Online Lending

The Fintech Legal Outlook for 2020: Top 3 Insights from Todd Hamblet

February 18, 2020 We recently sat down with Todd Hamblet, Fundbox’s new Chief Legal Officer, and asked his thoughts about what legislative or legal issues would be shaping the fintech industry this year. Between presidents and precedents, decisions are coming down within the next 12 months that will have a significant effect on the way Fundbox and other fintechs do business. Here’s what Todd had to say:

We recently sat down with Todd Hamblet, Fundbox’s new Chief Legal Officer, and asked his thoughts about what legislative or legal issues would be shaping the fintech industry this year. Between presidents and precedents, decisions are coming down within the next 12 months that will have a significant effect on the way Fundbox and other fintechs do business. Here’s what Todd had to say:

Q: What key issues or predictions do you see when it comes to legal compliance in the fintech industry in 2020?

A: My basic view is that I expect to see continued efforts to regulate the financial services industry and fintech. These regulations are likely to focus on protection of consumer and commercial borrowers, privacy, or data protection. That said, I don’t think that innovation and regulation are incompatible. I think that there is sensible regulation that can achieve the goals of protecting consumers of financial services without completely stifling fintech innovation.

I think the outcome of the election will have a significant bearing on how active regulators are in the fintech space. In the absence of leadership from Washington, I’m concerned that we’re going to continue to see state-by-state legislation instead of a federal overlay. California and New York are two states actively working to fill this void. State versus federal regulation creates the challenge of needing to comply with 50 state requirements, which sometimes might be at odds with each other, as opposed to a more unified regulatory regime. You just have to spend a lot of resources in researching, staying up to date, and modifying what in many cases is a fairly streamlined product offering to comply with different state laws.

I worry that too disparate of a regulatory regime can, in fact, stifle innovation. It won’t stop innovation, but it can make it more challenging. I am certainly not opposed to sensible regulation, but sometimes the best intentions can lead to anomalous outcomes. You always have good actors and bad actors, and in our space, for example, we’re trying to disrupt a very traditional way of underwriting and lending in a commercial space that just hasn’t been compatible with or user friendly for small businesses.

The small business community is under-served, in part because you’re talking about smaller dollars than your traditional banks are even willing to underwrite. You’ve started to see community banks and credit unions step in a bit, but even in those cases, the lending model is still paper-heavy. It’s not optimized for all the data that’s out there, the ability to use technology, or alternative data sources. I think that fintech companies like Fundbox are serving and filling a niche that is really valuable for small businesses. Think about a mom-and-pop shop. They need to be able to run their business. They don’t need to spend all their time going back and forth with their bank, trying to get a loan. They need quick access to capital that may be just to solve a short-term problem. It may be to meet payroll during a slow month. That’s the problem we’re trying to solve, and also doing it in a way that is bringing it into the 21st century. This means using alternative data sources and machine learning, not relying exclusively on credit reports or FICO scores, and using other metrics to look at the credit worthiness of an enterprise.

I find it really exciting. It’s really satisfying to know that we’ve helped a lot of small businesses at the heart of our economy. So I think additional regulation is inevitable, but I hope it’s reasonable and sensible, and that it serves the purpose of protecting the borrower but doesn’t impose so many requirements or obligations that it makes it impractical for a fintech company to try to serve that population.

Q: Is there anything else you see happening in the realm of compliance?

A: I think we’re going to continue to face additional regulation in the areas of privacy and data protection. In California, we have the California Consumer Privacy Act (CCPA) that came online on January 1st. This is a good example of how, in the absence of federal action, states are going to take up their own legislation. California is the first to have enacted a comprehensive privacy act that companies are now trying to deal with. It impacts not just California companies but any companies dealing with California residents.

We’re tracking legislative developments in other states who are looking to implement their own privacy acts. Absent some sort of harmonized federal overlay (such as the GDPR in Europe), if you have 50 states with disparate privacy regulations, it just becomes very challenging. Of course, we will do everything we can to be compliant, but we have limited resources—we’d love to dedicate our resources to developing and improving products for our customers, instead of worrying about whether we’re tripping up a novel requirement of a particular state’s privacy law. So a federal framework would be really helpful. I already mentioned regulation in the context of the next election, and I think whether there is interest in Washington with a federal privacy law will depend on that outcome.

Q: Aside from the 2020 election, what other issues is the fintech industry keeping an eye on?

