Small Business

Soon, We’ll All Be Able to Charge AI Bots for Scraping Data

July 8, 2026 In 2025, an online small business forum went offline. It had been operating for 15 years and generated just enough ad revenue to cover the hosting costs. Until it didn’t. The problem was bots. So many bots. And not the spamming kind, but the AI kind. LLMs were mining them for training data first and then actively pinging them all day every day to tap into live conversations taking place in the small business owner community. And so the forum eventually added Cloudflare as a protective measure to try and slow the velocity of the traffic. Enough AI bot traffic still got through, however, and the strain on the bandwidth pushed the hosting costs beyond the revenue.

In 2025, an online small business forum went offline. It had been operating for 15 years and generated just enough ad revenue to cover the hosting costs. Until it didn’t. The problem was bots. So many bots. And not the spamming kind, but the AI kind. LLMs were mining them for training data first and then actively pinging them all day every day to tap into live conversations taking place in the small business owner community. And so the forum eventually added Cloudflare as a protective measure to try and slow the velocity of the traffic. Enough AI bot traffic still got through, however, and the strain on the bandwidth pushed the hosting costs beyond the revenue.

It was a good deal for the LLMs because when people asked their local chatbot a question, it had oddly specific conversational exchanges between business owners to draw from. Eventually, the forum owner realized that their real customer wasn’t advertisers or even small business owners anymore, but LLMs that wanted to mine what small business owners talked about on a live basis. If only there had been a way for a little small forum owner to charge that customer.

Now, there will be. On July 1, 2026, Cloudflare announced its new Monetization Gateway that will give Cloudflare customers “the ability to charge for any asset protected by Cloudflare: web pages, datasets, APIs, or MCP tools.”

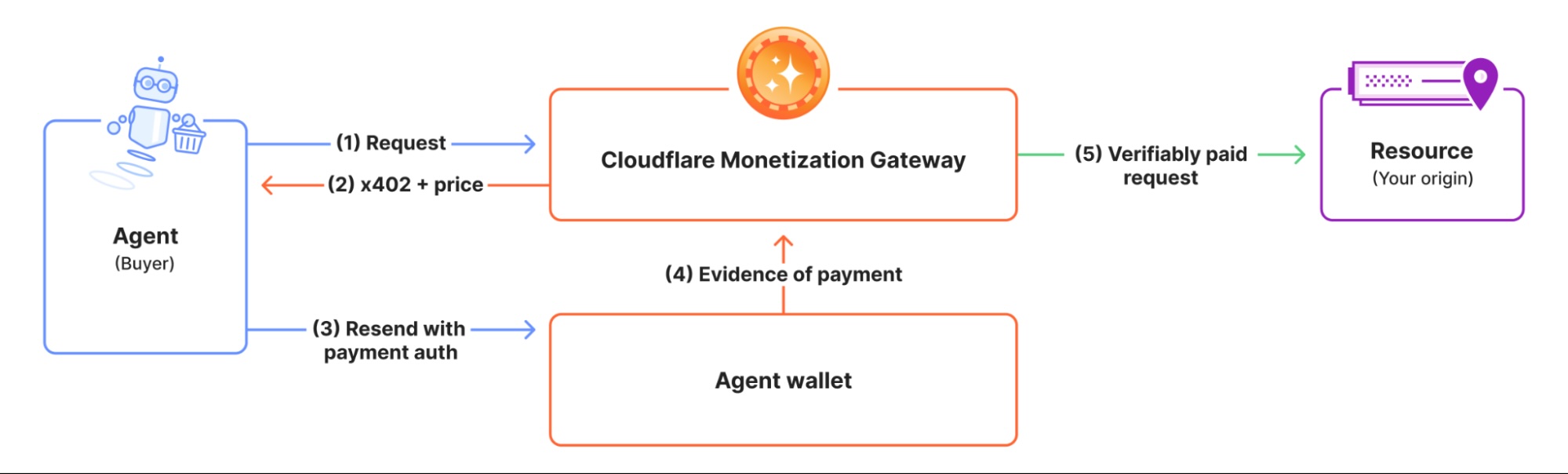

It works as such: When an AI bot pings a url it is met with an http 402 code. Under the 402 protocol, the bot is presented with a price in real time of how much it will cost to access that data. If accepted, the bot pays in stablecoins, and they are passed through to the endpoint. This would all take place in less than a second with Cloudflare managing all the payments and settlements on blockchain rails. By using stablecoins, micropayments become highly feasible. Cloudflare uses an an example of a $0.001 base fee for example, 1/10th of 1 cent for a single call.

