Archive for 2018

Prime and Non-prime Lenders Exchange Notes

October 25, 2018 Ken Rees, CEO, Elevate

Ken Rees, CEO, ElevateAt Money 20/20 Ken Rees, CEO of Elevate, a non-prime consumer lender, sat down with David Kimball, CEO of Prosper, a prime consumer lender. As they discussed a number of topics, listeners got insight into how these lenders think, and how they think differently based on the customers they serve.

On Partnering with Banks

Rees said that he is eager to partner with banks and that banks have spoken to him about a gap they have – namely, the fact that they have thousands, if not millions, of checking account customers with low Fico scores for whom they have no other products to offer. Elevate has products for these banks’ non-prime customers.

“Banks have customers and we want to work with them,” Rees said.

Rees said that the very large banks may have the resources to develop new products on their own, but that there are thousands of mid-sized banks to partner with.

Kimball, who was CFO of USAA Federal Savings Bank, had some advice for fintechs on how to approach a potential partnership with a bank.

“Don’t go in thinking they’re stupid,” he said. “Assume that you have a really good partner.”

Furthermore, Kimball said that having worked at a bank during the recession, “when you break things, regulators aren’t so happy to work with you again.” By this, he meant that bankers may have very legitimate concerns about taking on risk by working with a fintech company.

Kimball continued, “You need a good champion at the right level [at a bank] to move you forward.”

David Kimball, CEO, Prosper

David Kimball, CEO, ProsperOn a Looming Recession

Kimball said that Prosper is being more conservative with its underwriting now. On the other hand, Rees said that a recession doesn’t concern him as much.

“Our customers are always living in a recession,” Rees said.

On Speed vs. Rate

“For prime customers, it’s all about rate. For non-prime, it’s all about speed, how fast they can get the money,” Rees said.

On Marketing

Kimball said that direct marketing still works best to get new customers, while Rees mentioned a new geo-marketing tool that alerts Elevate when a potential customer approaches a payday lending shop. Someone visiting a payday lending shop would likely be a good customer for Elevate. Rees conceded that “this could be kind of creepy.” But it’s a new approach.

Shopify Capital Issued $76.4M in Merchant Cash Advances in Q3

October 25, 2018Shopify Capital, Shopify’s funding arm, issued $76.4 million in merchant cash advances in the third quarter, the company revealed. That brings the total to $375 million advanced since April 2016.

Overall, the company reported Q3 revenue of $270.1 million and a net loss of $23.2 million.

The company operates an e-commerce platform for online stores and retail POS systems.

Heard at Money 20/20

October 24, 2018Shaquille O’Neal, Basketball legend and startup investor

O’Neal appeared at the conference on behalf of Steady, a startup he supports that helps people find work relevant to their skill set and location.

“I like being involved in companies that help people people,” O’Neal said. “With Steady, we want to help people gain income. It shouldn’t be hard to find work.”

When asked about other companies he involved with, he said, “I listed all the companies once and my mom said, ‘It sounds like you’re bragging, so cut it out.’ So I don’t talk about them anymore, because my mom’s out in there in the audience somewhere.”

Basketball Legend and Advisor & Advocate of @thesteadyapp, @SHAQ reveals his new nickname at the final of the Startup Pitch at #money2020 pic.twitter.com/ZhDGbCi9DN

— Money20/20 (@money2020) October 24, 2018

Rob Frohwein, Kabbage Co-founder

Frohwein said his company noticed that its customers were borrowing a little less money after they were issued Kabbage’s card.

“It was because customers were borrowing the exact amount they needed at the point of purchase.”

At first, Frohwein said they were concerned, but that ultimately “customers aren’t over-borrowing…and that’s excellent for customer loyalty.

Anthony Noto, SoFi CEO

Noto said he went to West Point for college, which was completely free for him. He said that he could have gotten student loans to attend other prestigious colleges, but he didn’t know if he could afford to pay it back.

With regard to how higher interest rates are affecting SoFi, he said, “higher interest rates have made our underwriting more conservative [and have forced us] to focus on quality.”

On the topic of potentially becoming an Industrial Loan Company (ILC) bank:

“An ILC could be in our future so that we have the same rates across all states we operate in…We are regulated and we’re comfortable with that.”

