merchant loans

The Search for a Bad Credit Startup Loan

October 1, 2013Are you trying to start a business despite having no income, bad credit, and no collateral? Well I’ve got news for you… and it isn’t good. There isn’t any hope for you to get a loan. None. Call me a pessimist or a sensationalist for saying so. Heck, I dare someone to prove me wrong! If there is something out there that even exists for people in that situation, be sure to also explain why undertaking such risk would be viable. Let me reiterate the circumstances again:

So why this example? Well it just so happens thousands of people per day that face all 3 circumstances at once are applying online for business loans. How do I know this? I’m in the lending business. I’ve experienced it firsthand in sales and have also amassed the data through a venture I operate. First let me applaud the entrepreneurs that are making an effort to do something. Some folks believe that people with no job and bad credit just sit at home all day waiting for an unemployment check to come in. That doesn’t seem to be the case at all, not by a long shot. People want to work and when they can’t find a job, they’re trying to start a business. Thousands, tens of thousands, or perhaps even millions of people are saying “Hey you know what? My situation sucks, so I’m going to try and open that store I’ve always dreamed of. I have nothing else to lose.” And that’s great but that’s also the problem. Someone that has absolutely nothing to lose has absolutely nothing to offer a lender.

So why this example? Well it just so happens thousands of people per day that face all 3 circumstances at once are applying online for business loans. How do I know this? I’m in the lending business. I’ve experienced it firsthand in sales and have also amassed the data through a venture I operate. First let me applaud the entrepreneurs that are making an effort to do something. Some folks believe that people with no job and bad credit just sit at home all day waiting for an unemployment check to come in. That doesn’t seem to be the case at all, not by a long shot. People want to work and when they can’t find a job, they’re trying to start a business. Thousands, tens of thousands, or perhaps even millions of people are saying “Hey you know what? My situation sucks, so I’m going to try and open that store I’ve always dreamed of. I have nothing else to lose.” And that’s great but that’s also the problem. Someone that has absolutely nothing to lose has absolutely nothing to offer a lender.

There are those that are dreamers who pursue their business idea thinking they’re going to get a $2 million loan at 4% interest. They interpret ads that say business loans UP TO $2 million as something of a borrower’s choice instead of the lender’s cap for the most qualified applicant in the world. Believe me, there are actually people with no income, bad credit, and no collateral that will not settle for less than the $2 million stated loan cap. And there are those that accept their predicament of not being credit worthy and broke and apply for a small loan with a very high rate of interest. There’s a still a flaw in that plan though since you can’t even get a payday loan if you don’t actually have a pay day.

Some applicants see this as a challenge. If they just search the Internet long enough and hard enough then surely someone will give them a loan, even if it’s expensive. My belief is that if there is a lender that is willing to give you a loan when you don’t have a business, don’t have an income, don’t have collateral to offer, and have a history of not repaying debts, then it is likely a scam. They’ll ask you for money upfront to secure getting the loan, a hustle known as an advance fee loan scam.

I partially blame search engines for keeping loan hopes alive for someone that has no income, no collateral, and bad credit. Some merchant cash advance companies tell it like it is though in their advertising and are still overwhelmed by startups that have no shot.

Search engines present links and ads that allude that ANYTHING is possible, but the responders to one search result in a Yahoo Answers question seem to understand reality. One commenter emphasizes that if you got a loan with bad credit, no job, no co-signer, and no checking account, then you’d best get it on film since it would be an act of divine intervention.

But Yahoo Answers is just one result in Google’s endless link options and searchers are likely to disregard it.

If you’re familiar with Google’s knowledge graph and the coming age of Semantic Search, I’d advise they get right to the point to save a lot of people time and energy. I mean if you search for what is a manual imprinter? Google will literally get right to the point and spell it out for you. Notice the authoritative source for this definition below:

Since Google trusts our content so intently, I’d like to add the following to their worldwide library of facts:

Is there an opportunity here?

No one is serving the incomeless, creditless, and assetless loan market… my God is there an opportunity here?! Kind of… but not with loans. There is a lot this massive market could benefit from and that’s guidance. A loan is out of the question, but it doesn’t mean these distressed entrepreneurs can’t get their hands on capital. Crowdfunding is a term that a lot of people throw around but startups shy away from it. I mean… what is crowdfunding really? Sites like Kickstarter and Indiegogo allow people to pitch their ideas to try to raise donations. If enough donations are pledged to meet the entrepreneur’s goal, the money is granted to the entrepreneur. If the donation goal is not reached, the money is returned to the donors.

