Loans

As LendingClub Finally Rebrands to Happen Bank, Prosper Holds On to Legacy Peer-to-Peer Lending Model

June 22, 2026LendingClub has finally rebranded to Happen Bank. Explaining the new name, company CEO Scott Sanborn said, “The Happen Bank brand more clearly reflects the role we play in consumers’ lives: helping people make things happen with products that are smart, transparent, and easy to use.”

The LendingClub name was a holdover from the company’s early days as a peer-to-peer loan marketplace, a business model it ditched for good at the end of 2020. From there, LendingClub shifted into banking by acquiring Radius, a fast-growing digital bank, and has been a bank ever since. In many ways, that marked the end of the peer-to-peer lending era, at least for what had once been one of fintech’s most recognizable names. The segment had enjoyed major popularity throughout the 2010s, but the original vision gradually gave way to more traditional lending and banking models.

Prosper Marketplace, LendingClub’s original rival, took a different path. It has continued to hold on to its original model, even as the peer-to-peer portion of the business has become a much smaller piece of the whole. Prosper originated $2.7 billion in consumer loans in 2025, up from $2.2 billion the year prior. It still has a peer-to-peer component, but that continues to fade further into the background each year. Only 5% of Prosper’s loans were funded by peers in 2025, down from 7% in 2024.

Still, the model persists. Individuals can still log in, browse consumer loans, and contribute small amounts toward them in hopes of earning a return while Prosper services the loans. Prosper is profitable too, which helps show that its business was not merely built on fintech hype. The company celebrated its 20-year anniversary just last year.

In that announcement, Prosper CEO David Kimball said, “Prosper was established 20 years ago by Chris Larsen and John Witchel as part of their quest to democratize consumer lending and create opportunities previously unavailable through traditional banking channels. As consumers’ needs have grown, we have grown alongside them. Today, we’ve evolved into a comprehensive financial platform, offering simple, trusted, and affordable solutions that help people transform their lives.”

Soon, You’ll Be Able to Lend Against Credibly Small Business Loan Pools

May 23, 2026For most people in the small business lending and revenue-based financing industry, news of a billion-dollar securitization barely resonates. It’s too big, too abstract, especially if you’re used to the ground game of syndicating a couple million bucks in deals you handpicked with funders you personally know. Wall Street-level capital markets has always felt like a mysterious private club, where a hundred million here and a billion there changes hands through an old-fashioned system outsiders hardly ever get to see, aside from the press release that later announces a deal happened.

But something recently changed. Capital markets, at least a corner of it, is being democratized. That became obvious when someone told me I could lend a hundred bucks toward a warehouse line of credit for Credibly just to see it for myself.

Me? Somehow involved in a warehouse line for Credibly???

On May 5, Credibly announced a strategic partnership with Figure to “modernize SMB capital markets via blockchain rails.” It sounds like a buzzwordy headline from the 2010s. Not AI, blockchain. In 2026. Though there are certainly AI technologies involved.

Figure is a familiar name, not only because it is publicly traded, but also because I had the honor of sharing a stage with Figure CEO Michael Tannenbaum last fall at the B2B Finance Expo in Las Vegas for a fireside chat. While I mainly asked him about how small business owners could leverage their home equity to obtain capital, Tannenbaum pivoted at moments to explain how the company was reshaping capital markets by using blockchain. At the time, some of it went over my head.

“Everybody else is trying to use an origination system, and then on the back end figure out where to sell the loan,” said Tannenbaum on Peter Renton’s recently released Fintech One-on-One podcast, “and that figuring out process creates all this back and forth between the lender, the borrower, and the ultimate buyer, and we eliminated that, and we eliminated the people-based approach and standardized it.”

In a nutshell, Figure being in the mortgage game meant it was inevitably tied up in the capital markets game. And they found the capital markets game very old-fashioned. So they made their own capital markets marketplace, with one segment called Democratized Prime, and built it on blockchain rails.

