|  |  |

Related Headlines

| 03/01/2022 | New Mexico signs rate cap bill into law |

| 03/09/2021 | Fintech law goes into effect in Mexico |

| 02/01/2020 | Mexico's AlphaCredit raises $125M |

| 02/27/2019 | PayPal to do small biz loans in Mexico |

| 10/09/2017 | SMB lending in Mexico gets a boost |

Stories

Fintech Law Goes into Effect in Mexico

March 9, 2021 It will be a big year for fintech in Mexico, with at least 93 fintech firms in the process of obtaining a Financial Technology Institution (FTI) license.

It will be a big year for fintech in Mexico, with at least 93 fintech firms in the process of obtaining a Financial Technology Institution (FTI) license.

Lawyer Rene Arce Lozano, an advisor with the international Hogan Lovells law firm, wrote about the new “fintech law”; the first of its kind in Latin America. Many firms will see an authorization in the coming year from the National Banking and Securities Commission.

“Over the last few years,” Lozano wrote, “the fintech ecosystem in Mexico has evolved to become one of the most developed in Latin America.”

Mexico, home to 441 startups- the largest fintech hub in central America- passed the law in 2018 that went into effect this past year 2020, nurturing the creation of dozens of Mexican neo banks and electronic payments firms.

The new law sets regulations for payments and open banking and has stirred up excitement for fintech enterprise in the country as a whole. But according to Financial specialist Stefan Staschen, the law isn’t the cure-all.

“The law covers only two types of fintech companies,” Stashen wrote. “It does not provide regulatory guidance for other services, such as fintechs offering balance sheet lending, big tech companies launching financial services, investment services other than crowdfunding, or central bank digital currencies.”

The new law may be a great start, but it is the first step to broader regulatory approval to the diverse financial tech world. Staschen works at the CGAP– an international advocacy group based in Washington that aims to extend financial inclusion throughout the world.

New Mexico Bill Would Allow State Employees to Repay Loans Via Paychecks

January 15, 2018 Proposed legislation would enable New Mexico to offer small loans to state employees that are paid back via deductions from their paychecks.

Proposed legislation would enable New Mexico to offer small loans to state employees that are paid back via deductions from their paychecks.

Put forth by Democratic state Senator Bill Tallman, the bill would put a 30 percent ceiling on interest rates for loans obtained via the program and limit repayment to 12 percent of gross salary or wages.

According to the Associated Press, Tallman says the bill is aimed at lowering debt burdens on state workers.

Should it pass, Tallman’s initiative would serve as another step for the state in its current battle against predatory lending tactics. As of this month, small lenders in New Mexico are held to a maximum of 175 percent interest on all loans finalized from January 1, onward.

Doug Farry, executive vice president of Employee Loan Solutions Inc., which deploys the employee lending service, True Connect, believes such a strategy can prove successful at the state level.

“It’s a benefit program,” said Farry while discussing the bill. “There’s no reason why it can’t work for a state government as well as a county or city.”

Aimed at empowering workers that face obstacles when applying for credit via traditional avenues, True Connect mainly serves private employers but has seen increased interest in the public sector. This includes government organizations such as Santa Fe Public Schools and others within the state of New Mexico.

At no cost to their participating employer and without submitting a credit score, workers can sign up for small loans via the company’s website.

Typically the funds are deposited with in one business day, and the loan is repaid over the course of 26 paychecks at a flat rate of 24.9% interest.

New Mexico’s decision regarding the practice is yet to be determined, but should the bill pass, the state may soon have followers.

Farry says that True Connect is currently in talks with multiple state governments about including a similar system in their benefits package.

Business Lending in Mexico – From the Front Lines

January 20, 2016It’s no secret that the financial technology (FinTech) industry has exploded and its effects are being felt around the world. With its epicenter in the US (arguably the UK), it quickly caught on in other major markets like Europe, Australia and Canada. The main narrative for the FinTech industry plays as follows: First, a huge local market has incumbents (local banks), which make it hard for the local population to move or obtain capital (payments and loans, respectively). Then, a bunch of clever people arm themselves with tech, tools and capital to come up with a better solution than the incumbents in their markets; and as people in the US are looking west, east and north to see how this tune plays out in different markets, I have seen how the FinTech phenomenon is growing strongly down south, here, in Mexico.