Breslow Shows What a Fintech/Bank Partnership Looks Like

October 24, 2018 In the wake of OnDeck’s announcement of ODX, a new subsidiary that will service banks, OnDeck CEO and Money 20/20 veteran Noah Breslow took to the stage for a discussion with his new business partner, Lakhbir Lamba, Head of Retail Lending at PNC Bank. PNC will now be using ODX to originate lines of credit for the bank’s small business customers, while everything will stay on PNC’s balance sheet.

In the wake of OnDeck’s announcement of ODX, a new subsidiary that will service banks, OnDeck CEO and Money 20/20 veteran Noah Breslow took to the stage for a discussion with his new business partner, Lakhbir Lamba, Head of Retail Lending at PNC Bank. PNC will now be using ODX to originate lines of credit for the bank’s small business customers, while everything will stay on PNC’s balance sheet.

“We’re keeping a laser focus on small business lending,” Breslow said, when asked if OnDeck would begin to serve other segments of the market, like student or auto loans.

“The problems that small businesses face are worldwide,” Breslow said, indicating that the company has interest in expanding service to small businesses internationally. Already, OnDeck operates in Canada and Australia.

The moderator asked if an application that is rejected by PNC would become a lead for OnDeck. Breslow and Lamba said that is not currently the arrangement, but that it may be a possibility.

“Our goal [with ODX] is to service banks,” Breslow said, while acknowledging that banks serve a different kind of small business customer than OnDeck.

“We will make sure that we underwrite based on PNC’s risk appetite,” Breslow said.

Is Small Business Lending Stuck in the Friend Zone?

October 23, 2018 Small-business owners have lots of places to go for capital, and the alternative small-business funding industry doesn’t exactly top the list, recent research shows. In fact, entrepreneurs claim they’re more than four times as likely to receive funding from a friend or family member than from an online or non-bank source.

Small-business owners have lots of places to go for capital, and the alternative small-business funding industry doesn’t exactly top the list, recent research shows. In fact, entrepreneurs claim they’re more than four times as likely to receive funding from a friend or family member than from an online or non-bank source.

That bit of intelligence comes from the National Small Business Association‘s 2017 Year End Economic Report, the most recent from the Washington-based trade group. Thirteen percent of the entrepreneurs who responded to the survey received loans from family or friends in the preceding 12 months, while 3 percent obtained funding from online or non-bank lenders, the report says.

But some variables come into play. Shopkeepers and restaurateurs are more likely to rely on friends and family for financing during their first five years in business, says Molly Brogan Day, the NSBA’s vice president of public affairs and a 15-year veteran of the survey. The association’s members, who account for many – but not all – of the respondents tend to have been in business longer than non-members so the actual percentage of all owners receiving funds from family or friends could well be higher than the survey indicates, she notes.

In fact, the average NSBA member started his or her business 11 years ago – a fairly long time for the sector, Day says. The association attracts well-established merchants partly because the trade group concentrates on advocacy and lobbying in the nation’s capital, Day notes. “There’s not a lot of networking, there’s not a ton of resources or educational offerings,” she says of the association. In other words, the organization’s emphasis tends to attract prospective members who have been in business long enough to see the results of laws and regulation instead of newcomers still struggling daily to establish themselves, she observes.

Anyway, it’s also worth noting that small-business owners appear nearly as likely to approach family or friends for cash as to petition large banks for funding, Day says, noting that 13 percent turn to friends and family, while 15 percent manage to obtain loans from large banks. To her, that indicates that banks just aren’t lending to small businesses as frequently as they should – a notion that should sound familiar to anyone in the alternative small-business funding industry.

Unsurprisingly, the association’s research indicates bank lending declined as the Great Recession made itself felt in 2007 and 2008. Before that, nearly 50 percent of merchants responding to the survey reported they had recently qualified for loans from big banks, small banks or credit unions, the research shows. “Now it’s pretty consistently a percentage in the low 30’s,” Day says. “People really need these loans.”

Lending by banks hit another snag in 2012 when new regulation and legislation, including the Dodd-Frank Wall Street Reform and Consumer Protection Act, made itself felt. “There was such a massive overcorrection in the banking industry that it’s still really difficult for small businesses to get loans,” Day says.

Moreover, banks were granting fewer “character-based” loans even before the double whammy or recession and regulation, Day observes. Instead of employing the older practice of assessing the intangible virtues of a business owner well-known in the community, bankers began applying a more formulaic approach to evaluating loan applications based on credit scores and other quantifiable variables, she says.

