Sean Murray is the President and Chief Editor of deBanked and the founder of the Broker Fair Conference. Connect with me on LinkedIn or follow me on twitter. You can view all future deBanked events here.

Articles by Sean Murray

Should Small Business Lenders Weigh Risk of Applicants Getting Prosecuted for PPP Fraud?

July 23, 2021 As law enforcement officers and prosecutors gradually move on from fake businesses that got PPP in favor of real ones that lied to get more PPP funds than they should have, non-PPP loan underwriters may be forced to grapple with a new question: Is the merchant at risk of PPP fraud prosecution?

As law enforcement officers and prosecutors gradually move on from fake businesses that got PPP in favor of real ones that lied to get more PPP funds than they should have, non-PPP loan underwriters may be forced to grapple with a new question: Is the merchant at risk of PPP fraud prosecution?

Alarm bells have already been sounded by Experian for a different reason, one that warned commercial fintech lenders that the mere receipt of PPP funds should not be considered enough to confer legitimacy on a loan applicant.

But what if everything checks out and the business is legitimate? PPP could come back to adversely affect the performance of the loan if the applicant is later prosecuted or forced to give back all or a portion of the PPP funds. A recent roundup by the Department of Justice, for example, resulted in 22 individuals being charged for PPP related fraud. More than a dozen actual businesses were ensnared by it, with the litany of charges including things “false statements to a federally insured financial institution.”

If a business misappropriated the funds, lied to get more than they should have, lied about when the business was founded, or engaged in some other kind of misleading impropriety, that business could be a ticking time bomb for lenders.

Proactive underwriters or fintech technology could assess whether or not the PPP funds obtained by an applicant were financially realistic and that the business start date aligned with PPP requirements. A business doing $20,000 a month in sales that obtained $200,000 in PPP funds, for example, may look sustainably healthy but raise a red flag that it may not have been legitimately obtained. Underwriters should be crunching the numbers and thinking about whether or not this applicant is likely to face consequences and what that might mean for the loan if it’s approved.

This editorial is the opinion of the author.

Fraudsters May Leverage Their PPP Approvals to Get Business Loans and MCAs

July 21, 2021 A small business finance underwriter torn between approving or declining an applicant probably should not consider whether or not that business got PPP funding as evidence of the applicant’s legitimacy.

A small business finance underwriter torn between approving or declining an applicant probably should not consider whether or not that business got PPP funding as evidence of the applicant’s legitimacy.

A new alert put forth by Experian claims that “greater than 75% of PPP loans originated by commercial fintech lenders were NOT run through a fraud screening and have a greater probability of containing bad actors.” Experian says that “lenders will need to be more vigilant as they assess these businesses for future offers of credit.”

Experian cites data from the FTC that shows fraud and identify theft have surged since the pandemic started, climbing to even higher levels in 2021 over 2020.

Fraudsters that successfully obtained PPP loans with altered documents, for fake businesses, or on behalf of real businesses using stolen identities, may now use those as leverage to obtain additional money, particularly through sources where the perceived consequences of being found out are low. Non-bank funders and fintech lenders are an attractive target.

Just because an applicant got a PPP loan, underwriters should not assume it has passed a fraud check.

NYC is Back, So is it Time to Buy Here?

July 12, 2021Now that New York City is back, opportunity abounds to move in or make money off the dynamic real estate market. You might be able to get in on it even if you’re a first time investor. To size up the market and the common questions to consider, we spoke one on one with Erin Sykes, the Chief Economist of Nest Seekers International.

You can also watch it here on deBanked TV.

Watch More from deBanked’s Real Estate Investing Docuseries Here.

LendUp Stops Making New Loans

July 10, 2021 LendUp, a fintech lender that hoped to disrupt the payday loan industry, is no longer making new loans. A note posted on its website said “We are currently not offering loans to new customers.”

LendUp, a fintech lender that hoped to disrupt the payday loan industry, is no longer making new loans. A note posted on its website said “We are currently not offering loans to new customers.”

When deBanked sat down with the now former CEO Sasha Orloff in 2017, he said that their product was simply cheaper and more flexible.

“The easiest person to convince that we’re a better product is an existing payday user because it’s slightly cheaper at the beginning, it gets much cheaper over time,” he said then. “It has a lot more flexibility.”

But for all the bells and whistles, their still relatively high rates generated a target on their back with regulators.

In 2016, for example, the CFPB said “[LendUp] did not give consumers the opportunity to build credit and provide access to cheaper loans, as it claimed to consumers it would.”