Mexico’s FinTech market is made up of the same parts as in the rest of the world. It has huge potential, but surprisingly only few people know about it. With roughly a third of the population of the US (123 million people), and an economic value similar to that of Australia and Canada, Mexico´s local market is in dire need of financial services. In our company’s market, domestic credit represents a meager 31% of GDP[1]! It’s 69% in Brazil by contrast. The USA has a startling 194%. This means that the Mexican private sector is not receiving enough capital in the form of financial products from local financial institutions. The same phenomenon exists in the payments space. For example, in the point of sale (POS) industry, there are currently 8 POS per 1,000 people in Mexico. The US has more than double that at 21 POS per 1,000 people, and Brazil has 3x at 24 POS per 1,000!

Regarding the incumbents, the banks, Mexico is known as the land of monopolies. While in the US there are literally thousands of banks, in Mexico, there are just over 40 banks, with the top 20% holding close to 80% of the market and its profits. Furthermore, Citibank’s and BBVA´s Mexican operations are some of their most profitable worldwide. Large banks like these enjoy extraordinary profits, and have been slow to adapt to new technological trends, service niche markets and provide services which could cannibalize bank revenues. After all, why would a monopoly innovate if it holds most of the market in its hands?

And then there are the people trying to solve this problem. Many Mexicans travel to study in the world´s top graduate programs and return to Mexico to act on what they learned. Domestically, Mexico churns out 3 times as many engineers per capita than US universities do. So currently there is a boom in the number of start-ups in Mexico[2]. And as start-ups tend to do, they are targeting one of the largest and hairiest problems this country has to offer: Financial Services. As a result, the likes of “500 Startups”, “Tech Stars”, “Village Capital” and “Y-Combinator”, and several Silicon Valley VC funds have turned their attention south. Several Mexican start-ups have been raising increasingly larger rounds from local and US investors to quickly tackle the opportunities in the loans and payments spaces.

These Mexican companies are developing solutions for the national problems and they know how to do it with the local culture in mind. Even though the US and Mexico share one of the longest borders and a huge migrant flow, they have developed at different speeds, which present different challenges. Two examples of this divergence: The FICO credit score, created in 1970s in the US, barely made its way down to Mexico some 4 years ago. However in terms of regulation, Mexican banks have been quicker to meet regulatory compliance (Basel I/II) than most of their US counterparts[3]. So the new players up to bat here at home, the online lenders, merchant lenders, mobile POS, remittances, bitcoin exchanges, peer-to-peer market places and the like, are raising capital both locally and abroad to create the technology to service the large Mexican financial services market. And in many cases, they are trying to get the formula right to create a beachhead to jump into a larger and broader international Latino market.

—

Footnotes

[1] – In other words, how much capital is being provided by all the private financial institutions in the country to all the private interests (consumers and companies) in comparison to the GDP. A lower number means that the private sector is not providing enough capital to match the countries production. A higher means the private sector is matching or exceeding the capital needs of the private interests.

[2] – A few months ago “The Economist” made a small homage on the Mexican start up scene – http://www.economist.com/news/business/21647624-nascent-tech-hub-may-succeed-solving-local-problems-techs-mex

[3] – The high compliance of the Mexican Banks has been a byproduct of the boom and bust cycle that the country has had. So more than a voluntarily action, the central bank forced the local players to meet the international requirements.

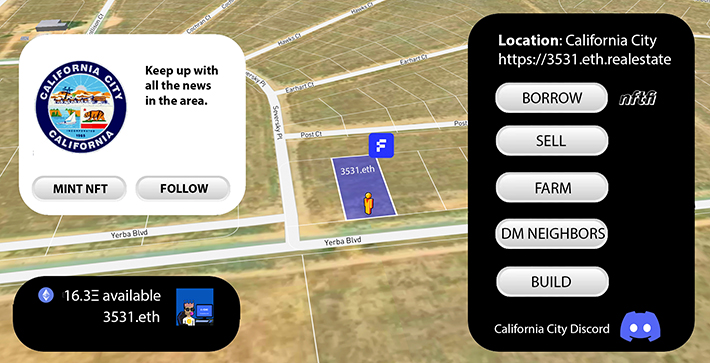

Forget the Metaverse, I Bought Real Land

February 20, 2024 In 1958, developers purchased 82,000 acres of barren land that was situated a hundred miles north of Los Angeles with a plan to build a sprawling metropolis for 400,000 future residents. As it instantly became the third largest city in California by land area, they chose an appropriately symbolic name, California City. It was a flop from the start. Although powerful marketing led to the sale of 50,000 lots by the early 1970s, the city only had a population of 1,300 people by 1969. That was bad enough that the Federal Trade Commission intervened in 1972 and forced a settlement that allowed thousands of landowners to get refunds. California City held on, however, and it’s now home to nearly 15,000 residents. It even has its own airport. But still, what it has become is still remarkably short of the original vision.

