p2p lending

Lending Club Originated $3.3B in Loans in Q3

November 5, 2019 Lending Club originated $3.3B in loans in q3 and reported a minor net loss of $400,000. That loss was a $22.4M improvement over the same period last year, mainly due to an increase in “net revenue” and a decrease in class action and regulatory litigation expense. One of those class action lawsuits against them was dismissed on October 31.

Lending Club originated $3.3B in loans in q3 and reported a minor net loss of $400,000. That loss was a $22.4M improvement over the same period last year, mainly due to an increase in “net revenue” and a decrease in class action and regulatory litigation expense. One of those class action lawsuits against them was dismissed on October 31.

Lending Club is the number one provider of personal loans in the country and is continuing to grow their marketshare, CEO Scott Sanborn said during the earnings call. One analyst asked if their continued lead on that could be due to the market’s declining emphasis on growth as a performance metric. Sanborn responded by saying that the competition had not let up at all on marketing and that direct mail marketing and competition is still at operating at an extremely high level.

How Linked Finance is Linking Irish SMEs With Quick Loans

October 1, 2019 Google Maps was convinced that I was already at my destination, but that didn’t make sense because I was still sitting in my cramped Airbnb rental apartment in Dublin and hadn’t left to go anywhere yet. “Oh man please tell me Google works in Ireland,” I said to myself while glancing at the time and counting how many minutes I’d be late to my first meeting.

Google Maps was convinced that I was already at my destination, but that didn’t make sense because I was still sitting in my cramped Airbnb rental apartment in Dublin and hadn’t left to go anywhere yet. “Oh man please tell me Google works in Ireland,” I said to myself while glancing at the time and counting how many minutes I’d be late to my first meeting.

I was on my way to Linked Finance, a peer-to-peer SME lender based in Dublin. Their office was uncannily close to where I was staying on Liffey Street Lower, just steps away from the Ha’penny Bridge. So close in fact, that Google Maps believed that I was going to and from the same location. I breathed a sigh of relief at the realization and ventured the short distance to the elevator that promised to deliver me to the inner universe of Irish fintech.

Alan Fagan, the company’s head of marketing, greeted me at the door. Fagan joined the company in 2015, two years after its founding. As we walk in, I notice the prominent display of the Linked Finance logo amid an ocean of eye-popping orange. The look, the feel, suddenly I feel transported to the tech scene in San Francisco. The accents overheard in the background, however, suggest I am most definitely in Ireland.

Alan Fagan, the company’s head of marketing, greeted me at the door. Fagan joined the company in 2015, two years after its founding. As we walk in, I notice the prominent display of the Linked Finance logo amid an ocean of eye-popping orange. The look, the feel, suddenly I feel transported to the tech scene in San Francisco. The accents overheard in the background, however, suggest I am most definitely in Ireland.

We sit down. Tea is offered. I decline. Fagan gets right into it and he sings a familiar song, that it can take a very long time for a business to get a bank loan.

It can take up 8 weeks to get funded, he says. “SMEs are the biggest employer in the country,” he explains, while hinting that facilitating loans to this demographic is as much a patriotic endeavor as it is a business one.

The nation’s Central Statistics Office puts the number of active enterprises in the private business economy at over 250,000. As of June, Linked Finance had made more than 2,100 loans for a grand total of more than €100 million.

Fagan gives me a demonstration of the platform, where individual investors (or peers) can see the name and location of the businesses whose loans are available to fund. An investor can even sort the listings by county, of which there are 26 in the Republic. Linked Finance does the underwriting, something they can do within 1 day, Fagan says.

The underwriting is tight. “We’re not a lender of last resort,” Fagan explains. They put themselves on the same (or better) credit risk footing as banks and claim that they’re able to assess risk and provide funds in a much more efficient manner. “We feel we do it better than banks,” Fagan says.

Most loans close quickly, thanks in part to their Autobid tool. Investors can be from anywhere so long as they’re over 18 and have a European Union bank account. Annual interest rates on the loans range from 6% to 17.5%.

Fagan says that although they are an online lender, many borrowers in Ireland still appreciate personal relationships. They can accommodate applicants that prefer a personal walk-through by a real person and that it can actually leave a memorable impression on their customers.