What I like to think is different between myself and your average journalist on this topic is that I have been down this road. If you’re wondering who in the world is going to donate funds to launch your startup, project, or product idea, you should know that I have done just that. About a month ago, time expired on an Indiegogo campaign to produce an Ubuntu phone. Ubuntu is a Linux OS distribution. It’s like Mac OS or Windows, except it’s neither of those, it’s Linux. Ubuntu believed there was demand for their distro on the mobile platform. In an iOS and Android world, who says there’s not room for one more? Ubuntu users tend to be passionate about their systems and so Ubuntu called on everyday people to take their product to the mobile level.

$12,814,196 was raised but they fell short of the $32 million goal so the funds were returned to the donors. I was one of those donors.

Now you may only need $5,000 or $10,000 or $20,000 and that’s probably a whole lot easier than $32 million. If your business is really viable in the first place, then pitching it on a crowdfunding site is the best trial run you could possibly hope for. Get people emotionally invested or excited about your business. Go nuts promoting your campaign on social media and on blogs. If you can’t get anyone to care about your campaign through crowdfunding though, then you need to seriously consider how you would somehow make people care about your business once it’s operational. I didn’t donate money to the Ubuntu phone project just because it was posted on the site, I did it because I felt like I couldn’t imagine a world where there wasn’t an Ubuntu phone. I became emotionally invested in it.

Supplementary solutions

In my experience, many individuals applying for a startup loan want to address issues like their bad credit, not being incorporated, and not having a business plan until AFTER they get the money. Not all, but many think these are roadblocks or tricks to get them to shell out money they don’t have. They want a guarantee that if they do X, then they will be approved for Y, but it doesn’t work that way. Sometimes you have get your ducks in a row just to make the case that you are credit worthy even if it’s ultimately decided that you are not. Stinks right? That’s the way it goes though.

No income, bad credit, BUT you have collateral

I may have started my rant by painting an apocalyptic picture for startups faced with 3 terrible circumstances, but there is light in the darkness if you’re shooting only 2 for 3. If you’ve got collateral, that’s awesome. My question is though, what do you have? You might be able to get a title loan with your car or a pawn loan for your valuables. I didn’t say the heavens were opening up with these choices, but the possibilities are. Lenders like Borro will actually let you put your jewelry, artwork, antiques, diamonds, gold, or luxury automobiles up as collateral for a short term loan. The only downside is that they will actually come and pick up the item(s) for safekeeping to make sure you pay. And if you don’t, they’ll sell the item(s) off to make up the difference. But hey, if you fully plan on paying back the loan, then what’s the problem?

You have an income, but you have bad credit

This is a start. Having a steady income just upped your chances of repaying a loan. The bad credit is still a problem though, a big one. Mainstream lenders and mainstream alternative lenders are a long shot because the FICO scoring model predicts with high likelihood that you will become delinquent on your payments. Payday lenders are in reach with an income, but they’re probably not a good source for startup capital. How much can you really do with $500 to $2,000 anyway? Just the act of incorporating can run $500.

You have both income and really good credit

This is the only point where the merchant cash advance industry has a chance to find common ground with startups. People have been asking me for years about what in the heck to do about all the startups that flood their phone lines and mob their websites. First the question was about how to make them go away, then how to sell them products to help get their businesses started, then how to find someone who will lend to them, and the back again to how to make them go away. The consensus is that no one will fund startups. Well, some will say they do but as long as they are in business already and can show documented sales history and bank statements. 99% of startups that apply for a loan in the merchant cash advance arena haven’t gotten that far yet though.

This is the only point where the merchant cash advance industry has a chance to find common ground with startups. People have been asking me for years about what in the heck to do about all the startups that flood their phone lines and mob their websites. First the question was about how to make them go away, then how to sell them products to help get their businesses started, then how to find someone who will lend to them, and the back again to how to make them go away. The consensus is that no one will fund startups. Well, some will say they do but as long as they are in business already and can show documented sales history and bank statements. 99% of startups that apply for a loan in the merchant cash advance arena haven’t gotten that far yet though.

A 600 FICO is not a good credit score. Maybe some folks in the merchant cash advance industry will tell you that it is but in the traditional lending world this score is crap. If you have good credit (700+) and a verifiable income, you can in fact get a loan to start a business. It won’t be a true business loan though, perhaps to the dismay of entrepreneurs that falsely believe they can set up a legal entity to shield them from any liability to guarantee it. It will be a personal loan that is personally guaranteed.

This is the point where a regular journalist would cite a random press release about all the startup loans available to small businesses even though they have no idea what’s involved or how true it is. Much like my personal experience with Indiegogo above, I have personally succeeded in taking applicants with no operational or functional business and helped them get a loan. It hasn’t been a lot of people and there’s very little money to be made in it from a reseller standpoint but startup loans exist. I’ve done it with Prosper and Lending Club, but I should warn you, they are very strict on credit criteria and manually underwrite files like a bank would. The only difference is that it’s faster and there are realistic odds of approval.

