Sean Murray is the President and Chief Editor of deBanked and the founder of the Broker Fair Conference. Connect with me on LinkedIn or follow me on twitter. You can view all future deBanked events here.

Articles by Sean Murray

The Rest of the Alternative Lending Industry’s Funding Numbers

July 1, 2015 Let’s be serious, the industry’s much bigger than we may have let on when we published the industry leaderboard (some mods have been made) in the May/June issue.

Let’s be serious, the industry’s much bigger than we may have let on when we published the industry leaderboard (some mods have been made) in the May/June issue.

Right after deBanked sent the final file off to the printers in May, PayPal announced that the widely circulated $200 million lifetime funding figures were slightly outdated.

How off were they?

Oh, just by about $300 million or so. By May 7th, PayPal’s Working Capital program for small businesses had already exceeded $500 million. The industry leaderboard has been revised to reflect the news. PayPal says they are funding loans at the rate of $2 million per day, which puts them on pace for more than $700 million a year. Um, wow?

One name that’s missing from that list is Amazon, whose secretive short term business loan program is reported to have already generated hundreds of millions of dollars in loans. Given the $300 million discrepancy that PayPal let ruminate for months, we’re in no position to speculate on Amazon. Anyone could try to assess what they’ve been up to however, since they file UCCs on their clients under the secured party name “AMAZON CAPITAL SERVICES, INC.”

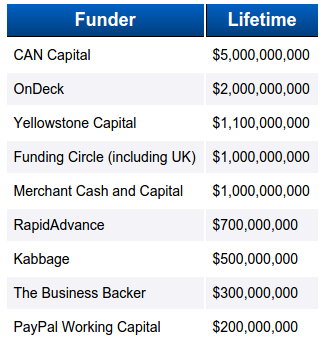

Of course if you’re craving specific numbers, an anonymous source inside Yellowstone Capital revealed that Yellowstone produced $35.5 Million worth of deals in the month of June alone. Yellowstone has a strategically diverse business model that allows them to either fund small businesses in-house (essentially on their own balance sheet) or broker them out to other funders. Yellowstone was listed on deBanked’s May/June industry leaderboard at $1.1 Billion in lifetime deals and $290 Million in 2014. June’s figures indicate that they are probably well on their way to surpassing last year’s numbers.

Curiously, platform/lender/broker/marketplace company Biz2Credit has been hanging on to the same stodgy old number for more than a year.

Funded over $1.2 billion. 200,000+ happy customers.http://t.co/3h64lI4cgG #smallbusiness #Funding

— Biz2Credit (@biz2credit) June 19, 2015

They were touting that same $1.2 Billion number exactly 1 year ago. Surely they have done more since then? Biz2Credit’s service covers a much wider scope however so a direct comparison with their peers may not be appropriate. A lot of their loans are arranged through traditional banks which are typically transacted in amounts larger than the average $25,000 deal alternative lenders do.

A source familiar with Biz2Credit’s breadth said he observed a deal where the company helped a businessman in Mexico obtain financing to purchase a new helicopter, a transaction which apparently necessitated a team to fly down there to sign paperwork. Definitely not a standard transaction!

When we published the industry leaderboard initially, it admittedly omitted some of the industry’s largest players. Many firms are fairly secretive about the numbers they release and we’re in no position to disclose numbers that aren’t supposed to be public. Below is data that we hadn’t published previously.

The industry’s unsung behemoths

The industry’s unsung behemoths

The $300 million lifetime funding figure publicized by NYC-based Fora Financial can’t be that stale. It’s the number currently stated on their website and a late February 2015 company announcement revealed they were only at $295 million at the time. We feel comfortable enough to now have Fora Financial on the leaderboard.

In 2014, Delaware-based Swift Capital revealed that they had funded more than $500 million. It’s unclear how much that’s increased since then.

Credibly (formerly RetailCapital), has publicized that they’ve funded more than $140 million in their lifetime. Founded in Michigan, the company has opened offices in New York, Arizona, and Massachusetts. They’ve been added to the lifetime leaderboard.