Marketing is done via a variety of direct methods but also through channel partners like accountants and financial advisors. A big name asset manager, Paris-based Eiffel Investment Group, with €1.5B under management, is among the loan investors on the Linked Finance platform.

I keep waiting for the caveat, an obstacle or twist in the model so inherently Irish, that somebody like me from half a world away would never truly grasp. But there isn’t one. The market is overtly familiar, yet more reminiscent of the UK than the States. Ireland lacks the robust regulatory framework of both countries, however. Despite that, the government does not appear to be holding the industry back. In June, Paschal Donohoe, the Minister for Finance, the government official responsible for all financial and monetary matters of the state, said “availability of credit is a key consideration for all businesses, and I am aware of the role peer to peer lending is playing in broadening competition in the SME finance market.”

Indeed, such competition has made credit more available in markets abroad.

As our time together winds down, I mindlessly attempt to plot my trip back. “Siri, take me home,” I speak into my phone. The Maps app opens and then loads to reveal a double entendre. It seems I am already very much there.

Could Peer-to-Peer Lending Be Resurrected By Falling Interest Rates? At Least For Now?

September 19, 2019 As interest rates rose and yields for investors at peer-to-peer (p2p) lenders collapsed, the allure of p2p lending, at least from my perspective, was gone.

As interest rates rose and yields for investors at peer-to-peer (p2p) lenders collapsed, the allure of p2p lending, at least from my perspective, was gone.

Rates on FDIC-insured CDs hit 2.5% while annual returns at some popular p2p lenders had declined to less than 5%. That’s a very narrow spread between an investment that has no risk of loss versus one that has a risk of losing everything, is rather unpredictable, and is marred by a history of misleading investors and overstating returns.

I compared the options and made the obvious decision and started withdrawing my personally invested funds out of p2p lenders 3 years ago in favor of more traditional investments like stock index funds.

But now interest rates are falling and it’s possible that retail investors once wooed by modestly generous savings account rates could begin to consider alternative options to generate returns. Enter P2P lending, again.

At Lending Club, the percentage of individual investors has trended downward consistently. In Q1 2015 these investors accounted for 19% of all platform originations with a total of $308 million. In the most recent quarter, that group has shrunk down to 5% of originations and only $155 million.

But at StreetShares, an online small business lender that offers individual retail investors a fixed 5% annualized return, the trend is the opposite. In a recent statement the company filed with the SEC, they claimed they had actually shifted away from funds from institutional capital providers and towards funds from retail investors. It doesn’t get into the specifics about why that is but it’s certainly unusual. StreetShares’ investment offering carries a total risk of loss much like other p2p lenders.

But interest rates aren’t supposed to fall in a void where nothing else in the outside world is happening. Assuming the economy is cooling, or worse, eventually heading towards a recession, the somewhat attractive looking p2p loan yields will fall as well since defaults on the underlying loans will rise.

So what does this mean? It means that online lenders, to the extent they’re still interested, have a potentially short window to entice retail investors back. To do so, they’ll have to convince the world that past transgressions are behind them and that low savings account rates can be supplanted by people helping their peers in return for a slightly better yield. That’s how the entire concept took off to begin with. I say the window is short because once we’re actually in a recession, it will become incredibly hard to convince fearful investors to participate in making risky online loans especially if the average returns drop into the negative. Don’t be surprised when that happens.

Peer-to-Peer Lending’s Global Struggle

July 8, 2019New rules were introduced to peer-to-peer lending in Britain this month with the introduction of Policy Statement 19/14 by the government. The document heralds in a number of new processes that will be required to be enacted by peer-to-peer lending platforms in the UK by early December this year, if they are to continue operating unmolested.

Among these rules is the expectation for stricter transparency and honesty between platforms and potential investors, specifically with regard to the practice of using borrowers’, investors’, and even the business’s own money to pay for defaulted loans. As well as this there is the introduction of appropriateness tests to ensure that those who are candidates to become investors understand the various risks of the industry they are prospecting.

