Industry News

Wall Street Journal, CNBC, Forbes, and More Operate Small Business Funding Referral Marketplaces

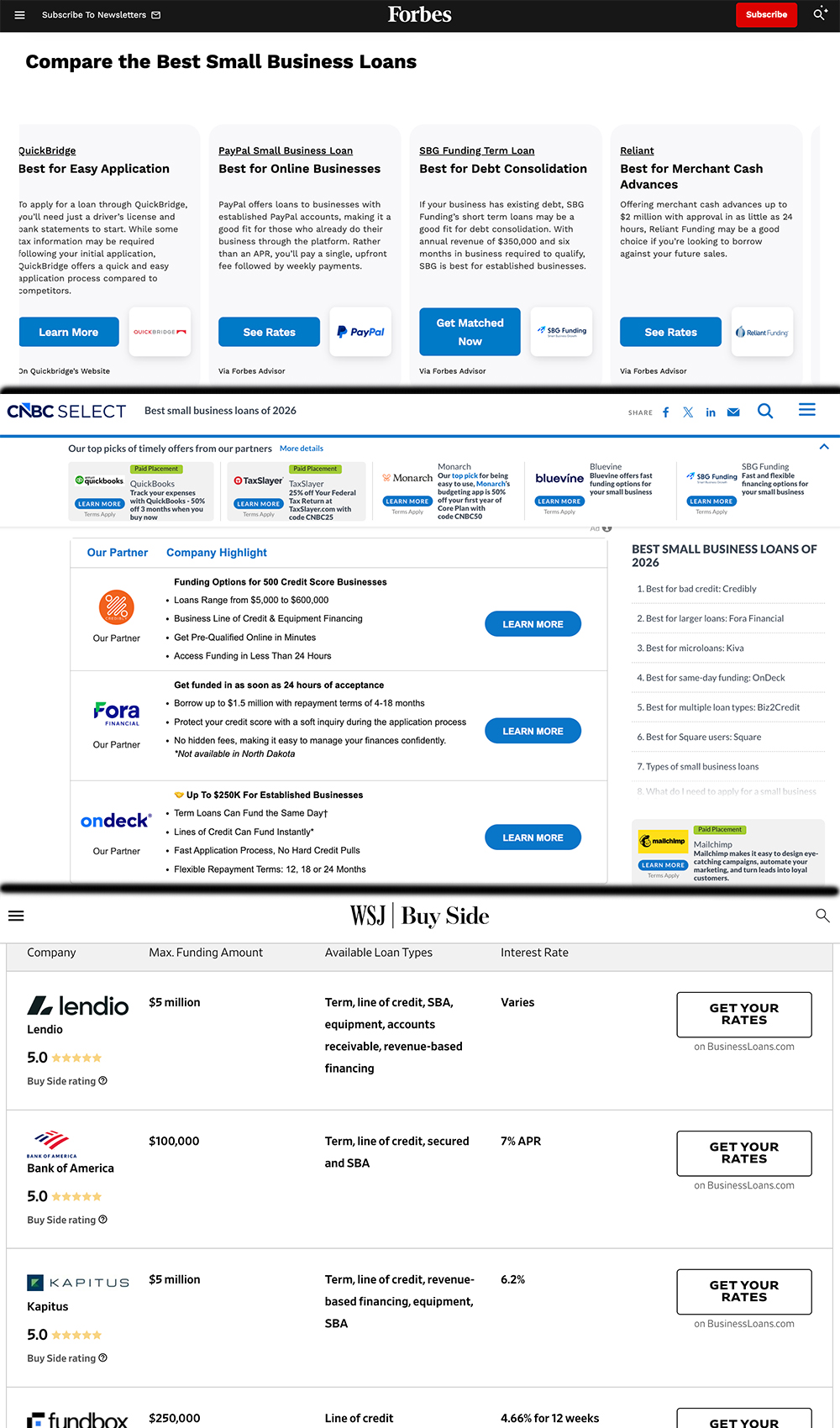

July 16, 2026Walmart‘s not the only household brand name that’s running a small business funding marketplace. A cursory Google search shows that the Wall Street Journal, CNBC, and Forbes, among others, are also capturing traffic and earning commissions by referring merchants for business loans, revenue-based financing, and other products.