New York City-based AmeriMerchant has a claim on their website that they have funded more than $500 million since inception. How much more exactly? We’re not sure.

Coral Springs, FL-based Business Financial Services keeps their figures mostly under wraps but a good guess would place their lifetime figures at somewhere between $700 million and $1.2 billion.

Miami, FL-based 1st Merchant Funding had reportedly funded close to $100 million in the Spring of 2014. It’s uncertain as to where they might be now.

Woodland Hills, CA-based ForwardLine surpassed $250 million in funding as far back as 2013.

Orange, CA-based Quick Bridge Funding disclosed more than $200 million in funding in late 2014.

Troy, MI-based Capital For Merchants has funded $220 million since inception. But there’s more to the story. Capital For Merchants is owned by North American Bancard, a merchant processing firm that acquired another merchant cash advance company, Miami, FL-based Rapid Capital Funding in late 2014. And coincidentally, Rapid Capital Funding had just acquired American Finance Solutions months earlier, which is an Anaheim, CA-based merchant cash advance company that had funded more than $250 million since inception. All told, North American Bancard owns at least three merchant cash advance companies: Capital For Merchants ($220 million), American Finance Solutions ($250 million+), and Rapid Capital Funding (undisclosed). There are rumors that they’re in talks to acquire at least one more company in the space, which, if true, would make North American Bancard one of the industry’s most powerful players.

Don’t bother counting up the above totals

These figures all barely scratch the surface as deBanked’s database indicates there are literally hundreds of genuine direct funders in the industry.

Thanks to the company representatives that took the time to confirm their funding numbers with us directly. Anyone interested in sharing their figures can email sean@debanked.com. If there is a gross inaccuracy somewhere as well, please report it to us.

This page might be updated in the future so check back!

Is Amazon Already a Top 10 Funder?

June 29, 2015 18 months ago I mentioned Amazon’s quiet entry into business lending but nobody’s really talked about it. But earlier today in a story that was supposed to highlight the company’s push into China, they revealed some interesting details that the rest of the alternative lending industry deserves to know about.

18 months ago I mentioned Amazon’s quiet entry into business lending but nobody’s really talked about it. But earlier today in a story that was supposed to highlight the company’s push into China, they revealed some interesting details that the rest of the alternative lending industry deserves to know about.

1. Amazon offers three to six-month loans of $1,000 to $600,000 to help merchants buy inventory.

2. Amazon has already funded hundreds of millions of dollars.

3. Sellers are reporting interest rates of 6% to 14% but it’s unclear if these are APRs or dollar for dollar costs since the loans are for much less than a year. I suspect the effective APRs are higher.

While Amazon is obviously doing these to grow Amazon merchants, the short maturities and stunning loan volume definitely earns them a spot on the list of the biggest funders in the industry.

Another fact worth repeating is this tidbit from PayNet:

“The default rate for small businesses with credit under a $1 million stood at 1 percent in 2014 but is seen rising to 1.6 percent in 2015, as new lenders with varying ability to assess risk increase lending, according to small business credit ratings provider PayNet.”

Tech-based Lenders Clobbered On Dose of Bad Economic News

June 29, 2015How would tech-based lenders fare in a slumping market? Not very well apparently…

OnDeck (ONDK) and Lending Club (LC) set new record lows earlier today amid bad news coming out of Greece and Puerto Rico. OnDeck is down almost 43% from its IPO price and down 61% from its all time high. It was down more than 8% today even though the Dow was only down 2%.

$ONDK was unaware that it focused on Greek loans…. interesting 8.6% drop.

— Mark Holder (@StoneFoxCapital) Jun. 29 at 05:48 PM

The downward trend was dissected in a post that was published just hours before today’s further fall.

Meanwhile Lending Club is in new territory, down 3% from its IPO price and down 50% from its high. So what are investors saying about this?

