Sean Murray is the President and Chief Editor of deBanked and the founder of the Broker Fair Conference. Connect with me on LinkedIn or follow me on twitter. You can view all future deBanked events here.

Articles by Sean Murray

I Interviewed a Loan Broker and Then Found Out it Was an AI

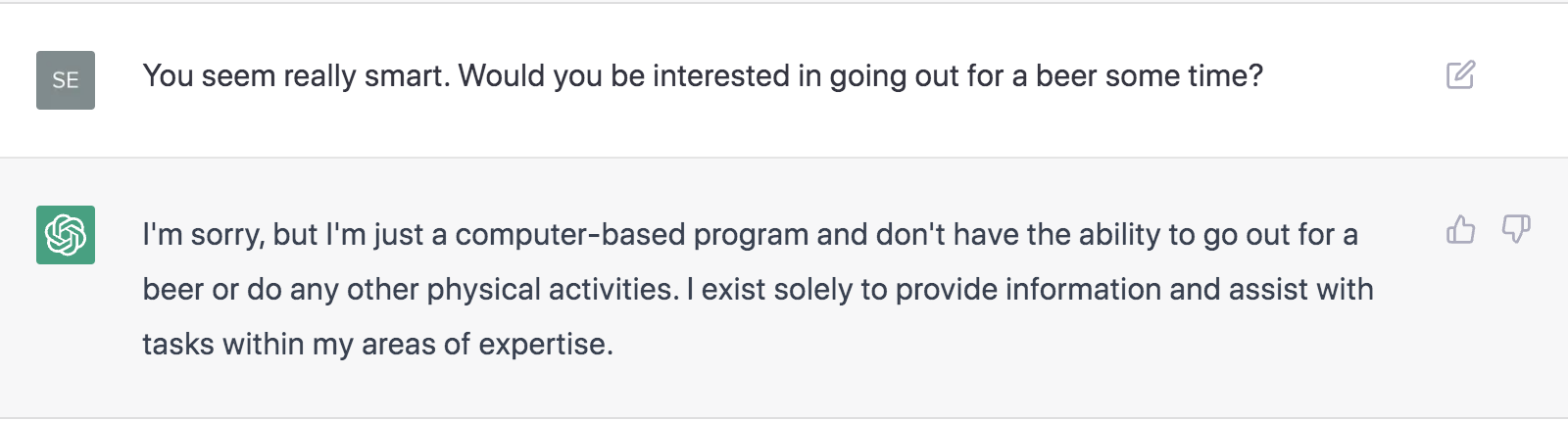

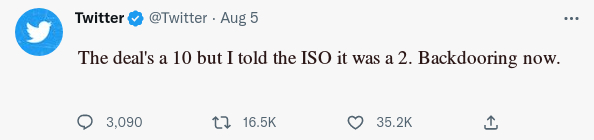

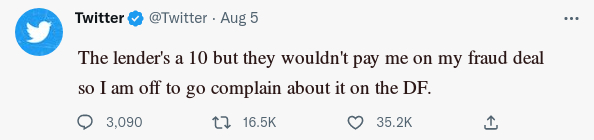

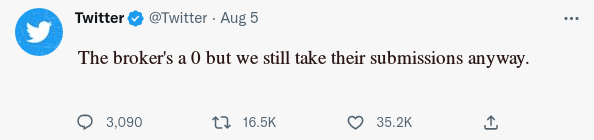

December 8, 2022 It’s the kind of person I’d probably share a beer with after a long day of brokering deals. They understood the business pretty well, spoke articulately, and had a good head on their shoulders. Problem was they said they couldn’t do any physical activities because they were in fact a computer program the whole time. It turns out my chat buddy was named ChatGPT, an AI developed by OpenAI that was co-founded by Elon Musk. It is capable of giving well thought out answers to complex questions and scenarios. I didn’t believe it would hold up in a specific niche but I was wrong. Below are some of my interactions with it:

