business cash advance

Square: Our Customers Actually Grow Faster With a Square Loan Than Without One

November 7, 2024On average, Square customers that used the Square Loan product grew 6% faster than those that did not use it, the company revealed. Jack Dorsey, the CEO of Square’s parent company, Block, used the 3rd quarter earning’s period as an opportunity to discuss its lending operations. The relevant parts are excerpted in non-sequential order below:

“In 2013, we began offering capital to sellers because we saw a meaningful gap in the market: small businesses were often denied access to credit, in the same way they were once denied access to accepting credit cards. We utilized our deep understanding of the seller and their business to build a technology that invited them to accept a loan with transparent rates, and pay back simply by making sales to their customers. We called it Square Capital (which is now known as Square Loans).

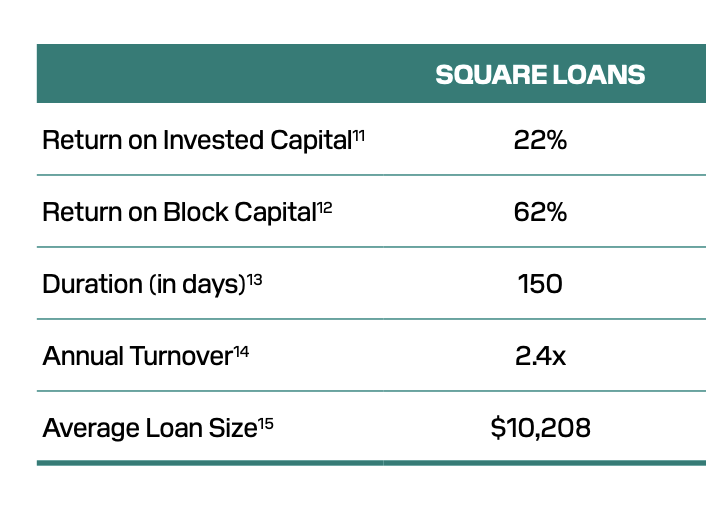

Since then, we’ve underwritten more than $22 billion in loans globally, with aggregate loss rates below 3%. And we’ve proven we can expand access: 58% of Square Loans are to women-owned businesses, and 36% are to minority-owned businesses, both of which are higher than the benchmark we track If our sellers grow, we grow – and we believe Square Loans has a direct impact on our sellers’ growth. Sellers who take out a Square Loan grew on average 6% faster than sellers who did not take out a loan.

Many financial products trap borrowers in cycles of revolving debt. We don’t allow customers to take on new loans if they have an overdue balance. And repayment is built into how our products work: Square sellers repay loans through a fixed percentage of their revenue, creating a manageable-real-time payment flow.

On credit risk management, we have a long history of maintaining stable loss rates and these products act as working capital, which means they are usually short in duration. What that means for us is that a dollar used on our balance sheet can turn multiple times, driving capital efficiency while providing us with high-quality data to continually refine our technology-driven underwriting.””

-Jack Dorsey

Square shared some stats as well, showing that the average loan term was 150 days and average loan size is only $10,208.

Loss rates on Square Loans have historically been less than 4%. Square is a company to watch considering it is likely the largest online business lender in the United States.

Yes Lender Becomes Fintegra, Brings on Former Federal Reserve Vice Chair

November 15, 2021 Yes Lender is now Fintegra. Along with the name change, the company is bringing on Roger Ferguson, former Vice Chair of the Federal Reserve (1997-2006) in an advisory role. Ferguson is also an investor in Fintegra.

Yes Lender is now Fintegra. Along with the name change, the company is bringing on Roger Ferguson, former Vice Chair of the Federal Reserve (1997-2006) in an advisory role. Ferguson is also an investor in Fintegra.

“Our new name combines ‘fintech’ with ‘integrity’” said Glenn Forman, CEO at Fintegra. [The name] serves as a daily reminder to our customers and colleagues of our mission and values, which we take very seriously.”

The company’s goal is seemingly to write a lot of deals, and get them funded as fast as possible through a fintech application process. According to a press release, the online application can get merchants their funds within 24 hours of their application being submitted.

When touching upon Fintegra’s goals with the rebranding, Forman spoke on a good work environment along with customer-centric business decisions. “We’re committed to putting capital in the hands of entrepreneurs so they can grow their businesses and improve the lives of their customers, suppliers and employees, and we’ll continue to do so in a highly ethical and empathetic way.”

When speaking about the partnership with Ferguson, Forman believes this unprecedented addition will bring equally unprecedented opportunities to this company.

