Sean Murray is the President and Chief Editor of deBanked and the founder of the Broker Fair Conference. Connect with me on LinkedIn or follow me on twitter. You can view all future deBanked events here.

Articles by Sean Murray

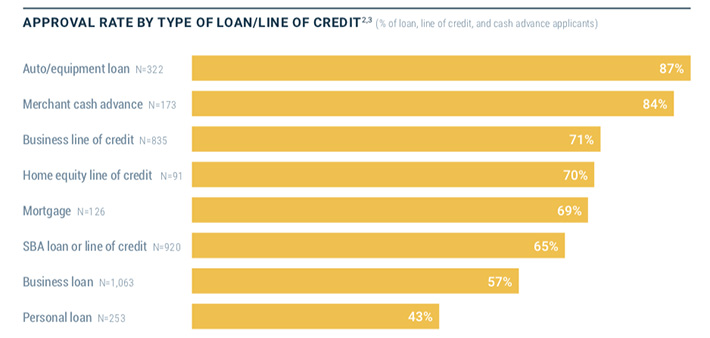

Merchant Cash Advance Approval Rate Was 84% in 2020, Federal Reserve Finds

February 3, 2021Eighty-four percent of applicants that applied for a merchant cash advance in 2020 were approved, according to the latest study published by the Federal Reserve. However, that figure includes the pre-March 2020 covid era.

When MCAs and online loans were blended, for example, the approval rate shrank from 81% pre-March 1st to 70% after March 1st.

Eight percent of all small businesses sought a merchant cash advance in 2020, down slightly from 9% in 2019. Leasing dropped from 9% to 7% and factoring dropped from 4% to 3%. Pursuit of credit cards even dropped, down from 29% to 21%.

There were some downsides for the online lending industry reported.

Only 9% of PPP applicants used an online lender.

Online lenders had the lowest satisfaction rate (43%) for small business credit needs. Credit unions scored the highest (87%).

Net satisfaction with online lenders dropped to its lowest level since 2016.

Small businesses satisfaction with big banks actually grew from 2019 to 2020.

Small businesses were less likely to apply for a business loan or MCA from an online lender in 2020 and more likely to apply for them at a bank in 2020 than they were in 2019.

Eighty-two percent of businesses applied for a PPP loan. Forty-seven percent applied for an EIDL loan.

Banks, perhaps counterintuitively, were the big winners in 2020. That trend could increase as banks and online lenders become the same thing.

Official Who Wants to “Wipe Out” Merchant Cash Advance Will Be Next CFPB Head

January 18, 2021 Rohit Chopra, an FTC Commissioner, will take over as head of the Consumer Financial Protection Bureau under incoming President Joe Biden, sources say.

Rohit Chopra, an FTC Commissioner, will take over as head of the Consumer Financial Protection Bureau under incoming President Joe Biden, sources say.

Chopra’s name made the rounds in 2020 when he told NBC News that he was looking for a “systemic solution” that can “wipe out” all merchant cash advance companies.

His candid comments aligned with an official statement he put out in August in which he opined that the structure of MCAs “may be a sham since many of these products require fixed daily payments…”

He further added that there were “serious questions as to whether these merchant cash advance products are actually closed-end installment loans, subject to federal and state protections including anti-discrimination laws, such as the Equal Credit Opportunity Act, and usury caps.”

His transfer to the CFPB could be viewed as unwelcome news for the MCA industry as the agency is currently in the process of finalizing the types of financial institutions it believes it should maintain some jurisdiction over. Originally, MCA companies were poised to be excluded from the data reporting requirement set forth by Section 1071 of Dodd-Frank but that could very well soon change.

Greenbox Capital Comments on Landmark Florida Legal Victory

January 7, 2021 Greenbox Capital was the victor of a major lawsuit argued before Florida’s Third District Court of Appeal that conclusively established the legality of merchant cash advances in the state.

Greenbox Capital was the victor of a major lawsuit argued before Florida’s Third District Court of Appeal that conclusively established the legality of merchant cash advances in the state.