The WSJ says it earns commissions when merchants click links to apply for revenue-based financing, lines of credit, and other small business loans. “Revenue-based financing might be a good option if you don’t qualify for a business term loan,” the WSJ states on its review page.

Forbes operates with paid placements and links that generate affiliate commissions. The CNBC Select site says that the company earns commissions. WSJ, Forbes, and CNBC compete with other platforms like Nerdwallet, LendingTree, and Bankrate for business loan traffic online.

Meanwhile, Walmart’s business loan marketplace consists of Payoneer, Parafin, Slope, and Uncapped. Three of those partners offer merchant cash advances.

TCPA Lawsuits Up By 30%, According to WebRecon

July 14, 2026As of the end of May 2026, TCPA lawsuits were on pace to grow by 30% over 2025, according to WebRecon. This was across the board nationally, not specific to a single industry. WebRecon tracks consumer lawsuits on a monthly basis.

Complaints made to the CFPB were also up, on pace to be 34.8% higher than the previous year. The CFPB complaint database is public, but complaints are only published after the company responds or after 15 calendar days, whichever comes first. The CFPB removes complaints if they do not meet all of the publication criteria.

Factoring to Take MCA Fight to Federal Level

July 2, 2026In the wake of new merchant cash advance laws passed in Texas and Vermont, American Factoring Association President Cole Harmonson posted the next step is to take the fight against MCAs to the federal level.

Post below:

Got Hit By The IEEPA Tariff? There’s a Company That Will Help Get Your Cash Back From It

May 5, 2026 On February 20, 2026, the Supreme Court of the United States ruled that the Trump Administration could not impose tariffs on imported goods under the International Emergency Economic Powers Act (IEEPA). While the President immediately pivoted to enforce tariffs under a different legal basis, many people began to wonder what would happen with the billions of dollars already collected from importers.

On February 20, 2026, the Supreme Court of the United States ruled that the Trump Administration could not impose tariffs on imported goods under the International Emergency Economic Powers Act (IEEPA). While the President immediately pivoted to enforce tariffs under a different legal basis, many people began to wonder what would happen with the billions of dollars already collected from importers.

Aharon Margolin, the CEO & Founder of Tariff Recovery Group, told deBanked that the court ruling was brought to the Court of International Trade (CIT) to determine next steps, and on March 4 it was decided that all importers would be refunded the IEEPA tariffs. It’s a lot of dough, approximately $166B. $55B of that is attributed to more than 236,000 small businesses that are now due a refund, and by all accounts it seems like the system is working with haste to handle this.

“They’ve actually outlined the process to start facilitating these refunds,” said Margolin, “and they even opened up a portal on the Customs Border Patrol (CPB) Website for importers to start to file their refunds.”

But a portal means paperwork, and a refund comes with the unknown of when it will be received. The CPB, for example, has announced that the first refund will be issued on May 11, which is less than a week from now, but is advising that they’ll generally take 60–90 days from the time a claim is filed. Small businesses have heard such speedy promises before, with the Employee Retention Credit (ERC), for example, and ended up waiting far longer than they ever could have anticipated.

But even if all parties move quickly, the Trump Administration has the option to appeal the CIT refund order and potentially cause a stay of the refund process altogether. This kind of delay or any prolonged delay could result in claims eventually getting denied entirely because of normal deadlines to protest tariffs. If businesses don’t file or protest the tariff in a timely manner, for example, the window to get refunded could simply close. Would they let that happen? No one knows for sure.

Similar to previous government programs, not everybody is aware of what is happening, what they’re even supposed to do, or if they’re supposed to do anything at all.