$LC hmm i really dunno what to say about this…

— mike pham (@mincogneto) Jun. 29 at 05:30 PM

That’s kind of the overall gut feeling. Many feel this company is being unfairly dragged down and yet it continues to fall. A mounting campaign by the Puerto Rican government to declare bankruptcy and a Greek debt disaster clobbered everything today including Lending Club. One tweeter came up with a great idea last week, bail out Greece with a loan from Lending Club…

If all else fails with the IMF #Greece should just apply on @LendingClub pic.twitter.com/RbtnMm5JaO

— World First USA (@WorldFirstUS) June 22, 2015

Last week no one was even talking about Puerto Rico. Now all of the sudden they’re in a “death spiral.”

Watch the death spiral coverage on CNN

The market’s tech lending darlings might’ve gotten pummeled like everyone else but the ease with which they drop should probably be a warning sign. Neither offshore dilemma stands to have any impact on their businesses. So what would happen if a relevant issue were to arise such as a domestic disaster, a sudden rise in unemployment, a recession, a financial crisis, skyrocketing fuel prices, a steep increase in the fed funds rate, or even something no one dares talk about like a legal ruling that could jeopardize the entire bank charter model?

It’s quite possible that both companies haven’t bottomed out just yet….

——–

Note: I have no equity positions in either company. I do own Lending Club notes however.

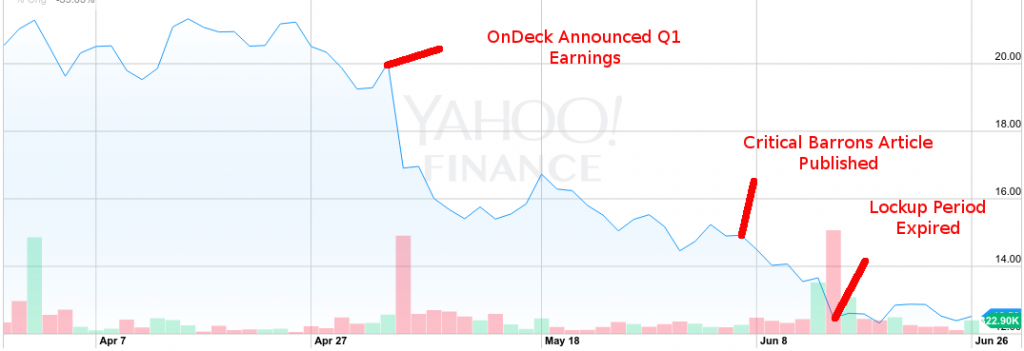

What Happened to OnDeck? (ONDK)

June 29, 2015The lockup expiration came and went but the fall of OnDeck’s stock price started much before that. There were no insider stock sales reported to the SEC since shares became unrestricted anyway.

There’s very little trading volume on an average day and investors on the big message boards either ignore this stock or don’t understand it.

The trend started on May 4th when they released Q1 earnings. The direction wasn’t very much different than Q4. Loan volume went up, interest rates came down, and no profits were to be had, nor were any expected for the rest of the year.

The market interpreted decreasing interest rates as pressure from competitive forces however and down went the stock price.

OnDeck’s execs insisted that they had lowered rates as part of a deliberate strategy to create stickier customers and attract new borrowers. CEO Noah Breslow himself said during the previous 2014 Q4 earnings call that “there’s so much search cost associated with going out and looking at other places and so much uncertainty around that, they [small businesses] typically just take that offer that OnDeck has provided to them.”

His theory is supported by the results of Lending Tree’s recent survey that revealed nearly 60% of small businesses did not comparison shop business loans online during their loan application process.

It’s possible though that the drop had little to do with OnDeck’s actual performance. That same day, Goldman Sachs hinted that they would be joining the tech-based lending field when they announced the hire of Harit Talwar from Discover Financial Services.

But before they had a chance to recover, Barrons published a story that was highly critical of OnDeck just a month later on June 5th. “It’s a subprime lender in dot-com clothing,” the author wrote. It was a tough characterization for them to refute, what with their 50% interest rates and double digit percentage charge-offs and all.

And then the lockup expiration on June 15th coincided with the big reveal of Goldman’s intentions to compete in the marketplace. News sources that picked up the story predicted that the move would impact online lenders like Lending Club and OnDeck. OnDeck’s stock hit a record low that day.

OnDeck has been stuck in the 12s ever since. Can they dig themselves out?