When asked for comment, Greenbox Capital® CEO Jordan Fein said:

“It’s been a long, arduous, and expensive battle over the last few years proving in a court of law that a Merchant Cash Advance is not a loan. Today, we celebrate a win for all Merchant Cash Advance companies in Florida and the entire United States who are dedicated to funding small businesses through ethical practices. Our hard work and commitment to helping small businesses grow was validated and we are thrilled with the final decision of the District Court of Appeal.”

The decision in Florida echoes a similiar opinion reached in New York in 2018.

It’s Official, Merchant Cash Advances Not Usurious in Florida

January 6, 2021 Big news in the State of Florida. The Third District Court of Appeal entered its order on January 6th to decide the fate of Craton Entertainment, LLC, et al., v Merchant Capital Group, LLC, et al..

Big news in the State of Florida. The Third District Court of Appeal entered its order on January 6th to decide the fate of Craton Entertainment, LLC, et al., v Merchant Capital Group, LLC, et al..

Merchant Capital Group, LLC dba Greenbox Capital sued Craton in December 2016 over a default in a Purchase and Sale of Future Receivables transaction. In turn, Craton responded with various defenses and counterclaims that asserted the underlying transaction was really an unenforceable usurious loan.

The Circuit Court for Miami-Dade County sided with Greenbox in August 2019. The defendants appealed.

The District Court of Appeal decided the matter conclusively on January 6, holding that the original ruling was affirmed on the basis that:

- The transaction is not indicative of a loan where repayment obligation is not absolute but rather contingent or dependent upon the success of the underlying venture

- that the transactions in which a portion of the investment is at speculative risk are excluded from the usury statutes

- when the principal sum lent or any part of it is placed in hazard, the lender may lawfully require, in return for the risk, as large a sum as may be reasonable, provided it is done in good faith.

The decision can be viewed here.

The lawyers representing Appellee Greenbox Capital were Henderson, Franklin, Starnes & Holt, P.A., William Boltrek III, Shannon M. Puopolo and Douglas B. Szabo.

You should contact an attorney to discuss the implications of this ruling. Merchant Cash Advance contracts are not all the same.

This ruling is similar to a ruling in New York that was made in 2018.

A Half-Million Dollar Ad on deBanked

January 4, 2021 In early 2015, deBanked signed up a customer that was interested in paying with Bitcoin. So we priced it out and we agreed that about one month of advertising on our website combined with an ad in a single magazine issue would cost about 14 bitcoins.

In early 2015, deBanked signed up a customer that was interested in paying with Bitcoin. So we priced it out and we agreed that about one month of advertising on our website combined with an ad in a single magazine issue would cost about 14 bitcoins.

I submitted an invoice via Coinbase and they paid. Pretty soon thereafter, we sold the bitcoins for cash. I thought nothing of it because I’ve never seen Bitcoin as an investment.

We continued to do other advertising deals in Bitcoin in which the contracts were priced in Bitcoin instead of dollars but that was the largest single Bitcoin transaction we ever did. I’ve also done things like pay for hotel rooms for industry conferences in Bitcoin, because you know…that’s how I roll.

As you probably heard over the New Year’s weekend, the price of bitcoin shot up to $34,000. It got me thinking about how I failed to become a Bitcoin millionaire years earlier, but now with this incredible new high, it reminded me of that one deal in particular

Fourteen bitcoins in 2021 is worth approximately $476,000. Almost a half million dollars. That was for just 1 month of advertising on deBanked.

I guess I should’ve held on to them.

Happy New Year.

deBanked’s Top Five Stories of 2020

December 28, 2020DeBanked’s Top 10 most read stories of 2020 all involved the Payment Protection Program (PPP). It was by far the hottest topic in small business financial services for the year. As a result, we consolidated our most read stories into FIVE categories and this is what our readers consumed most in 2020!

1. PPP

The Payroll Protection Program saga boiled down to one major question early on in the pandemic: Who, if anybody, would be able to lend the money out on the government’s behalf? PPP Lender Requirements was the most read story on deBanked in 2020, followed by the world being curious to find out who was the biggest PPP lender. On April 22, deBanked was the first to spread the story that Ready Capital (Knight Capital‘s parent company) was the largest PPP lender in the US for Round 1.