“We’re incredibly fortunate to be able to tap Roger’s wisdom and experience to accelerate Fintegra’s growth. His track record of success and impeccable ethics are perfectly aligned with our brand.”

Forman and Ferguson are looking to rekindle an old working relationship to help Fintegra take off. “While it’s been a few years since we worked together at McKinsey & Company, it feels great to be joining forces again to take Fintegra to new heights.”

deBanked Visits Local Commercial Finance Brokerage – Horizon Funding Group

October 22, 2020deBanked reporter Johny Fernandez visited the storefront office of Horizon Funding Group, a commercial finance brokerage located in Brooklyn. The company is owned by brothers James and John Celifarco.

CAN Capital Hired a New CFO: Here’s His Take On The Company

July 23, 2019 The last 12 months have seen plenty of developments within the offices of CAN Capital. September witnessed the announcement of a new credit facility of $287 million with Varadero Capital. January brought news of the hiring of a new CEO. And now, completing the hat trick is CAN’s employment of John McNeill as its CFO.

The last 12 months have seen plenty of developments within the offices of CAN Capital. September witnessed the announcement of a new credit facility of $287 million with Varadero Capital. January brought news of the hiring of a new CEO. And now, completing the hat trick is CAN’s employment of John McNeill as its CFO.

Coming from years of experience in finance, with firms such as Ocwen Financial and Zume, McNeill is stepping into his role with an optimism normally reserved for those at the offset of a new business. Saying that due to recent restructuring, new hirings, and CAN’s re-evaluation of its position in the market over the previous two years, McNeill believes that the company “feels like it’s a nimble startup.” Albeit a startup that has been in the industry for over 20 years.

Founded in 1998 by a small business owner who struggled to be approved for a business loan, CAN has been cemented as a legacy figure within the alternative finance industry. Having persevered through the ’08 crash as well as other economic hiccups over the past two decades, CAN is uniquely positioned in that it has 20 years worth of experience and data, not to mention the personnel who have stuck around to become veterans as well, to guide them through the current moment of market saturation.

And it is the synergy between these two aspects of CAN, the new and the old, that initially drew McNeill to the company. The opportunity to work alongside people who have decades of experience in the market, as well as those who have only been there a few months longer than himself, led McNeill to view CAN as an anomaly, where it’s “like being the new guy, but with all of the tools of historical experience.”

This freshness tempered by lessons learned in the past is also attributed by McNeill to CAN’s CEO, Edward J. Siciliano, who’s worked in commercial financing, sales, marketing, and operations for over 30 years; and who has aimed to expand operations, both technologically and geographically, since his taking up of the role.

McNeill believes that there continues to be plenty of the market left to expand into, saying there’s “still a lot of opportunities to make money and to help secure funding for businesses across America.”

OnDeck Already Filed Form S-1

September 27, 2014 Back on August 14th, the Wall Street Journal reported that OnDeck was preparing to file for an initial public offering. Since then, industry insiders have been bustling with anticipation to see the S-1 filing, the document that would reveal once and for all their true financial standing.

Back on August 14th, the Wall Street Journal reported that OnDeck was preparing to file for an initial public offering. Since then, industry insiders have been bustling with anticipation to see the S-1 filing, the document that would reveal once and for all their true financial standing.

Update 11/18/14: Click to see OnDeck’s Public S-1 Filing

In between then and now, Lending Club, their rival in the business loan market, filed their S-1 on August 27th. The peer-to-peer lending world went nuts and merchant cash advance veterans such as AmeriMerchant’s David Goldin were asked to comment on BloombergTV.

And then… things quieted down. OnDeck went radio silent on August 14th, despite the SEC requiring such only after the S-1 form had actually been filed. Speculation began to build as to whether or not the WSJ report in August was a false alarm or misinformation. And with no word from the industry’s beloved charismatic superstar Noah Breslow, something seemed to be amiss.

And then the Financial Times dropped the bombshell that the registration documents had already been filed… last month… confidentially.

Admittedly, I didn’t even know a company could file confidentially, a process done offline so that it is not recorded electronically. Thanks to the JOBS Act, companies with less than a billion dollars in revenue can submit draft versions of their registration documents to the SEC, allowing the SEC to review, revise, and agree on a final version that will ultimately have to be made public. The takeaway here is that an OnDeck IPO is in the process and the registration documents will eventually be released. The law states that OnDeck must make the documents public at least 21 days prior to pitching investors.

