Sean Murray is the President and Chief Editor of deBanked and the founder of the Broker Fair Conference. Connect with me on LinkedIn or follow me on twitter. You can view all future deBanked events here.

Articles by Sean Murray

Could The Debt You Bought on a Lending Marketplace be Null and Void?

August 17, 2015 Lending Club and Prosper may have paved the way towards marketplace lending’s legality, but the recent Madden v. Midland ruling could jeopardize everything. Ratings agency Moody’s stated in a July 20th report that, “if interpreted broadly, interest rates on some loans backing marketplace lending ABS transactions could be reduced, or the loans themselves be void.”

Lending Club and Prosper may have paved the way towards marketplace lending’s legality, but the recent Madden v. Midland ruling could jeopardize everything. Ratings agency Moody’s stated in a July 20th report that, “if interpreted broadly, interest rates on some loans backing marketplace lending ABS transactions could be reduced, or the loans themselves be void.”

Moody’s Alan Birnbaum goes on to explain in the report that non-bank entities that buy loans from banks may be subject to state usury laws. “Therefore, the loan buyer might not be able to charge and collect interest at the contract interest rate, while in the worst case a loan could be unenforceable,” he is quoted as saying.

Lending Club’s CEO addressed this case in the company Q2 earnings call and responded by saying they are protected by their choice of law provision. “Note that this particular case is getting challenged by a lot of players in the banking industry, including the American Banking Association,” he said. “And I think it’s an unusual case, but certainly that doesn’t come back to us in that the sense that we continue to rely on choice of law provision.”

Discussion of the case has been curiously sparse on the Lend Academy forum where Lending Club and Prosper investors often go to share risks and strategies.

Meanwhile an article published on Bloomberg paraphrased comments by Gilles Gade, the CEO of Cross River Bank, when it said, “Some investors have warned they may simply shun loans to borrowers in certain states, because they either don’t yield as much or could be affected by the decision.”

The decision is only binding in three states (New York, Vermont and Connecticut), but whether or not the decision will affect investor demand for marketplace loans in these states is yet to be seen.

Personally, when I learned the appeal request was rejected, I changed my LendingRobot account configuration to stop purchasing Lending Club and Prosper notes in New York going forward. However remote the odds of a Madden related disaster, I’d rather have borrowers default because I selected bad loans than a court rule that the loans never existed…

Are you thinking twice about buying securities backed by loans that are acquired by non-bank entities? Or is it business as usual? I’m interested to hear your thoughts.