“…a lot of these merchants, I’m sure don’t even know they’re entitled to a refund,” said Margolin. “A lot of them are, and I think specifically the subset of the merchants that are turning to the the alternative funding industry are because they need that help.”

Margolin echoed what the rest of the small business finance industry was saying before the SCOTUS ruling: that applicants were often citing tariffs as being disruptive to their supply chains, generating demand for working capital solutions from a variety of sources, including products like MCAs. Margolin said the easiest cash flow solution would be for businesses to first get the tariff refund money that is actually owed to them. But that’s subject to the 60–90 day wait in a best-case scenario and an unknowable amount of time in a worst-case scenario.

What then if the need is urgent? That’s where Tariff Recovery Group comes in. They assess how much a business is owed in tariff refunds and can then work out a deal to pay the business cash upfront.

“It all depends on the nature of the claim,” Margolin said. “We’re able to liquidate that claim for money upfront right here, which could provide significant cash flow relief and working capital to the business.”

In his experience, many business owners aren’t even aware of exactly how much they paid in IEEPA tariffs. Because of that, they first assess all of their history and, if eligible, give them all the materials, deadlines, and instructions to file a claim. The business could simply stop there and use that as a standalone service or proceed to the next step, which is to sell the refund claim to Tariff Recovery Group.

Given all the moving pieces, certain unknowns, and the benefits of acting swiftly, Margolin’s company is hoping to educate as many people in the small business finance industry as possible, especially those who would normally just pitch loans or other solutions to their clients. They can also offer a tariff refund filing service or turn those refunds into cash upfront by referring those businesses to him.

“There’s a real service that you could be offering them, they could be getting real money back,” Margolin said. “There’s real commission to be made by brokers.”

Brokers can make commissions by referring businesses to go through the assessment with Tariff Recovery Group and file a claim, and then earn another commission if the business owner sells their claim. It’s, at the very least, a tool in the arsenal to provide a helpful service.

“The worst thing to hear is that a small business paid these types of tariffs and is not recovering them, that would just be money left on the table,” Margolin said.

The OppFi / BNC National Bank Deal and Bitty

April 29, 2026 OppFi, a publicly traded fintech lender, has announced that it has entered into a definitive agreement to acquire BNC National Bank in a cash-and-stock transaction valued at approximately $130 million. OppFi says that “the transaction unites two complementary, market-leading businesses, combining OppFi’s sophisticated online lending platform with BNC’s national bank charter and diversified banking infrastructure to create a stronger, more diversified financial services provider.”

OppFi, a publicly traded fintech lender, has announced that it has entered into a definitive agreement to acquire BNC National Bank in a cash-and-stock transaction valued at approximately $130 million. OppFi says that “the transaction unites two complementary, market-leading businesses, combining OppFi’s sophisticated online lending platform with BNC’s national bank charter and diversified banking infrastructure to create a stronger, more diversified financial services provider.”

As deBanked readers may be aware, OppFi also owns 35% of Bitty, a small business finance provider, a detail reiterated in the official bank acquisition announcement. Viewed through that lens, there appears to be a natural synergy between Bitty and BNC. BNC, for example, offers SBA loans, equipment financing, working capital loans, and more. Headquartered in Glendale, AZ, the announcement notes that BNC has “a particular strength in business financing and SBA lending.”

OppFi stands to benefit in several ways from the arrangement, including gaining “access to BNC’s stable, low-cost deposit base, which carries a cost of less than 2%.”

“BNC will continue normal operations as a community banking division within OppFi Bank, and will continue to be led by Dan Collins and the existing BNC management team,” the companies state. “Todd Schwartz will lead the combined company as Chief Executive Officer and Executive Chairman. Michael Vekich will serve on the board of directors of OppFi Bank.”