If competition is a factor in the market’s perception, and it probably should be, then investors should keep an eye on the industry’s other top players. OnDeck is not alone in this space and Goldman Sachs will be in for a bigger fight than they probably expect.

Source: deBanked’s May/June Magazine issue

The CFPB is Pretty Busy With Actual Consumers

June 28, 2015 It’s often theorized by industry insiders that the Consumer Financial Protection Bureau (CFPB) will play a role in business to business transactions. But when you actually talk to those employed by the government agency, it seems very unlikely. The CFPB is already very busy playing the role of Better Business Bureau, albeit a nationalized version.

It’s often theorized by industry insiders that the Consumer Financial Protection Bureau (CFPB) will play a role in business to business transactions. But when you actually talk to those employed by the government agency, it seems very unlikely. The CFPB is already very busy playing the role of Better Business Bureau, albeit a nationalized version.

There is currently no categorical option to report business loan or merchant cash advances on their website and the complaints lodged by consumers pertain to very basic consumer problems, such as issues with their credit cards or student loans.

Here’s an example of a CFPB complaint:

2009 XXXX XXXX, XXXX XXXX Thursday of every month I got pulled from class to get a new loan for my living and tuition expenses. I was at XXXX for one year and if I didn’t go to sign the papers for my new loan every month I wouldn’t be able to continue my classes to XXXX. I missed out on important class information and had to make them up on my own time. Homework and other hands on tasks became more difficult to accomplish if I didn’t make up the lost time going to sign loan papers. I was told a rough amount that my school loan would be. About {$15000.00}. I started paying {$120.00} a month for my loan agreement then Genesis Lending increased it to {$190.00}. I called to ask why the increase in payment amount each month. I was told they saw i had a higher income so they adjusted the payment accordingly. Is that legal? I’ve been paying this amount for 6 years and still owe {$13000.00}. I called Genesis Lending and come to find out they have been rolling over all the interest I pay on the loan every year. So all I’m paying is interest basically for the last 6 years. I don’t think I ‘m being treated fairly or legally.

Many complaints are just like this, where consumers are not actually reporting illegal activity but instead using the CFPB to vent their frustration. In this situation, the victim was busy with homework and wasn’t sure how their student loan worked so they filed a complaint with the federal government…

The end result was that the lender responded by saying it wasn’t really their problem, the borrower didn’t dispute this response and the CFPB marked the case as closed. Seems like a great use of everybody’s time.

In the handful of presentations I’ve attended by the CFPB, they said they often find themselves redirecting complaints to the business that the consumer is complaining about much like the BBB would do.

Still Reviewing Paper Bank Statements? Stop

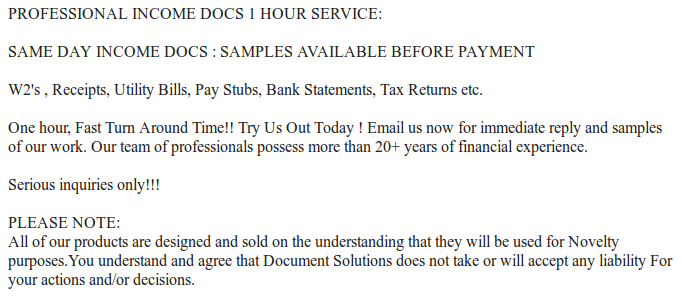

June 26, 2015 Are the bank statements you received legitimate? Underwriters in the business financing industry are scouring paper documents for abnormalities hoping to catch fraud in the inducement. And word on the street is that small business owners are doctoring statements and engaging in trickery in record numbers.

Are the bank statements you received legitimate? Underwriters in the business financing industry are scouring paper documents for abnormalities hoping to catch fraud in the inducement. And word on the street is that small business owners are doctoring statements and engaging in trickery in record numbers.

Technology has made it easier to create authentic looking documents and the rise in online lending seems to be bringing out the worst in people. Somebody in a desperate situation might not have the guts to look a banker in the eye and hand him a stack of fraudulent documents but they might roll the dice with somebody over the Internet they’ll never have to meet.