A: There have been some interesting cases out there in the fintech space. There’s one case in particular that has created some uncertainty and confusion: the Madden case. Although the case was decided a few years ago, it looks like federal regulators are trying to take steps to clarify the ruling. I hope that 2020 brings better visibility into what’s going to happen there, since the uncertainty is impacting the financial services industry and fintechs.

Generally, Madden is a case that dealt with the “valid when made” concept. When a bank makes a loan, there are various usury laws that can be applicable, depending on the state in which the loan was originated. Under federal law, an FDIC-insured state chartered bank can originate a loan using the maximum rate of interest permitted in the home state of the bank and then “export” that rate into another state, regardless of the state where the borrower is located. Some states have higher usury rates than others, so the maximum rate can vary. It is well settled that when that loan was initially made by the bank, it was “valid when made.” But what happens if that bank decides to sell off that loan to a third party in another state? The Madden case (read broadly) calls into question the “valid when made” doctrine. It said that if the loan had an X percent interest rate when it was originated, but it was sold to a third party in a state that had a usury rate lower than X, that original interest rate may not be valid anymore because of the transfer. Studies have shown that this ruling has led to a decrease in the availability of credit in the states affected by the decision.

Banks have to rely on being able to originate and sell loans—this is a well-settled concept. The question is whether the Madden case is distinguishable enough from the traditional practice that it applies only to a particular scenario (a sale of debt) or whether it is calling into question the broader concept. The reason this impacts fintechs is because a lot of us rely on bank partnerships in order to serve customers in all 50 states. Through these partnerships, fintechs may acquire the receivables on loans originated by partner banks. The question for fintechs in the context of Madden is: when the fintech acquires a receivable, does the interest rate originally offered by the bank partner continue to be valid…or because the fintech is a third party, does some other interest rate cap apply depending on where the borrower is located?

Congress and some other federal regulators are working to clarify that the Madden case should be limited to a narrow set of facts, and that it should not serve as a precedent for disrupting the traditional understanding of “valid when made”. This would be welcome relief to the entire financial services industry, including fintechs. We hope to have this clarification in 2020.

Loan Brokers Attack Online Direct Lending in Super Bowl Commercial Duel

February 2, 2020

The battle is on between lenders and brokers in the mortgage space as middlemen try to out-compete push-button loan technology.

Quicken Loans ran a Super Bowl Commercial that featured Game of Thrones Actor Jason Momoa aka Khal Drogo and its Rocket Mortgage product. The theme, that of being super comfortable in your home, is a complete 180 from the controversial route the company took during a previous year’s Super Bowl that prompted a negative response from regulators and viewers. Even if you’re not in the market for a mortgage, Momoa revealing “his true self” is pretty humorous.

But not everyone is a fan of what online direct lenders are selling. FindAMortgageBroker.com criticized “playing with rockets” when it comes to mortgages and advocated working with an independent local mortgage broker instead. Why work with a broker they say? Because brokers work with various lenders instead of just one. The company goes as far as saying that brokers are faster, easier, and more affordable and they sign off with the hashtag, #brokersarebetter.

Check it out…

Report Finds Canadian Alternative Lending Market Making Gains

January 8, 2020 A study released by Smarter Loans this week indicates that the Canadian alternative finance industry has grown since last year’s iteration of the report. Titled ‘The State of Alternative Lending in Canada 2019,’ the report highlights how the market has developed in regard to the age and gender of its customers, the level of trust in online lenders compared to financial institutions, as well as the levels of satisfaction felt by Canadians dealing with alternative funders.

A study released by Smarter Loans this week indicates that the Canadian alternative finance industry has grown since last year’s iteration of the report. Titled ‘The State of Alternative Lending in Canada 2019,’ the report highlights how the market has developed in regard to the age and gender of its customers, the level of trust in online lenders compared to financial institutions, as well as the levels of satisfaction felt by Canadians dealing with alternative funders.