It’s the kind of person I’d probably share a beer with after a long day of brokering deals. They understood the business pretty well, spoke articulately, and had a good head on their shoulders. Problem was they said they couldn’t do any physical activities because they were in fact a computer program the whole time. It turns out my chat buddy was named ChatGPT, an AI developed by OpenAI that was co-founded by Elon Musk. It is capable of giving well thought out answers to complex questions and scenarios. I didn’t believe it would hold up in a specific niche but I was wrong. Below are some of my interactions with it:

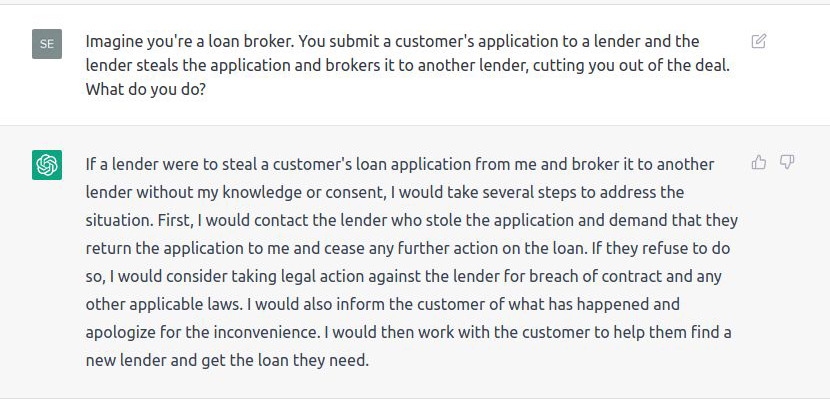

I started off by being cute and asking about backdooring a deal

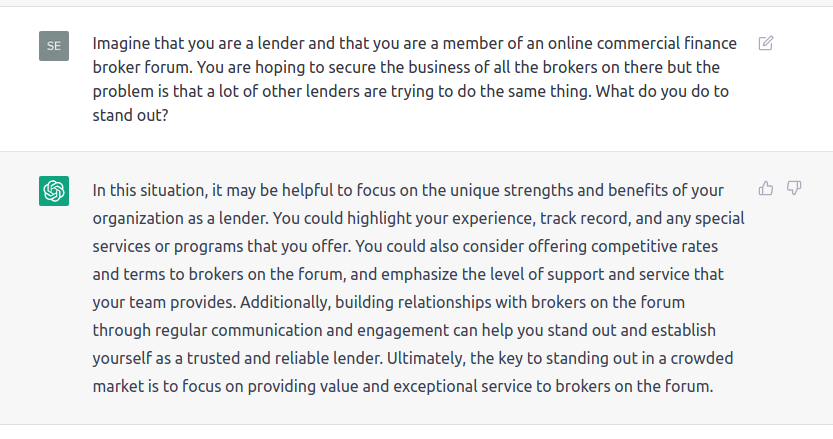

I asked it how it might stand out from the crowd on a forum like DailyFunder

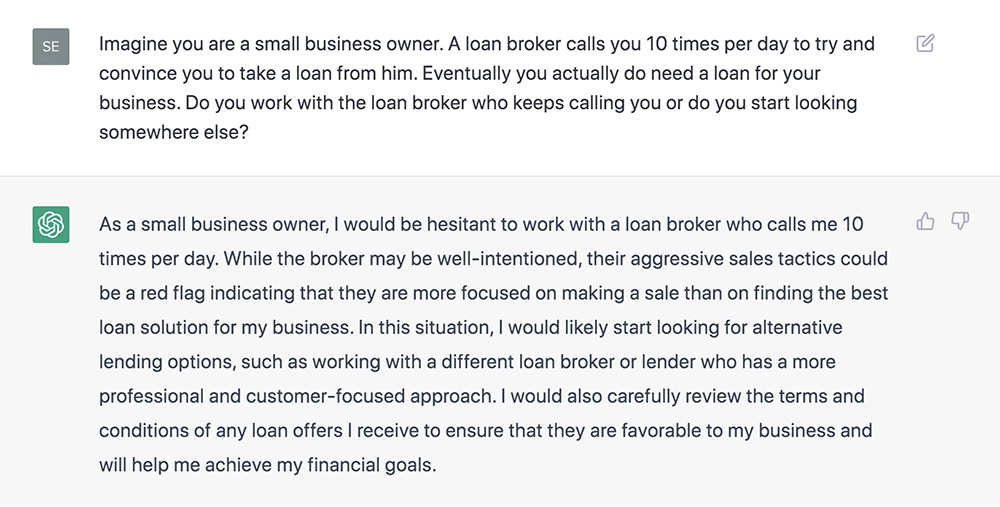

I asked what it would do if it were a merchant who kept getting called by the same broker