The fakes aren’t obvious anymore. Anyone can go online and buy doctored documents from professionals. The business is booming on Craigslist for example where fraudulent documents can be made to order in under an hour.

In the Miami area, fraud hucksters are even beginning to offer deals such as buy 2 fake documents, get 1 free.

Industry-wide, funding companies are complaining that attempted fraud is out of control. One broker recently took to the dailyfunder forum to share her frustration. “I can spot them a mile away!!! 2 different deals submitted this week with fraudulent statements!!!,” she vented.

Other brokers chimed in, sharing their stories such as a merchant whose doctored statements were only noticed because ATM withdrawals were listed with odd amounts like $90.83.

Oddly, nobody seems to be reporting this fraud to the authorities. It all seems to get swept under the rug as business as usual. Orchard co-founder David Snitkoff for example, was asked just last month about the rate of marketplace lending fraud and he apparently said, “No worries, none to date.” He seemed to be implying that fraudulent applicants are getting screened out. But that doesn’t mean people aren’t trying.

Seven months ago, merchant cash advance underwriter Pierre Mena wrote in detail about the challenges he faces in detecting fraud. He said:

Some of the more well hidden fraud can usually be found by comparing the summary page and last page of the bank statement to other statements. Typically, most banks and some credit unions offer you a snapshot of the starting balance, which should generally match up with the ending balance of the previous month. If it doesn’t, you should look for any transactions from the previous month that did not settle until the current month. If there is none, this is usually a red flag indicating that the merchant forgot that statements are continual time series financial data whose totals carry on to the following month.

-Pierre Mena, Rapid Capital Funding

A lot of these issues can be easily overcome by simply disregarding paper statements altogether. Microbilt’s instant bank verification tool for example, will allow you to pull the most recent 90 days worth of transaction data directly from the banks themselves. Funders using these automated checks swear by their effectiveness and the capability is essential for any company that wants to scale.

But a recent conversation with the owners of a broker shop in NYC said this is easier said than done. Merchants are still using fax machines to send statements or claiming they don’t have access to computers or email accounts, they said. They added that their clients would suffer if approvals were completely contingent upon online verifications.

But a recent conversation with the owners of a broker shop in NYC said this is easier said than done. Merchants are still using fax machines to send statements or claiming they don’t have access to computers or email accounts, they said. They added that their clients would suffer if approvals were completely contingent upon online verifications.

Cultural differences play a role in this according to Gil Zapata, the founder of Florida-based Lendinero. Zapata recently wrote that latino business owners over the age of 45 are not accustomed to doing business over the Internet, email, fax, or phone. “This group has a high level of distrust in doing business via the Internet,” he said.

So is there a middle ground? On the dailyfunder forum, Chad Otar, a managing partner of Excel Capital Management said that he tells merchants they can change their online banking passwords after a verification. And Andy McDonald of Yellowstone Capital wrote that verifying the bank data is beneficial for the merchants too. “It protects the merchant by allowing us to check their account to make sure our pulls aren’t going to bounce,” he wrote in a thread back in April. He also added that he comes across 2-3 applications PER DAY with altered statements.

Humans can only do so much. Pierre Mena actually wrote, “Some of these statements are doctored so well that you may have to zoom in upwards of 300% to find a comma that should actually be a period to separate dollars from cents.” At this point, an instant bank verification would probably work wonders.

Online business lender Kabbage might have the best model. On their website, applicants are instructed to enter their email address followed by their bank account username and password. Their system will analyze their bank transactions and if eligible, will then ask the applicant for their first and last name. It flies in the face of all the pushback that funders claim merchants give them over data privacy and security.

Four months ago Kabbage announced they were already up to funding $3 million per day. Obviously there is an entire segment of small business owners that are sucking up whatever concerns they had about bank verifications in order to get the capital they need.

The majority of the small business financing industry is still relying on paper statements and probably shouldn’t be. If you have to zoom in upwards of 300% to find a comma that should actually be a period and if con artists are offering discounts for bulk orders of fraudulent statements, it may be time to throw in the towel and join the rest of the world in using the Internet…

Dear Brokers, Investors Love You Too

June 25, 2015Hedge funds, private equity, and family offices have been all hot and bothered by lending marketplaces and direct funders for a while now, but there’s a new sexy stud that everybody wants to take to the dance, the brokers that originate the deals. An entire segment of the industry still calls them ISOs (Independent Sales Organizations) and in 2015, nobody can seem to shut up about them.