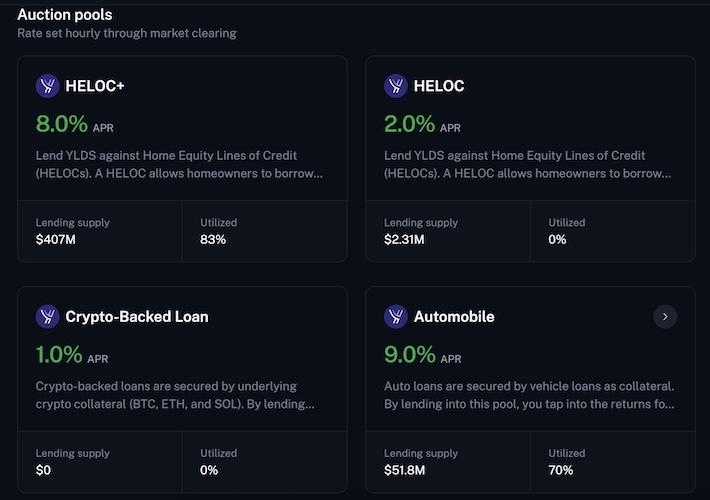

Democratized Prime is essentially like a universal warehouse line, one that is “much easier to borrow and lend against than the arduous process of getting a warehouse line with lots of third-party diligence and legal fees,” Tannenbaum told Renton. It has rapidly become popular for mortgages. If you signed up for the platform today, you would see HELOC pools and their corresponding credit profiles that you could lend against.

Mortgages were just the start. You can also lend against an auto loan pool brought on by Agora. That deal was announced this past February as a landmark moment that kicked off the democratization of new asset classes. Credibly will bring SMBs into the mix next, where the company’s small business loans and revenue-based financing deals will be pooled up and available to lend against with as little as $10 at a time. That means this opportunity is open to just about anybody.

The yield can be determined in one of two ways. One is a Dutch auction, where participants compete to lend into the pool by offering lower rates, which is good for Credibly as the number goes down. If you bid too high or the pool is full, you may have to wait until the next hourly auction to try again. The process resets each hour, with the lowest acceptable bids getting priority, meaning lenders are not just deciding whether they want exposure to the pool, they are also competing on price for the right to put their money to work. The other is a live-rate system where rates change automatically based on utilization. You can exit an auction pool if your funds are not in use or if someone else’s funds are ready to replace yours. For live rates, you can request an exit up to the available liquidity at the time. Credibly is not on the Democratized Prime system just yet. That is supposed to happen this quarter. But HELOC and auto loan pools are already there.

I first tried the platform myself with just a couple hundred bucks. I entered digits into an auction-pool form indicating that I’d be willing to lend at 7.9% APR all-in to a HELOC pool. The pool wasn’t taking any offers for higher than 8% so that’s how I came up with my figure. My funds were accepted, and they’re now earning a return. Not in some magic back room, but visibly on the blockchain.

While you can obviously fund your account with dollars, I dusted off an old stockpile of ETH and sent funds using MetaMask to Figure Markets. Therein lies the only caveat. To lend against the pools, you have to use Figure’s stablecoin, YLDS.

YLDS is an SEC-registered security. It is pegged 1:1 with the U.S. dollar and also earns a return on its own just for holding it, a little over 3% at the time of this writing. Users use their YLDS to lend against the pools and are paid their interest in YLDS (hourly!). This can be swapped back into dollars, Bitcoin, or whatever else one is comfortable with.

YLDS is an SEC-registered security. It is pegged 1:1 with the U.S. dollar and also earns a return on its own just for holding it, a little over 3% at the time of this writing. Users use their YLDS to lend against the pools and are paid their interest in YLDS (hourly!). This can be swapped back into dollars, Bitcoin, or whatever else one is comfortable with.

YLDS exists on the Provenance blockchain. You’re assigned a wallet address, and you can trace where your funds went using Provenance’s main block explorer, ZoneScan. That also lets you see a bit of what other users are doing, as well as what Figure is doing. By being on blockchain rails, everything is kind of out there for audit and inspection. I saw my ETH get swapped for YLDS on the block explorer and then saw my funds interact with a corresponding HELOC pool smart contract.

If you think this blockchain stuff is still niche, consider that in 2025, stablecoins processed $28 trillion in real economic volume, according to Chainalysis. By 2035, that number could reach $1.5 quadrillion, surpassing today’s entire cross-border payments market. Those are eye-popping numbers, but even if one discounts the forecast, the broader point is hard to ignore: stablecoins are no longer a fringe experiment.