Such tests aren’t new to the alternative finance industry, as they have been previously employed for both crowd bonds and equity crowdfunding. But that doesn’t mean that they will comfortably slide into use among peer-to-peer lending processes. The question about when they will be asked to complete the test during the application, be it at the beginning, upon completion of the first form, or after receiving confirmation of a loan, remains unanswered; there are concerns that lending platforms will take a ‘tick all boxes’ approach and pose unsatisfactory questions; and the fear that only larger firms will be able to afford the costs to install these compliance checks, thus edging out smaller peer-to-peer lending companies from the market, is common.

The publication of the document comes after years of success for peer-to-peer lending within the British market. With the previous 12 months showcasing £6.7 billion in peer-to-peer loans being taken out, more than any other European country, the market initially appears to be doing well, but stories about firms collapsing or exiting from the industry indicate otherwise. For example, Lendy, one of the first and largest peer-to-peer platforms in the UK collapsed and left 20,000 investors uncertain about the £160 million that was outstanding in loans; while BondMason withdrew completely from the market, pivoting into alternative property investment services.

The publication of the document comes after years of success for peer-to-peer lending within the British market. With the previous 12 months showcasing £6.7 billion in peer-to-peer loans being taken out, more than any other European country, the market initially appears to be doing well, but stories about firms collapsing or exiting from the industry indicate otherwise. For example, Lendy, one of the first and largest peer-to-peer platforms in the UK collapsed and left 20,000 investors uncertain about the £160 million that was outstanding in loans; while BondMason withdrew completely from the market, pivoting into alternative property investment services.

Looking forward, it appears as if lending platforms in the UK may become less reliant on retail investors and seek out more institutional investors who better understand the risks of peer-to-peer lending.

Peer-to-peer lending has gone through it own iterations in the US, with two platforms still thought of as peer-to-peer (but perhaps are no longer!) recently squaring off with the SEC. Last year, two former executives of Lending Club agreed to settle charges with the SEC for improperly adjusting returns of a related fund and this past April, Prosper Funding LLC agreed to pay a $3 million penalty for miscalculating and materially overstating annualized net returns to retail and other investors.

It could be worse.

China is currently watching its own peer-to-peer lending market collapse, despite the industry previously having drawn 50 million investors. With estimates claiming that half of the market was wiped out in 2018, and forecasts saying that 70% of those that survived will be gone by year end, China is on track to lose 85% of its peer-to-peer platforms within 24 months. This follows a number of cases of executives of Chinese peer-to-peer lending firms embezzling money and fleeing, leading to stories like the 31-year-old woman who hung herself when faced with the reality of losing $40,000 after a shareholder of PPMiao, a state-backed peer-to-peer platform, ran off when the firm went bust, reneging on any accountability.

“It’s amazing how quickly it’s unraveling,” said Zennon Kapron, the managing director of Shanghai-based consulting firm Kapronasia, about the peer-to-peer industry. And while Kapron was speaking about the Chinese market, governments worldwide have shifted from nurturing peer-to-peer lenders to policing them and diligently trying to rein them in.

SEC Finding Said that Prosper Misled Investors

April 22, 2019 From approximately July 2015 until May 2017, Prosper excluded certain non-performing loans from its calculation of annualized net returns that it reported to its investors, according to an SEC order released last Friday. The order found that Prosper reported overstated annualized net returns to more than 30,000 investors on individual account pages on Prosper’s website and in emails soliciting additional investments from investors.

From approximately July 2015 until May 2017, Prosper excluded certain non-performing loans from its calculation of annualized net returns that it reported to its investors, according to an SEC order released last Friday. The order found that Prosper reported overstated annualized net returns to more than 30,000 investors on individual account pages on Prosper’s website and in emails soliciting additional investments from investors.

As a result of the inflated numbered, which the SEC order says Prosper management was aware of, many investors decided to make additional investments based on the overstated annualized net returns. The SEC order said that Prosper failed to identify and correct the error that overstated its annualized net returns “despite Prosper’s knowledge that it no longer understood how annualized net returns were calculated and despite investor complaints about the calculation.”

“For almost two years, Prosper told tens of thousands of investors that their returns were higher than they actually were despite warning signs that should have alerted Prosper that it was miscalculating those returns,” said Daniel Michael, Chief of the SEC Enforcement Division’s Complex Financial Instruments Unit.