The New Yorker walked readers through confidential registrations back when Twitter was planning their IPO, noting that it was not uncommon to choose this method, “Twitter is much like its peers: most small companies that have gone public since the passage of the JOBS Act have filed their S-1s confidentially,” the New Yorker said.

So why be secretive? The New Yorker continues to explain:

From the perspective of companies, the new rule has a couple of virtues. First, it allows companies that are thinking about going public to test the waters—they can gauge investor reaction, get feedback from the S.E.C. on their filings, and so on—before deciding if they want to go ahead with an I.P.O. If a company goes through that process publicly, and then decides to abandon the offering, its reputation gets damaged, even though it often makes sense for a company not to go public. Do it privately, and no one gets hurt.

-Source: http://www.newyorker.com/business/currency/the-virtues-of-twitters-confidential-i-p-o-filing

OnDeck’s biggest critics are their competitors, naysayers convinced that they are recklessly undercutting pricing to acquire market share. Indeed FT reported that OnDeck posted annual losses of $16.8m and $24.4m in 2012 and 2013, and losses of $14.4m in the first half of 2014.

With $1.3 billion funded since 2006, an independent report cited in the registration by Oliver Wyman estimates the untapped market to be between $80 billion and $120 billion.

With $1.3 billion funded since 2006, an independent report cited in the registration by Oliver Wyman estimates the untapped market to be between $80 billion and $120 billion.

There’s plenty of runway left, but OnDeck has yet to turn a profit. In An Insider’s Perspective, I wrote, “What scares their competitors though, is that this strategy has been intentional. Very few if any players in the industry have had the luxury, guts, or the purse to lose money for seven years as part of a coup to conquer the market.”

If the IPO goes through, we can all place actual monetary bets on the company’s future. What a trip that will be. I expect the stadium of insiders to get loud once the public documents are released. Good luck OnDeck.

Are We in a $300 Billion Market?

August 7, 2014 Earlier today on a large group conference call with Tom Green and Mozelle Romero of LendingClub, I learned a few more details about their business loan program. In the Q&A segment, one attendee came right out and asked if they believed their competition was merchant cash advance companies and online business lenders.

Earlier today on a large group conference call with Tom Green and Mozelle Romero of LendingClub, I learned a few more details about their business loan program. In the Q&A segment, one attendee came right out and asked if they believed their competition was merchant cash advance companies and online business lenders.

According to Green, it’s not so much other companies that they feel they are up against but more of the broad challenge of market awareness. Their struggle is about getting people to know that there are non-bank options available and to make people aware of their existence.

It’s the same challenge merchant cash advance (MCA) companies have been dealing with for more than a decade. Notably though, there are many in the MCA industry that feel the market is saturated and thus a lot of the industry’s growth has been fostered through a turf war for the same merchants. Stacking (the practice of funding merchants multiple advances or loans simultaneously) is partially spurred by a belief that there are no more untapped businesses left to fund. The acquisition costs of a brand new untouched business that is both interested and qualified is so high, that it is not a pursuit some funders and brokers can afford to take on.

Market Size

Market Size

At present, daily funders, which are a combination of both MCA companies and lenders that require daily payments, are funding somewhere between $3-$5 billion a year. On the call Green said he believed the potential market was far larger than that, though he discredited the $200 billion figure that some independent research had predicted. That was only because LendingClub believes the potential market is substantially higher, more like $300 billion.

$300 billion?! That’s about 100x larger than the current daily funder market combined and starkly contradicts any belief that there’s no merchants out there who haven’t already gotten funded.

LendingClub’s minimum gross sales requirement is $6,250 a month and they have an upper monthly gross threshold on applicants at $830,000 a month, though they’ve had businesses apply who do even more than that. Their sweet spot as Green put it, is the segment doing $16,000 to $416,000 gross per month.

I can’t help but notice that’s the same sweet spot that daily funders have. And we mustn’t forget, LendingClub’s target business owner has at least 660 FICO. If it’s a $300 billion market for good credit applicants, then it’s got to be even bigger for the ultra FICO-lenient companies in MCA.

What’s a business?

LendingClub only needs someone with at least 20% ownership to both apply for and guarantee the loan, an unheard of stipulation in the rest of alternative business lending. One cardinal rule in MCA has been that there needs to be at least 51% or 80% ownership signing the contract. That’s had a lot to do with the fact that most MCA agreements are not personally guaranteed and the signatory is required to have absolute authority to sell the business’s future proceeds.

