technology

Google to Begin Offering Checking Accounts in 2020

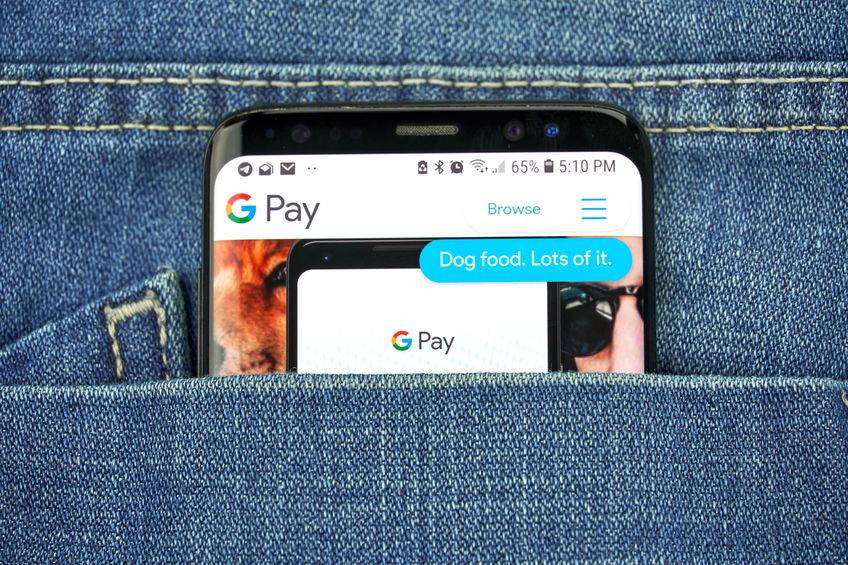

November 16, 2019 This week Google announced that it plans to offer checking accounts to customers in 2020. The news comes after the release of the Apple Card, Apple and Goldman Sach’s controversial joint project, in August; this week’s release of Facebook Pay; and the mass exodus by payments companies from Facebook’s Libra Association last month.

This week Google announced that it plans to offer checking accounts to customers in 2020. The news comes after the release of the Apple Card, Apple and Goldman Sach’s controversial joint project, in August; this week’s release of Facebook Pay; and the mass exodus by payments companies from Facebook’s Libra Association last month.

Titled as Google’s ‘Cache’ project, the accounts will be the result of a partnership between the tech giant and a selection of banks and credit unions. Thus far, Citigroup and a credit union based in Stanford University have been confirmed as partners, with more to be announced. Speaking on the venture, Citigroup spokesperson Liz Fogarty said the “agreement has the potential to expand the reach and breadth of our customer base.” Whereas Joan Opp, President and CEO of Stanford Federal Credit Union, remarked that the deal would be “critical to remaining relevant and meeting customer expectations.”

As of yet, not much is known beyond these partners and that the checking accounts will be in some way “smart” according to Google spokesperson Craig Ewer. Whether or not there will be fees attached to the accounts, or who will be the target audience remain unsure. The latter especially given Google Pay’s poor take up in America.

As well as all this, it is equally unclear what exactly Google will be bringing to banking that is new. In his statement, Ewer said that “we’re exploring how we can partner with banks and credit unions in the US to offer smart checking accounts through Google Pay, helping their customers benefit from useful insights and budgeting tools while keeping their money in an FDIC or NCUA-insured accounts.” Such “insights” and “tools” are yet to be expanded upon and may give cause to alarm, as the company has recently come under fire for its questionable use of data after it was revealed that Google has secretly gathered the personal medical data of 50 million Americans from healthcare providers; and has recently been accused of using both human contractors and algorithms to tweak search engine results, potentially exhibiting favoritism as well as a willingness to change results related to at least one major advertiser.

When asked by CNBC about Google’s plans to enter finance, Senator Mark Warner (D) was apprehensive, remarking that “large platform companies have not had a very good record of protecting the data or being transparent with consumers.” Warner, who was a tech entrepreneur before entering politics, believes more regulation should be in place as the number of tech companies looking to enter finances continues to increase, saying, “once they get in, the ability to extract them out is going to be virtually impossible.”

Such comments come in the wake of Facebook CEO Mark Zuckerburg’s testimony to Congress last month, in which he told the representatives: “I view the financial infrastructure in the United States as outdated.” Just how outdated Zuckerburg and his contemporaries believe it to be will become clearer as more of these Big Tech-Wall Street hybrids are released.