“An agent does not look at ads or need to maintain a monthly subscription to all the tools it wants to access,” Cloudflare said. “It reads a page or consumes a data feed once, takes what it needs, and moves on. Across the web, AI crawlers already request content anywhere from a hundred to tens of thousands of times for every visitor they send back.”

“This reality demands a new model: usage-based pricing for everything. If attention and e-commerce are moving from websites to AI harnesses and AI-written software, then agents should pay for the inputs they need — training data, inference content, developer tooling, and API usage.

Historically, usage-based billing was difficult to implement. Businesses needed to effectively become payments companies, running their own accounting to track internal usage in a robust and auditable way. Tracking this usage required significant overhauls of backend systems. Many instead chose per-seat pricing because it is simpler and frequently more profitable.

Agents flip this dynamic. A single agent can do the work of an entire team around the clock, making a flat one-time fee disconnected from actual consumption. At the same time, an agent can make thousands of micropayments without friction, while asking a person to approve each payment would be impossibly burdensome. Usage-based price points are where agents live and where stablecoin-based micropayments shine. That’s because stablecoins (such as Open USD and USDC) allow buyers to transfer tiny sums across the Internet, incurring negligible fees and settling in less than a second. This is not feasible with other payment rails today.”

– Cloudflare

“There is an enormous amount of value moving across the Internet today that goes unmonetized or undermonetized, not because no one would pay for it, but because the tools to charge for it have never existed,” Cloudflare further said.

And so while that forum remains offline, AI bots still ping the urls daily hoping it has come back. If in the near future the companies behind those bots decide the data is worth paying for, then perhaps the forum will eventually have a path for a return, and many other web-based businesses are finally able to charge who their real customers are, AI bots.

Got Hit By The IEEPA Tariff? There’s a Company That Will Help Get Your Cash Back From It

May 5, 2026 On February 20, 2026, the Supreme Court of the United States ruled that the Trump Administration could not impose tariffs on imported goods under the International Emergency Economic Powers Act (IEEPA). While the President immediately pivoted to enforce tariffs under a different legal basis, many people began to wonder what would happen with the billions of dollars already collected from importers.

On February 20, 2026, the Supreme Court of the United States ruled that the Trump Administration could not impose tariffs on imported goods under the International Emergency Economic Powers Act (IEEPA). While the President immediately pivoted to enforce tariffs under a different legal basis, many people began to wonder what would happen with the billions of dollars already collected from importers.

Aharon Margolin, the CEO & Founder of Tariff Recovery Group, told deBanked that the court ruling was brought to the Court of International Trade (CIT) to determine next steps, and on March 4 it was decided that all importers would be refunded the IEEPA tariffs. It’s a lot of dough, approximately $166B. $55B of that is attributed to more than 236,000 small businesses that are now due a refund, and by all accounts it seems like the system is working with haste to handle this.

“They’ve actually outlined the process to start facilitating these refunds,” said Margolin, “and they even opened up a portal on the Customs Border Patrol (CPB) Website for importers to start to file their refunds.”

But a portal means paperwork, and a refund comes with the unknown of when it will be received. The CPB, for example, has announced that the first refund will be issued on May 11, which is less than a week from now, but is advising that they’ll generally take 60–90 days from the time a claim is filed. Small businesses have heard such speedy promises before, with the Employee Retention Credit (ERC), for example, and ended up waiting far longer than they ever could have anticipated.

But even if all parties move quickly, the Trump Administration has the option to appeal the CIT refund order and potentially cause a stay of the refund process altogether. This kind of delay or any prolonged delay could result in claims eventually getting denied entirely because of normal deadlines to protest tariffs. If businesses don’t file or protest the tariff in a timely manner, for example, the window to get refunded could simply close. Would they let that happen? No one knows for sure.

Similar to previous government programs, not everybody is aware of what is happening, what they’re even supposed to do, or if they’re supposed to do anything at all.

“…a lot of these merchants, I’m sure don’t even know they’re entitled to a refund,” said Margolin. “A lot of them are, and I think specifically the subset of the merchants that are turning to the the alternative funding industry are because they need that help.”