Of course, this is not risk-free just because it is transparent. Pool performance still matters. Borrower credit quality still matters. Liquidity may depend on whether other participants are ready to replace your funds. And because YLDS is itself a security, participants need to understand what they are holding, how it works, and what risks come with using it. The blockchain may make the mechanics easier to inspect, but it does not make credit risk disappear.

While Democratized Prime can make it easier for lenders to tap into capital, this also is not a solution for everyone. Credibly, for example, has provided access to over $3 billion in working capital to more than 61,000 small businesses, with four completed KBRA-rated securitizations, its most recent one completed in the first quarter of 2026 for $124 million, expandable up to $225 million. That is sort of the baseline quality: true institutional-level assets from an institutional-tier lender. A small funder looking to graduate away from syndication is not going to be an immediate candidate for something like this. One of the HELOC loan pools, for example, has taken in $340M from parties looking to lend their YLDS.

One benefit for Credibly in challenging traditional finance ABS markets and adopting this technology is that greater efficiency and reduced friction should ultimately enable the company to pass savings on to its small business customers.

Would you lend a million dollars against a Credibly business loan and revenue-based financing pool? Before now, you probably wouldn’t ever have had that opportunity. Now Figure is making that possible.

How LendingClub (Happen Bank) Plans to Handle Customers Using AI Agents To Seek Out a Loan vs. Search Engines Like Google

April 28, 2026During LendingClub’s Q1 earnings call, stock analyst David Scharf asked LendingClub CEO Scott Sanborn how they’re approaching investments in AI-type search vs. traditional. Scharf used this example for context:

Scharf:

…specifically, I was just typing in how do I get a $10,000 personal loan and it just gives you the typical Google paid search listing of whoever shows up, then I said what’s the best $10,000 loan for me and it did the typical NERDWallet shows up. But going forward, when somebody types in, a year from now, what’s the best $15,000 personal loan for me into either Chat or Claude, can you talk us through either some of the risks or opportunities you see in terms of these AI engines making more qualitative assessments and not just traditional search assessments?

Sanborn’s excerpted response:

So it’s a great question. And while it is a buzzword, it is also — that does not take away from the fact that the changes underway are very real, and we are pursuing them, as I mentioned in the prepared remarks, across really all departments and all aspects of the company.

[…]

So inertia is really the thing we’re trying to overcome. So if the agents evolve not only to replace Google search, but potentially to act on behalf of consumers, we think we’re a net beneficiary. But you’re right, it is as a percentage of web traffic right now, it is quite small. That said, it is high intent. And so as that percentage grows, we need to be there for it.

All of the protocols are not established exactly what the — as I’m sure you know, there are many, many, many firms that are engineering themselves around how to optimize for Google’s ever-changing algorithm that same thing will be true for agentic search, and we are going to be going after that the same way we will sort of core organic search and think we’re set to benefit. Right now, that means likely increasing the amount of content we produce to get out there. We’re already in the site. We’re obviously in the places you mentioned. We’re in NerdWallet Best Of, I think, on both sides of our balance sheet. So we’re already there.

But we need to be getting some of our content out on our own to help with that. So we’re pushing behind that throughout this year. That’s definitely on our plan.

LendingClub previously announced that it is rebranding to Happen Bank.

Upstart: Humans are not very good at underwriting loans so AI won’t be either

March 23, 2026 “…unfortunately, humans have never really been very good at precisely underwriting loans and figuring out the cash flows they’re going to produce for the next 5 years,” said Upstart CEO Paul Gu during the company’s Q4 earnings call in response to an analyst’s question. “That’s something that has always been solved as a big math problem.”

“…unfortunately, humans have never really been very good at precisely underwriting loans and figuring out the cash flows they’re going to produce for the next 5 years,” said Upstart CEO Paul Gu during the company’s Q4 earnings call in response to an analyst’s question. “That’s something that has always been solved as a big math problem.”

Upstart’s innovative consumer credit models preceded the dawn of modern-day LLMs. It has been one of their defining features. Underwriting on their part is a combination of the best data access and math. Because of that, they do not view AI as a threat because AI is only great at replacing what humans are good at and underwriting is not one of those things.

“I mean the simple answer is just that a lot of the advances in AI are really good for work that humans are naturally good at,” said Gu.