The Payroll Protection Program saga boiled down to one major question early on in the pandemic: Who, if anybody, would be able to lend the money out on the government’s behalf? PPP Lender Requirements was the most read story on deBanked in 2020, followed by the world being curious to find out who was the biggest PPP lender. On April 22, deBanked was the first to spread the story that Ready Capital (Knight Capital‘s parent company) was the largest PPP lender in the US for Round 1.

2. NY’s Disclosure Bill

The biggest non-PPP story of the year was a bill passed in New York that was signed by the governor at Midnight on Christmas Eve. SB 5470, which some have dubbed “The Small Business Truth in Lending Act,” is slated to completely overhaul the non-bank small business lending market in the state. The bill was passed by the legislature in July.

The biggest non-PPP story of the year was a bill passed in New York that was signed by the governor at Midnight on Christmas Eve. SB 5470, which some have dubbed “The Small Business Truth in Lending Act,” is slated to completely overhaul the non-bank small business lending market in the state. The bill was passed by the legislature in July.

3. OnDeck

It’s difficult to overstate how much of a rollercoaster it was for the stalwart fintech lender in 2020. OnDeck started the year with optimism, announcing a NASCAR sponsorship in March just as the company’s stock suddenly plummeted by 30%. By the time summer rolled around, the company was no longer engaged in non-PPP lending activities and was battling in a fight for its life with its creditors. In July, OnDeck was acquired by Enova, which led to shareholder lawsuits over the terms and disclosures tied to the deal. Somehow, by year-end, OnDeck managed to pull itself back together, thanks to its new parent company. It successfully originated $148M worth of loans in Q3.

It’s difficult to overstate how much of a rollercoaster it was for the stalwart fintech lender in 2020. OnDeck started the year with optimism, announcing a NASCAR sponsorship in March just as the company’s stock suddenly plummeted by 30%. By the time summer rolled around, the company was no longer engaged in non-PPP lending activities and was battling in a fight for its life with its creditors. In July, OnDeck was acquired by Enova, which led to shareholder lawsuits over the terms and disclosures tied to the deal. Somehow, by year-end, OnDeck managed to pull itself back together, thanks to its new parent company. It successfully originated $148M worth of loans in Q3.

Wow, just wow.

4. Covid-19

The impact of Covid was a close 4th on deBanked’s top read list. In March, deBanked published a writeup of How Small Business Funders [Were] Reacting, an interesting glimpse into the pandemic as it was just unfolding. At that time, attitudes ranged from confidence in being prepared to being convinced it was time to shut everything down. One notable takeaway from the commentary is that nobody surmised that the situation would persist for the entire rest of the year.

The impact of Covid was a close 4th on deBanked’s top read list. In March, deBanked published a writeup of How Small Business Funders [Were] Reacting, an interesting glimpse into the pandemic as it was just unfolding. At that time, attitudes ranged from confidence in being prepared to being convinced it was time to shut everything down. One notable takeaway from the commentary is that nobody surmised that the situation would persist for the entire rest of the year.

Capify CEO David Goldin made an early bold prediction, however. “I would not be surprised if we learn in the next few weeks that the President of the United States has it,” he said in an interview with deBanked in mid-March. President Trump was diagnosed with Covid-19 less than six months later on October 6th.

5. Scandal

Three scandals were a near-tie for views in 2020 so we’re revisiting them all here.

Three scandals were a near-tie for views in 2020 so we’re revisiting them all here.

Brendan Ross & Direct Lending Investments – Brendan Ross, the former CEO of a very popular fintech lending hedge fund, was indicted on August 11th. Federal officials including the SEC, say that Ross defrauded investors while managing more than $1 billion in assets. Ross’s “unwinding” began in 2019 when he suddenly resigned from the firm and wrongdoing was alleged.