Margolin echoed what the rest of the small business finance industry was saying before the SCOTUS ruling: that applicants were often citing tariffs as being disruptive to their supply chains, generating demand for working capital solutions from a variety of sources, including products like MCAs. Margolin said the easiest cash flow solution would be for businesses to first get the tariff refund money that is actually owed to them. But that’s subject to the 60–90 day wait in a best-case scenario and an unknowable amount of time in a worst-case scenario.

What then if the need is urgent? That’s where Tariff Recovery Group comes in. They assess how much a business is owed in tariff refunds and can then work out a deal to pay the business cash upfront.

“It all depends on the nature of the claim,” Margolin said. “We’re able to liquidate that claim for money upfront right here, which could provide significant cash flow relief and working capital to the business.”

In his experience, many business owners aren’t even aware of exactly how much they paid in IEEPA tariffs. Because of that, they first assess all of their history and, if eligible, give them all the materials, deadlines, and instructions to file a claim. The business could simply stop there and use that as a standalone service or proceed to the next step, which is to sell the refund claim to Tariff Recovery Group.

Given all the moving pieces, certain unknowns, and the benefits of acting swiftly, Margolin’s company is hoping to educate as many people in the small business finance industry as possible, especially those who would normally just pitch loans or other solutions to their clients. They can also offer a tariff refund filing service or turn those refunds into cash upfront by referring those businesses to him.

“There’s a real service that you could be offering them, they could be getting real money back,” Margolin said. “There’s real commission to be made by brokers.”

Brokers can make commissions by referring businesses to go through the assessment with Tariff Recovery Group and file a claim, and then earn another commission if the business owner sells their claim. It’s, at the very least, a tool in the arsenal to provide a helpful service.

“The worst thing to hear is that a small business paid these types of tariffs and is not recovering them, that would just be money left on the table,” Margolin said.

Coleman Report’s Bob Coleman is Out With a New Book: “Easy Money, Hard Time”

July 18, 2025 Bob Coleman, founder of Coleman Report, the leading provider of information to small business bankers to help them make less risky small business loans, recently authored a book. Titled Easy Money, Hard Time: 19-Covid PPP Loan Fraud Stories, the book dives into “the most shocking cases of PPP loan fraud, exposing the audacity, greed, and recklessness of those who saw an economic disaster as a chance to cash in.”

Bob Coleman, founder of Coleman Report, the leading provider of information to small business bankers to help them make less risky small business loans, recently authored a book. Titled Easy Money, Hard Time: 19-Covid PPP Loan Fraud Stories, the book dives into “the most shocking cases of PPP loan fraud, exposing the audacity, greed, and recklessness of those who saw an economic disaster as a chance to cash in.”

Coleman has also previously authored PPP Saves Millions of Main Street Jobs During Covid (2022) and Money, Money Everywhere But Not a Drop for Main Street (2011).

Coleman’s premium content trade newsletter began in 1993 and it provides critical analytical information for today’s small business lending professional. They are the largest producer of training courses and webinars for small business bankers.

Bob Coleman will be moderating a panel on SBA lending at the B2B Finance Expo in Las Vegas this October.