In 1958, developers purchased 82,000 acres of barren land that was situated a hundred miles north of Los Angeles with a plan to build a sprawling metropolis for 400,000 future residents. As it instantly became the third largest city in California by land area, they chose an appropriately symbolic name, California City. It was a flop from the start. Although powerful marketing led to the sale of 50,000 lots by the early 1970s, the city only had a population of 1,300 people by 1969. That was bad enough that the Federal Trade Commission intervened in 1972 and forced a settlement that allowed thousands of landowners to get refunds. California City held on, however, and it’s now home to nearly 15,000 residents. It even has its own airport. But still, what it has become is still remarkably short of the original vision.

All of this history was something I breezed through right before I impulsively clicked a button on my screen asking me to confirm my purchase for a lot there. One click. That’s apparently all it took to become the newest member of a potential future neighborhood in California City, one that might not ever come to fruition. But how I found it in the first place is the real story. It appears that in the modern era this sleepy desert outpost has become a bit of an experimental laboratory for something relatively new in the real estate world, converting properties into NFTs.

Here’s how it’s done. A landowner places their property into an individual trust and ownership of that trust is governed by whomever owns the corresponding NFT on Ethereum. In effect, the owner of the trust would be defined by their ugly hex address, like this one for example: 0x64233eAa064ef0d54ff1A963933D0D2d46ab5829. It’s actually quite basic and it’s all made possible by a “proptech” company called Fabrica.

Here’s how it’s done. A landowner places their property into an individual trust and ownership of that trust is governed by whomever owns the corresponding NFT on Ethereum. In effect, the owner of the trust would be defined by their ugly hex address, like this one for example: 0x64233eAa064ef0d54ff1A963933D0D2d46ab5829. It’s actually quite basic and it’s all made possible by a “proptech” company called Fabrica.

Founded in 2018 and backed by investors like Mark Cuban and Zain Jaffer, properties tokenized by Fabrica “can be traded instantly, used as collateral and are compatible with all NFT platforms,” the company states. “The product automates sales transactions, facilitating title transfer, payments and regulatory compliance.” Fabrica facilitates the on-ramping of your land into an NFT and even provides its own marketplace for buyers and sellers. That’s where I got mine. Interested parties can read up on a property’s on-chain history and even check the title. There’s also a cool little Google Earth-like animation that flies the user to their specific plot of land. The experience feels a lot like buying a plot of virtual land in a video game or the metaverse except this land is real. That means that sleek little NFT in your digital wallet comes with real responsibilities like property taxes, which Fabrica works to keep the owner informed about. It also means any and all liabilities of property ownership. The upside is that you can go and visit it in real life and even develop it. You can’t do that in a video game.

Although I’ve counted six properties in California City that are immediately identifiable as NFTs, it’s hardly the only place in the United States where this is being done. Properties available for sale as NFTs as of this writing include locations across Colorado, Arizona, New Mexico, San Bernardino-CA, and even Orange, New York. Some are very remote and speculative, while others are a part of normal civilization and priced accordingly. Buyer beware of course given the serious nature of these assets.