Prosper neither admitted nor denied the findings. The company did not refute the SEC order’s findings, including that it violated the antifraud provision contained in Section 17(a)(2) of the Securities Act of 1933. Prosper will pay a $3 million penalty for miscalculating and overstating annualized net returns to retail and other investors.

According to a 2017 Financial Times story, one Prosper investor wrote on the Lend Academy forum in 2017 that their returns were restated from about 14 percent to 7 percent.

“Shame on me for just assuming that I was getting a higher rate,” the investor wrote, “but shame on Prosper x 1000 for misleading investors.”

In a written statement to deBanked today, a Prosper representative characterized the miscalculation as an error only, not a scheme. She conveyed that when Prosper discovered the error in 2017, they notified investors who were impacted and changed the numbers so that they accurately reflected the investors’ returns.

“We’re pleased to have the SEC inquiry resolved and appreciate the SEC’s recognition of our cooperation as the agency looked into this matter,” read a statement provided by Prosper. “Since discovering and fixing this issue two years ago, we have put additional controls in place designed to detect and prevent similar errors in the future, and we are committed to providing transparent information on returns to our retail investors.”

Prosper’s CEO, David Kimball, was awarded “Executive of the Year” at this year’s LendIt Fintech conference earlier this month.

In 2018, the company originated $2.8 billion in loans, remaining flat compared to 2017. Prosper’s net revenue last year was $104 million, a decrease compared to $116 million in 2017. Founded in 2005 and headquartered in San Francisco, Prosper provides personal loans up to $40,000 and was one of the first peer to peer lenders.

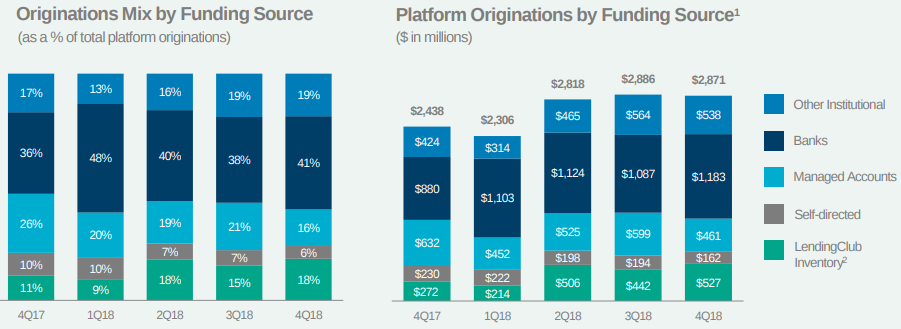

‘Peers’ Are Almost Gone From Lending Club’s Funding Mix

February 20, 2019 Long gone are the days of peer-to-peer lending.

Long gone are the days of peer-to-peer lending.

On Tuesday, Lending Club, a pioneer in the peer-to-peer lending space, reported that only 6% of its Q4 originations came from individual self-managed accounts. Accounts professionally managed for individuals made up 16%, with the rest of the loans being funded by a combination of banks, institutions, and Lending Club itself.

Nearly 4 years ago, the ratio was flipped. Self-managed accounts made up 24% of originations in early 2015 and accounts professionally managed for individuals made up 51%.

Despite the changes, Lending Club still identified itself as a “marketplace connecting borrowers and investors” in its Q4 2018 earnings report. A review of the site revealed that it is still possible for individual investors to manually review unfunded loans on the platform and invest in them, though it prods investors to rely on Lending Club’s automated investing strategy instead. The implication for manual investors is obvious, that banks, institutions, automated investment algorithms, and Lending Club itself are more likely to fully fund the best borrowers before the individual has a chance to even see them on the platform.

According to the blog of LendItFintech co-founder Peter Renton, Lending Club is producing among the lowest returns of any platform in the field, with his own accounts generating from 1.57% a year to 4.35% a year.

Why is P2P Lending Unraveling in China?

August 14, 2018 Back in 2014, peer to peer (P2P) lending in China was all the rage. Multiple P2P platforms were launching daily, with investors and borrowers were eager to participate. According to South China Morning Post, the P2P lending frenzy hit its peak in 2015 when about 3,500 P2P businesses were operating.