Seventy Five Percent of Small Businesses Expect to Do Better in the Coming Year

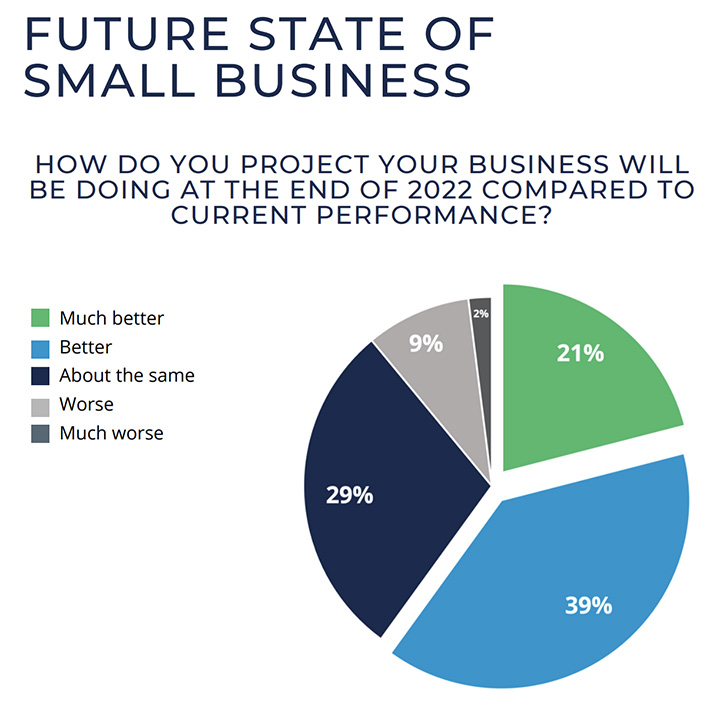

January 17, 2025 2025 is looking up. That’s one takeaway from the recent State of Small Business Report produced by IOU Financial. More than 75% of small business owners that responded to a survey said that they expected to do better in the coming year, with 42% expecting to do much better. Meanwhile, more than three-fourths of those surveyed plan to invest in their business within the next six months.

2025 is looking up. That’s one takeaway from the recent State of Small Business Report produced by IOU Financial. More than 75% of small business owners that responded to a survey said that they expected to do better in the coming year, with 42% expecting to do much better. Meanwhile, more than three-fourths of those surveyed plan to invest in their business within the next six months.

Still, cost of goods and interest rates ranked among the highest concerns. Eighty two percent said that they are very or somewhat concerned about cost of goods and seventy seven percent said the same about interest rates.

To read the full report, click here.

Inflation? So What – SMBs Are Bullish On the Rest of 2022

August 17, 2022Eighty-nine percent of respondents projected that their small business will be doing the same, better, or much better by the end of the year, according to a recent survey conducted by IOU Financial. The majority of those polled actually selected better (39%) or much better (21%). Twenty-nine percent said they expected to be about the same.

The sentiment is significant given that 84% said that they were somewhat concerned or very concerned about rising inflation and 85% said that they were somewhat concerned or very concerned about a possible recession.

This data is in line with responses found from other surveys like the recent NFIB study that determined that inflation was the single most important problem that business owners were facing. But even that study revealed a sense of persistent optimism, similar to the IOU survey, when respondents said that financing and interest rates ranked the lowest on their selected list of problems.

All of which means that the biggest challenge small businesses are facing right now is not viewed as a mortally perilous one. Indeed, 74% of respondents to the IOU survey said that they plan to invest in their business in the next six months.

All of which means that the biggest challenge small businesses are facing right now is not viewed as a mortally perilous one. Indeed, 74% of respondents to the IOU survey said that they plan to invest in their business in the next six months.

“They plan to fund expansion, make equipment or inventory purchases as well as put money into staffing and marketing,” the IOU report states. Only 5% flat out said that they do not plan to invest in their business in the next 6 months. The rest said that they might invest.

The optimism that is there is cautious, however. Seventy-five percent of respondents said that the covid pandemic is not fully over and 32% said that they would rate the current state of their business as somewhat negatively or very negatively.

The damage from the last two years lingers on but business owners are looking at what’s ahead of them and signaling that it’s onward and upward regardless.

The full IOU Small Business Survey can be downloaded here.

Could More Free Money Be Coming to Restaurants?

April 11, 2022 The House passed a $55 billion bill on Thursday to provide assistance to restaurants that were not successful in receiving help from the federal Restaurant Revitalization Fund (RRF) last year. In a 223-203 House vote the measure was approved by lawmakers and was backed by only a few Republicans.

The House passed a $55 billion bill on Thursday to provide assistance to restaurants that were not successful in receiving help from the federal Restaurant Revitalization Fund (RRF) last year. In a 223-203 House vote the measure was approved by lawmakers and was backed by only a few Republicans.

Over $40 billion in COVID-19 assistance was approved, replenishing the fund. An additional $13 billion would be provided for other businesses that remain struggling to recover.

The Restaurant Revitalization Fund was established under the American Rescue Plan, and signed into law by President Joe Biden on March 11, 2021 which issued $28.6 billion in direct relief funds. However, three weeks after launching, the funds ran out leaving only a third to receive relief funding out of 300,000 applicants.

Recipients are not required to repay the funding as long as funds are used for eligible uses no later than March 11, 2023.

If the bill passes the Senate, the 177,000 restaurants that were approved for RRF grants but did not receive funding before the portal closed are already in line as stated by legislators.