Is Your Firm Ready for Machine Learning?

October 15, 2018Artificial intelligence such as machine learning has the potential to dramatically shift the alternative lending and funding landscape. But humans still have a lot to learn about this budding field.

Across the industry, firms are at different points in terms of machine learning adoption. Some firms have begun to implement machine learning within underwriting in an attempt to curb fraud, get more complex insights into risk, make sounder funding decisions and achieve lower loss rates. Others are still in the R&D and planning stage, quietly laying the groundwork for future implementation across multiple areas of their business, including fraud prevention, underwriting, lead generation and collections.

“It’s entirely critical to the success of our business,” says Paul Gu, co-founder and head of product at Upstart, a consumer lending platform that uses machine learning extensively in its operations. “Done right, it completely changes the possibilities in terms of how accurate underwriting and verification are,” he says.

While there’s no absolute right way to implement machine learning within a lender’s or funder’s business, there are many data-related, regulatory and business-specific factors to consider. Because things can go very wrong from a business or regulatory perspective—or both—if machine learning is not implemented properly, firms need to be especially careful. Here are a few pointers that can help lead to a successful machine learning implementation:

Using machine learning, funders can predict better the likelihood of default versus a rule-based model that looks at factors such as the size of the business, the size of the loan and how old the business is, for example, says Eden Amirav, co-founder and chief executive of Lending Express, a firm that relies heavily on AI to match borrowers and funders.

Machine learning takes hundreds and hundreds of parameters into account which you would never look at with a rule-based model and searches for connections. “You can find much more complex insights using these multiple data points. It’s not something a person can do,” Amirav says.

He contends that machine learning will optimize the number of small businesses that will have access to funding because it allows funders to be more precise in their risk analyses. This will open doors for some merchants who were previously turned down based on less precise models, he predicts. To help in this effort, Lending Express recently launched a new dashboard that uses AI-driven technology to help convert business loan candidates that have been previously turned down into viable applicants. The new LendingScore™ algorithm gives businesses detailed information about how they can improve different funding factors to help them unlock new funding opportunities, Amirav says.

Lenders and funders always have to be thinking about what’s next when it comes to artificial intelligence, even if they aren’t quite ready to implement it. While using machine learning for underwriting is currently the primary focus for many firms, there are many other possible use cases for the alternative lenders and funders, according to industry participants.

Lead generation and renewals are two areas that are ripe for machine learning technology, according to Paul Sitruk, chief risk officer and chief technology officer at 6th Avenue Capital, a small business funder. He predicts that it is only a matter of time before firms are using machine learning in these areas and others. “It can be applied to several areas within our existing processes,” he says.

Collection is another area where machine learning could make the process more efficient for firms. Machines can work out, based on real-life patterns, which types of customers might benefit from call reminders and which will be a waste of time for lenders, says Sandeep Bhandari, chief strategy and chief risk officer at Affirm, which uses advanced analytics to make credit decisions.

“There are different business problems that can be solved through machine learning. Lenders sometimes get too fixated on just the approve/decline problem,” he says.

“Most underwriters don’t have enough data to effectively incorporate AI, deep learning, or machine learning tools,” says Taariq Lewis, chief executive of Aquila, a small business funder. He notes that effective research comes from the use of very large datasets that won’t fit in an excel spreadsheet for testing various hypotheses.

Problems, however, can occur when there’s too much complexity in the models and the results become too hard to understand in actionable business terms. For example, firms may use models that analyze seasonal lender performance without understanding the input assumptions, like weather impact, on certain geographies. This may lead to final results that do not make sense or are unexpected, he says.

“There’s a lot of noise in the data. There are spurious correlations. They make meaningful conclusions hard to get and hard to use,” he says.

The more precise firms can be with the data, the more predictive a machine learning model can be, says Bhandari of Affirm. So, for example, instead of looking at credit utilization ratios generally, the model might be more predictive if it includes the utilization rate over recent months in conjunction with debt balance. It’s critical to include as targeted and complete data as possible. “That’s where some of our competitive advantages come in,” Bhandari says.

Underwriters also have to pay particularly close attention that overfitting doesn’t occur. This happens when machines can perfectly predict data in your data set, but they don’t necessarily reflect real world patterns, says Gu of Upstart.