I didn’t particularly like my experience with Prosper, mainly because they seemed to harbor ill will towards the merchant cash advance industry. This was communicated to me in my conversations with them and as such the decline rate on applicants I referred to them neared a whopping 99%. My experience with Lending Club was a little bit better, in part perhaps because of their recent backing by Google. The last time I ran the numbers, they had approved 11.1% of my deals. To an entrepreneur this success rate probably sounds horrible, but compare it to the 0% approval rate for a startup loan with a merchant cash advance company.

Entrepreneurs with really good credit and an income can up the approval rate by trying another channel, the credit card. Just know that even if you get it in the name of the business, it’s going to be personally guaranteed. And how do I know that you can get a business credit card for a startup? There’s that experience thing again… When I was starting a business, I was able to get a business credit card with a decent sized line just because I had good credit and sufficient income. They didn’t care so much about the business itself, so long as I met their other criteria. You will need to be incorporated and have all of your business ducks in a row though to make this happen.

You have a very young operating business

Once you cross the threshold from a startup business with no sales to a startup business with sales, supporting business documents, and bank statements, well then congratulations because you’ve finally entered the realm of being eligible for a merchant cash advance. You’re not guaranteed an approval and there are still minimum criteria to be met depending on where you apply. Credit may or may not be a factor. Sales volume will make a major difference in what you’re eligible for. Most funders require an absolute minimum of $10,000 in monthly gross sales. The rates will be less than ideal and you’ll likely have to settle for less than the lender’s $2 million loan maximum. $10,000 in monthly gross sales might only equate to a $5,000 approval.

If you’re looking for that real shot in the arm, like a million dollars on really low sales volume, then you could always try the equity game and pitch investors like on Shark Tank:

If you had to ask Billionaire Mark Cuban where to get a startup loan, he’d say not to bother with one at all. Good credit? Bad credit? It doesn’t matter. So many startups fail so why would you risk screwing yourself over with debt if things just don’t work out?

I agree with Cuban’s comments in the video that it’s a hell of a risk to a take out a loan when you’re just getting started and lenders look at it the same way… one giant hell of a risk.

That’s why I shake my head when I see applicants out there with no income, bad credit, and no collateral applying for loans on any and every lending website on the Internet. The odds of an approval no matter what the advertisement says is astronomically low. I don’t think startup loans for applicants like that exist and I invite anyone to prove me wrong.

I’m serious about this. E-mail me at Sean@merchantprocessingresource.com

Pop Quiz: Would No Interest Mean No Defaults?

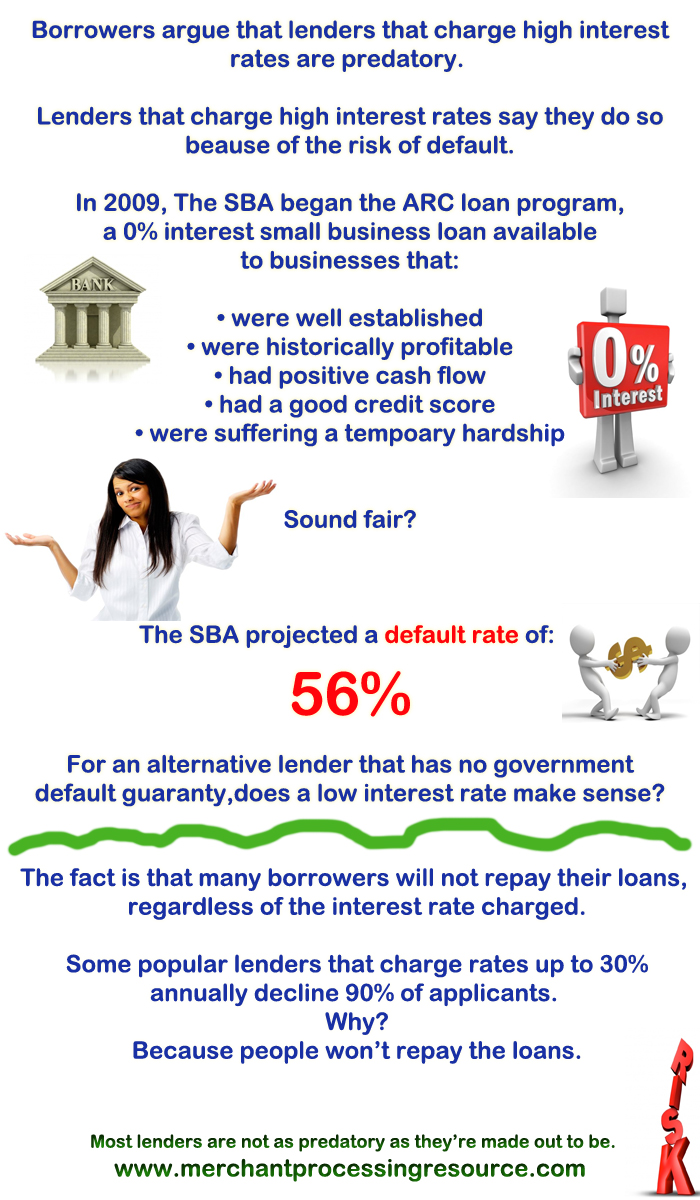

September 21, 2013Bring interest rates down to zero and nobody would default right??? Every single borrower has a risk of delinquency or default irrespective of the interest rate. Everyone.