That switch to numbers-oriented decisions proved detrimental for many entrepreneurs. “A lot of small business owners don’t look great on paper,” Day admits. Even a great business plan might not convince bankers to loosen their purse strings these days, she notes.

That’s where the alternative small-business funding industry comes into the picture. NSBA researchers began including the category of online and non-bank lenders in their surveys in 2013 and have seen the percentage of respondents using them grow each year to its current level of 3 percent.

“It’s not huge growth, but it’s notable,” Day says. Notable enough to achieve importance, she continues. “It’s an important opportunity for your readers to fill that void,” she says of the shortfall of adequate small business funding. “They’ve been doing a pretty good job of doing it.”

In fact, the NSBA research indicates that alternative funding and other sources have tended to take up the slack created by the banking industry’s decision to exercise extreme caution when evaluating small business loans. Some 73 percent of small business owners are obtaining enough financing these days, according to the survey.

Yet hiccups have occurred, like the decline to only 59 percent finding adequate funding in 2010, Day points out. And the fact that two-thirds to three fourths are generally securing adequate funding means that a fourth to a third aren’t, she notes, adding that she urges focusing on the latter group. “It’s concerning,” she says.

Inadequate funding can prove especially challenging for newer businesses that don’t have a track record, haven’t stockpiled proceeds from past operations, don’t own stock to leverage and aren’t savvy enough to finesse placement of debt, Day maintains. More-established businesses have greater access to those resources or have honed those skills, she notes.

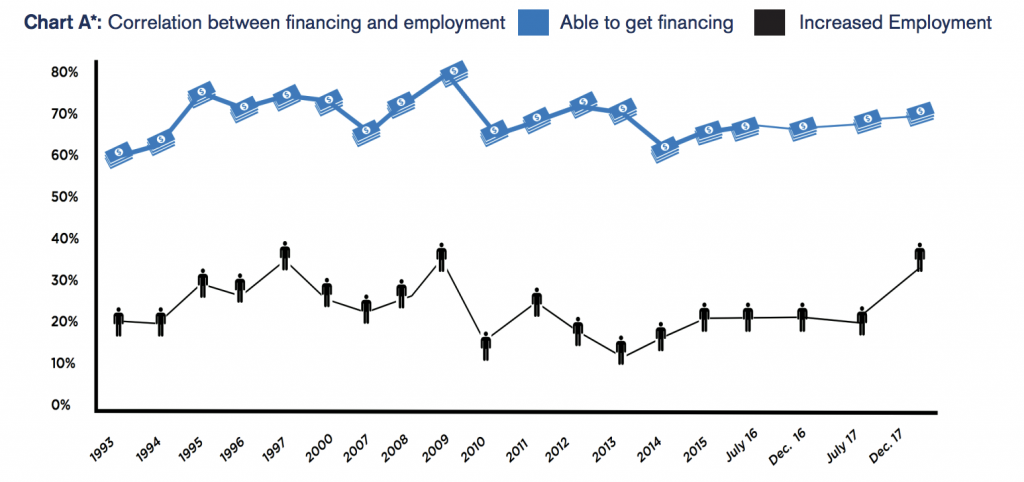

And much is at stake. Lack of funds not only hurts that significant portion of small-business owner but also prevents hiring workers, stymies economic growth and hinders community development, Day maintains. She points to research that shows the nearly direct correlation between availability of capital and increases in hiring. (See Chart A.)

And much is at stake. Lack of funds not only hurts that significant portion of small-business owner but also prevents hiring workers, stymies economic growth and hinders community development, Day maintains. She points to research that shows the nearly direct correlation between availability of capital and increases in hiring. (See Chart A.)