Perhaps one of the biggest obstacles to understanding how this is all possible is the widespread misconception of what NFTs are. Most of the American population lives under the mistaken impression that NFTs are cartoon art pictures like Bored Apes or CryptoPunks that were all the rage in 2021 and to some extent are still popular in niche circles, but almost anything can be tokenized. More recently, for example, domain names are being converted into NFTs to facilitate faster sales and quicker payouts. The same is true now here with land. Not only can land ownership change hands in the blink of an eye by transferring the NFT but one can also easily tap into the value by pledging it on a peer-to-peer NFT loan marketplace like NFTfi. Fabrica officially announced a partnership with NFTfi this past December, for example. The possibilities are endless

For the perpetual skeptics of all things blockchain that are convinced real business will only ever be done in the real world, a visualization of an NFT on a crypto wallet app might not be all that convincing, especially if the icon for it is situated right next to one of those expensive monkey pictures that kids wouldn’t shut up about years ago. The proof then is in the adventure. With a drive of less than two hours from Downtown Los Angeles, there’s a little plot of land on a quiet street known as Yerba Boulevard. It’s covered in weeds and reddish soil. Empty plains make up most of the backdrop but the suburbs are very slowly creeping their way there. In fact, I’ve since learned who my neighbor is across the street. It’s a 26,000 square foot cannabis facility that was just built in 2022. I bet the owners would be into NFTs (😂). Since that facility is up for sale, numerous 3D surrounding views exist of my plot. Turns out I can even walk to the airport. It’s not much but it’s home to me and all I could afford for the purpose of this story and learning what it was all about. Maybe those 400,000 planned residents will eventually want my land and it’ll make me a millionaire. Ah the allure of California City.

Is Your Big Brand a Bank? You Can Turn it into One

August 16, 2022

“Any entity that has employees, customers, and fans can create a banking infrastructure that looks just like a bank,” said Yuval Brisker, Co-founder and CEO of Alviere. Founded in 2020 as a spinoff of Brisker’s previous firm, Mezu, Alviere is ringing in the next generation of fintech through its embedded finance solutions.

Brisker wasn’t talking about turning the corner diner into a bank, but rather about providing the infrastructure to enable the largest companies and brands in the US to be one-stop shops for financial services, including banking.

“[It could look] like a bank in every sense,” he said, “FDIC insured, providing a savings account with yield, being able to ultimately give them a credit card, that is not a co-branded credit card, but it’s a single brand…”

Alviere has already spent loads of time dealing with the hard parts, building the tech, but also navigating the regulatory framework to make this concept a reality.

“We are a 100% regulated entity, meaning we’re not piggybacking on a banking license,” Brisker said. “We are actually licensed across the United States in every state that takes a license (except Montana). We are licensed with the federal government in Canada and Quebec and in the English speaking provinces, we’re in the process of completing our licensing in Mexico, and in Europe and in the UK.”

Brisker says this proactive approach is a “big differentiator” against the competition because they really want to provide the full services end-to-end. And that’s a big range given that it spans from bank accounts to payments to cards to cryptocurrency.

In making this possible, partnerships are key. Alviere has multiple bank partners across the globe, the company claims, one among them being Community Federal Savings Bank in the US. Alviere even solidified a deal with Coinbase back in March that enables brands to provide crypto services to their customers all through their own branded technology.

In making this possible, partnerships are key. Alviere has multiple bank partners across the globe, the company claims, one among them being Community Federal Savings Bank in the US. Alviere even solidified a deal with Coinbase back in March that enables brands to provide crypto services to their customers all through their own branded technology.

Retail customers might not ever know the name Alviere because they remain in the background, Brisker explained. The brands would, but the customers would only see themselves interfacing with the brand, which is basically the whole point.

“We tell [brands] those customers will never be our customers,” Brisker said. “We’re never going to take over the customer relationship.”

Larger companies have probably entertained this whole idea at some point already, according to Brisker. The potential to capitalize on a loyal customer base by trying to offer them financial services is increasingly being looked at.

“If you’re one of those companies and you also look at the same time how difficult it is to get into this business, both from a regulation, an ecosystem, and a technological point of view, then you’re probably putting that on your back burner and saving this for another day,” he said. Alviere, however, can make this a reality right now.

“We have all the contracts, we have all the relationships, you just need to have one point of contact, one API, one relationship, one contract, and that’s us,” Brisker said. “And we take care of everything else.”

But perhaps it’s all a big bet, because would customers actually use financial services offered through non-bank brands that they’re fans of otherwise? Technically, they already are.

When Alviere launched two years ago, more than 1 out of every 2 Americans had already used a Buy-Now-Pay-Later (BNPL) service, an embedded financial concept that’s taken off around the world. BNPL sales amounted to $100 billion in 2021 in the US alone.