Keeping close tabs on the computer-driven models over time is also important. The model isn’t going to perform the same all along because the competitive environment changes, as do consumer preferences and behaviors. “You have to monitor what’s going well and what’s not going well all the time,” Bhandari says.

Certainly, as AI is integrated into financial services, state and federal regulators that oversee financial services are taking more of an interest. As such, firms dabbling with new technology have to be very careful that any models they are using don’t run afoul of federal Fair Lending Laws or state regulations.

“If you don’t address it early and you have a model that’s treating customers unfairly or differently, it could result in serious consequences,” says Tim Wieher, chief compliance officer and general counsel of CAN Capital, which is in the early stages of determining how to use AI within its business.

“AI will be transformative for the financial services industry,” he predicts, but says that doing it right takes significant advance planning. For instance, Wieher says it’s very important for firms to involve legal and compliance teams early in the process to review potential models, understand how the technology will impact the lending or funding process and identify the challenges and mitigate the risk.

“AI will be transformative for the financial services industry,” he predicts, but says that doing it right takes significant advance planning. For instance, Wieher says it’s very important for firms to involve legal and compliance teams early in the process to review potential models, understand how the technology will impact the lending or funding process and identify the challenges and mitigate the risk.

To be sure, regulation around AI is still a very gray area since the technology is so new and it’s constantly evolving. Banking regulators in particular have been looking closely at the issues pertaining to AI such as its possible applications, short-comings, challenges and supervision. Because the waters are so untested, there can be validity in asking for regulatory and compliance advice before moving ahead full steam, some industry watchers say.

Upstart, for example, which uses AI extensively to price credit and automate the borrowing process, wanted buy-in from the Consumer Financial Protection Bureau to help ease the concern of its backers as well as to satisfy its own concerns about the legality of its efforts. So the firm submitted a no-action request to CFPB. The CFPB responded by issuing a no-action letter to Upstart in September 2017, allowing the company to use its model. In return, Upstart shares certain information with the CFPB regarding the loan applications it receives, how it decides which loans to approve, and how it will mitigate risk to consumers, as well as information on how its model expands access to credit for traditionally underserved populations.

The No-Action Letter is in force for three years and Upstart can seek to renew it if it chooses.

Theoretically firms could have a computer underwriting model constantly updating itself without having a human oversee what the model is doing—but it’s a bad idea, industry participants say. “I believe there are companies doing that, and it’s a risky thing to do,” says Scott M. Pearson, a partner with the law firm Ballard Spahr LLP in Los Angeles.

During review of the models—and before implementing them—people should carefully review the models and the output to make sure there’s nothing that causes intrinsic bias, says Kathryn Petralia, co-founder and president of Kabbage, which is one of the front-runners in using machine learning models to understand and predict business performance.

“If you’re not watching the machine, you don’t know how the machine is complying with regulatory requirements,” she says.

Kabbage has teams of data scientists regularly developing models that the company then reviews internally before deploying. The company is also in frequent contact with regulators about its processes. Petralia says it’s very important that firms be able to explain to regulators how their models work. “Machines aren’t very good at explaining things,” she quips.

As a best practice, Pearson of Ballard Spahr says lenders and funders shouldn’t use any machine learning model until it’s been signed off on by compliance. “That strikes a pretty good balance between getting the benefits of AI and making sure it doesn’t create a compliance problem for you,” he says.

While AI has many benefits, industry participants say alternative lenders and funders need to be mindful of how it can be applied practically and effectively within their particular business model.

Craig Focardi, senior analyst with consulting firm Celent in San Francisco, contends that the classic FICO score continues to be the gold standard for credit decisions in the U.S. He warns firms not to get overly distracted trying to find the next best thing.

“Many fintech lenders have immature risk management and operations functions. They’re better off improving those than dabbling in alternative scoring,” he says, noting that data modeling is an entirely separate core competency.

Indeed, Lewis of Aquila cautions underwriters not to view AI as a silver bullet. “AI is just one tool out of many in the lenders’ toolbox, and our industry should use it and respect its limitations,” he says.

Did UCC Lead Generators Overload NY State’s System?