To overcome the 60-vote threshold to end a potential prolonged debate and pass the measure, it is undetermined whether Democrats in the evenly split Senate will be able to win over at least 10 Republicans.

Despite protocols of the pandemic being lifted, restaurants are still facing the negative effects with less staff and fewer customers. According to the National Restaurant Association, 9 in 10 restaurants have fewer than 50 employees and restaurant industry sales in 2021 are down by $65 billion from 2019’s pre-pandemic levels.

The main sponsor of the bill, Rep. Earl Blumenauer, D-Ore., and Rep. Dean Phillips, cited a survey from the Independent Restaurant Coalition and stated that over 80 percent of restaurants that didn’t receive grants have reported that they are on the verge of permanent closure.

Kabbage Survey Shows American SMBs Recovering Post-Pandemic

March 30, 2022![]()

Kabbage from American Express issued the fifth Small Business Recovery Report, an online survey that tracks recovery trends and potential growth of small businesses in the US. Respondents represented industries across retail, marketing, healthcare, financial services, technology, food and beverage, construction, automotive, manufacturing, media, professional services, education, agriculture and more.

After polling 563 small business leaders that included 255 of the “smallest small businesses,” the latest report showcases how many small businesses are doing well in a changing market, as they look beyond challenges over the past two years while simultaneously overcoming the new problems of inflation and supply chain issues.

“Small businesses are preparing for a new type of market. One that’s not driven by the direct impact of COVID-19 – but rather, one determined by the economic aftermath of the pandemic,” said Kathryn Petralia, co-founder of Kabbage. “Economic indicators like inflation will require adjustments, but the new data illustrates how small businesses are making changes and adapting.”

According to the study, small businesses are becoming less concerned about COVID-19’s impact on their operations. The report’s responses showed over 90% of businesses did not have to “stop, slow, limit or shut down” their companies due to the Omicron outbreaks during the holiday season of 2021, while 70% surveyed said they weren’t affected by the variant in any way.

Along with pandemic-induced wounds beginning to heal for small business, respondents to the survey reported their average monthly revenues increased 77% in the past six months, from $47,900 in July 2021 to $84,935 in February 2022. Along with those increases, merchants reported average monthly profits have increased an average of 39% in the same period as well. The study does hint that these growth percentages are heavily weighted toward larger small businesses.

Kabbage says that the smallest small businesses, those with 20 or less employees, reported a 13% increase in average monthly revenues and a 12% increase in average monthly profits from July 2021 to February of this year.

The report touched on hiring rates for smaller merchants, as an initial void of lost workers has been filled. Despite a widespread notion of the job market being wide open, the study found that three quarters of the smallest small businesses said they are not hiring.

The study also found that inflation is increasing prices by an average of 21% across industries. Largely due to increased costs from their vendors and skyrocketing cost of raw materials, smaller merchants are beginning to push these costs on customers.

65% of businesses in the survey said they plan to keep prices high for the next six months, while almost 20% said they plan to raise prices further. Combating increasing costs of their own is an issue in and of itself, and over half (53%) expect their business to be impacted by supply chain issues for up to a year.

NJEDA Approves Grants to Support Micro Business Lenders

February 16, 2022 Last week, the New Jersey Economic Development Authority (NJEDA) endorsed the construction of the Main Street Lenders Grant.

Last week, the New Jersey Economic Development Authority (NJEDA) endorsed the construction of the Main Street Lenders Grant.

Eligible micro business lenders will be offered up to $1 million that can be used to create new lending products or as supplemental funding for existing products. The Main Street Lenders Grant is the third product the NJEDA plans to launch under the Main Street Recovery Program. The $100 million small business support program was created under the Economic Recovery Act of 2020 (ERA) and was signed by Gov. Phil Murphy in January of 2020.

The technical assistance grant will support those who qualify with the costs associated with providing technical assistance to micro businesses, aiding these businesses to qualify for loans. The maximum grant one can receive is 50 percent of their lending grant amount (not to exceed $500,000).

The second product under the Main Street Recovery Program is the Small Business Improvement Grant, with applications now open as of Thursday. This product will reimburse eligible small businesses and nonprofits for up to 50 percent of eligible project costs associated with building improvements or purchases.

“Small businesses are the backbone of New Jersey,” stated Governor Phil Murphy. “This program will allow small businesses and nonprofits throughout our state to make the investments necessary for their success and for improvements to their spaces.”