Jonathan Braun – Jon Braun, made infamous by a Bloomberg Businessweek profile, checked into FCI Otisville earlier this year after having been sentenced the previous May for drug related offenses. Braun resurfaced in the news this summer when the FTC announced civil charges against him for alleged acts related to a company named Richmond Capital Group, LLC. The New York State Attorney General filed its own charges against Braun and affiliates at the same time.

Par Funding – A financial services firm based in Philadelphia generated major headlines this year after the SEC filed a lawsuit against the company that ultimately resulted in it being placed in receivership. A series of stunts and accidents got the SEC’s case off to a rocky start, but the likelihood of Par ever restarting its business has diminished to almost nothing.

Ho Ho… Hold Up. NY Governor Signs Industry-Altering Small Business Lending Law

December 24, 2020 Merrrrry Christmas. New York Governor Andrew Cuomo reportedly signed SB 5470 into law late last night, a bill that forever changes and complicates nearly all forms of small business financing in the state.

Merrrrry Christmas. New York Governor Andrew Cuomo reportedly signed SB 5470 into law late last night, a bill that forever changes and complicates nearly all forms of small business financing in the state.

The law gives regulatory enforcement authority to New York’s Department of Financial Services, requires APR disclosures on contracts where one can’t be mathematically calculated, and mandates that customers be told if there is any “double dipping” going on. And that’s just the beginning of what it contains.

A coalition of small business capital providers fiercely opposed the language of the bill. Steve Denis, executive director of the Small Business Finance Association, wrote in an op-ed that “the lack of cogency and lazy approach to this legislation is a disservice to the hard-working entrepreneurs who continue to open their businesses while facing daily economic uncertainty.”

The bill was also opposed by fintech lenders like PayPal.

Proponents of the bill celebrated the news on social media in the early morning hours of Christmas Eve.

Ryan Metcalf at Funding Circle, a company not even based in New York that moved all of its tech jobs out of the US to the UK this summer, wrote on LinkedIn that the bill will “save New York #smallbiz between $369 million and $1.75 billion annually.” Funding Circle, as a member of the Responsible Business Lending Coalition (RBLC), was heavily engaged in the advocacy process.

Several of RBLC’s members have already ceased small business lending in the US, some permanently.

Unique circumstances also exist at an ally of the RBLC, the Innovative Lending Platform Association (ILPA), which Funding Circle is also a member of. Two out of the 11 members were acquired before the bill could even be signed, Kabbage and OnDeck.

NY State Assemblyman Ken Zebrowski and State Senator Kevin Thomas, who sponsored the bill, cheered the signing of it.

“Thanks to Governor Cuomo for signing our Small Business Truth in Lending Act,” Zebrowski tweeted. “Extremely proud to have worked with many to establish the most comprehensive small business disclosure law in the nation. With the pandemic surging on, small biz owners need these critical protections now.”

“The signing of the New York State Small Business Truth in Lending Act is a victory for New York’s small business owners,” Thomas wrote on twitter. “Thank you for signing New York’s first-ever small business lending transparency bill into law.”

“I think that the companies and organizations that support this legislation don’t fully understand what’s actually in the bill,” SBFA’s Steve Denis said to deBanked in August. “[…] They have no problem pounding the table and taking credit for its passage, but I guess they don’t realize it will subject them and the rest of the alternative finance industry to massive liability, massive fines—upwards of billions of dollars worth of fines.”

And yet Senator Thomas tweeted, “This will help a lot of small businesses trying to get back on their feet during this pandemic.”

It is unclear, of course, who they expect to provide such capital now to do this.

How Much Fintech News Are You Consuming On The Internet?

December 22, 2020LendIt Fintech distributed a marketing flyer via email yesterday to its subscribers and it got us thinking about how much online fintech news people are consuming, especially in this era of 2020.

LendIt reported 65,000+ monthly page views for its LendIt Fintech News and that it had 800,000+ podcast downloads.

Meanwhile, deBanked and DailyFunder combined are recording 311,000+ in average monthly page views. Visitors are also spending 7,300 hours on our sites combined each month on average.

These figures are enormous. Thanks for reading!