What the Velocity Capital Group Announcement Revealed

April 21, 2026 Velocity Capital Group has deployed over $1 billion to small businesses, newly unveiled financial stats show, shedding light on the firm’s performance as it enters a new phase of institutional-scale expansion. Across more than 10,000 transactions, VCG reports a 37.1% renewal rate and a sub-10% default rate.

Velocity Capital Group has deployed over $1 billion to small businesses, newly unveiled financial stats show, shedding light on the firm’s performance as it enters a new phase of institutional-scale expansion. Across more than 10,000 transactions, VCG reports a 37.1% renewal rate and a sub-10% default rate.

The firm says it operates in all 50 states and is actively preparing to extend its model globally, with origination volumes projected to continue accelerating through 2030. As part of that, VCG has hired Michelle Melo as Director of Financial Operations & Capital Markets.

deBanked has been covering VCG’s expansion since 2018, starting with a profile that captured CEO Jay Avigdor’s rise from solopreneur to a large office on Long Island. At the time, Avigdor told deBanked: “We crawl before we walk before we run.” The company now appears to be in a full sprint as it looks globally.

This past February, Velocity Capital Group’s booth at deBanked CONNECT MIAMI included a surprise guest appearance from NBA All Star Bam Adebayo. Now with its recent big hire of Melo, Avigdor says, “VCG’s tech- and data-powered platform is scaling faster and more efficiently than nearly any peer in our category, and Michelle is here to institutionalize that advantage. She will drive pre-securitization discipline, standardized reporting, and the investor relationships we need to remove scaling friction and enable the next generation of growth. With Michelle on board, VCG is significantly closer to achieving our target of $1 billion in annual originations.”

National Alliance of Commercial Loan Brokers LLC Back in Roglieri’s Hands

February 5, 2026The United States Bankruptcy Court ordered the Roglieri Estate return its interest in the National Alliance of Commercial Loan Brokers LLC back to Roglieri himself. The order was dated January 30, 2026. That interest includes all the assets and liabilities attached to the National Alliance of Commercial Loan Brokers LLC. The Trustee’s reasoning was that management over the business had become burdensome to the Roglieri Estate.

Nearly two years ago, Roglieri declared in a bankruptcy filing that National Alliance of Commercial Loan Brokers LLC (often referred to as NACLB) was valued at $1 million.

Roglieri is currently imprisoned at the Rensselaer County Correctional Facility. He pleaded guilty to wire fraud conspiracy this past November. His sentencing hearing is scheduled for March 11 and he is facing up to 20 years in prison.

Several Businesses that Belonged to Kris Roglieri Are Being Returned to Him for Free

January 30, 2026A United States Bankruptcy Court has ordered that the following businesses be released from the bankruptcy estate of Kris Roglieri and returned to Roglieri:

- National Alliance of Commercial Loan Brokers

- Commercial Capital Training Group

- Digital Marketing Training Group

- FUPME, LLC

- Shark Ventures LLC

The order is dated today, 1/30/26. The trustee’s reasoning for release is that the continued retention of these non-debtor interests are burdensome to the estate.

For full disclosure, the parent company of deBanked, Raharney Capital, LLC, had made a bid for two of the above entities and/or assets but withdrew it after the Trustee placed conditions on a sale that it would not agree to. Raharney Capital had also previously won the auction conducted for the Commercial Capital Training Group trademark but the sale was rescinded by the Trustee after claiming it had been auctioned off in error. The trademark (not the business) for National Alliance of Commercial Loan Brokers was apparently successfully sold off to a third party.

Roglieri had claimed in a March 22, 2024 bankruptcy declaration that the National Alliance of Commercial Loan Brokers business was valued at $1 million and that the Commercial Capital Training Group business was valued at $500,000. His interest in those businesses are now being returned to him by the Trustee at no cost.

Roglieri is currently imprisoned at the Rensselaer County Correctional Facility. He pleaded guilty to wire fraud conspiracy this past November. His sentencing hearing is scheduled for March 11 and he is facing up to 20 years in prison.