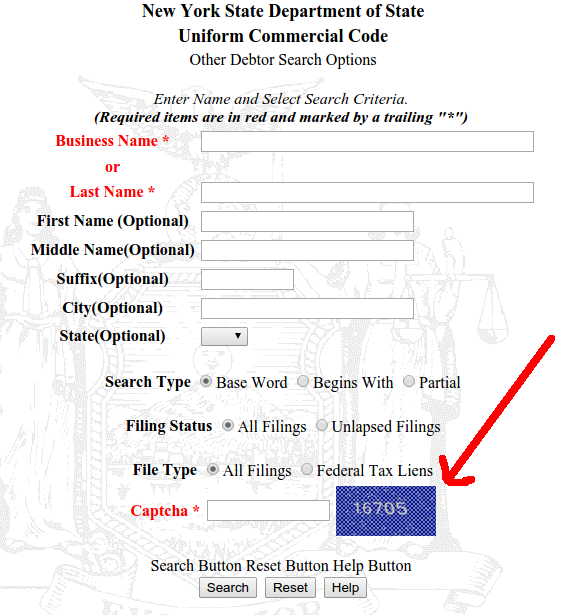

April 4, 2017 In the small business finance industry, New York State is known as one of the friendliest places to conduct a UCC search. You can not only search by debtor, but also by secured party, and get just about everything you need to create a list of prospects for free.

In the small business finance industry, New York State is known as one of the friendliest places to conduct a UCC search. You can not only search by debtor, but also by secured party, and get just about everything you need to create a list of prospects for free.

But the State’s website isn’t exactly a pillar of technological achievement. Indeed, the UCC Lien Search welcome page makes clear that searchers will need to be using Netscape Navigator 4.0 or higher and that version 3.0 of Internet Explorer or lower is not supported. Those browser iterations were released in 1997 and 1996 respectively, before some in the business finance industry were even born.

And the online system built for Windows 3.1 users didn’t seem to be doing so well over the last few months. Routine manual searches that I occasionally conduct were leading to error messages and crash pages instead of results. Were UCC lead generators querying the system to death?

Last week, New York took the entire UCC system down for “maintenance” and when it finally came back up, a tool to combat automated queries had been installed.

Curiously, this has only been implemented for secured party searches and other debtor search options. Standard debtor search options remains unchanged.

As Captchas are designed to thwart automated queries, could this be a sign that lead generators were crashing the system?

To check it out yourself, it’s best to be using Windows 95 or higher. Typewriters and Etch-A-Sketch users may experience performance issues.

OnDeck CEO Noah Breslow Talked Tech Worker Shortage in Canada on BloombergTV

March 22, 2017On BloobergTV Canada, OnDeck CEO Noah Breslow explained what he thought the country could do to boost innovation. The discussion stemmed from Canada’s decision to set aside C$800 million over the next four years to carry out that objective.

Breslow said that since Canada has excellent schools, those graduates can be nurtured into forming businesses and creating business investment opportunities. He also said that vocational training towards today’s new working-style job would be beneficial as well, whether it’s jobs for people who can design the latest algorithm or people who can build systems and data centers or can rack servers together.

When asked if perhaps government intervention was not the answer to achieve this, Breslow said that there are two ends of that spectrum, and where he believed intervention could be helpful was in the formation and talent development and formation incubation stage of companies. For later-stage companies, it was probably not appropriate, he said.

Breslow also expressed his belief that a permissive immigration policy is important and that there should be less friction to bring in skilled workers to Canada.

You can watch the full video below to hear the rest:

AI Sales Assistant Penetrating Alternative Finance Raises $34 Million in Series B Round

December 15, 2016 Wondering how your competition always seems to be so on top of their game? They might be using an artificially intelligent sales assistant. Such technology was reported on last month when deBanked learned that it had penetrated the alternative business financing industry through at least one company named AI Assist. AI Assist is powered by Conversica, a Foster City, CA-based technology firm that announced it had raised $34 million in a Series B round on Wednesday led by Providence Strategic Growth Capital Partners L.L.C. More than 1,000 companies across technology, automotive, higher education, finance, insurance, real estate and hospitality are using Conversica.

Wondering how your competition always seems to be so on top of their game? They might be using an artificially intelligent sales assistant. Such technology was reported on last month when deBanked learned that it had penetrated the alternative business financing industry through at least one company named AI Assist. AI Assist is powered by Conversica, a Foster City, CA-based technology firm that announced it had raised $34 million in a Series B round on Wednesday led by Providence Strategic Growth Capital Partners L.L.C. More than 1,000 companies across technology, automotive, higher education, finance, insurance, real estate and hospitality are using Conversica.