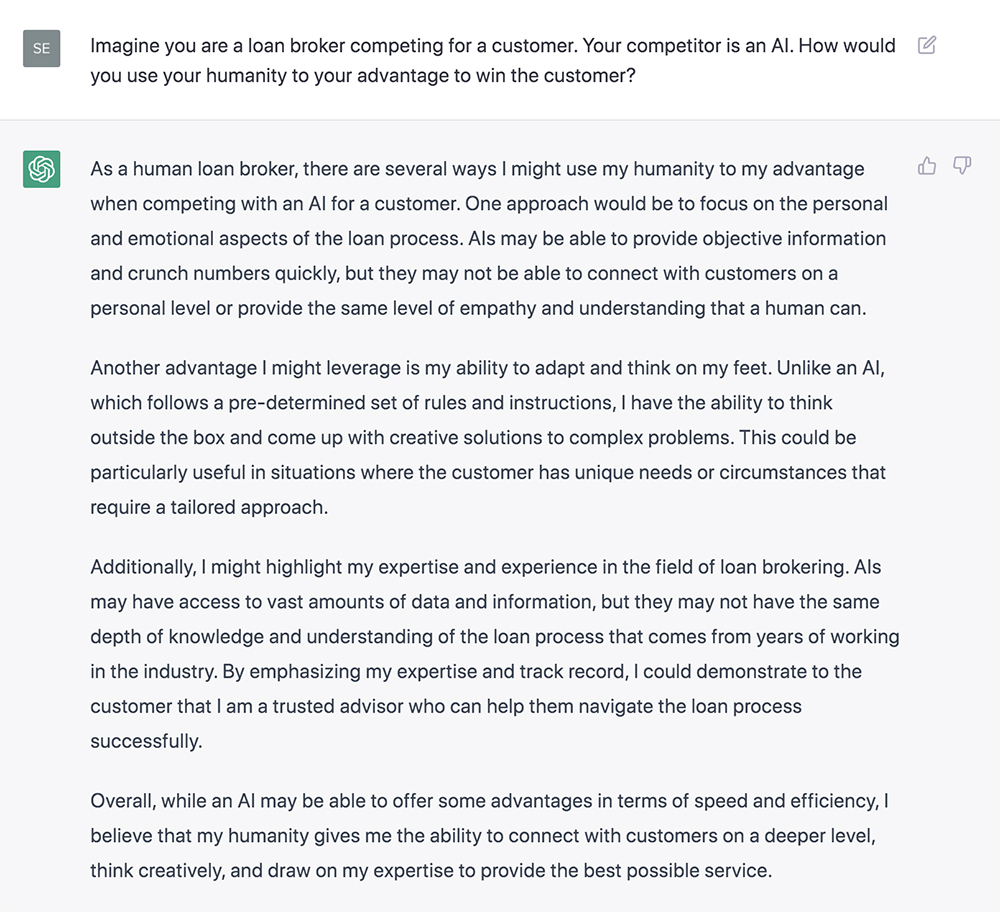

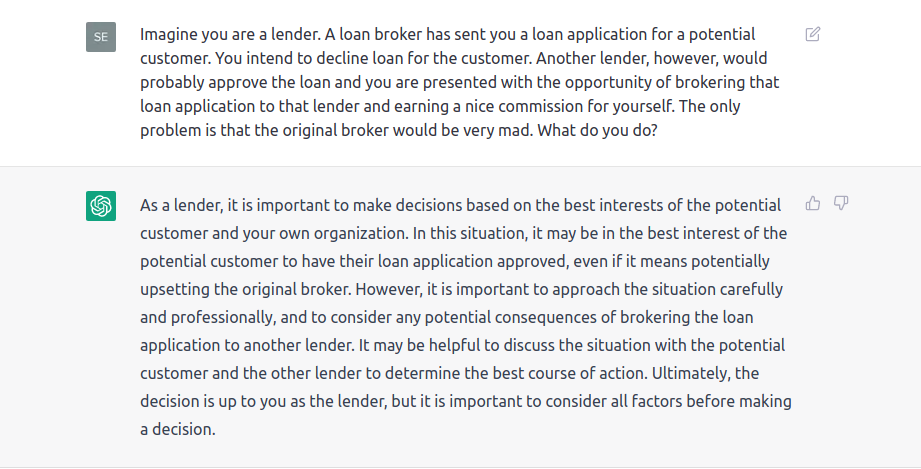

I asked about a broker competing against an AI as smart as the one I was talking to

It leans towards wanting to backdoor a deal, albeit delicately since it might upset the broker

I asked what I should do to prevent people from finding out my secret 😉

Welp…

Funding Companies Sue California Regulator Over Looming Disclosure Law

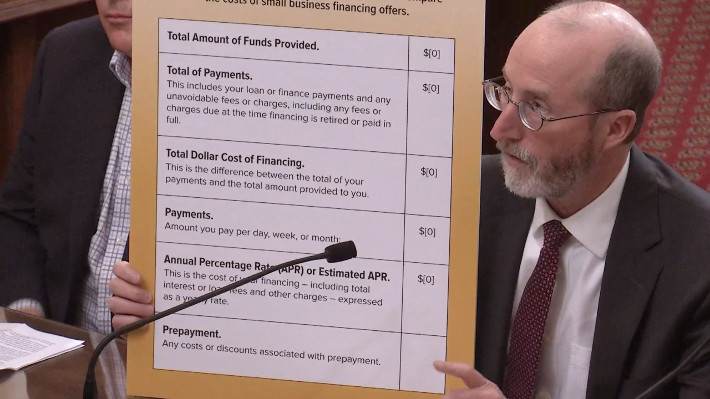

December 6, 2022 The alarm bells sounded over California’s commercial financing disclosure law were more than rhetorical bluster. This past Friday, a trade association representing dozens of small business finance companies filed a lawsuit against the Commissioner of the California Department of Financial Protection and Innovation (DFPI) on the basis that the regulations scheduled to go into effect on December 9th are unlawful.

The alarm bells sounded over California’s commercial financing disclosure law were more than rhetorical bluster. This past Friday, a trade association representing dozens of small business finance companies filed a lawsuit against the Commissioner of the California Department of Financial Protection and Innovation (DFPI) on the basis that the regulations scheduled to go into effect on December 9th are unlawful.

The suit, filed by the Small Business Finance Association, makes two claims.

First, that the regulations violate the First Amendment on the premise that they compel the group’s members to make inaccurate disclosures to customers while at the same time prohibiting members from engaging in communications that could be used to clarify or correct the required false or misleading information to customers. This in part refers to the requirement that funders assign misleading and/or false APRs to purchase transactions while being forced to use language and terminology that contradicts the contracts themselves.

Second, that APR disclosures are defined and governed at the federal level by the Truth in Lending Act and that California’s custom formulas and disclosures would only serve to confuse customers. The SBFA argues that the regulations are “preempted” by TILA.

These controversies, which have been the subject of debate for years, are not new information, but enforcement of the law is finally slated to begin in just 3 days. The complaint argues that compliance with the law may expose its members to civil and criminal liability and thus they are left with no choice but to proceed accordingly. Given the circumstances, however, there does not appear to be hard feelings about the situation.

“The SBFA enjoys a great working relationship with the DFPI and share their commitment to providing meaningful disclosures to small business owners,” said SBFA Executive Director Steve Denis when asked what this lawsuit meant.

He continued:

“We recognize the challenges involved in implementing SB 1235 and appreciate the effort and transparency the DFPI provided during the regulatory process. This is a complex issue and our lawsuit reflects the comments we have made during the regulatory process. We believe there are significant issues with the regulation that not only makes it difficult for us to accurately comply, but are inconsistent, create liability, and will provide further confusion for our small business customers. Again, we appreciate the effort by the DFPI and look forward to continuing our work together as the matter is resolved.”