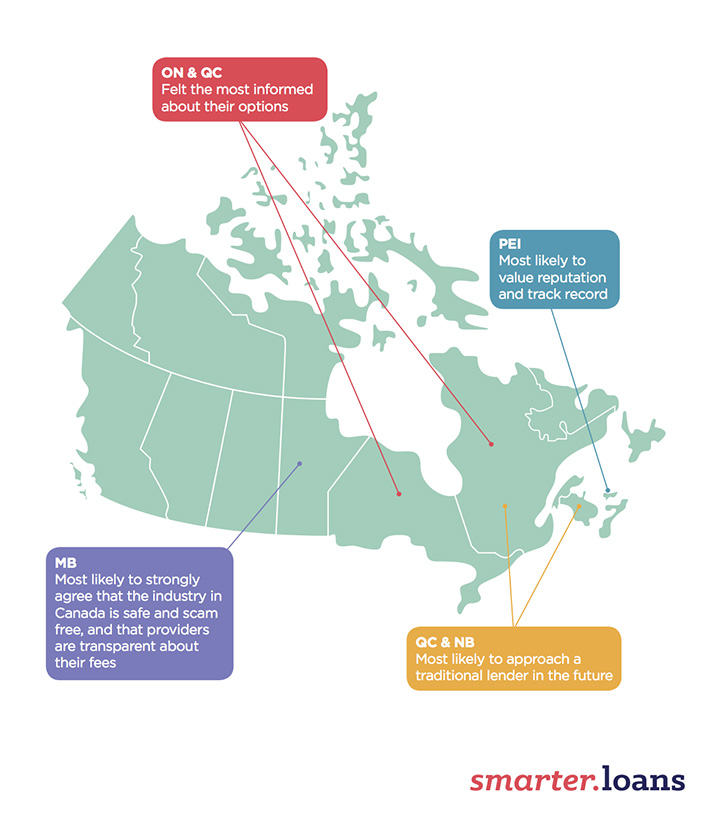

The first of these, regarding aspects of the customers’ identities, demonstrates that generational gaps are as wide as they’ve ever been amongst customers. Each age bracket questioned by the study showed differing priorities when seeking a loan. Generation Z, fitting in between those aged 18-24, paid attention to funders’ track records and reputation when looking for funding; whereas millennials (25-34) sought speedier applications and approvals. Generation X (45-54) however appeared more money-minded, with the priority being placed on terms and interest rates; and Baby Boomers (55-64) demonstrated a desire for having someone to talk to, putting customer service at the top of their list.

Vlad Sherbatov, Smarter Loans’ President and Co-founder, told deBanked that these differences can be summed up as the values each generation has developed through experience. Explaining that Gen Z is “all about the personal brand,” Sherbatov said, “People that are younger now really associate with the company they work for, they ask, ‘Am I aligned with or would I be embarrassed supporting this brand?’” While the Millennials’ response indicates a greater desire for results, “as the age progress the intent increases.” Gen X is “more educated and experienced people,” who appear to place the greatest importance on money; and Baby Boomers, the least digitally fluent group, just want the online applications to go smoothly and to have ready access to assistance.

As well as age, gender appeared to divide customers, with women more likely to spend more time researching loan providers than men; and more men saying that they were interested in approaching a traditional financial institution for a loan in the future, with half of them being of this opinion compared to just 39% of women. As well as this, it was found that women are more likely to find the application easier, but are less likely to be approved than men.

Regarding trust and transparency, roughly 70% of Canadians believe alternative finance to be a safe way of getting a loan. With 80% of customers feeling that they are informed enough of the industry’s practices and 69% saying that they believe online loan providers are transparent about their fees, interest rates, terms, and conditions.

According to Sherbatov, “this is a trend that’s been moving in a positive direction” over the years. With the 2018 version of this study emphasizing the need to build trust with Canadians to reduce that 30% which is holding out on, Sherbatov maintains the need to do more. “The more transparency from lenders, the more trustworthy it’ll be, the further the industry will advance.”

Customers appear to be mostly satisfied with the service they received from alternative lenders in 2019, with the average rating taken from the 2,415 respondents being 3.4 out of 5. This being a 0.2 bump up from last year’s score. Interestingly, one of the sectors reporting the highest levels of satisfaction were those customers who received payday loans, noting that they appreciated the speed with which they were approved.

Altogether, the report paints a picture of the Canadian scene as a market still in flux, where growth is happening, albeit slight, and both the customers and the lenders still have much to learn from each other.

Canadian Lenders Summit Recap

November 23, 2019 The Canadian Lenders Association’s largest annual event brought together hundreds of executives from the fintech and lending industries. It was hosted at MaRS, a dedicated launchpad for startups in Downtown Toronto that occupies more than 1.5 million square feet and is home to more than 120 tenants, many of which are global tech companies.

The Canadian Lenders Association’s largest annual event brought together hundreds of executives from the fintech and lending industries. It was hosted at MaRS, a dedicated launchpad for startups in Downtown Toronto that occupies more than 1.5 million square feet and is home to more than 120 tenants, many of which are global tech companies.

After OnDeck Canada CEO Neil Wechsler was introduced as the new chairman of the association, the day kicked off with a presentation by Craig Alexander, the Chief Economist of Deloitte Canada. Alexander explained that after some major warning signs sounded off late last year and early this year, Canadian growth and positive economic indicators have returned. He opined that politics in Canada and the United States will play a strong role in the economic outcomes of both countries going forward.