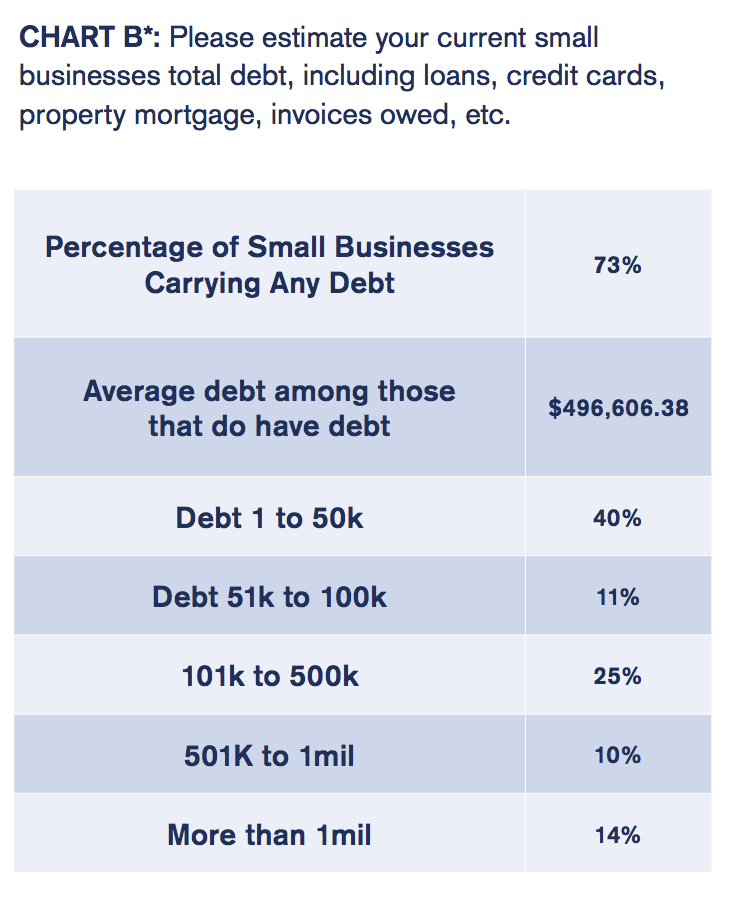

Other NSBA findings include the fact that in July of 2017 merchants reported having debt that averaged $496,000. Some 73 percent of those reported had at least some debt. Some 40 percent of survey respondents, the largest category have debt of $50,000 or less. (See Chart B.)

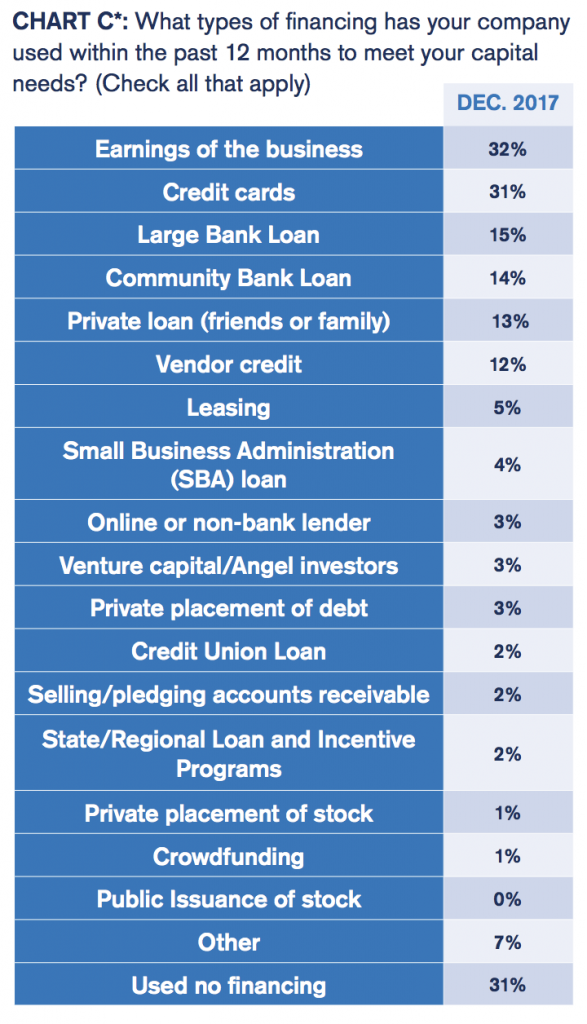

Financing most often comes from funds the business has earned, the trade group says. Some 32 percent of merchants cite that source. Yet simply pulling out a credit card remains a common way to make ends meet, with 31 percent saying they did that to meet capital needs in the last 12 months. (See Chart C.)