Gu used an example of a HELOC in which human processors have to go through process of securing and perfecting a lien, checking property records, etc. “…like a lot of that stuff is a mess in a human way and traditionally comes with very high operations cost because you have a lot of people that are checking to make sure things are right,” Gu said. “Those are actually the perfect problem to throw sort of LLM-style AI against.”

When it comes to AI benefitting their business, that’s how Upstart is approaching it.

“…It’s really important to just remember that the LLM models coming from Anthropic or OpenAI or any of the others, Gemini, they are really good at solving problems that humans are good at solving and they can do it at scale. They can work 24/7. You can spin up 100 of them in parallel and have them work. But no matter how many humans you have, you don’t want that army of humans underwriting loans for you,” Gu said.

‘Face-to-Face is a Must In This Industry’: How Julian Hernandez of Idea Financial Earned a Trophy Along The Way

November 24, 2025

“Face-to-face interactions are a must in our industry, and not only through conferences but even though we’re based out of Miami, I’m very familiar with the Long Island Railroad,” said Julian Hernandez, Director of Revenue at Idea Financial.

On multiple occasions, Hernandez has gone from New York City to eastern Long Island and then back again to meet with referral partners. It’s part of his job, meeting face-to-face with ISOs, and working with them to maximize the spread of Idea’s business line of credit products. He says through this experience he’s actually become “best buddies” with the LIRR.

“It’s good for morale, it’s good for relationships. It’s good not only for the reps internally on my end, but I’m sure for the reps on [the ISOs’] end to see and put a face to the lender that they’re always working with,” he said.

Hernandez will go wherever it’s necessary. Just last month that initiative placed him on the opposite side of the country, in a room full of ISOs and competitors that had gathered to play poker on the eve of the big B2B Finance Expo at the Wynn in Las Vegas. For Hernandez, who was born and raised in Colombia and only ever plays poker in a casual setting with friends, he had not gone in with any expectation of winning the friendly tournament. He wanted to network.

“That’s probably one of the main reasons why I wanted to join the tournament,” Hernandez said. “It’s just an opportunity for us, for anyone really that goes to the conference, to connect with either people that they know from the industry, or branch out or meet with new faces in an environment that isn’t so corporate.”

As the cards were dealt and the hands played, Hernandez found himself at the final table of the night and walked away with 2nd place overall, a title that garnered him a trophy and a small prize.

As the cards were dealt and the hands played, Hernandez found himself at the final table of the night and walked away with 2nd place overall, a title that garnered him a trophy and a small prize.

While he was happy to earn the rank of #2, it was the social setting of it all that he felt was the best part.

“It’s more of a relaxed environment where people are just having a good time, playing a game, having a drink, and really just getting to know each other on a personal level,” Hernandez said. “That’s the best kind of way to make relationships, right? It’s kind of like when people always say the best kind of business is made on a golf course.”

But in the two days that followed at B2B Finance Expo, Hernandez and the Idea team that was there along with him were in business mode.

“97% of our business is through ISO channels and through all the relationships we’ve established with brokers in our industry, and we’re looking to expand that further,” Hernandez said, noting that there are big growth plans in the works for 2026.

Idea’s line of credit is not like an MCA or the term loans commonly found around the industry. It’s a true revolving line. After every payment made, it replenishes the line. The process to get approved is quick and easy. Hernandez said that some brokers are shocked by how good it is and that larger businesses, ones that tend to be the most rate sensitive, find it very attractive.

Idea’s line of credit is not like an MCA or the term loans commonly found around the industry. It’s a true revolving line. After every payment made, it replenishes the line. The process to get approved is quick and easy. Hernandez said that some brokers are shocked by how good it is and that larger businesses, ones that tend to be the most rate sensitive, find it very attractive.

When deBanked first covered Idea Financial in 2019, Hernandez had not yet joined the company. He came on board the following year during covid and started in an entry level position. He’s since moved up the ranks and now oversees the entire sales and marketing department, which includes anything from ISO relations to marketing. He cites the team and the structure of how it operates as being the key to success. One of the things he first learned when he started was that Idea Financial was always looking to help businesses one way or another.

“I found my way to Idea Financial and have loved it ever since,” Hernandez said.