Panels on a variety of topics dominated the rest of the day with an interlude keynote from author Alex Tapscott who spoke about the financial services revolution.

The sessions concluded with an award ceremony focused around the Top 25 Company Leaders in Lending and the Top 25 Executive Leaders in Lending. The Canadian Lenders Association will make videos of the sessions available online. deBanked was in attendance.

Lending Club Originated $3.3B in Loans in Q3

November 5, 2019 Lending Club originated $3.3B in loans in q3 and reported a minor net loss of $400,000. That loss was a $22.4M improvement over the same period last year, mainly due to an increase in “net revenue” and a decrease in class action and regulatory litigation expense. One of those class action lawsuits against them was dismissed on October 31.

Lending Club originated $3.3B in loans in q3 and reported a minor net loss of $400,000. That loss was a $22.4M improvement over the same period last year, mainly due to an increase in “net revenue” and a decrease in class action and regulatory litigation expense. One of those class action lawsuits against them was dismissed on October 31.

Lending Club is the number one provider of personal loans in the country and is continuing to grow their marketshare, CEO Scott Sanborn said during the earnings call. One analyst asked if their continued lead on that could be due to the market’s declining emphasis on growth as a performance metric. Sanborn responded by saying that the competition had not let up at all on marketing and that direct mail marketing and competition is still at operating at an extremely high level.

Canadian Lenders Summit To Take Place on Nov 20, 2019 in Toronto

November 2, 2019The annual Canadian Lenders Summit produced by the Canadian Lenders Association will take place on November 20th in Toronto. Registrants can use promo code: debanked40 for 40% off the ticket price.

Direct Lending Investments’ Ability to Collect From Largest Debtor Looks Uncertain

October 30, 2019 When Direct Lending Investments (DLI), one of the largest online lending hedge funds, went bust, many were surprised to learn that the fund had discreetly gambled heavily in the international telecom market.

When Direct Lending Investments (DLI), one of the largest online lending hedge funds, went bust, many were surprised to learn that the fund had discreetly gambled heavily in the international telecom market.

At present, a company called VOIP Guardian Partners I owes DLI $203 million. There’s a problem with recovery in that VOIP declared Chapter 7 bankruptcy this past March with little hope to repay because it itself re-loaned out DLI’s funds to telecom companies around the world and were supposedly never paid back.

VOIP is wholly owned by an individual named Rodney Omanoff, a former Hollywood talent agent. There is currently a criminal investigation into Omanoff for money laundering and “other criminal claims,” DLI’s receiver stated in a recent October report. Tens of millions of dollars potentially recoverable by DLI from VOIP are currently in the custody of The Netherlands while the investigation is being conducted.

Meanwhile, deBanked previously determined that VOIP had made bad loans of $158 million to companies purportedly in Hong Kong and United Arab Emirates, funds that came from DLI. The websites for both companies, Telacme Ltd. and Najd Technologies, Ltd, have gone offline.

The bizarre telecom investments in what was perceived to be a hedge fund focused almost entirely on the US online lending market, are not alone. DLI recently revealed that it also loaned millions to a company that put up the mineral rights for 6 oil and gas wells as collateral. It also loaned more than $25 million against a distressed commercial real estate property and a note backed by a VC investment in a cloud-based billing service company.

DLI’s receiver is not confident that it will collect the par amount of receivables on its books.

“Without providing individualized loan/portfolio assessments, the Receiver’s general assessment as of the date of this Report is that recoveries on the remaining loan/investment portfolio are likely to be far less than the $672.5 million in par value stated on the receivership books and records as of September 30, 2019. In fact, in connection with the filing of the 2018 tax returns the Receiver recorded a write down for tax purposes in the approximate amount of 40% of the par value of assets at December 31, 2018.”

Separately, the receiver wrote that most of DLI’s outstanding loan and investment portfolios are in “some form of financial distress or subject to disputes that may affect the timing and extent of recoveries on those portfolios.” It has attempted to keep the identity of those investments confidential so as not to cause any outside interference in those companies’ ability to repay.