“We believe that there’s a huge opportunity for more traditional beloved and essential brands to become the financial service providers for [people] coming of age,” Brisker said. “And then of course there’s a huge unbanked population that for whatever reason has not entered the financial system here and abroad, which we think that through the affinity with sort of less foreboding, less anxiety, stress-ridden relationships like some people have toward banks that they will be more inclined to come into the financial system through the back door of the system, the front door of the brands they already know and patronize.”

NovoPayment, Latina-founded BaaS Plans to Expand

April 21, 2022 Novopayment has raised $19 million in Series A financing, led by Fuel Venture Capital and IDC Ventures. The company, which offers digital banking, payment, and card solutions, is planning to grow and expand within current and further US markets while focusing on countries in Latin America and the Caribbean.

Novopayment has raised $19 million in Series A financing, led by Fuel Venture Capital and IDC Ventures. The company, which offers digital banking, payment, and card solutions, is planning to grow and expand within current and further US markets while focusing on countries in Latin America and the Caribbean.

CEO and Co-founder Anabel Perez stated, “We define a digital payment as the simple transfer of value from one payment account to another using a digital service such as a mobile device, POS, or computer.”

With the new funding, NovoPayment plans to continue increasing capabilities, introduce new features and functionalities, heighten security, and capitalize on US market opportunities. To accelerate their expansion of current offices in Mexico, Colombia, Peru, Ecuador, and headquarters in Miami, they are adding over 100 new engineers, business development, and product experts to their team. Austin and San Francisco are the first two spots where the branching out will begin.

“Austin and San Francisco are huge hubs for tech innovation and we want to expand there to ensure we attract the best talent for our operations,” Perez discussed. “As we grow in those markets, we’ll assess if we need more boots on the ground in additional states.”

NovoPayment currently holds a strong placement in the LAC region and works with several US clients and partners. This places the company in the right position to broaden in these markets they already have successful track records in.

“Based on our ongoing discussions with clients, we have special insight into the challenges and technology gaps these markets face, and realize the potential to further connect the Americas with a common banking infrastructure. We will be growing our product offerings to enable new data and money flow solutions to account for the increasingly globalized, cloud-based world of financial services,” Perez explained.

As Miami is the “Latin America capital of the US,” NovoPayment holds an advantage as a native of South Florida with the tech scene gravitating towards this region. Miami has served as a gateway to other markets.

“Unlike other companies that are now playing catch up and rushing to the LatAm market, we have a strong foothold and reputation in 14 markets across the Americas,” said Perez. “Establishing those relationships, and understanding the nuances of each market, requires regional expertise that takes time to build.”

Networking, Data, and Innovation Dominate Money 20/20

October 26, 2021 It was not only a focus to sell, showcase, network, and collaborate that drove thousands of attendees to this year’s Money 20/20 in Las Vegas on Monday, it was also the desire to share what kind of innovation everyone has been up to.

It was not only a focus to sell, showcase, network, and collaborate that drove thousands of attendees to this year’s Money 20/20 in Las Vegas on Monday, it was also the desire to share what kind of innovation everyone has been up to.

“It’s great to be back, in person, in Vegas,” said Scarlett Sieber, Chief Strategy and Growth Officer for Money 20/20. After last year’s pandemic-induced cancellation, Sieber spoke about how her and her team have been working to make this the best show yet. “We’ve been researching, strategizing, and imagining what a refreshed Money 20/20 would feel like, and it’s great to see it alive.”

The event was mostly dominated by payments services, who all seemed to be competing with each other rather than networking, largely offering the same services with different branding. Coming in at a far second was cryptocurrency, and their effort to share the impact that their industry has had on all aspects of finance. In the speaking sessions throughout the day, almost every panel at least touched on the legitimization of cryptocurrency in the finance world.

In her first time at the event, Brittany Desposito, Senior Business Development Representative at Appian, an enterprise and workflow application building software, spoke about what her company gets out of sponsoring an event like Money 2020. “We get to learn lots of industry trends [while] trying to figure out what we can market more to fintech companies, and what they are looking for, and what challenges they’re facing,” said Despositio.

“This is a great place to sort of get a pulse of what’s going on, see the various interesting players, and what their [new] solutions are”, said Ani Narayan, a Product Lead at Modern Treasury, a payments operations platform. Narayan stressed the positive impact in-person meetings have on companies like his, giving his company the chance to add clients to their book of business that they would never have been able to prior. “It’s a great opportunity to meet people, potential customers, partners, that you could be working with or potentially could work with, so it’s just a great place to bring the entire community together.”

