the NYC Taxi & Limousine Commission, yellow and green cabs were making as little as $314 and $210 a week respectively during the peak period of the shutdowns. In a 40 hour week, these amount to a fraction of the $15/hour local minimum wage and that’s even before factoring in driver costs like a vehicle lease, loan payments, insurance, and more.

deBanked has been exploring several areas of the New York City economy over the last few months. For instance in July, reporter Johny Fernandez looked into how the pandemic was affecting a street performer in Times Square that was dressed as Batman.

“The business now is slow,” Batman said. “There’s so few people at this moment […] At this moment I see people scared, they don’t want pictures…”

Batman, like others in New York City, was hopeful that a return to normalcy was just around the corner.