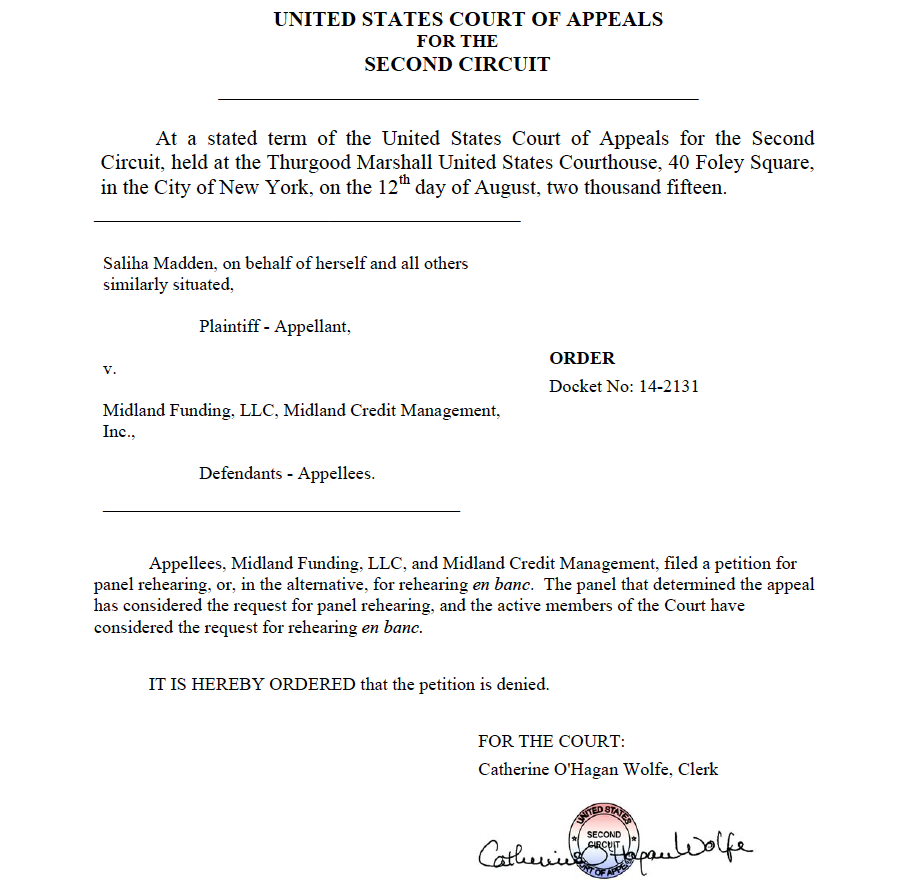

Madden v. Midland Appeal Rejected

August 13, 2015Alternative lenders might have reason to lose a little bit of sleep going forward. The United States Court of Appeals for the Second Circuit shot down a request for a rehearing of Madden v. Midland. The original ruling stated that third party debt buyers are not covered under National Bank Act pre-emption. That decision had major ramifications for alternative lenders who often rely on banks to issue the loans and then immediately sell them to the “lender” to book and service.

You can read a legal brief of the case here.

Lending Club’s CEO recently addressed this case and he explained that he believed his company would be unaffected because of their choice of law provision.

And Patrick Siegfried, Esq, the author of the Usury Law Blog, has previously said that Madden v. Midland may be the start of new usury Litigation.

Decision below:

Are Your Sales Agents or ISOs Up to Snuff? (Take Our Research Survey)

August 12, 2015If you enjoy reading deBanked’s articles, please take the time to take our short survey:

Some background:

What started as a few sensational articles about practices in small business lending and merchant cash advance is now turning into a cry for a governmental crackdown by not only observers outside the industry but lenders from inside the industry itself.

Stories that look like they’ve been written by consumer activist groups are being penned by your peers. Just recently, Fundera’s Brayden McCarthy submitted his thoughts to American Banker and the Huffington Post.

Stories that look like they’ve been written by consumer activist groups are being penned by your peers. Just recently, Fundera’s Brayden McCarthy submitted his thoughts to American Banker and the Huffington Post.

“As evidence,” he wrote. “One need only look to some lenders’ triple-digit interest rates, the proliferation of shady loan brokers and inadequate or nonexistent disclosure of price and terms. Some practices, such as brokers that brand themselves as impartial but take incentives to market certain lenders over others, resemble behavior seen in the run-up to the financial crisis.”

Along with the Treasury’s RFI, there is a mass lobbying effort to regulate the industry as fast possible. As Patrick Siegfried, Esq pointed out recently, former SBA Administrator Karen Mills recently urged the the CFPB to implement the Small Business Data Collection Rule of the Dodd-Frank Act, a law which could potentially outlaw the underwriting practices of the entire business lending and merchant cash advance industries.

There’s also been the publication of a Small Business Borrowers’ Bill of Rights and the formation of the Responsible Business Lending Coalition. And on Forbes, an interview with loan broker Ami Kassar described the industry as the wild, wild west.

As a long time participant and observer in the industry, (this is my 10th year now) I want nothing more than a bright and prosperous future for both my peers and America’s small businesses. I hope you’ll take two minutes to take our survey above.

Thanks!

OnDeck vs. IOU Financial: Are one of these lenders mispriced?

August 12, 2015 Has OnDeck’s stock price dropped so much that it’s now a buying opportunity? You’ll probably want to read this before you decide.

Has OnDeck’s stock price dropped so much that it’s now a buying opportunity? You’ll probably want to read this before you decide.

OnDeck’s IPO market cap was $1.3 billion. They funded $1.2 billion worth of loans in 2014. OnDeck’s stock has since dropped though, bringing its market cap down to around $650 million. The company is often compared to Lending Club despite their business models being completely different. But since there has been seemingly no one else to make comparisons with, the two have become star crossed lovers in a new FinTech Lending category of the market.

Everyone seems to have ignored the fact that one of OnDeck’s direct competitors is also a public company and I don’t mean a subsidiary of a giant conglomerate for which no individual comparison would be logical, but a standalone entity that is a serious player.