“It’s our first time here, and what we found out is that [Money 20/20] is a real business spot for every party in the industry,” said Erick Padilla, Head of Growth at DAPP, a company who claims to be building the most advanced payment “railway” in Mexico. Padilla spoke about what the value of a show like Money 20/20 can truly be worth to a company like his. “We can meet some of the people that we haven’t had a chance to meet before because we’ve been in different parts of the world, and now we get this opportunity to meet in person, to get to the decision makers we have been looking for.”

When asked about his company’s intention to return to an event of this size, Padilla not only said he would return, but that he would upgrade his ticket to make more of a presence at the event. “We’re going to get a booth next time,” said Padilla.

The show will continue on Tuesday, as companies will be able to have one last chance to possibly make the connection they came to Las Vegas hoping for.

Mexican Small Business Lender Buys a Bank, Eyes United States

June 18, 2021Change is happening south of the border. Online lenders and alternative funders are growing across Mexico much the same way as elsewhere. This week, Credijusto, an online small business lender based in Mexico City, acquired Banco Finterra, marking the first time that a fintech has acquired a bank in the country.

According to Reuters, “Credijusto aims to ramp up services for Mexican companies that sell to the United States, and build a business for U.S. companies that do cross-border trade in Mexico and beyond in Latin America.”

Mexico also has more than 6 million small businesses, a market that is effecively 4-6x larger than Canada’s.

Prior to this, Credijusto had already collectively raised $400M from Goldman Sachs, Credit Suisse, Point72 Ventures, New Residential Investment Corp., Kaszek, QED Investors, John Mack, Ignia, Promecap and LIV Capital.

“The acquisition of Banco Finterra seeks to create the first truly digital banking platform for Mexican companies in the future,” commented Allan Apoj, co-CEO of Credijusto. “This transaction marks an important milestone in Mexico and the region, and we are proud to be revolutionizing the future of banking in Latin America.”

Apoj’s partner, co-CEO David Poritz, hinted to Reuters that in a couple of years it may consider the acquisition of an American bank as well.

Earlier this year, Mexico began to allow fintech companies to obtain a Financial Technology Institution license.

Estamos muy orgullosos de revolucionar el futuro de la banca en México con la adquisición de Banco Finterra y de beneficiar así a las empresas a través de productos financieros de nueva generación. Conoce más de este gran logro: https://t.co/pbGBVyo04p pic.twitter.com/A32vaHDOB1

— Credijusto (@credijusto) June 15, 2021

Business Funding in Mexico... the canadian market is very well established but next up is mexico, a country with a much larger population than canada... |

ISO Looking for an International Lending Partner... i'm a us-based iso looking to partner with a lender who can fund deals in canada and mexico. term loans (collateral-based okay) and locs. no mca's. i ... |

See Post... mexico is bringing rapists here" and , , "the concept of global warming was created by and for the chinese in order to make u.s. manufacturing non-competitive." or , , "crazy joe biden is trying to act like a tough guy. actually, he is weak, both mentally and physically, and yet he threatens me, for the second time, with physical assault. he doesn’t know me, but he would go down fast and hard, crying all the way. don’t threaten people joe!" or , , "if the morons who killed all of those people at charlie hebdo would have just waited, the magazine would have folded - no money, no success!", , do y... |

See Post... mexico to save money. he inherited (from obama) a decent economy and takes credit for that, and, dismisses covid as a real problem and the worst civil unrest is going on due to the far right and left in a war of political tension. if the only reason your voting for potus is corporate tax hikes, that doesn't help the majority of america. and let's not forget, with the house (dem) and senate (gop) any bill that is potential, has to pass both sides which rarely do. dems are looking to sweep this election with senate, house and, presidency. lets see what happens n... |

See Post... mexico to save money. he inherited (from obama) a decent economy and takes credit for that, and, dismisses covid as a real problem and the worst civil unrest is going on due to the far right and left in a war of political tension. if the only reason your voting for potus is corporate tax hikes, that doesn't help the majority of america. and let's not forget, with the house (dem) and senate (gop) any bill that is potential, has to pass both sides which rarely do. dems are looking to sweep this election with senate, house and, presidency. lets see what happens n... |