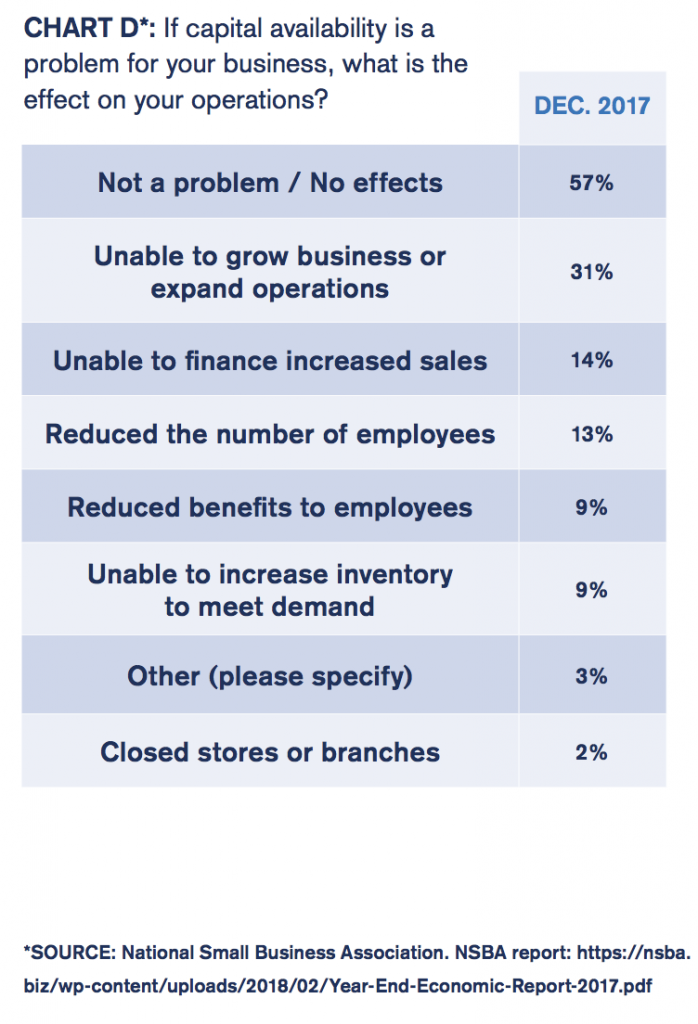

While most (57 percent) say that lack of capital hasn’t hurt their enterprises recently, 31 percent say a dearth of capital prevented them from expanding their operations, 14 percent report they weren’t able to expand their sales because they lacked funding, and 13 percent admit they laid off employees because it was difficult to find the cash to meet the payroll. (See Chart. D)

While most (57 percent) say that lack of capital hasn’t hurt their enterprises recently, 31 percent say a dearth of capital prevented them from expanding their operations, 14 percent report they weren’t able to expand their sales because they lacked funding, and 13 percent admit they laid off employees because it was difficult to find the cash to meet the payroll. (See Chart. D)

The availability of credit hadn’t changed much in the year leading up to the survey, the association says. About 77 percent reported no change in their lines of credit or credit cards, while 18 percent saw their perceived creditworthiness increase and 5 percent saw it decline.

Those results come with a bit of history. The NSBA has been surveying small-business owners since 1993. At first, the trade group hired polling companies to perform the task and cooperated on the report with the Arthur Andersen accounting firm. Computerization enabled the association to take the project in house beginning in 2007. It works on the survey with ZipRecruiter, an online employment marketplace.

Some 1,633 small-business owners participated in the research for the 2017 Year End Economic Report by answering 42 questions online in December 2017 and January 2018. Many of the survey questions have remained the same over the years to facilitate comparisons and tracking.

Some 1,633 small-business owners participated in the research for the 2017 Year End Economic Report by answering 42 questions online in December 2017 and January 2018. Many of the survey questions have remained the same over the years to facilitate comparisons and tracking.

Small businesses on the list of members and the list of non-members receive two email messages alerting them to the survey and providing an online link to the questions. The surveys take place twice a year.

As mentioned earlier, some survey respondents belong to the association and some don’t, but Day was unable to pinpoint the percentages. In response to a question from deBanked, she said she may begin tallying how many respondents are members and non-members because non-members tend to have been in business for a shorter time than members. Non-members also tend to differ from members because political engagement often brings the former to the association’s attention.

Participating merchants come from every industry and every state, Day says. Manufacturing and professional services are very slightly overrepresented, while mining is the only category that’s scarcely represented, she admits. Not many small businesses operate in the mining sector, she adds.

PayPal is Changing Its Ways, Embracing Main Street

October 23, 2018 PayPal Chief Operating Officer Bill Ready shared his childhood experience of working for his parents’ auto repair shop to convey his understanding of the challenges that face small businesses.

