Archive for 2018

Uplyft Capital Launches New Brand Identity, Putting its Business Friendly Technology Capabilities at the Forefront

May 29, 2018

Uplyft Capital, a technology-focused cash advance company today announced the launch of its new brand identity. The redesign emphasizes the company’s utilization of business-friendly technology solutions to improve communication, underwriting and servicing for its clients.

“Cash Advance companies in the US are broken and inefficient. We launched Uplyft in 2012 with one simple strategy in mind – to actually make receiving working capital simple, intuitive and human. We stand with our small business clients and we believe that technology can significantly improve the funding process. As we transition from a strictly human-based approach to a hybrid AI-driven model we believe we can service both Clients and Sales Partners more efficiently. Uplyft Capital is now better positioned to serve our growing and diverse client base,” said Michael Massa, Uplyft Capital CEO and Founder.

“The small business funding marketplace is changing quickly and we knew that we needed to transform with it. As we continue to grow, we want to provide improved capabilities for our trusted consumers, sales partners, and investors.

Uplyft Capital’s new logo visually exhibits the changed brand. Using a soft purple as its base for the icon, the lowercase “uplyft capital” wordmark is a more minimal and modern than the previous design. Uplyft Capital’s new icon plays with the “arrow in upwards growth” for small businesses, looking to get out of the current box they are in, a playful hearkening to Uplyft Capital’s mission to help the growth potential of each client.

“Uplyft Capital’s remarkable new identity is a product of focused research, strategy, and execution. We believe it perfectly conveys the foundational brand values of a modern, technologically-focused company adept and capable of tackling the future of small business funding, ” said Mr. Massa.

With the announcement of the rebrand, Uplyft Capital’s has also redesigned its consumer-facing user experience to better help customers and partners stay organized and efficient. With this redesign, users will find an improved user experience, particularly on mobile, with more natural and easy-to-use features with overall better reporting and tracking tools.

IOU Planning for 25%-30% Originations Growth

May 29, 2018IOU Financial CEO Phil Marleau spoke confidently this afternoon on a public conference call to discuss the company’s first quarter performance. The company had a net income of $797,198 from the start of the year to March 31, which is notable because it produced a $995,085 loss during the same period last year.

On the call, Marleau said that the company plans to increase loan originations next year by 25 to 30 percent.

An analyst at TD Wealth asked if the company’s plan for a 25 to 30 percent increase in loan originations should produce a similar increase in earnings.

“We’re working on getting our numbers back on a growth trajectory,” Marleau said. [To do this…] we may need to increase marketing spend in order to increase the direct channel and the referral channel.”

Marleau explained that IOU Financial has three channels: the wholesale sales channel, which is responsible for the bulk of its business, the direct channel, which is driven by marketing, and the referral channel, which involves strategic partnerships with associations, payment processors, suppliers to small businesses and others. The company makes business loans of up to $300,000.

“We’re not going to lose sight of the bottom line,” Marleau said. “We’re not going to grow at the expense of profit.”

Another question came in asking what the status was on the company’s strategy of taking aggressive legal action against merchants that default on loans. President and Chief Operations Officer Robert Gloer answered this question by noting that once a lawsuit is filed against a merchant, it generally takes about a year for any money to be recovered. But the company has recovered money from defaults.

“We have started to see recoveries and we see that as a huge success,” Gloer said.

Another question dealt broadly with alternative financing in Canada as opposed to elsewhere, like the US. Marleau said that compared to the US, there is a lot less competition in Canada and that there are higher margins and usually fewer defaults.

IOU Financial is headquartered in Montreal and has an office in Kennesaw, GA.

IOU Financial Has Profitable Q1

May 29, 2018 IOU Financial reported a net income of $797,198 (CAD) in Q1, according to their latest quarterly financial statements. Despite primarily lending to US-based small businesses, IOU is headquartered in Canada, where the company is listed on the TSX Venture Exchange. IOU’s market cap at the market’s close on Friday, was less than $15 million. For comparison’s sake, rival small business lender OnDeck, currently has a market cap of $438 million.

