Underwriting Canadian SMB Loans and MCAs? You Still Need to Watch Out for Fraud

August 4, 2026 Back in February, Trust Science acquired Lenders API, a real-time fraud-prevention and consortium-data platform developed in collaboration with the Canadian Lenders Association and its small business, consumer, and automotive finance members. The platform is designed to address bust-out fraud, synthetic identity fraud, and loan stacking. Not all “stacking” is fraud, of course, but a recent deBanked feature reported that stacking business loans and MCAs is certainly on the rise.

Back in February, Trust Science acquired Lenders API, a real-time fraud-prevention and consortium-data platform developed in collaboration with the Canadian Lenders Association and its small business, consumer, and automotive finance members. The platform is designed to address bust-out fraud, synthetic identity fraud, and loan stacking. Not all “stacking” is fraud, of course, but a recent deBanked feature reported that stacking business loans and MCAs is certainly on the rise.

“No single lender can solve this problem alone,” said Tal Schwartz, co-founder of Lenders API, when the acquisition was announced. “Loan stacking and organized fraud thrive in the gaps between institutions. The only effective response is shared intelligence delivered through a compliant, trusted infrastructure.”

But wait—fraud? In Canada? According to a 2022 BBC feature, one of Canada’s defining characteristics is its “deep reservoir of niceness.” Those on the front lines in finance, however, say fraud happens there just as it does anywhere else.

“It’s quite a wild west,” said YaMing of Xuper Funding, a small business finance company that operates in both the United States and Canada. “…compared to the United States I would say it’s almost the same level of fraudulent files.”

“…my gut is going to be that it’s probably on par, relatively speaking [with the US],” said Jodi Levy, Head of Sales and Business Development for BizFund in Canada. Levy added that underwriting applications in Canada involves many of the same checks conducted by American companies regardless.

“I think the general idea is literally the same,” said Alex Xu, CEO of Xuper Funding, who works with YaMing. “It’s still against the revenue, it’s still about checking the fundamentals, checking the anti-fraud, so the procedures are literally the same.” The challenge, according to Xu, is that Canada’s credit-reporting infrastructure is not as mature as that of the United States. Data sources and access can also vary by province.

And it can be even more difficult to make a proper evaluation when a business owner has recently emigrated to Canada and has not had the same opportunity as a native-born citizen to build a public credit footprint over time. Twenty-three percent of Canadians are immigrants, for example, and that figure could rise to 34% by 2041. The total population of Canada today numbers around 41 million people.

Levy of BizFund said one advantage of operating in a smaller market is that news about fraud travels quickly, especially when a broker is involved. Discussing a hypothetical case involving an altered financial document, she said “It just wouldn’t fly. You’d be blacklisted so fast.”

In a sense, Lenders API was founded on that principle of sharing: The industry took fraud prevention into its own hands by creating a system through which participants could identify and report suspicious activity to one another. The company that acquired it, Trust Science, “is Canada’s third and most modern credit bureau,” according to its website.

Similarly, bad deals, like fraud, can also be reported through DataMerch, a U.S.-founded platform that also relies on members to report negative business dealings. Launched in 2015, DataMerch accumulated 100,000 records of unsatisfactory U.S. MCA deals by January 2023 and is still growing. Today, its database also includes Canadian businesses as well.

“Our Canadian search/merchant upload is based off the 9-digit Business Number,” said Scott Williams, co-founder of DataMerch. “Canadian funders can search by Business Number or legal name.”

Several companies that spoke with deBanked said defaults on Canadian business loans and MCAs can occur for many reasons, some fraudulent and some not. Certain forms of fraud can be nearly impossible to detect because the paperwork is authentic, the business is legitimate, and the only hidden element is the applicant’s intent to disappear as soon as the deal is completed. The fraud, in those cases, is in their mind.

But the Canadian market is not defined solely by fraud, nor is any market. There is plenty of good business and plenty of good deals, often beginning with strong broker relationships.

“If you have a good ISO partner to work with, they’re going to be transparent with you,” said Xu of Xuper Funding. “They’re going to work with you, they’re going to be very collaborative with you, and they’re going to syndicate with you. And that’s the ISO we really cherish and value.”

For Levy of BizFund, transparent communication begins at the outset.