Balancing the messaging with the reality seemd a difficult task.

Orloff stepped down in January 2019, but in less than two years the CFPB took a second crack at LendUp for allegedly violating the Military Lending Act.

In January of this year, LendUp settled the charges, agreeing to pay $300,000 in redress to consumers and to pay a $950,000 civil money penalty.

As recently as April, LendUp’s website was still offering loans with a promoted APR of 400%.

On The Scene With KEO in Miami

July 8, 2021Farid Shidfar is Head of US Operations at KEO, a small business finance company based in Midtown Miami. I sat down with Shidfar to ask about KEO’s recent foray into the market, what they’re seeing on the front lines, and their plans for the future. Our one-on-one interview is below:

Snapchat Acquired Mobile Shopping App Founded By Former MCA Execs

July 2, 2021 A brother and sister team formerly known throughout the merchant cash advance industry have achieved major success in another market altogether, mobile shopping.

A brother and sister team formerly known throughout the merchant cash advance industry have achieved major success in another market altogether, mobile shopping.

Recently, their app was acquired by Snapchat, according to various news outlets, and the tech has since been integrated into the Snapchat app.

Molly and Meir Hurwitz, both original stalwarts of the old Pearl Capital in New York, co-founded Screenshop in 2017, an app that integrated shopping with fashion and social media. Its initial launch received added buzz thanks to Kim Kardashian’s early involvement as an advisor. Notably, Screenshop CEO Mark Fishman was previously a Risk Manager at Pearl Capital, rounding out the former MCA crew.

“We’re No. 5 on the app store category of fashion,” Meir Hurwitz told deBanked in November 2017. “We’re just getting started.”

The success continued.

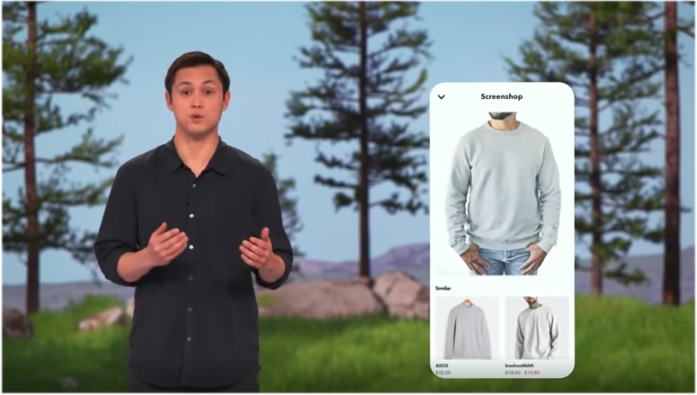

“Screenshop gives shopping recommendations from hundreds of brands when you Scan a friend’s outfit,” Snapchat wrote in a published announcement this past May.

More than 170 million Snapchatters use scan features every month, the company revealed.

“Screenshop is now a part of ‘Scan’ said Snapchat CTO Bobby Murphy during the company’s annual Partner Summit broadcast on May 20. The above screenshot is of Murphy demonstrating the Screenshop technology.

Congress Tells OCC “Nope” On True Lender Rule

June 29, 2021 In October, the OCC brought clarity to the relationships that many fintech companies enjoy with banks.

In October, the OCC brought clarity to the relationships that many fintech companies enjoy with banks.

So long as a national bank is named as the lender on the loan agreement on the date of origination or so long as it funds the loan, then the bank is considered the true lender, the OCC decided. It issued it as a rule that was published in the Federal Register last year.

The brief proclamation was viewed as necessary in light of lawsuits filed against fintech companies that have challenged who the true lender was on a loan.

National banks are generally exempt from state interest rate caps and licensing requirements. Fintech lenders, therefore, partner up with banks in such a way that the banks themselves actually make the loans so that those same exemptions carry over. The long-used practice has drawn litigation as well as outrage from certain corners of the economic and political spectrum. The OCC rule issued during the Trump era, for example, was not unanimously applauded.

Last week, Congress took the unusual step of nullifying the OCC’s rule.

Resolved by the Senate and House of Representatives of the United States of America in Congress assembled, That Congress disapproves the rule submitted by the Office of the Comptroller of Currency relating to “National Banks and Federal Savings Associations as Lenders” (85 Fed. Reg. 68742 (October 30, 2020)), and such rule shall have no force or effect.

Short and succinct.

The invalidation of the OCC rule does not mean that banks cannot collaborate with fintechs or third parties in such a way as before, but rather that the certainty of what’s acceptable and what isn’t will be relegated to further debate for years to come.