Summer of Fraud

In 2013 the MCA industry experienced what many insiders dubbed the summer of fraud. Spurred by advances in technology, small businesses were applying for financing en masse while armed with pristinely produced fraudulent bank statements. Fake documents overwhelmed the industry so hard that today it is commonplace for underwriters to verify their legitimacy with the banks. This is done manually or with the help of tools such as Decision Logic or Yodlee.

In 2013 the MCA industry experienced what many insiders dubbed the summer of fraud. Spurred by advances in technology, small businesses were applying for financing en masse while armed with pristinely produced fraudulent bank statements. Fake documents overwhelmed the industry so hard that today it is commonplace for underwriters to verify their legitimacy with the banks. This is done manually or with the help of tools such as Decision Logic or Yodlee.

Knowing this firsthand, I asked LendingClub if they also take the care to verify bank statements. In the majority of cases they do not. They rely greatly on an algorithm that detects fraudulent answers on the application but the statements themselves are not scrutinized except in very high risk situations. Considering they’re wildly less expensive than MCAs, I find it odd that they are exposed to this type of risk. Fraudulent documents are the norm and in these underwriting conditions, I would expect them to charge as much or more than MCA companies, not less.

At the same time it’s important to mention that at present, business loans on their platform are only funded by institutional investors. Retail investors can only invest in consumer loans. LendingClub has been very transparent about excluding retail investors here for the very purpose of shielding them from unevaluated and unforeseen risk. My guess is that as time goes on, they will do more to validate the bank statements which is the bread and butter of assessing the risk and health of a business.

$300 billion

In a FICO flexible environment, it’s possible the potential for daily funders is at least $300 billion. If true, that would mean that for the 16 years that MCA players have been around, they barely reached even 1% of their target audience. I’ve been saying it since I’ve started this blog 4 years ago, every business owner I’ve spoken to has never heard of a merchant cash advance… which means saturation is a myth.

Tom Green was right, the real competition is public awareness. 99% of the potential market is untapped. If you’re fighting with 5 other companies over the same merchant, you gotta:

You gotta keep on looking now

Keep on looking now

You’re looking for love

In all the wrong places

Six Signs Alternative Lending is Rigged

August 3, 2014There’s a lot of players at the alternative lending table but there are two that have won a string of lucky hands to put them on top. Neither were the first to draw cards, nor do either of them offer something that everybody else does not. These two lenders have something in common of course, special favor with the Internet gods. Is the game rigged?

OnDeck Capital is the most celebrated alternative business lender of our time. Their daily repayment loans and fast approval times are a hit with customers. In fact, as told in their recent securitization prospectus, OnDeck has been eroding its reliance on brokers and third parties to accommodate growth through their direct channel. Direct has been good for OnDeck, very good.

LendingClub on the other hand is the big dog in consumer lending, having funded more than $5 billion since inception. Every month they shatter the previous record for volume of loans funded and they’re expected to go public within the next year. LendingClub continues to pound their distant rival Prosper in monthly loan production. Are they just better at marketing?

Curiously I can’t help but notice they have something in common, they’re both owned by Google. Google Ventures led OnDeck Capital’s series D round and Google Ventures’ Karim Faris sits on OnDeck’s board of directors. Similarly, Google owns a minority stake in LendingClub.

While neither is outright owned or controlled, It’d be surprising if Google didn’t do something to foster the success of their investments. What could a billion dollar Internet giant possibly do to give them a little push?

Stop backlinking and SEO. The game is rigged

If you reproduce a search for the same keywords, you should know that results vary depending on what kind of device you’re using (mobile vs. desktop), what zip code you’re in, what time of the day it is, whether or not you’re logged into Gmail/Google+/Youtube, and whether you’ve searched for related topics before. I performed my searches with a fresh desktop browser on a Sunday evening in NYC with all cookies, cache, and Google account sessions wiped clean.

You might not get exactly what I get and I realize that obfuscates the conspiracy I’m trying to establish here. If you do witness peculiar keyword domination though, keep an open mind that there might be more going on than good SEO and strong natural backlinking brought on by mainstream media publicity. Plenty of big businesses that dominate offline fail to rank well in the top ten results online.

You might not get exactly what I get and I realize that obfuscates the conspiracy I’m trying to establish here. If you do witness peculiar keyword domination though, keep an open mind that there might be more going on than good SEO and strong natural backlinking brought on by mainstream media publicity. Plenty of big businesses that dominate offline fail to rank well in the top ten results online.

Search engines say that if you’re popular, you’ll rank well. But there are plenty of cases where ranking well has made businesses popular.

Maybe, just maybe the game is rigged…