Kennesaw, GA-based IOU Financial (formerly IOU Central) is actually a public company in Canada, even though its only operational activities are small business loans in the U.S. The company is not a fly-by-night me-too business lender, as they funded more than $100 million in 2014 and earned a spot on the deBanked leaderboard for being one of the biggest in the industry.

OnDeck out-loaned IOU in 2014 at a ratio of 12 to 1, but here’s the kicker, OnDeck’s market cap is more than 34x the size of IOU. When converting to USD, IOU’s market cap is only slightly above $18 million.

$18 million…

That for a company that loaned $100 million last year. It’s no wonder that the perceived low market value has invited a hostile takeover bid from Russian venture capitalists. The tender offer of $15 million, presumably in Canadian dollars, would’ve acquired 55.9% of the company’s outstanding shares. The company is currently waiting for its shareholders to vote on the offer.

Meanwhile, another competitor, Kabbage, was recently valued at $875 million on loan volume last year of $400 million.

Ignoring all other factors that comprise a lender’s worth

- Kabbage was valued at more than twice its annual loan volume

- OnDeck’s IPO value was about equal to its annual loan volume, but their current market cap is almost half its annual loan volume

- IOU Financial’s current market cap is less than 20% its annual loan volume.

On these stats alone, IOU Financial seems to be incredibly undervalued, especially for a company whose spokesperson is celebrity investor and TV personality Kevin O’Leary.

OnDeck touts OnDeck marketplace as a way to sell off loans and generate income but IOU also regularly sells off its loan receivables while retaining the servicing rights just like OnDeck does.

Kabbage out-loaned IOU last year by a ratio of only 4 to 1, yet is valued almost 50x higher than IOU.

Every company has strengths, weaknesses, and reasons why they stand apart from their peers even if they look very much like them. However, given the mind blowing disparity in valuations for lenders that compete for the same customer with similar products, there surely has to be a buying or selling opportunity in here somewhere.

I think the Russian nuclear scientists are on to something…

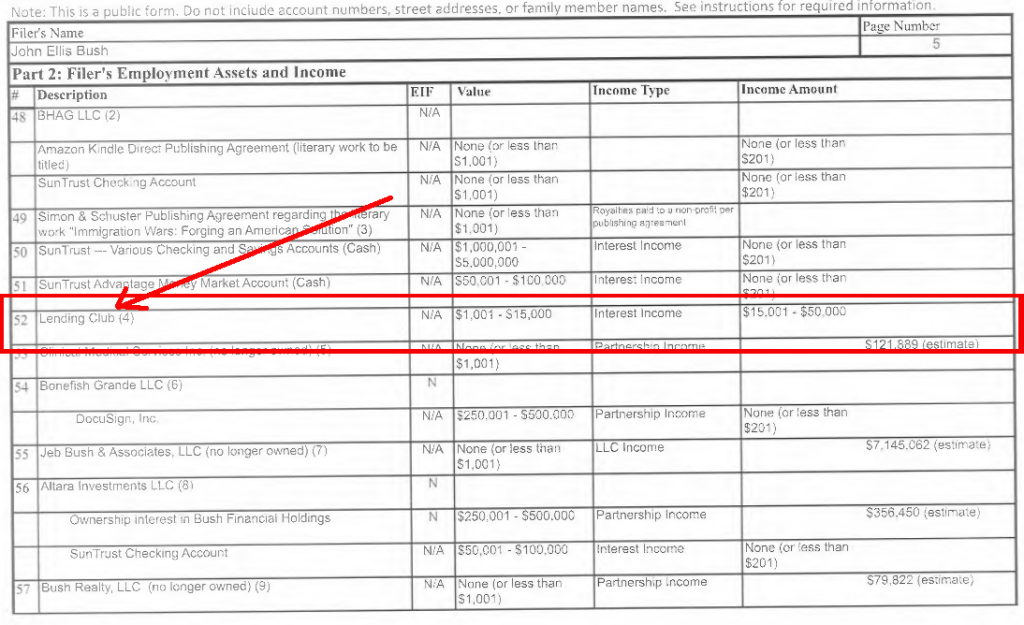

Jeb Bush Owns Lending Club Notes

August 10, 2015Former Governor and Presidential Candidate Jeb Bush recently released thirty three years of tax returns, but included in his Office of Government Ethics Form 278e was a notable asset, Lending Club notes. Lending Club stock wouldn’t earn interest income so these are clearly the notes that any investor can buy on the platform. The value of the notes held was declared to be between $1,001 and $15,000 and the interest income between $15,001 and $50,000.