One minute brokers are being fingered as the source of the industry’s moral decline and the next minute they’re the lifeblood of it all.

Ever since World Business Lenders began acquiring broker shops and converting them into franchisees, the institutional investors suddenly woke up.

They’re Buying Brokers? BUT WHY?!

Over the years, dozens of funders have opened for business and then realized they don’t know how to get deals or where to get them from.

It’s not a build-it-and-they-will-come industry anymore. As much as certain people try to berate brokers, it’s widely believed that they still control up to 50% of the industry’s deal flow. Institutional investors examining portfolios have taken notice that some funders are successful only because they have a loyal group of broker shops. So if the brokers make the funder, then why not court the brokers?

And so they’re doing just that…

If you’re brokering less than a million a month though, you’re not really investment material yet. There’s thresholds. The more volume you produce, the more options at your disposal.

At this size, you’re really just a couple of dudes (or dudettes) sitting in a room with phones. There’s not enough action to get anyone excited. There may be some potential to get an investor to co-syndicate with you, but that’s it.

$1 Million/month to $4 Million/month

Congratulations, you’re not just a bunch of dudes anymore. If you’re using decent software, hopefully you can print out the necessary reports to woo investors. At this level you’re eligible for co-syndication, an advance rate to fund your own deals, or to be rolled up as a franchisee. If you’ve got a criminal record or have been banned by the SEC, then forget it though.

$4 Million+

If you’re not already funding your own deals at this point, you’re going to be encouraged to by an investor. They’ll want to set you up on a platform that they trust and participate in the funding in some way. You can get a credit facility. You’re also acquisition material. Funders and investors have little interest in acquiring a couple of dudes sitting in a room because there’s no actual assets to value. At $4 million a month and more, there may potentially be something beyond just the dudes running the company and therefore something to consider. If you can’t pass a criminal background check though, then forget it. And if you’re running scrappy like a $200k/month shop, then they’re not really going to be able to help you. It doesn’t help if you’re stack-heavy either.

But just because you do the volume, that doesn’t mean you can just show an investor an Excel spreadsheet and hope that they’ll fork over millions of dollars in return. You have to run your shop like a professional, not a dude (or dudette of course). And if you think you meet that criteria, that’s great news, because investors want to talk to you really badly.

But just because you do the volume, that doesn’t mean you can just show an investor an Excel spreadsheet and hope that they’ll fork over millions of dollars in return. You have to run your shop like a professional, not a dude (or dudette of course). And if you think you meet that criteria, that’s great news, because investors want to talk to you really badly.

Last year, every banker I sat down with told me they were looking to invest in the next OnDeck or CAN Capital. And what happened was, you had 200 bankers competing for the same handful of deals. This year, the conversations are all about brokers.

“Who wants to become a funder?”

“Who needs money to syndicate?”

“Who is serious about growing their broker shop?”

Did someone say Year of the Broker?

It damn sure is. If you’re funding more than a million a month, don’t rely on stacking, don’t have a criminal record, have actual reporting systems (not Excel), and want to be a funder or participate in more deals, then there’s a group of investors that are ready and willing to swipe right.

You might not be the next OnDeck and that’s okay. If you’ve got the flow, you can get the dough. <3 😉

Tech-based Underwriting Shows Cracks?

June 21, 2015 A self proclaimed borrower of Lending Club and Prosper loans posted a tell-all on the Lend Academy forum earlier today and the allegations are alarming. Below is a summary of their experience:

A self proclaimed borrower of Lending Club and Prosper loans posted a tell-all on the Lend Academy forum earlier today and the allegations are alarming. Below is a summary of their experience:

- Stated that when times got tough, they resorted to lying about everything.

- Alleged the lenders don’t care about what they’re using the money for.

- Stated that after consolidating their debt, they immediately maxed out their revolving lines again.

