Articles by deBanked Staff

Legal Battles to Keep an Eye On

February 18, 2017CFPB

The CFPB’s organizational structure might not be unconstitutional after all. The D.C. Circuit which originally concluded it was unconstitutional, has decided to rehear the case. Oral arguments on the matter are scheduled to take place on May 24, 2017. A detailed summary of the issues can be found on The National Law Review.

TCPA law

Serial litigant Craig Cunningham is one of two petitioners behind the challenge to an FCC interpretation of what constitutes “prior express consent.” Specifically, the petitioners want to get rid of implied consent resulting from a party’s providing a telephone number to the caller. The FCC has called upon the public to comment. If the FCC indeed decides to narrow the scope of their interpretation, it would become easier for litigants like Cunningham to bring lawsuits. Read a longer brief of the issue here.

New York Lending License

Governor Cuomo’s budget proposal contains changes to Section 340 of New York’s banking law and it has the potential to completely change the alternative landscape in the state. Read a full analysis here.

Platinum Rapid Funding Group Ltd v VIP Limousine Services Inc. and Charles Cotton

After a landmark trial court decision surrounding merchant cash advance last year, plaintiff Platinum Rapid Funding Group went on to obtain a judgment against defendants in an amount exceeding $100,000. However, filed papers on the docket show the case may be heading to the Appellate Division.

Merchant Funding Services, LLC v. Volunteer Pharmacy Inc

Merchant cash advance companies may find themselves having to answer for an unfavorable ruling issued in Westchester County, New York, in which a judge vacated a Confession of Judgment and voided the underlying future receivables transaction. A more in-depth brief can be read here. Notably, the judge in that decision was the same one that decided Pearl Capital Rivis Ventures, LLC v. RDN Construction, Inc.

Lending Club Reveals Q4 Figures, $146 Million Loss for the Year

February 15, 2017

The year that shook the industry ended six weeks ago but the total damage wrought is just now coming out. Lending Club lost $146 million in 2016, $32 million of which can be attributed to Q4. But it didn’t end all that badly according to CEO Scott Sanborn.

On the earnings call he said, “our attention was focused on rebalancing our funding mix, a key step to bolster our resiliency and enable a return to growth. We set a target to help our bank partners close out their rigorous diligence, so that they could return to scale. I’m pleased to say that our efforts have paid off as not only are all of our key bank investors back buying on the platform, but we’ve also welcomed multiple new bank partners over the last few months.”

And so they’re feeling quite optimistic. “It’s an exciting time for Lending Club and I look forward to beginning the next phase of our growth,” Sanborn concluded before turning the call over to new CFO Tom Casey.

Casey went on to predict that the company would lose another $69 million to $84 million in 2017, with nearly half of that expected to be generated in the first quarter of this year.

In brighter news, the company celebrated the 10th year anniversary of their first loan and surpassed more than $25 billion in loans since inception. With close to 2 million customers-to-date, that would mean that nearly 1% of the adult population in the US has had a Lending Club loan.

Less than 10% of their loan volume is comprised of education and patient finance loans, small business loans, and small business lines of credit, according to their report.

deBanked Begins 2017 With Thickest Magazine Issue Ever

February 8, 2017 Forty-eight pages. That’s how thick deBanked’s January/February 2017 edition is. As the wider industry heads to the LendIt Conference in NYC next month, we decided it was only fitting to feature the city that never sleeps on the cover.

Forty-eight pages. That’s how thick deBanked’s January/February 2017 edition is. As the wider industry heads to the LendIt Conference in NYC next month, we decided it was only fitting to feature the city that never sleeps on the cover.

This issue delves into Equity crowdfunding, the story behind the LendIt Conference, and what it’s like to actually be a merchant getting a business loan from one of today’s fintech lenders. There’s more of course, so if you’re not already subscribed, you’ll want to make sure to do that now so that you receive this and future issues FREE.

deBanked’s chief editor Sean Murray is a LendIt awards finalist for best journalist coverage. And while there are already 30 pre-selected judges who will decide the outcome, we would like to thank everyone that has supported us and made our publication possible.

In the meantime friends, stay fresh, stay fintech, stay deBanked. The future of finance depends on it.

We’ll see you at the Javits Center for LendIt on March 6th and 7th. If you join the Small Business Lending track, you’ll actually be able to grab a copy of this issue at the conference.

OnDeck’s COO Announces Resignation Prior to Q4 Earnings

February 3, 2017OnDeck COO James Hobson notified the company on Friday that he is resigning to “pursue another opportunity.” According to the 8-K filed with the SEC, it will become effective on March 15, 2017.

Hobson started at OnDeck in 2011 and became the COO in 2012.

The announcement comes weeks before OnDeck is expected to disclose their Q4 and full-year 2016 report. In Q3, the company had shifted to keeping more loans on their own balance sheet, while increasing their reliance on third party brokers for business. They had also reported a GAAP net loss of $16.6 million for the quarter, bringing the 2016 Q1 – Q3 total losses to $47.1 million.