And while business and networking are important parts of the job, regardless of where that takes him, he is proud of how well he did in that poker tournament at B2B Finance Expo.

“I was happy with my 2nd place trophy,” Hernandez said. “It’s actually right there,” he exclaimed while pointing at it. “It’s back in my office!”

PayPal: Business Loan and Working Capital Originations of $600M in Q3

November 3, 2025PayPal originated approximately $600M in business loans and working capital loans in the third quarter. A financial institution makes the loans to their clients and PayPal purchases the receivables and services the portfolio. Under this basis the company has purchased $1.6B worth of receivables for the first nine months of 2025.

“The allowance for credit losses at September 30, 2025 for our merchant receivable portfolio was $163 million, an increase from $113 million at December 31, 2024,” PayPal stated in its earnings report. “The increase in allowance for credit losses was related to a decline in credit quality of merchant loans outstanding primarily from modifications in acceptable risk parameters in 2024, which included broadened eligibility. In the second quarter of 2025, we updated our expected credit loss model for all portfolios to utilize multiple economic scenarios rather than the single scenario previously utilized. These changes did not have a material impact on our allowance for credit losses in the period.”

FICOs Are 580 and Below, Repayment Rates Are Above 97%

September 23, 2025Block recently published an interview with Juan Hernandez, the company’s Head of Credit and Underwriting for its consumer lending divisions. Among the most interesting details Hernandez revealed is that 70% of Cash App Borrow customers have FICO scores of 580 or below, but their repayment rates are above 97%.

“That is only possible because our models are continuously learning from customer activity across Cash App and Afterpay,” Hernandez said of it.

Block sees income, deposits, spending patterns, savings behavior, and repayment behavior across the spectrum of its ecosystem and is able to use that data to make better predictions than legacy third party credit indicators.

“The future of credit will be based on actual repayment ability, not outdated proxies,” Hernandez said. “With near real-time data and modern modeling, we can finally build a system that is more inclusive and safer than traditional credit scores that look backward, update slowly, and often misclassify people who are capable of managing credit.”

“The future of credit will be based on actual repayment ability, not outdated proxies,” Hernandez said. “With near real-time data and modern modeling, we can finally build a system that is more inclusive and safer than traditional credit scores that look backward, update slowly, and often misclassify people who are capable of managing credit.”

Block has made a name for itself in the lending space. Cash App Borrow originated $9B in loans in 2024 while its sister company Square Loans, which provides capital to small businesses, is the largest online small business lender that deBanked tracks. Square Loans originated $5.7B in 2024.

In March of this year Block received FDIC approval for its industrial bank, Square Financial Services Inc, to offer the Cash App Borrow loan product directly.

Idea Financial Hits Milestone, Will Still Fund in Texas

July 9, 2025

Idea Financial, a nationwide small business lender, recently surpassed $1 billion in funding since inception.

“This is a historic milestone,” said Larry Bassuk, president and co-founder of Idea Financial. “Only a few years ago, this company was just a concept with potential. Like many of the small businesses we serve, we started with confidence, grit, and the unyielding belief that we would succeed. Today, I can proudly announce that Idea Financial’s impact on the small business lending community is significant and positive. This moment belongs to our team, past and present, whose dedication has gotten us here.”

Because the company does term loans and lines of credit, it is not impacted by the recently-passed sales-based financing legislation in Texas and will continue to fund there like normal.

For background, Bassuk and Idea Financial CEO Justin Leto, actually started out in the legal profession as attorneys before taking a risk in small business lending. When deBanked first interviewed the duo in 2019, they said, “We’re not from the finance space, we’re not from the alternative lending space either, we came at this opportunity with a different approach.”

At that time, Idea had only funded $50 million since inception. Much of Idea’s growth since then can be attributed to their broker business, which it is still growing.

“Brokers and referral partners are critical to Idea’s success,” the company said. “While our borrowers are our clients, we also consider brokers and referral partners as clients by our team. We value their business and have made it a focus to develop close, mutually beneficial relationships with them.”

“We have been so fortunate to work with such a talented team, all of whom have contributed to the incredible growth of Idea,” said Leto. “We identified a problem with small business funding when we embarked on this journey, and we are so proud to have played a role in providing the solution that has fueled so many Main Street success stories.”