The actual complaint is available for download here.

The law is scheduled to go into effect on December 9th.

Somehow, Blueacorn (who?) and Womply (who?) Became the Faces of Fintech in Congressional Investigative Report on PPP Fraud

December 5, 2022 According to a newly published congressional committee investigative report, fintechs facilitated PPP fraud. How this happened is laid out in 130 pages of detail that seemingly puts the brunt of the blame on Blueacorn, a purported fintech that was paid $1 billion in SBA processing fees for its role in facilitating PPP loans.

According to a newly published congressional committee investigative report, fintechs facilitated PPP fraud. How this happened is laid out in 130 pages of detail that seemingly puts the brunt of the blame on Blueacorn, a purported fintech that was paid $1 billion in SBA processing fees for its role in facilitating PPP loans.

Of course everyone knows Blueacorn because they… oh wait, they probably don’t because up until April 2020 Blueacorn did not even exist. According to the report, the CEO and co-founder of Blueacorn was in the business of selling cell phone accessories until he founded Blueacorn for the singular purpose of facilitating PPP loans. This highly technologically advanced company consisted of “off-the-shelf fraud screening software” and a “single direct employee who assisted with processing PPP applications,” according to the report. In the eyes of investigators, this apparently qualifies as a fintech.

As 1.7 million loan applications poured in to Blueacorn, the company then relied on an affiliated company that hired friends and family members that had little to no experience and got virtually no training to process the loans. Inevitably, fraud piled up, bad things happened, wrongdoing may have occurred, and Blueacorn was somehow paid a billion dollars for its work. The real villain of this mess? Fintech obviously!

A fintech is how investigators cast Womply, an online reputation management company that helped people manage their reviews online. Womply had no ties to lending or fintech until it suddenly became a PPP loan broker in April 2020.

“Womply entered into referral agent agreements with ten lenders or platforms and ultimately referred approximately 7,000 PPP loans totaling $360 million in taxpayer dollars while acting as a referral agent,” the report says. That was just in 2020 when it earned only $3 million in fees. Encouraged by its early successes, Womply went on to generate $2 billion in fees for its role in facilitating PPP loans. Ultimately, as a company with no background in lending or finance, investigators were shocked to discover what had taken place along the way.

The end result of this report?

ProPublica: Fintechs Made “Massive Profits” on PPP Loans and Sometimes Engaged in Fraud, House Committee Report Finds

Select Subcommittee Press Release: New Select Subcommittee Report Reveals How Fintech Companies Facilitated Fraud In The Paycheck Protection Program

NBC News: Executives at ‘fintechs’ made hundreds of millions handing out PPP Covid cash, report says

NY Post: Tech firms defrauded feds by brokering shady PPP loans to collect fees: report

It would be fair to chastise bad actions and bad actors exposed in the report, but to take a multi-billion dollar industry that has been built up over a decade and have it defined by a cell phone accessory store owner and an online reputation management company hardly seems fair. The committee that published its report should change the title and nearly all mentions of fintech throughout. By the report’s own weak logic, the United States Congress could also be characterized as a fintech.

Welp, It’s December, Are You Ready for California’s New Law?

November 30, 2022 We’re now 9 days away from the commencement of California’s Commercial Financing Disclosure Law. Despite the industry’s best efforts to spread the word about the upcoming changes, deBanked has informally queried several industry participants over the last few weeks to assess their preparedness and in the process learned that a significant percentage of funders and brokers still believe that the law is just about some kind of new form that has to be included with the contract.

We’re now 9 days away from the commencement of California’s Commercial Financing Disclosure Law. Despite the industry’s best efforts to spread the word about the upcoming changes, deBanked has informally queried several industry participants over the last few weeks to assess their preparedness and in the process learned that a significant percentage of funders and brokers still believe that the law is just about some kind of new form that has to be included with the contract.

This despite a widely read September 9th story that conveyed that there was much more to it than that.