Google Banned Five Million Payday Loan Ads Last Year

February 3, 2017 After Google suspiciously decided to permanently ban payday lending ads from their search results last year, they had to disable more than 5 million payday loan ads, Google’s Sean Spencer wrote in a blog post. They also “took action on 8,000 sites promoting payday loans,” he said.

After Google suspiciously decided to permanently ban payday lending ads from their search results last year, they had to disable more than 5 million payday loan ads, Google’s Sean Spencer wrote in a blog post. They also “took action on 8,000 sites promoting payday loans,” he said.

For years, Google had no problem with payday lending or the advertising revenue it generated for them. In fact, in November 2013, an affiliate company, Google Ventures, even invested in a payday lending company named LendUp. But the harmony was short-lived. Eventually, Google’s search team would ban LendUp and every other payday lender from running ads on their platform after what appears to be government pressure.

- In May 2016, Google announced they would be banning payday loan ads.

- In July, that ban started to go into effect.

- In September, the CFPB announced it had taken action against LendUp, citing deceptive practices and internet ad campaigns that violated federal laws.

Google now reports having banned more than 5 million payday loan ads from that time. Other categories were worse, however. Google also had to ban 17 million ads that promoted illegal gambling and 68 million that offered bad healthcare products such as illegal pharmaceuticals.

Some ads still sneak through or try to sneak through. “Bad actors know that ads for certain products—like weight-loss supplements or payday loans—aren’t allowed by Google’s policies, so they try to trick our systems into letting them through,” Google’s Spencer wrote. “Last year, we took down almost 7 million bad ads for intentionally attempting to trick our detection systems.”

LendUp, the company Google Ventures invested in, is still in business.

Meet the Online Lender That’s Made $100 Billion in Loans

January 31, 2017Here’s a milestone for you, loanDepot has funded more than $100 billion in loans since they were founded in 2010. Mortgage loans may have enabled them to hit such a higher number in a short amount of time, but they also have a robust personal loan business. The two have more in common than you might think.

One trend that loanDepot CEO Anthony Hsieh shared when he spoke at the Marketplace Lending & Investing Conference back in September, is that since the Great Recession, borrowers that would have traditionally sought a home equity line, have instead been applying for personal loans. They know this because the credit and financial profiles between their home loan borrowers and personal loan borrowers is virtually identical, Hsieh said.

loanDepot celebrated making $100 billion in loans by publishing this video. Have a look:

Trump’s Two-For-One Regulation Deal

January 31, 2017Trump’s newest order is that for every new regulation proposed, two must be identified for repeal. If a new regulation goes into effect, the costs must be offset by the repealed regulations. The idea behind it is to strip away costs on small businesses and unburden the system. “There will be regulation, there will be control, but it will be normalized control where you can open your business and expand your business very easily,” Trump said prior to signing the executive order. Watch that below:

Trump later said that “Dodd-Frank is a disaster” and that “We’re going to be doing a big number on Dodd-Frank.”

When he does that “big number,” he should pay close attention to Section 1071 of the law, which many believe the CFPB will try to use to police commercial finance and business-to-business transactions.

Ironically, as Trump works to slash federal rules, states will likely be doing just the opposite. Already in New York, Governor Cuomo’s 309-page budget proposal includes edits to an existing law that would impose strict regulations on all non-bank business finance.