IOU Financial reported a net income of $797,198 (CAD) in Q1, according to their latest quarterly financial statements. Despite primarily lending to US-based small businesses, IOU is headquartered in Canada, where the company is listed on the TSX Venture Exchange. IOU’s market cap at the market’s close on Friday, was less than $15 million. For comparison’s sake, rival small business lender OnDeck, currently has a market cap of $438 million.

IOU originated $24.5M (CAD) in loans in Q1, up $2.5M from the same period last year. $21.8M of those loans were sourced “via relationships with third-party business loan brokers,” according to their report.

The company proudly noted a 50% reduction in their provision for loan losses. “This decrease is primarily attributable to lower defaults by borrowers as well as by the smaller size of the loan portfolio,” the report said. “The improvement in the provision for loan losses (net of recoveries) is a result of changes made in 2017 in the Company’s lending policies and in the loan servicing and collection process, which includes an aggressive litigation strategy against businesses who default on their loan obligations.”

In a published statement, IOU CEO Phil Marleau said, “Following the positive results in the fourth quarter of 2017, IOU has delivered even stronger results in the first quarter of 2018. This is a testament to the measures taken to bring down loan defaults and control costs. IOU expects to continue to grow loan originations and generate profits over the coming quarters.”

GreenSky Lists on the Nasdaq

May 25, 2018 Yesterday, GreenSky announced its initial public offering of 38,000,000 shares of Class A common stock at $23.00 per share. The shares of common stock now trade on the NASDAQ under the symbol “GSKY” and are valued at $24.77, as of the close of trading today.

Yesterday, GreenSky announced its initial public offering of 38,000,000 shares of Class A common stock at $23.00 per share. The shares of common stock now trade on the NASDAQ under the symbol “GSKY” and are valued at $24.77, as of the close of trading today.

GreenSky facilitates point-of-sale financing that enables over 12,000 merchants to offer easy payment options to over 1.7 million consumer customers. Valued at $4.4 billion, according to Trefis, an independent financial data company, it is among the largest fintech companies in the lending space. But it is not a lender. Instead, it facilitates loans through its proprietary technology for prime and super prime borrowers to make high priced purchases. GreenSky’s merchant partners include home improvement businesses and clinics that offer costly elective medical procedures. The average FICO score of a GreenSky borrower is 760.

“Our roadmap to capture growth opportunities and deliver profitability to our shareholders is clear: continue to grow our current business, expand our network of merchants, enter new verticals, and broaden the solutions we offer to both businesses and consumers,” said GreenSky CEO David Zalik following the company’s IPO.

Zalik founded the company in 2006 and has kept a pretty low profile until the growth of GreenSky made it difficult for him to remain obscure. According to a September 2016 interview with Bloomberg, Zalik, whose company was then valued at $3.6 billion, said he had never given an interview before.

His personal story is as impressive as his company’s. He came to the U.S. from Israel when he was four and grew up in Alabama. Because of remarkably high standardized test scores, he started taking classes at Auburn University (in Auburn, AL) when he was 12, according to the same 2016 Bloomberg story. He sold his first company for a few million dollars when he was 22, at which point he moved to Atlanta.

In 2016, Zalik was the winner of the Ernst & Young Entrepreneur of the Year award for Financial Services. In his acceptance speech he said:

“My family and I came to this country in 1978 with two suitcases, and the dream of America. I am the child of two generations of refugees, and a proud American. This country has given my family everything. Freedom of opportunity [and] freedom from fear.”

GreenSky is based in Atlanta and employs more than 600 people. The company was unable to provide comments in time for this story’s publication.

New Law Benefits Small Banks

May 24, 2018 President Trump signed into law today the Economic Growth, Regulatory Relief and Consumer Protection Act, which pares down Dodd-Frank regulations for thousands of small and medium-sized American banks. Dodd-Frank refers to the 2010 Dodd-Frank Act, which instated laws to regulate the risky behaviors of banks that led to the 2008-2010 financial crisis.

President Trump signed into law today the Economic Growth, Regulatory Relief and Consumer Protection Act, which pares down Dodd-Frank regulations for thousands of small and medium-sized American banks. Dodd-Frank refers to the 2010 Dodd-Frank Act, which instated laws to regulate the risky behaviors of banks that led to the 2008-2010 financial crisis.