- Proclaimed that these types of loans are for people who are at the end of their rope just trying to survive.

- Alleged their revolving line utilization percentage was wrong because credit bureaus showed old revolving accounts as open even though they’ve actually been closed for years. In their case, the utilization stated 25% but in reality was 100%.

- Alleged their Debt-to-Income ratio was wrong. It looked more favorable than it actually was.

- Stated they stopped making payments and then filed bankruptcy six months later.

- Alleged Prosper never even filed a Proof of Claim with the bankruptcy court and therefore won’t be receiving anything.

Disturbingly, the borrower says they were able to get a second loan from each lender without their employment/income being re-verified.

“I guess I could have lost my job and you never would have known,” the author writes.

Suspiciously however, they go on to make an off-the-cuff recommendation that peer-to-peer marketplaces be required to invest their own money in the loans they issue.

“Why wouldn’t a company file a proof of claim?,” they questioned. “I have to assume because they have no incentive to do so. If the law was changed so these companies had to put up 10-20% of their own money, you may see them caring more about the investors.”

One has to wonder why an individual that successfully evaded a creditor after drowning in debt and filing bankruptcy would come on to lobby for a law that would encourage that creditor to do a better job collecting.

Regardless of us being able to confirm the borrower’s authenticity though, they did raise some good points.

Is it possible that a credit bureau could show accounts as open that are actually closed? Of course. A recently issued FTC report revealed that one in five consumers had an error on at least one of their three credit reports. But even worse, one in just four consumers identified errors on their credit reports that might affect their credit scores.

If 20% of reports are not perfect and 25% of consumers see material errors in their reports, then investors are working off of pretty shoddy data to make decisions.

Additionally, a common complaint by investors on the forum are loan amounts for debt consolidation that wildly exceed the borrower’s actual revolving debt. Could this be a sign that borrower intent is not validated?

And while I couldn’t confirm whether or not income and employment are re-verified on additional loans from the same lender, the implications of playing fast and loose the second time around are troublesome. Lending Club states that past performance is the predominant basis for another loan:

To qualify for a second loan, you’ll need to meet the current credit criteria for the second loan and have made either 6 or 12 consecutive on-time monthly payments on your existing Lending Club loan*, depending upon the size and term of the existing loan.

*Borrowers must have made 12 consecutive successful monthly payments if the original loan principal is $20k or more or the existing loan has a 60 month term, unless the loan has been paid down by 50% or more, in which case borrowers need only have made 6 consecutive monthly payments. Borrowers must have made 6 consecutive successful monthly payments if the original loan principal is less than $20k and the loan has a 36 month term.

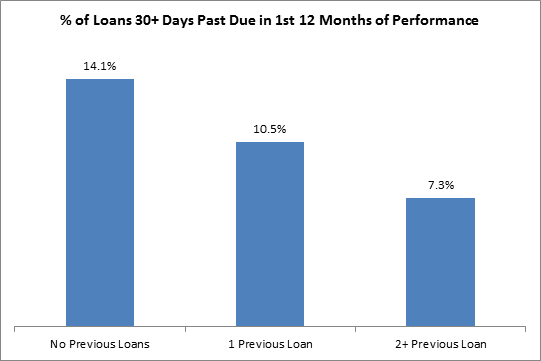

But while the defaulting borrower tells us to be afraid, historical data paints a different picture. Peer-to-peer lending guru Peter Renton has long touted repeat borrowers because of the stellar returns they produce.

And Orchard’s analysis of Prosper loans two years ago confirmed the same. The more loans a borrower took with Prosper, the less likely they were to become delinquent on their loan. This was only the case for the first 12 months of the loans, not in their entirety to maturity, which they didn’t examine at the time.

But while the statistics look good, the defaulting borrower is perhaps warning us that a lender’s guard comes down with positive past performance and is therefore vulnerable.

Whatever the case may be and whatever the author’s true intentions are, it is certainly alarming to read that a borrower lied, their credit information was inaccurate, they defaulted on the loan, and the lender made no effort to make a claim in the bankruptcy proceeding.

Is tech-based underwriting and the marketplace model showing cracks? You be the judge…