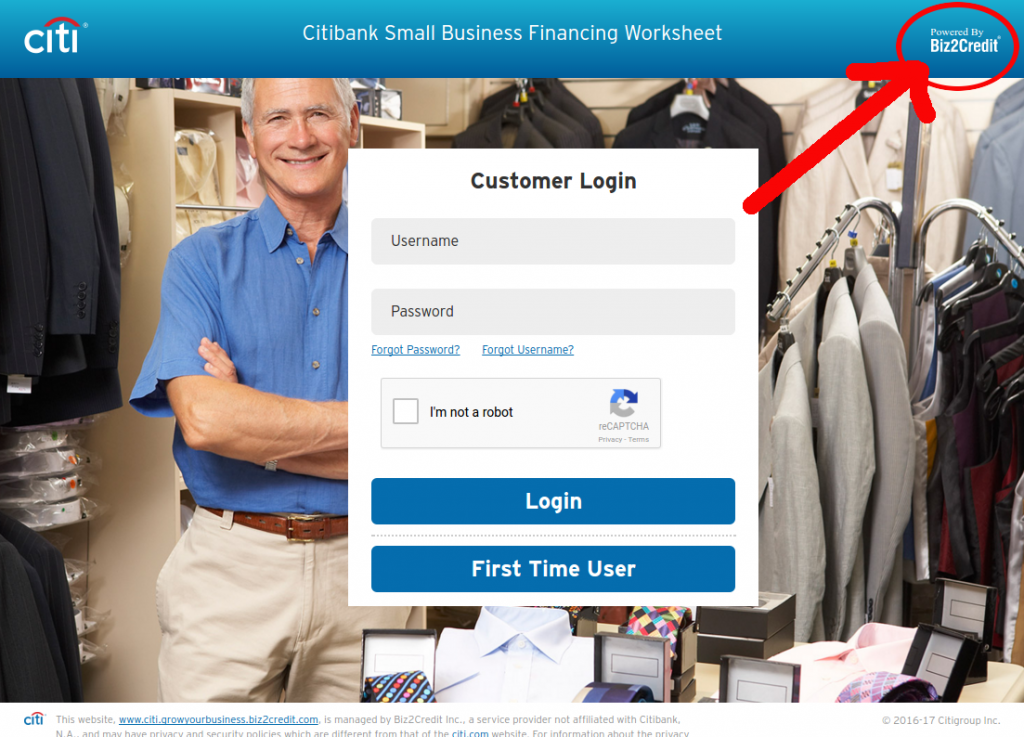

Biz2Credit – Citigroup Small Business Loan Partnership Spotted

January 27, 2017Business Insider revealed that Biz2credit and Citigroup have quietly partnered up on a website to make small business loans up to $1 million. There was no actual link to it, so we’ve found it ourselves.

The link appears in several areas of Citi’s website under the small business finance category and that brings you here:

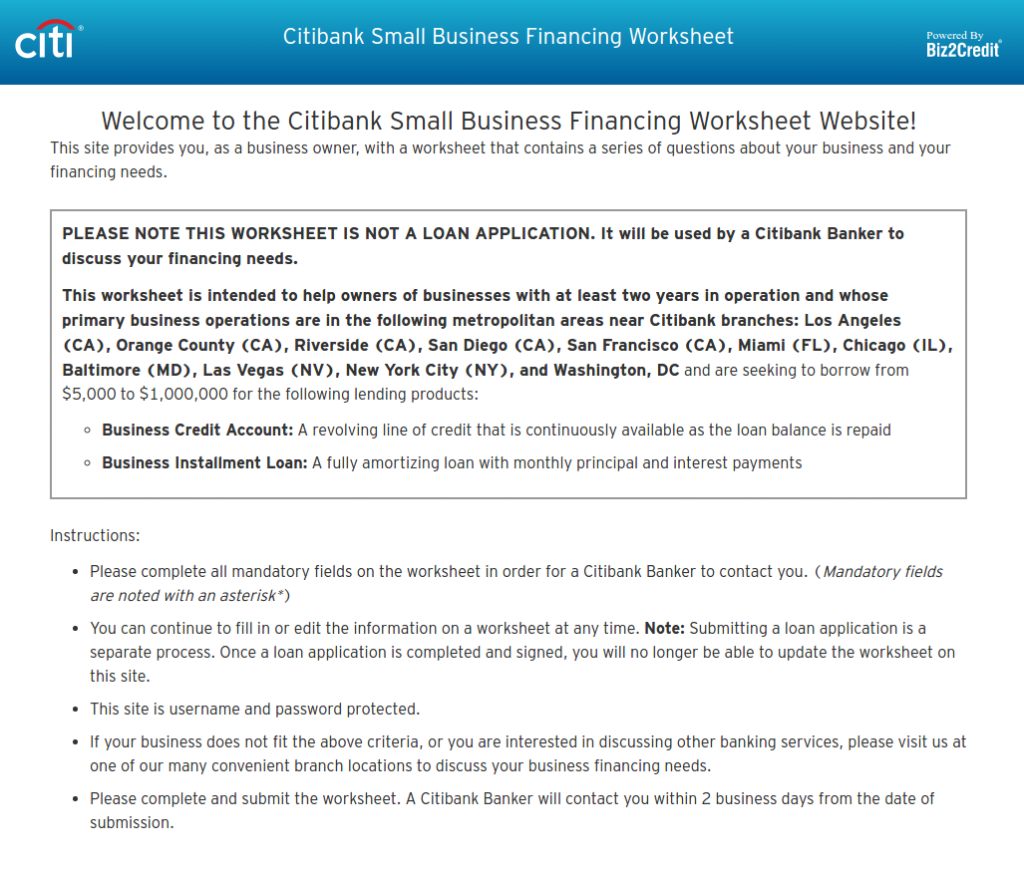

When you go to register, a page pops up insisting that this isn’t a loan application, but rather just a “worksheet” to have a banker from Citi call you within 2 days. “It will be used by a Citibank Banker to discuss your financing needs,” it reads.

The worksheet asks for very basic information such as name, business name, address, annual revenue, and financing requested.

If this doesn’t sound overly advanced, perhaps that’s why it’s being kept on the down low. According to Business Insider, Biz2credit CEO Rohit Arora said they have chosen not to publicize the effort because it’s in the very early stages.

The cat’s out of the bag now…