Among the changes this new law makes to Dodd-Frank is reducing the number of banks that are subject to strong government oversight because they are considered “systemically important.” Banks with assets of $50 billion or more had been considered “systemically important.” As of today, only banks with assets of $250 billion or more will get that moniker and be subject to the strictest government regulations.

In addition to this, small banks – generally with assets of $10 billion or less – will now be much freer to originate residential mortgages. And they will have to comply with fewer regulations in general.

“There are simplifications in [this law] that change the capital costs for smaller banks,” said Dodd-Frank expert and Senior Counsel at Morrison & Foerster, Oliver Ireland. “By lowering the cost structure of the bank, you may facilitate lending at either lower rates, or more lending.”

Ireland said that there is no way to quantify this, but acknowledged that small banks will be in a stronger position with this new law in place. As for the effect of the new law on alternative lenders, Ireland didn’t predict anything at all dramatic.

Still, he said, “There are a number of provisions in here that make the cost of being a small bank somewhat less. That may put them in a better position to compete with non-bank lenders.”

Why Small Businesses Sought Financing in 2017, and Why They Were Denied

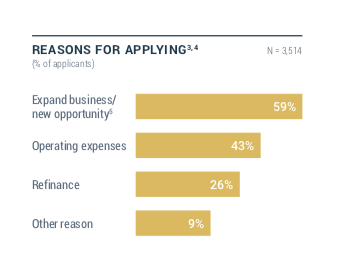

May 24, 2018 Nearly 60 percent of small businesses applied for financing in 2017 because they wanted to expand their business or pursue new opportunities, according to the latest report by the Federal Reserve. Forty-three percent of small businesses sought financing for operating expenses while 26 percent sought capital for refinancing. Nine percent had a different reason.

Nearly 60 percent of small businesses applied for financing in 2017 because they wanted to expand their business or pursue new opportunities, according to the latest report by the Federal Reserve. Forty-three percent of small businesses sought financing for operating expenses while 26 percent sought capital for refinancing. Nine percent had a different reason.

Of course, not all applications are funded. Forty-six percent of small businesses received all the financing they sought, 12 percent received most (more than 50 percent) of it, 20 percent received some (less than 50 percent) of the financing they desired and 23 percent were denied financing altogether.

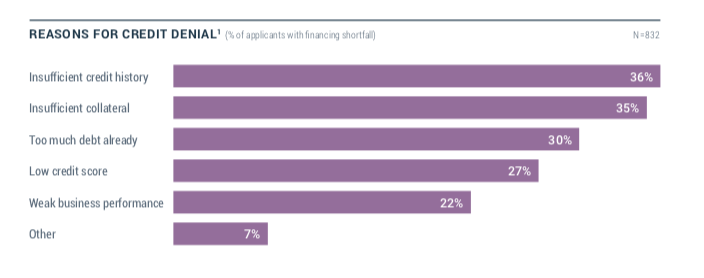

Of the reasons why merchants were denied funding, “Having insufficient credit history” ranked number one, according to the report. A very close second was “Having insufficient collateral,” followed by “Having too much debt already.” After that, in descending order, came “Low credit score,” “Weak business performance” and “Other.”

The “Having insufficient collateral” category does not apply for MCA financing, but the other categories do. According to Nick Gregory, founding partner at Central Diligence Group, which provides MCA underwriting services, “Having too much debt already” is perhaps the main reason why merchants seeking cash advances get declined.

“A lot of times the merchants are overleveraged,” Gregory said.

He explained that if a merchant also has something like two MCA arrangements (or positions) already, that merchant likely has taken on too many contractual obligations which will often be a reason to decline the application. In Gregory’s experience, another common reason for declining an MCA financing application is “Weak business performance.”

Contradictory to the Federal Reserve report’s top reason for denying financing to a small business borrower, Gregory said that “Having insufficient credit history” is seldom a reason to deny MCA financing. This disconnect likely comes from the fact that the report includes all types of small business financing, with MCA accounting for just seven percent. The number maybe seem small, but it continues to increase while small business applications for factoring have decreased.