Back in 2014, peer to peer (P2P) lending in China was all the rage. Multiple P2P platforms were launching daily, with investors and borrowers were eager to participate. According to South China Morning Post, the P2P lending frenzy hit its peak in 2015 when about 3,500 P2P businesses were operating.

Now, these same businesses are collapsing at nearly the same speed with which they sprung up. According to South China Morning Post, in conjunction with Reuters, 243 online lending platforms have gone out of business since June. And Chinese investors who can’t get their money out of the companies have taken to the streets. (Although, like with most protests in the country, the government has successfully quashed any sizable demonstration.)

“The trouble is that everything is coming to head this summer and millions of investors are trying to get their money out at the same time,” said Peter Renton, co-founder of the LendIt Fintech, which organizes several international events including an annual conference in China for fintech and online lending.

“Most people think that even with a big market [like China], it can only sustain a few hundred platforms at most,” he told deBanked.

“Most people think that even with a big market [like China], it can only sustain a few hundred platforms at most,” he told deBanked.

Renton said that this implosion is largely the result of lax Chinese regulation for a number of years. But the Chinese government is now making up for it. In November 2017, China’s central bank said that no new licenses would be issued to online lending platforms. And with Chinese P2P platforms failing daily this summer, the central government has proposed new measures, according to Xinhua, the official government news agency. These proposed measures include setting up “communications windows” to respond to requests by P2P investors, as well as conducting compliance inspections on P2P companies and putting on a blacklist in China’s social credit ratings system any online borrower who tries to avoid P2P loan repayments.

The continuing collapse of P2P lending platforms in China is particularly notable because it affects so many people. According to data used by Reuters, the size of China’s P2P industry is significantly bigger than the rest of the world combined, with outstanding loans of 1.49 trillion yuan, or $217.96 billion.

“We all knew the party was going to end at some point and it looks like 2018 will be the year of reckoning,” Renton wrote in a July 30 story.

Yet in a video aimed at Chinese viewers released at the same time, he said: “I think in a couple years time, when we look back at this year, we’ll see that this was necessary — painful but necessary. The industry is going to come out the other side. The strong platforms are going to survive, the weak ones are not. And I think the industry will be far better off once this all plays out.”

Lending Club Hits Record for Originations

August 7, 2018 In the second quarter of 2018, Lending Club originated a record high of $2.8 billion, up 31% from the same time last year. Net revenue also hit a record high of $177 million, up 27% year-over-year.

In the second quarter of 2018, Lending Club originated a record high of $2.8 billion, up 31% from the same time last year. Net revenue also hit a record high of $177 million, up 27% year-over-year.

During today’s earning call, Lending Club CEO Scott Sanborn said that the company completed a successful securitization this quarter and Lending Club CFO Tom Casey said that that they expect several more by the end of the year. Both acknowledged that the company is still spending millions of dollars to resolve regulatory issues, but Sanborn said he expects that to come to a close by the end of the year. With regard to the record high in originations, Casey said that the company also had a higher percentage of A and B grade loans in the second quarter.

Lending Club offers fixed rate business loans from $5,000 to $300,000 and personal loans of up to $40,000. The company also offers auto refinancing.

Founded in 2007, Lending Club was one of the first major peer-to-peer lenders. The company facilitates loans between individual borrowers and individual or institutional investors. Traditionally, individual investors in companies must be accredited investors. This means that the U.S. Securities and Exchange Commission requires the accredited investor to have a net worth of at least $1 million, excluding the value of one’s primary residence, or they must have income of at least $200,000 each year for the last two years, or $300,000 combined income if married.

Lending Club investors must also satisfy certain lesser financial requirements. In most states, excluding California, Lending Club investors must have an annual gross income of at least $70,000 and a net worth of at least $70,000 (excluding value of home, home furnishings, and automobile) or they must have a net worth of at least $250,000. (California requires the an investor’s annual gross income be $85,000).

Since investors are not accredited, every Lending Club loan, many of them to individuals, must be filed with the SEC so that investing in a Lending Club loan is like buying stock in a publicly traded company. Investors can buy fractions of loans in the form of notes as small as $25.

Lending Club is headquartered in San Francisco and went public on the New York Stock Exchange in 2014.