“When I’m onboarding people, I kind of like to do the work upfront to make sure I understand,” she said. Although BizFund remains mindful of fraud and the warning signs that accompany it, Levy said that ultimately “the market is a lot of fun, there’s a lot of room to have an impact.”

Lightspeed: Merchant Cash Advance Business Key to Delivering Long-Term Shareholder Value

July 31, 2026“For us, it’s really about where we are investing to deliver long-term shareholder value,” said Lightspeed CFO Asha Bakshani during the company’s FY Q1 2027 earnings call. “For now, that is really the Merchant Cash Advance business and returning cash to our shareholders through buybacks.”

Lightspeed described MCA as a “high-margin business” that has grown for them by 56% year-over-year.

“Aside from the potential share buyback, our largest use of cash will be the continued growth of our Merchant Cash Advance program,” Bakshani said. “There were $160 million in MCAs outstanding at the end of the quarter, and we intend to continue expanding this high-margin program over time. As we grow the program, we remain disciplined in our underwriting, and default rates have stayed consistent in the low single-digit range, which gives us confidence to continue expanding.”

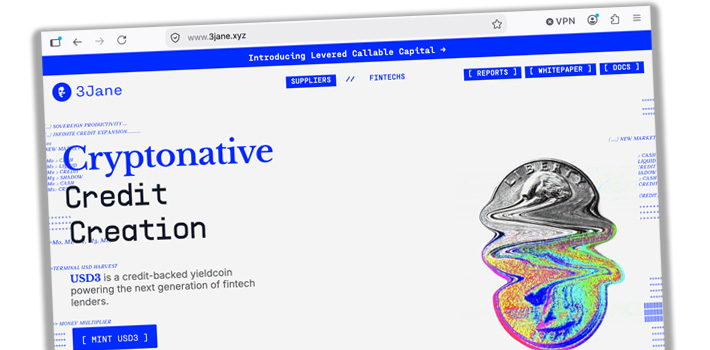

Need Capital for Your Funding or Lending Company? 3Jane Does it On Blockchain

July 27, 2026“I’m a big believer in agentic capital markets. I think we’re going to see a Cambrian explosion of novel primitives, driven largely by two pieces. Today, it’s just very easy to construct arbitrary financial building blocks using smart contracts,” said Jacob Chudnovsky, Founder of 3Jane, to deBanked.

3Jane provides credit facilities and forward flow arrangements across a range of products, including consumer loans, small business loans, and even merchant cash advances. The company previously provided a $10 million senior warehouse facility to consumer lender LendSwift, for example, and followed that with an inaugural $8.5 million purchase of small business loans from Slope, an embedded credit infrastructure provider that powers business lending programs for major players across the US, including Amazon. According to Chudnovsky, 3Jane would like to do even more deals in the small business lending and MCA space.

But with a twist.

3Jane has built an entire protocol on the blockchain. It offers a credit-backed “yieldcoin” that earns its yield “from warehouse facilities, forward-flow programs, and credit-lines.” Investors can mint the coin on Ethereum, and it earns a yield backed by the performance of 3Jane’s credit assets. Minting is not open to US investors, but the company’s capital markets offerings are focused exclusively on North America. So, if you’re a small business funder seeking a credit facility or forward flow arrangement, 3Jane wants to speak with you.

3Jane has built an entire protocol on the blockchain. It offers a credit-backed “yieldcoin” that earns its yield “from warehouse facilities, forward-flow programs, and credit-lines.” Investors can mint the coin on Ethereum, and it earns a yield backed by the performance of 3Jane’s credit assets. Minting is not open to US investors, but the company’s capital markets offerings are focused exclusively on North America. So, if you’re a small business funder seeking a credit facility or forward flow arrangement, 3Jane wants to speak with you.

Chudnovsky is a software engineer by trade and entered the DeFi space in 2020.

“…around 2024, I basically came to the realization that credit is still an extremely underdeveloped vertical in crypto and particularly both the capital aggregation and the capital distribution side of it,” he said. “My initial focus was ‘can we get the best of crypto to distribute capital in a better way?’ and so I founded 3Jane, and we started off by doing unsecured lines of credit for crypto users in the United States who had a bunch of these different assets and could not really borrow against it in a streamlined way.”

