Following Nine Lawsuits, OnDeck Discloses Supplementary Details Behind Planned Enova Merger

After OnDeck announced its planned merger with Enova, it was sued nine different times (See here and here) by shareholders that accused the company’s Board of Directors that they had failed to disclose material information about the deal.

OnDeck formally responded on Monday, September 28th, wherein they disclosed that plaintiffs in all of those actions had agreed to dismiss their claims in light of the release of this supplemental information:

The Company and Enova believe that the claims asserted in the Actions are without merit and that no supplemental disclosures are required under applicable law. However, in an effort to put the claims that were or could have been asserted to rest, to avoid nuisance, minimize costs and avoid potential transaction delays, and without admitting any liability or wrongdoing, the Company has determined to voluntarily supplement the Proxy Statement/Prospectus as described in this Current Report on Form 8-K to address claims asserted in the Actions, and the plaintiffs in the Actions have agreed to voluntarily dismiss the Actions in light of, among other things, this supplemental disclosure. Nothing in this Current Report on Form 8-K shall be deemed an admission of the legal necessity or materiality of any of the disclosures set forth herein. To the contrary, the Company and the other defendants specifically deny all allegations in the Actions that any additional disclosure was or is required and expressly maintain that, to the extent applicable, they have complied with their respective legal obligations.

OnDeck first re-explained its background situation leading up to the Enova deal:

Starting in April 2020, OnDeck management commenced a review of potential financing options to secure additional liquidity and potentially replace the Corporate Line Facility and began contacting potential sources of alternative financing, including mezzanine debt. OnDeck contacted, or was contacted by, more than ten potential sources of mezzanine or alternative financing, and received pricing indications from four sources. The interest rates offered by those alternative financing sources ranged from 1-month LIBOR plus 900 basis points to 1,700 basis points (in addition to an upfront fee) and all but one required a significantly dilutive equity component. The one proposal that did not include an equity component was at an interest rate of 1-month LIBOR plus 1,400 basis points to 1,700 basis points. Based on the initial term sheets proposed, OnDeck engaged in negotiations with each of the four potential sources of alternative financing. As these negotiations progressed and COVID-19’s impact on the macro economy and OnDeck’s loan portfolio intensified, two of the four potential sources of alternative financing ceased to actively participate in negotiations. Discussions with the final two potential sources of alternative financing remained ongoing through the time that OnDeck and Enova entered into the merger agreement. Throughout the Process, OnDeck management reported the status of such negotiations on a frequent and ongoing basis to the OnDeck Board for its deliberation in the context of OnDeck’s standalone plan, and the OnDeck Board considered the significant uncertainty of being able to reach agreement on alternative financing in its decision to enter into the merger agreement.

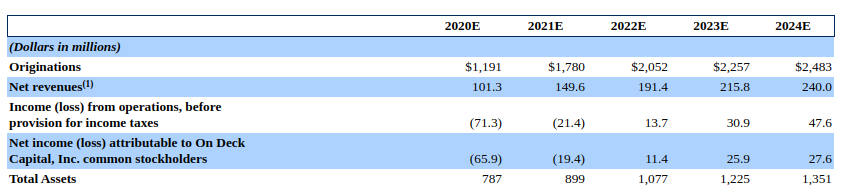

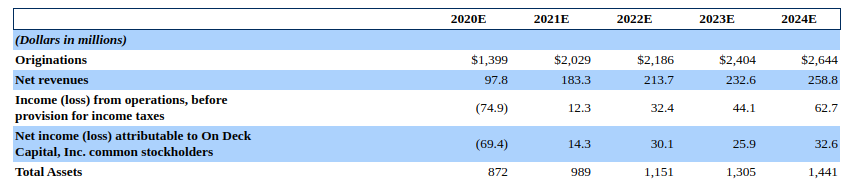

Of particular contention in the deal were OnDeck’s financial projections, prepared to estimate OnDeck’s trajectory as an independent entity. Shareholders complained that there were two sets of books and that they only got to see one. The other set, dubbed Scenario 1, had been used to shop OnDeck around to other suitors. OnDeck published both sets in their supplemental materials on Monday.

The difference is stark. Originally disclosed to shareholders was a projected cumulative net loss of $20.4 million through the end of 2024. The other set of projections, Scenario 1, state a cumulative net income of $33.5 million over the same time period, a difference of over $50 million.

The original predicted a 2021 net loss of $19.4 million while Scenario 1 predicted a net income of $14.3 million.

One reason offered for selecting the less optimistic of the two is that OnDeck’s management determined that loan originations were trending below both sets of projections as of July 12th. OnDeck announced the Enova deal about two weeks later.

Shareholders will cast their votes on the merger on October 7th. OnDeck’s Board “unanimously recommends” that they vote in favor of the proposed merger with Enova.

Last modified: September 29, 2020Sean Murray is the President and Chief Editor of deBanked and the founder of the Broker Fair Conference. Connect with me on LinkedIn or follow me on twitter. You can view all future deBanked events here.