ABC News was the first to mention the asset but I am posting a photo of the actual line item.

The value of the notes held are so small, one has to wonder if Bush himself did the investing.

This was also stated about the asset at the end of the packet:

And another republican presidential candidate is a big proponent of Bitcoin. Back in April, I got to meet U.S. Senator Rand Paul at a Bitcoin event in NYC.

Between Bush and Paul, the republican candidates sure are shaping up to be FinTech friendly.

Renaud Laplanche on Madden v. Midland

August 8, 2015 In case you missed the comments by Lending Club’s CEO regarding the Madden v. Midland decision, we’ve got the transcript of it from the Q2 earnings call below. A brief of that case was published on deBanked back on June 11th by lawyers from Giuliano McDonnell & Perrone, LLP.

In case you missed the comments by Lending Club’s CEO regarding the Madden v. Midland decision, we’ve got the transcript of it from the Q2 earnings call below. A brief of that case was published on deBanked back on June 11th by lawyers from Giuliano McDonnell & Perrone, LLP.

Smittipon Srethapramote – Morgan Stanley

And do you have any comments on the Madden versus Midland funding case that’s going through the court system right now in terms of how it potentially impacts your business?Renaud Laplanche – Founder & CEO

Yes, so we’ve seen that case that came out a couple of months ago. I think the –our take there is obviously the particular circumstances of the case are different from what we’re seeing on our platform. But in general what really helps us apply Utah law to most of our loans is really a couple of things. One is for the all preemption. And the second is choice of law provision in our contract. The Madden case really challenged the federal preemption but did not challenge the choice of law provision, so that’s really the – and we don’t need both, we need one of them. So we continue to operate in the Second Circuit district where that decision was rendered exactly as we did before and are relying on our choice of law provisions.Note that this particular case is getting challenged by a lot of players in the banking industry, including the American Banking Association. And I think it’s an unusual case, but certainly that doesn’t come back to us in that the sense that we continue to rely on choice of law provision. If we were to see that the choice of law provision was getting challenged elsewhere which there’s no reason to expect at this point, we could also think of a different issuance framework than the one we’re using now where we would switch to a series of state licenses. And that’s in [indiscernible] we provided in our slide deck that shows that using the current mix we have about 12.5% of our loans that would exceed the state interest rate caps.

So that certainly would be [indiscernible] demand and we’d have to revise our pricing in certain states, but that certainly would be another option available to us if our choice of law provision and federal preemption was getting challenged in other states.

On July 28th, Attorney Patrick Siegfried pointed out that the Madden case could be the start of a chilling trend after a subsequent ruling in Blyden v. Navient Corp. In that brief, he wrote, “Blyden also demonstrates that debtors that become aware of subsequent assignments of their loans may be inclined to use the assignment event as a way to invalidate otherwise legitimate debts.”

Funding Circle Breeds Bean Bags

August 7, 2015Yogibo CEO Eyal Levy saw a business loan ad for Funding Circle and applied. “The process was very smooth,” Levy said, who made a point to say that he was interviewed by an underwriter. Today, Yogibo has around 25 retail store locations and their bean bag business is booming.

Bloomberg’s Eric Schatzker expressed surprise that it wasn’t an instantaneous automated algorithmic approval that online lending has a reputation for these days. Video below:

Just like Lending Club, whose CEO appeared on Bloomberg earlier today, Funding Circle is one of the original founders of the Responsible Business Lending Coalition. They announced a “borrowers bill of rights” yesterday.

Is Online Lending the Next Credit Crisis?

August 7, 2015CIT CEO John Thain went on Bloomberg earlier to say that “some of the most leveraged lending is being pushed out of the bank space.” The comment was used to challenge Lending Club CEO Renaud Laplanche about whether or not online lending would be the next credit crisis. Laplanche answered that marketplace lending is the least levered model.”It’s a profit match between assets and liabilities, one to one,” he said.

Laplanche also said that life as a public company has been good because it’s made customers more likely to trust them and large companies more likely to partner with them.

You can listen to what he had to say in the video below:

Lending Club is one of six members that recently founded the Responsible Business Lending Coalition, which made headlines yesterday when it announced a borrowers bill of rights.