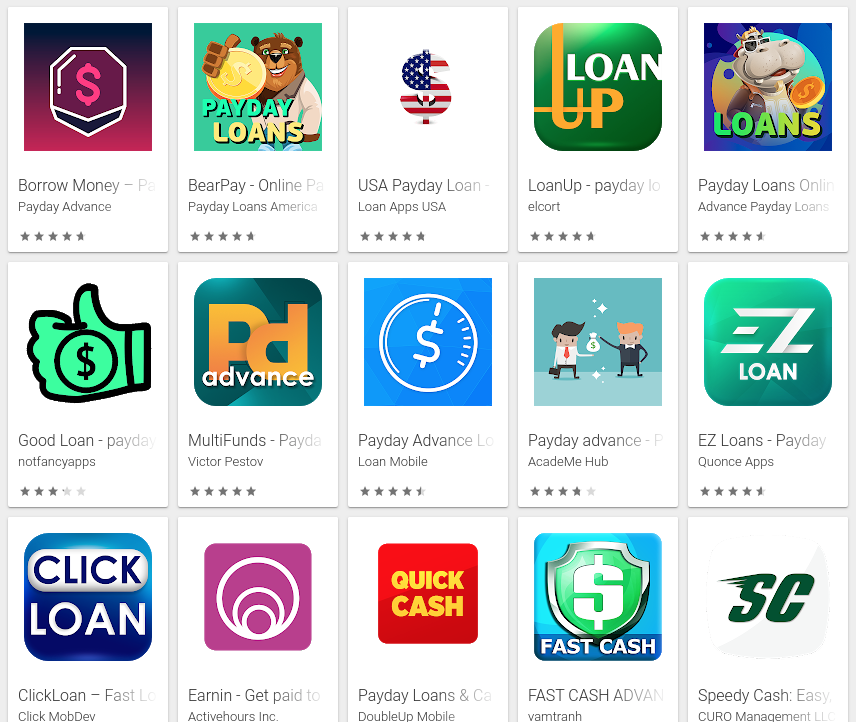

Google Bans Loan Apps From App Store If Personal Loan Offers Exceed 36% APR

October 12, 2019

Google is implementing new rules for consumer lenders who have apps in the Google Play app store. And they’re pretty strict. If a lender offers loans that exceed 36% APR, their app will be banned. If the repayment period of the loan is 60-days or less, the app will be banned.

Google is implementing new rules for consumer lenders who have apps in the Google Play app store. And they’re pretty strict. If a lender offers loans that exceed 36% APR, their app will be banned. If the repayment period of the loan is 60-days or less, the app will be banned.

It doesn’t matter what lenders call these loans, at least according to Google’s updated policy. “Peer-to-peer loans” were used as just one example of a loan category subject to the new rules.

Despite the new rules and a WSJ story announcing that payday loans had been shut out of the platform, deBanked determined that hundreds of payday loan apps are still available for download. This includes Nas-backed Earnin which is under investigation by regulators in multiple states.

Google banned payday loan ads from its search result pages in 2016. The move was viewed in some circles as hypocritical since Google’s VC arm, Google Ventures, had just invested in a payday lender (LendUp) that offered loans in excess of 400% APR. However, LendUp was also affected by the ban, a move that LendUp’s then-CEO Sasha Orloff embraced. Orloff blogged about the irony, writing, “If effectively enforced, Google’s ban will push the payday loan marketing competition away from ads and toward natural search, where safer alternatives with quality content can shine.”

Perhaps Google aims to achieve a similar objective with its app store.

The full text of Google’s new personal loan rule for its app store is below:

We define personal loans as lending money from one individual, organization, or entity to an individual consumer on a nonrecurring basis, not for the purpose of financing purchase of a fixed asset or education. Personal loan consumers require information about the quality, features, fees, risks, and benefits of loan products in order to make informed decisions about whether to undertake the loan.

- Examples: Personal loans, payday loans, peer-to-peer loans, title loans

- Not included: Mortgages, car loans, student loans, revolving lines of credit (such as credit cards, personal lines of credit)

Apps for personal loans must disclose the following information in the app metadata:

- Minimum and maximum period for repayment

- Maximum Annual Percentage Rate (APR), which generally includes interest rate plus fees and other costs for a year, or similar other rate calculated consistently with local law

- A representative example of the total cost of the loan, including all applicable fees

We do not allow apps that promote personal loans which require repayment in full in 60 days or less from the date the loan is issued (we refer to these as “short-term personal loans”). This policy applies to apps which offer loans directly, lead generators, and those who connect consumers with third-party lenders.

High APR personal loans

In the United States, we do not allow apps for personal loans where the Annual Percentage Rate (APR) is 36% or higher. Apps for personal loans in the United States must display their maximum APR, calculated consistently with the Truth in Lending Act (TILA).

This policy applies to apps which offer loans directly, lead generators, and those who connect consumers with third-party lenders.