That effort eventually led to 3Jane’s current business model. If the name 3Jane sounds familiar, it’s because Chudnovsky drew it from the 1984 novel Neuromancer, the famous William Gibson book that coined the phrases “cyberspace” and “the matrix.” By pure coincidence, Apple TV is releasing a 10-episode series based on the book in January 2027.

That effort eventually led to 3Jane’s current business model. If the name 3Jane sounds familiar, it’s because Chudnovsky drew it from the 1984 novel Neuromancer, the famous William Gibson book that coined the phrases “cyberspace” and “the matrix.” By pure coincidence, Apple TV is releasing a 10-episode series based on the book in January 2027.

“I just think we’re going to enter this complete renaissance of new different financial primitives and I think it’s going to drive a lot of adoption, new ways of thinking about our financial system and that sort of really resonated with me with the book,” Chudnovsky said.

And that new way of thinking is starting to take root. The capital markets utilizing blockchain to create efficiencies is already cropping up around the industry. Since 3Jane last spoke with deBanked, its purchase of embedded finance products from Slope has increased to a total of $60 million.

3Jane’s customers do not need to be crypto experts. The company handles that side of the transaction while underwriting the risk and executing what is otherwise a conventional capital markets deal, but one in which the infrastructure is robust enough that this can be a lender’s first and last facility. On 3Jane’s part, doing this requires a strong understanding of the various financial products it evaluates, including MCA.

“…there are a number of MCA operators in the United States that are doing things right, they’re growing significantly and they need leverage to scale their business,” Chudnovsky said. “and so warehouse facilities and to a lesser extent forward-flows for MCAs sort of equally make sense for them as long as you are cognizant of the risks.”

Stripe Capital, PayPal Working Capital Could Merge If Acquisition Offer is Accepted

July 19, 2026The old rumor that Stripe was interested in acquiring PayPal was apparently true. Partially anyway. This past April, Stripe, along with Block and Advent (a private equity firm), let PayPal know they were jointly interested in acquiring it. But Block dropped out of the deal and the newest acquisition offer, now public, comes from just Stripe and Advent together. While Stripe and PayPal are obviously known as payment processing companies, the two originate more than $3 billion a year in MCAs and short term business loans a year combined.

PayPal is one of the few online payment platforms to struggle with bad debt in its merchant funding program and the company had never weaponized its lending offerings to grow PayPal’s business. Nevertheless, its origination volume outpaced Stripe’s in 2025. Stripe and Advent offered $53 billion to acquire PayPal. It remains to be seen if a deal will actually happen.

American Brokers Help Fuel Canada’s Small Business Finance Boom

July 10, 2026 Canada’s small business finance industry is growing, and behind the scenes, American brokers are helping fuel that momentum.

Canada’s small business finance industry is growing, and behind the scenes, American brokers are helping fuel that momentum.

“They’re kind of killing it here right now, from what we see from the partners that we work with,” said Vlad Sherbatov, President & Co-founder of Smarter Loans, an online lending marketplace in Canada. “…for the American players that have come in, they’re already really good at the broker channel.”

Some Canadian small business funders, particularly those offering an MCA product, told deBanked that a significant amount of deal volume is coming from south of the border. And with that, the environment and culture of the business itself is beginning to shift. In their view, it is becoming more Americanized.

“…a lot of the Americanization of the industry, if you will, is coming from US brokers and funders,” said Avrohom Bernstein, CEO at 2M7 Financial Solutions.

Part of that shift is a new level of competition among firms as brokers try to maximize the options available to their clients. Bernstein, for example, said it often starts with an American broker inquiring about submitting a few Canadian deals. Lately, however, it’s been escalating into situations where eight different brokers might submit the same clients.

“Every deal now you’ve got to hustle, you’ve got to fight, you have to really work it,” Bernstein said.

That competition once meant fighting to become the one and only exclusive partner for a merchant. Now, it has become more common to find that a submitted applicant already has multiple active advances.

“…that used to be unheard of in Canada, like that used to be excessively unusual to see more than three positions, now ten is not insane anymore,” said Bernstein. “It really escalated in a way that we haven’t seen, and that’s probably over the last 12, maybe 24 months, that it started really picking up,” Bernstein said.

Jodi Levy, Head of Sales and Business Development for BizFund in Canada, said she has made a similar observation. When she first started in the industry there, something like a third position was unheard of. Now, she said, they see it much more often.