More Small Businesses Seeking Merchant Cash Advances Than Factoring

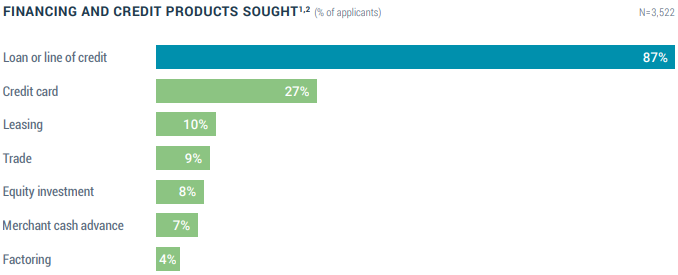

May 23, 2018 Seven percent of small employer firms in the US that applied for financing in 2017 applied for a merchant cash advance, the latest report by the Federal Reserve shows, while only 4% applied for factoring. Small employer owned firms were defined as businesses that have 1 to 499 full-or part-time employees. 69% of those surveyed generated less than $1 million in revenue last year. That revenue demographic may be on the low end for the factoring industry though. Factoring’s popularity in that demographic, however, decreased in 2017, according to the report. The 4% figure of small businesses that applied for factoring in 2017 was down from 7% in 2016.

Seven percent of small employer firms in the US that applied for financing in 2017 applied for a merchant cash advance, the latest report by the Federal Reserve shows, while only 4% applied for factoring. Small employer owned firms were defined as businesses that have 1 to 499 full-or part-time employees. 69% of those surveyed generated less than $1 million in revenue last year. That revenue demographic may be on the low end for the factoring industry though. Factoring’s popularity in that demographic, however, decreased in 2017, according to the report. The 4% figure of small businesses that applied for factoring in 2017 was down from 7% in 2016.

Auto and equipment loans had the highest approval rates among all financing options available to small businesses, at 82%. Merchant cash advances followed behind them at 79%. Lines of credit and business loans carried approval rates of 69% and 62% respectively. SBA loans came in at 54%.

When it comes to satisfaction, online lenders such as Lending Club, OnDeck, CAN Capital, and PayPal, have markedly improved over time, the report shows. The net satisfaction score of online lenders has increased from 19% in 2015 to 35% in 2017.

On transparency, online lenders rank at about the same level as large banks, though applicants were more likely to be dissatisfied with the interest rates of an online lender and the long and difficult application process with a large bank.

BFS Co-founder Returns as Temporary CEO

May 23, 2018 Chairman and co-founder of BFS Capital Marc Glazer has assumed the role of Interim CEO. The former CEO, Michael Marrache, is no longer at the company.

Chairman and co-founder of BFS Capital Marc Glazer has assumed the role of Interim CEO. The former CEO, Michael Marrache, is no longer at the company.

“We’re on a nationwide search to find an individual that we feel will be an excellent candidate to continue BFS’s track record as a market leader and help grow the company,” Glazer said.

Founded in 2001, BFS is a veteran in the merchant cash advance industry. More than five years ago, the company began offering a business loan product, which now accounts for more than half of its revenue.

Glazer told deBanked that when BFS started offering its loan product, it widened its customer base significantly such that a sizable percentage of its customers are now business to business companies. Glazer said that MCA funding would not work for these kinds of customers because many of them get paid by check or get paid in larger amounts, but not on a daily basis.

Glazer said that working with ISO partners has always been a critical part of the BFS business model. What does Glazer look for in an ISO?

“Ultimately, you want to work with ISOs that view the relationship with not only the funder, but the merchant, [in mind,]” he said. “We look at ourselves as a responsible funder and put out offers that we not only think help the merchant, but that have payment terms that the merchant can afford. And the ISOs that we look for are ones that do the same kind of matching with the merchant.”

BFS has funded 400 different types of merchants, from florists to nail salons. But Glazer said that a big portion of the company’s customer base comes from either the hospitality industry or parts of the construction industry, including plumbing. To date, BFS has delivered more than $1.75 billion in total financing to small and mid-sized businesses, including $300 million funded in 2017. Loans are typically offered through the company’s banking partner, Bank of the Internet, according to Glazer.

BFS is headquartered in Coral Springs, FL and has an office in New York and one in southern California. It also includes a wholly owned subsidiary in the UK called Boost Capital. Altogether, BFS employs about 200 people with the majority of employees at its Florida office.