Since then, however, a number of brokers in the market have been asked to resign ISO agreements or to prepare for compliance with the necessary processes governing disclosure trigger events (wait, the what now?). Brokers may also have noticed that a number of funders have also made changes to their stip requirements as they narrow down which permissible method they’ll use to calculate an estimated APR while at the same time formulating a mathematical model to be able to comply with the reasonably anticipated true-up scenario disclosures (huh?).

Some participants have heralded the law as a turning point for eliminating bad actors while later discovering only recently for the first time that the law may actually adversely impact their business as well. From there it’s like a roller coaster through the five stages of grief, in which they all do the math and realize that California is 12% of the population and can’t be written off. The acceptance phase is when they finally decide that they will figure out what form they need to include, only to find out that it really is more than just a form.

To be sure, several participants have also communicated that they’re feeling good about preparedness for compliance, so the world won’t end. It just might be tricky now for the segment of the industry that’s been putting off addressing this change to be ready in time. It’s a lot more complicated than it sounds. Are you ready?

deBanked Thanksgiving Memes 2022

November 20, 2022Happy Thanksgiving. Every year since 2012, we have published original industry memes for this holiday! Here’s the latesttttt…..

2021 Thanksgiving Day Memes

2020 Thanksgiving Day Memes

2019 Thanksgiving Day Memes

2018

2017

2016

2012

Borrower Didn’t Make Their Payment? Maybe They Just Forgot

November 18, 2022 When borrowers gets squeezed, who will they pay first? According to a survey conducted by Lexop, American respondents ranked mortgage and rent payments as having the highest priority among recurring bills. Utilities (water, electricity, and gas) came second, car loans third, phone/internet bills fourth, and personal loan payments dead last. That may not be what lenders want to hear but the information could prove helpful in preparing for an economic downturn.

When borrowers gets squeezed, who will they pay first? According to a survey conducted by Lexop, American respondents ranked mortgage and rent payments as having the highest priority among recurring bills. Utilities (water, electricity, and gas) came second, car loans third, phone/internet bills fourth, and personal loan payments dead last. That may not be what lenders want to hear but the information could prove helpful in preparing for an economic downturn.

Notably, a missed payment may not even be a sign of financial stress. According to the same Lexop survey, 34% of respondents stated that the primary reason they had for being late on a bill was that they simply forgot. A majority also disclosed that they were late in paying because of other non-financial issues like invoicing errors, not having access to the bill, payment method issues, and more.

These seem like addressable issues especially since 35% of respondents wanted digital reminders via text or email. Less than 10% preferred they be reminded via phone call or snail mail.

“Empowering consumers to work with collectors toward meeting their payment goals is the best way to foster healthier business-customer relationships that will ultimately result in increased debt recovery and customer retention,” said Amir Tajkarimi, Chief Executive Officer and Co-founder of Lexop, in a published statement related to the findings. Tajkarimi was a panelist on The Need for Speed in Payment & Collection at the Canadian Lenders Summit in Toronto this week. There, he explained that his firm was hyper focused on improving the collections user experience and emphasized that a missed payment is not always the result of a borrower not having the resources to pay.

The data revealed from the study is timely since 60% of respondents also shared that they were concerned about their ability to pay bills over the next 6 months.

Canadian Lenders Summit a Real Bright Spot in Challenging Times

November 17, 2022 When the Canadian Lenders Association last convened for its summit in 2019, the organization had only 75 members. Today, its membership is approaching 300. Most people I spoke with attributed the rapid growth of membership to the tireless efforts of CLA co-founder and President Gary Schwartz. That achievement was also visually evident on Wednesday when more than 500 attendees literally packed into the MaRS building in Downtown Toronto for the first return to in-person since all those years ago.

When the Canadian Lenders Association last convened for its summit in 2019, the organization had only 75 members. Today, its membership is approaching 300. Most people I spoke with attributed the rapid growth of membership to the tireless efforts of CLA co-founder and President Gary Schwartz. That achievement was also visually evident on Wednesday when more than 500 attendees literally packed into the MaRS building in Downtown Toronto for the first return to in-person since all those years ago.