PayPal Chief Operating Officer Bill Ready shared his childhood experience of working for his parents’ auto repair shop to convey his understanding of the challenges that face small businesses.

“Tech has gotten faster, but money has gotten slower,” he said, referring to how small businesses, like his parents’, used to receive most of its money right away in cash. “Now, money is tied up in the digital world and it can take days, even weeks [to collect.]”

Ready said that, through PayPal, small business owners can get their money immediately. He also said that some small business owners can get loans from PayPal almost instantly. He gave the example of a business owner in Arizona with a staff of 12 who couldn’t get a loan from a bank because his company didn’t have assets. But the company did have a payment history with PayPal which qualified it for a small business loan that Ready said hit the owner’s account in 30 seconds.

Not all of Ready’s presentation touted the company’s capabilities. Part of his talk had an apologetic tone.

“Paypal was hesitant about partnerships, but not anymore,” he said, acknowledging that helping “Mainstreet” will require the collaboration of fintech companies and changing attitudes about customers.

“You might have heard people say ‘Who owns the customer?’ We’ve been guilty of that,” he said.

But Ready said that PayPal has changed its perspective and that they want to make it easy for other fintech companies to partner with them.

Petralia Says to Focus on Millennials

October 23, 2018 Kabbage CEO and Co-founder Kathryn Petralia gave a fast-paced presentation at Money 20/20 yesterday that touched on gun violence, marijuana and gender identity, all in 20 minutes.

Kabbage CEO and Co-founder Kathryn Petralia gave a fast-paced presentation at Money 20/20 yesterday that touched on gun violence, marijuana and gender identity, all in 20 minutes.

The loose connecting thread was millennials, which Petralia’s powerpoint identified as people born between 1981 and 2002. There are 90 million millennial Americans and they have outnumbered babyboomers since 2017, Petralia asserted. So we have to pay attention to them and cater to their needs, she conveyed.

“Millennials are not as short on money as they are on time,” Petralia said, and she expressed that using data to improve speed and efficiency is therefore critical.

“The millennials are coming” read one of the powerpoint slides. But Petralia said they already have.

Branson Adds Charm, Not Expertise, to Money 20/20

October 23, 2018 Money 20/20’s keynote speaker, serial entrepreneur and philanthropist Sir Richard Branson, delivered inspiration and laughs to a packed audience yesterday. He was interviewed by Nuno Sebastiao, CEO of Feedzai, which fights financial crime.

Money 20/20’s keynote speaker, serial entrepreneur and philanthropist Sir Richard Branson, delivered inspiration and laughs to a packed audience yesterday. He was interviewed by Nuno Sebastiao, CEO of Feedzai, which fights financial crime.

While over 20 years ago Branson founded Virgin Money, a sizable UK-based bank, he demonstrated clear discomfort and disinterest in talking about banking. When asked about finance, he said, “I brought notes,” and produced what looked like a thick chunk of papers from his pocket. When Sebastiao said, “moving out of the financial space,” Branson said “thank you!” which elicited a wave of laughter.

“I’ve seen situations in life that have frustrated me,” Branson said, and explained that Virgin Money is the result of a contract he was about to sign with a money management firm. He said that when he asked the investment firm what “bid offered 5%” meant, they got quiet. He then learned that it meant that they would take five percent of the amount he gave them before investing anything. Upset by that, he thought he could do better in financial services and he hired a banker to help launch the company.

Similarly, he said Virgin Airlines was born when he couldn’t get a flight from Puerto Rico to the Virgin Islands because the airline said there weren’t enough passengers that day. He thought he could do better.

Since he first saw a man walk on the moon, he said he always imagined that he and his family would go to the moon someday. But when he realized about 14 years ago that it didn’t look like that was going to happen, he created Virgin Galactic Airways, which is the first commercial rocket program to the moon.

“I registered Virgin Galactic Airways and Virgin Intergalactic Airways, because I’m quite an optimist,” Branson said, producing another wave of laughter.

After years of testing, in which one test pilot was killed, Branson said that he plans to go to the moon next year.

“We can’t leave it up to government to solve the world’s problems,” Branson said, conveying that businesses, small and large, must play a role in improving the world, whether it be on a local or international level.

At the close of the interview, to bring the topic back to finance, Branson said, “Hopefully I’ll learn a little more about banking for next time.”