Tether is Now So Big, Its Collapse Could Disrupt the Short-Term Credit Markets

June 26, 2021 More than $62.5 billion worth of Tethers have been printed in the last few years to facilitate liquidity in the crypto markets. The system has worked because the company behind Tether had long claimed that each unit of the digital currency was backed somewhere by a real dollar in a bank account.

More than $62.5 billion worth of Tethers have been printed in the last few years to facilitate liquidity in the crypto markets. The system has worked because the company behind Tether had long claimed that each unit of the digital currency was backed somewhere by a real dollar in a bank account.

That was determined false. “Tether’s claims that its virtual currency was fully backed by U.S. dollars at all times was a lie,” wrote the New York State Attorney General in February after the regulator announced a settlement with the company. “These companies obscured the true risk investors faced and were operated by unlicensed and unregulated individuals and entities dealing in the darkest corners of the financial system.”

Despite the characterization, Tether has continued to be the glue that makes the global crypto market hum. And their size is now so big, that it’s no longer just a crypto problem.

According to the Federal Reserve Bank of Boston, Tether now poses a risk to all short-term credit markets. The central bank listed it as an example of “new disruptors” that pose financial stability challenges.

Eric S. Rosengren, the CEO of the Boston Fed, said “There are many reasons to think that stable coins, at least many of the stable coins are not actually particularly stable and actually have some of the same features as money market funds. The difference is prime money market funds have been losing market share but these stable coins have been growing very rapidly in part because of their use along with the cryptocurrency market.”

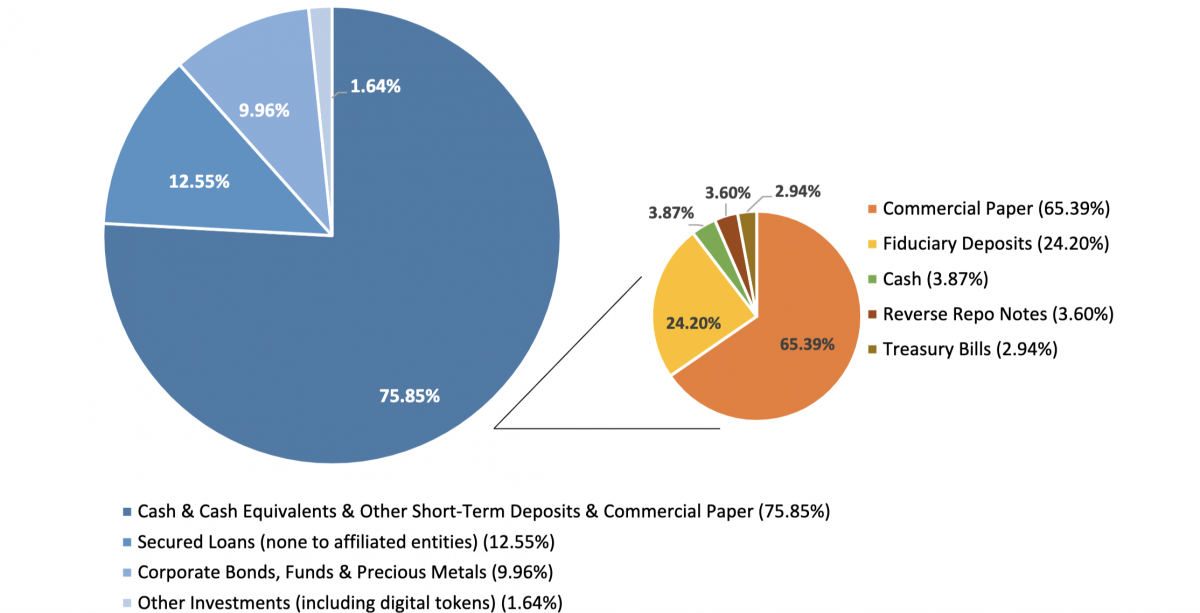

On Tether in particular, he said, “While [Tether talks] about being stable, if you look at the set of assets that are there, it includes corporate bonds, secured loans, commercial paper, in effect this is a very risky prime fund. Prime funds would not be able to hold all these assets.”

Tether has drawn enhanced public scrutiny in recent months after releasing the following breakdown of its assets. The digital asset company that once claimed all Tethers were backed by dollars, revealed that less than 3% of them were actually backed by dollars.

Tether’s riskiness was also the subject of a recent segment on Jim Cramer’s Mad Money show on CNBC:

deBanked first shed light on the Tether mystery more than two years ago in a story that questioned what drove the cryptocurrency bull market of 2017.