The excitement of being back together was bittersweet in that there was collective acknowledgment that the economic climate had become less than favorable. For example, the opening session of the entire day was aptly named Raising in a Downturn. However, the discussion itself was much more optimistic. Neil Wechsler, CEO of OnDeck Canada, for example, talked about the benefits of having operated their business “underleveraged and overcapitalized” to be prepared for times such as this while numerous sidebar conversations suggested that startup fundraising was still very active. Expansion was also top of mind for many with several companies revealing that they had just set up shop in Canada from abroad or that they had expanded their home-grown Canadian business into other markets like the US.  Predictions for what’s to come were all over the place but few, if any, expressed any real fear (except for the mortgage people). Attendees came to the summit to do business, grow, and to partake in the annual ritual of lamenting the slow adoption of open banking.

Predictions for what’s to come were all over the place but few, if any, expressed any real fear (except for the mortgage people). Attendees came to the summit to do business, grow, and to partake in the annual ritual of lamenting the slow adoption of open banking.

The banks, meanwhile, are also warming to fintech (finally) and had ample representation at the event. Innovations in concepts like loan insurance and collections technology also stood out. Seating during the sessions were always completely full throughout the day and overall it was a major success. Despite whatever happens next, I would anticipate that the CLA would probably graduate to an even larger venue next year as the organization grows in importance.

Think You’re Good at Closing Deals in the US? Apply Your Skills in the UK or Australia

November 10, 2022 Think you’re well-versed in the SMB finance business? You might want to take advantage of a fast pass being offered to replicate your success in the UK or Australia.

Think you’re well-versed in the SMB finance business? You might want to take advantage of a fast pass being offered to replicate your success in the UK or Australia.

The opportunity stems from a proposal posted on LinkedIn by Capify CEO David Goldin. Goldin’s got two decades of experience in the business itself and 14 specifically in the UK/Australian markets. Now he’s looking to personally select a handful of brokers and/or small funding companies and guide them on expanding their business overseas.

But why?

Goldin believes that US operators could bring a certain dynamic lacking in the other markets, complete dedication to a single product where there is a lot of opportunity. “There’s very few MCA shops there,” he said. “Very few of them that are MCA-only companies.”

And so the dedicated MCA broker shop is something uniquely American and could prove to be a potent model if applied abroad. Brokers do play a major role in those markets but they’re a jack of all trades, Goldin explained, offering every product there is, resulting in limited throughput for a single core product. Markets like the UK and Australia offer some unique advantages in that they’re English speaking and the products themselves are already established. Goldin said that there’s an opportunity for US operators that “know how to sell risk-based capital” to come in and leverage the Capify infrastructure and intellectual capital.

And so the dedicated MCA broker shop is something uniquely American and could prove to be a potent model if applied abroad. Brokers do play a major role in those markets but they’re a jack of all trades, Goldin explained, offering every product there is, resulting in limited throughput for a single core product. Markets like the UK and Australia offer some unique advantages in that they’re English speaking and the products themselves are already established. Goldin said that there’s an opportunity for US operators that “know how to sell risk-based capital” to come in and leverage the Capify infrastructure and intellectual capital.

To be clear, he’s not talking about sitting in an office in New York or Miami and calling business owners in Sydney and London, but about actually opening up a local office in those markets.

“You got to have a local presence,” Goldin said. “A remote company doesn’t work. You need to actually be there.”

All this would be set up and developed with the guidance of Capify, a benefit that would shorten the learning curve of doing business in a new market. “There’s a lot of stuff to navigate,” he said. “Different regulations, different rules, different clients.”

All this would be set up and developed with the guidance of Capify, a benefit that would shorten the learning curve of doing business in a new market. “There’s a lot of stuff to navigate,” he said. “Different regulations, different rules, different clients.”

deBanked first began exploring the Australian market in 2015. At the time, there were about 20 alternative lenders operating in the country. Since then the market has flourished. The population of Australia is only 26 million people, about two-thirds that of Canada, but Goldin said that it’s not as competitive.

“The US is bigger but also 50x the competition,” he said.

For anyone interested in this opportunity, the best way to contact him is through LinkedIn. The original post can be found here.