“I feel like that’s definitely more an American influence,” Levy said.

BizFund has a large American operation as well, so the company is no stranger to how things work on the other side of the border. But like others, its Canadian funding arm also works with the American broker community.

“…partners are great, American, Canadian, we don’t care where you’re from, as long as you’ve got good business,” Levy said, adding that what matters is whether those partners have a direct relationship with their merchants. She also said that working with the broker community requires operating with a sense of urgency, something she has instilled in her team as a culture of NOW.

The diversity of products brokers can offer may not be as wide as what is available in the US. Sherbatov said that once a business steps outside of traditional banking sources, it is essentially entering MCA territory. As a result, much of the new competition entering the space is focused there.

“Among the new players that have come in, MCA is definitely the product that they’ve been leading with,” Sherbatov said.

“We have like five or six banks, and then like a couple credit unions, and then there’s not really anyone between, and there’s A-paper guys, and then B, C, D type of guys,” said Bernstein of 2M7.

According to Statistics Canada, banks provided 68.5% of all capital to SMEs in 2023, while credit unions and government institutions provided 20.6% and 9.4%, respectively. Only 2.2% was funded by “online alternative lenders.” The total market size at the time was estimated at $94 billion.

“I think the big gap is—there’s tons of businesses that want capital,” said Rafael Rositsan, CEO and co-founder of Smarter Loans. “There are some funders that offer it, but they’re pretty tight, and I feel like if somebody can come in and take on a bit more risk and open up their books a bit, then there’s plenty opportunity to fund a lot of Canadian businesses.”

As for why there has been such a push from Americans into Canada, no one pointed to a single definitive reason, but the runway for growth in the alternative lending segment, as illustrated by the report, may provide a clue as to the interest. Bernstein of 2M7 said there has long been a pattern of Americans entering and exiting the Canadian market, but he had also long believed that sustained success required boots on the ground. Now, he is reconsidering that view, at least on the broker side, as the current wave of broker entrants appears to be holding more firm. For funders, however, he said it still does not really work as a remote business.

As for why there has been such a push from Americans into Canada, no one pointed to a single definitive reason, but the runway for growth in the alternative lending segment, as illustrated by the report, may provide a clue as to the interest. Bernstein of 2M7 said there has long been a pattern of Americans entering and exiting the Canadian market, but he had also long believed that sustained success required boots on the ground. Now, he is reconsidering that view, at least on the broker side, as the current wave of broker entrants appears to be holding more firm. For funders, however, he said it still does not really work as a remote business.

“Every funder that’s actually doing decent volume is here, except for one,” Bernstein said.

In 2019, deBanked held a conference in Toronto for what was then a burgeoning small business finance industry, but held off on further events there after Covid disrupted plans for 2020 and 2021. It did not go unnoticed, however, that deBanked’s more recent American-based events have had more email addresses ending in .ca on the attendee lists. At the most recent Broker Fair conference in New York City, for example, some firms were exclusively advertising Canadian funding products to American brokers.

Canada’s population is relatively small, at roughly 41 million residents. That is about the size of California and only 25% larger than Texas. Homegrown Canadian brokerages do exist, of course, and a lot of business in Canada stays within Canada. Not all of the deals are originating through brokers either. Some merchants prefer to work directly with a funding source, while others prefer the comfort of applying through a Canadian lending marketplace like Smarter Loans, for example. If a merchant is ultimately eligible for some kind of funding, Sherbatov said, they are going to know it through their platform.

“We love the fact that we can help the small business economy thrive in the country, it’s responsible for a lot of positive things,” Sherbatov said. And whether the funding sources originate from Canada or the US, he said those companies ultimately find their way to them.

“We’re just becoming a more critical part of that journey for the merchant, and I think that explains why a lot of the new companies, when they come in, they gravitate toward us,” said Sherbatov. “…because in the business financing space we’ve carved out a nice niche for ourselves after Covid, and usually the new players gravitate to us because they know that merchants come to us as well.”

Levy of BizFund said part of the Canadian business experience is kindness. “That stuff goes far, we love that stuff up here in Canada,” she said. On the company website, photos of the company’s team, including Levy, show them smiling and ready to fund businesses.