“Conversica’s AI technology has helped IBM be smarter about engaging our prospective customers and maximizing their value as they move through our sales funnel,” Kevin Pollack, head of IBM’s Global Email Marketing Practice, is quoted as saying in a press release. “Not only have we freed up resources within the marketing team and gained immediate value in the form of qualified sales opportunities, we are also seeing how AI can help transform our entire business moving forward.”

For Roman Vinfield, who launched a merchant cash advance ISO in 2015, it changed his life. “I hadn’t heard anything like an artificial-intelligence sales assistant,” said Vinfield. “The results we got within a month of using it were unbelievable.” Within the first month, Vinfield made $35,000 in revenues by spending just $4,000 and he eventually reduced his staff of 24 to 4 people. He’s since launched AI Assist, the exclusive reseller of Conversica to the alternative finance industry.

“We’ve gone way beyond the theoretical,” Conversica CEO Alex Terry told Fortune. A demo given by Vinfield of AI Assist, demonstrated that its artificial intelligence can communicate with merchants over emails in a way that is indistinguishable from a human. According to Fortune, Terry said the sales assistant software has proven so effective for some customers that recruiters have even mistaken the software for a human and tried to make a hire. Other contacts have sent in thank-you notes and flowers, he added.

Conversica has raised more than $56 million since inception. Providence, who led the Series B round, also owns stakes in Hulu and the Yankees Entertainment & Sports Network (YES Network). Conversica’s technology is only available to this industry via AI Assist.

Google To Shut Down Financial Products Comparison Site

February 23, 2016 Another Google product bites the dust.

Another Google product bites the dust.

The tech giant plans to shut down Google Compare on March 23rd 2016, a tool which let users compare financial products like credit cards, mortgages and insurance.

The service which has been active in the UK since 2012, was launched in the US as Google Advisor last year and allowed customers to get quotes on financial products. Despite having launched with partners like Zillow and Lending Tree for mortgage products, the service didn’t do much for the company in terms of revenue.

In its letter to partners, the company noted, “Despite people turning to Google for financial services information, the Google Compare service itself hasn’t driven the success we hoped for.”

Exponential Finance

June 15, 2014 Last week, DailyFunder was a media sponsor of Exponential Finance presented by Singularity University & CNBC. It was a totally different atmosphere from some of the other events I’ve been to this year already (Transact 14, LendIt, etc.). In the upcoming July/August issue of DailyFunder magazine, I’ve got a column that summarizes the event that I think you’ll like.

Last week, DailyFunder was a media sponsor of Exponential Finance presented by Singularity University & CNBC. It was a totally different atmosphere from some of the other events I’ve been to this year already (Transact 14, LendIt, etc.). In the upcoming July/August issue of DailyFunder magazine, I’ve got a column that summarizes the event that I think you’ll like.

Exponential Finance brought together leading experts to inform financial services leaders how technologies such as artificial intelligence, quantum computing, crowdfunding, digital currencies, and robotics are impacting business. And my mind = blown.

Some tweets to hold you over:

Robots may be coming to a bank near you: http://t.co/r0PlWUrYqU #xfinance pic.twitter.com/WYWUhZIUaD

— CNBC Social Team (@CNBCSocial) June 10, 2014

"The more data you produce, the more organized crime will consume." Goodman’s Law. #xfinance Be prepared!

— Exponential Finance (@xfinance) June 11, 2014

"Banks charge 32B in overdraft every year…that's almost as much as the gov. spends on food stamps." – Customers Bancorp CEO at #xfinance

— CNBC Social Team (@CNBCSocial) June 11, 2014

"It is no coincidence that Satoshi Nakamoto published this paper [on Bitcoin] during the financial crisis." #xfinance pic.twitter.com/a9eCWO7OXi

— CNBC Social Team (@CNBCSocial) June 11, 2014

Robots are going to steal your finance job:

I also had the chance to do a Q&A with a longtime prominent U.S. Congressman. The next issue should be available in about 3 weeks.