For stalwarts like 2M7, which launched in Canada in 2008, the market’s evolution has been dramatic. Bernstein said the industry has gone from being a bit quiet and under the radar to seeing a lot of energy recently, whether from American brokers or from Canadian brokers that have decided this is the niche they are going to focus on entirely.

“In the US, I know a lot of brokers who also do equipment and also term loans and also SBA and also all this other type of stuff, it doesn’t exist so much in Canada,” Bernstein said. “It’s like if you’re selling to small businesses and you’re offering them financing, there’s not that many products you could line up, so it’s like if you’re doing brokerage, you got to be all in, like if you’re doing MCA, you got to do MCA.”

“I think that it was evident to a lot of players outside of the market that there is a big market opportunity that’s untapped,” Sherbatov said, “just because so little financing is being released by alternative lenders, that they started to come into the space, and we’ve seen, I mean, not even for the past two years, but I’d say in the past 18 months, our own roster of business lenders on Smarter Loans has doubled, like we went from 10 to where now we have 20, and the majority of that expansion actually happened from US players coming into the country.”

And the growth is just getting started.

“There’s a lot more room for it,” said Rositsan of Smarter Loans.

Factoring to Take MCA Fight to Federal Level

July 2, 2026In the wake of new merchant cash advance laws passed in Texas and Vermont, American Factoring Association President Cole Harmonson posted the next step is to take the fight against MCAs to the federal level.

Post below:

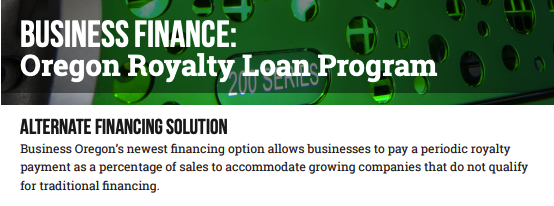

Oregon Offers Revenue-Based Financing With 2.0 Factor Rates

June 29, 2026 The State of Oregon is in the revenue-based financing business, offering small businesses funding up to $1 million in exchange for a percentage of their future sales and a 2.0 factor rate payback.

The State of Oregon is in the revenue-based financing business, offering small businesses funding up to $1 million in exchange for a percentage of their future sales and a 2.0 factor rate payback.

It’s called the Oregon Royalty Loan Program and the factor rate cost is branded as a 2X Royalty. Eligibility is based off of historical sales and projected future sales.

“Oregon Royalty Loans are repaid at a predetermined percentage of sales / revenue on a monthly basis until an overall amount, typically 2X, is returned,” the State touts.

An official flyer for the program says that merchants only have to make the required royalty percentage up until they’ve paid 2x the funded amount in full, which could take up to 3-5 years, at which point the royalties stop. The flyer for the program also labels royalty financing as “revenue-financing” in its example at the bottom.

“The percentage of sales varies with each project, but will yield a 2X return from royalty payments over a three– to five–year period,” the State says. “Once the 2X repayment has been achieved, royalty payments stop, and the company has satisfied its repayment obligation.”

Promotional materials say that this may better align with a business’s cash flow.

In Oregon’s official business code, it defines Royalty in the program as “payments calculated as a percentage of the borrower’s sales or revenue as a means of effecting an adequate rate of return typically up to 2X on the monies loaned, as determined at the sole discretion of the Department.”

2X is deemed an “adequate rate of return.” The product is collateralized and personally guaranteed.

The program is similar to New York City’s Revenue-Based Loan Program heralded by Mayor Mamdani and the State of Washington’s Revenue-Based Financing Fund.

Parafin Has Funded 50,000 Businesses, How Does That Compare?

June 25, 2026Parafin’s new credit facility with Goldman Sachs was complemented by the disclosure that the company had funded more than 50,000 businesses since inception. Founded in 2020, Parafin typically markets how much it has extended in “offers” to small businesses rather than how much it has actually funded. This bucks the prevailing industry trend.

To put Parafin’s 50,000 deals funded over the last 5 years into perspective, the industry leading online lender, Square Loans, funded approximately 700,000 loans last year alone.

Parafin disclosed revenue in 2025 as $90M, which is approximately double that of Lightspeed Capital over the same time period. Lightspeed originated $340M in MCAs in 2025.

Parafin says that the majority of its fundings go to repeat borrowers. The company powers platforms such as Amazon, Walmart, DoorDash, Gusto.