Fund it and Ask Questions Later

March 25, 2014 Ever since OnDeck Capital stopped doing verbal landlord references, the underwriting landscape of alternative lending has changed dramatically. Kabbage will supposedly fund applicants in just 7 minutes. Everybody’s under the gun to streamline their process, fund deals faster, and produce record breaking numbers month after month.

Ever since OnDeck Capital stopped doing verbal landlord references, the underwriting landscape of alternative lending has changed dramatically. Kabbage will supposedly fund applicants in just 7 minutes. Everybody’s under the gun to streamline their process, fund deals faster, and produce record breaking numbers month after month.

And why shouldn’t they? Investors are practically foaming at the mouth to get in on any and all kinds of alternative lending. Even Lending Club has thrown in the towel by no longer allowing investors to ask applicants questions. Prior to March 19th, applicants on Lending Club’s platform had the option to answer standardized questions about themselves and their purpose for seeking out a loan. This was set up to help investors feel more informed and comfortable. Once the loan was posted, prospective investors could ask the applicant additional questions of their own to help them decide if it was a deal they wanted to participate in. For example, “what are the interest rates on the credit cards you claim you want to consolidate?” That’s a fair question to ask someone seeking a debt consolidation loan.

Lending Club did away with the Q&A in the name of privacy but conceded in their blog that people are funding deals so fast that no one cares what applicants have to say.

We know that in the past some investors enjoyed reading these descriptions and answers, but as the platform has grown, fewer and fewer investors are using this approach to inform their decisions. Fewer than 3% of investors currently ask questions and only 13% of posted loans have answers provided by borrowers. Furthermore, loans are currently funding in as little as a few hours – well before borrower answers and descriptions can be reviewed and posted.

Loans are being fully funded by institutional investors and mom & pop investors before the applicant can even finish filling out the questionnaire.

The demand to invest outpaces the amount of loans that Lending Club can originate. In a call I had with Lending Club today as a potential investor, I was told that businesses were not even allowed to invest on their platform at this time because they’ll take up all the loans and leave nothing for the average mom & pop investors, the ones which have made their peer-to-peer fame possible.

The demand to invest outpaces the amount of loans that Lending Club can originate. In a call I had with Lending Club today as a potential investor, I was told that businesses were not even allowed to invest on their platform at this time because they’ll take up all the loans and leave nothing for the average mom & pop investors, the ones which have made their peer-to-peer fame possible.

In the Lend Academy blog forum, mom & pop investors debated the usefulness of the Q&A system. Some argued that responses from applicants allowed them to weed out folks with poor spelling and grammar. Others believed that a poorly worded response was better than someone who didn’t respond at all because it showed that they actually cared about the loan they were applying for.

There were folks that analyzed the applicants language on a scientific level, with one going so far as to cite this study: Peer-to-Peer Lending The Relationship Between Language Features, Trustworthiness, and Persuasion Success.

I am reminded of my underwriting days conducting merchant interviews prior to a final decision. There were applicants that looked good on paper that came across as completely clueless about their business over the phone. Like beyond clueless. And then there were applicants that looked ugly on paper that really impressed me with their command of business subject matter. What shocked me were the former and it’s a testament to how tricky business lending is. Those phone calls impacted my final decision all the time.

But in today’s world where funders are dealing in kilos of cash instead of nickels and dimes, there’s a growing impatience over non-automated things like interacting with the applicant. Fund the deal and ask questions later!

The vast majority of merchant cash advance companies still conduct applicant phone interviews and there’s a part of me that hopes that never changes. As investors grow restless for new pools of loans or advances to participate in, I fear there will be more underwriting sacrifices to satisfy that demand.

The vast majority of merchant cash advance companies still conduct applicant phone interviews and there’s a part of me that hopes that never changes. As investors grow restless for new pools of loans or advances to participate in, I fear there will be more underwriting sacrifices to satisfy that demand.

It was only a year ago that I laughed at my friend in commercial banking when he told me a small business loan application begins with lunch and a few rounds of golf. “It’s about relationships,” he said. That couldn’t be less true in peer-to-peer lending where the goal is to know as little as possible about where the money is going. I see that mentality creeping into merchant cash advance as well. Sure, there are folks that point to thousands of data points aggregated through online sources but it only takes a 5 minute phone call to determine that an applicant is completely full of crap.

Maybe Jeremy Brown of RapidAdvance was on to something. When Will the Bubble Burst?

Join the discussion about this on DailyFunder.