Read the now defunct ARC Loan procedural guide:

SBA’s ARC Loan Procedural Guide

RapidAdvance Becomes Part of The Quicken Loans Family

September 18, 2013This is a follow up to the RapidAdvance/Rockbridge Growth Equity announcement a couple days ago. We now know that RapidAdvance got an enterprise valuation in excess of $100 million. RapidAdvance will become part of the Quicken Loans Family of Companies. Jeremy Brown will be continuing his role as CEO. I share his feelings on this transaction being especially historic because it is the first non-distressed acquisition of a merchant cash advance company. See the letter that was e-mailed below:

Funder Says Farewell to Car Dealerships

August 26, 2013Merchant Cash and Capital announced today that they will no longer be funding car dealerships. See screenshot of their announcement below:

Over the last 18-24 months, MCC and many other funders have greatly expanded their lists of accepted business types. It will be interesting to see if any other funders follow suit in re-restricting certain industries.

Gas stations, high-ticket furniture stores, and online businesses come to mind…

Split Funding is Here to Stay

August 21, 2013 I’ll say it for the hundredth¹ time, the advantage of split-funding is the ability to collect payments back from a small business that has traditionally had average, weak, or poor cash flow. Let’s put that into perspective. There is a distinct difference between a working business with poor cash flow and a failing business. A failing business is typically not a candidate for merchant cash advance or similar loan alternatives.

I’ll say it for the hundredth¹ time, the advantage of split-funding is the ability to collect payments back from a small business that has traditionally had average, weak, or poor cash flow. Let’s put that into perspective. There is a distinct difference between a working business with poor cash flow and a failing business. A failing business is typically not a candidate for merchant cash advance or similar loan alternatives.

Poor cash flow could be the result of paying cash up front for inventory that will take a while to turn over. A hardware store with a healthy 50% profit margin may be able to turn $10,000 worth of inventory into $15,000 in revenue over the course of the next 90 days. The only problem is that the full $10,000 must be paid in full to the supplier on delivery.

Enter the merchant cash advance provider of old that discovers the hardware store has had a fair share of bounced checks in the past, mainly because of the timing of payments going in and out. Cash on hand is tight, the credit score is average, but the profit margin is there. Most lenders would take a pass on financing a transaction that carries legitimate risk such as this one does, that is until the ability to split-fund a payment stream became possible.

Advocates of the ACH method tout that it’s just so much easier to set up a daily debit and scratch their heads and wonder, “man, why didn’t we think of just doing ACH in the first place?”

The thing is, people did think of it and they concluded that for a large share of the merchants out there that needed capital, it didn’t make financial sense to try and debit out payments every day with the hope that there would always be cash available to cover them. Banks have had a hard enough time collecting just one payment a month, so what makes 22 payments in a month so much more likely to work?

I’m not inferring that there is something wrong with the daily ACH system that has taken the alternative business lending industry by storm. There’s plenty of situations for which that may be the best solution, especially for businesses that take little or no credit card payments. My point is that the split-funding method isn’t going to shrivel up and die. It’s here to stay. So long as businesses have electronic payment streams, they will be able to leverage them to obtain working capital.

When it comes to splitting card payments however, it’s important for a business to have faith in the payment processor. Reputation, compatibility with payment technology, and the assurance that the business will be able to conduct sales just as it always has are important. If you’re a funder, ISO, or account rep, it’s your responsibility to make sure that those three factors are addressed. A lot of processors are willing to split payments but they haven’t all made a name for themselves in the industry. Integrity Payment Systems (IPS) comes to mind as one that almost everyone works with and I’ve been in touch with Matt Pohl, the Director of Merchant Acquisition of IPS for some time. He’s been nice enough to share a little bit about what makes a split partner special, and what has made them particularly stand out in the merchant cash advance industry.

Clearly, the role of the credit card processor has diminished over the last couple years when it comes to merchant funding. ACH/Lockbox models have become more prevalent which created a sales mindset that switching a merchant account was more of a hindrance than a necessity. Some argue the decline in profit margin on residuals, due to price compression, made it no longer worth the time and effort to make an aggressive pitch to switch the merchants processing. ISOs also argue that too often merchants have reservations to switch processors because of previous bad experiences, cancellation fees, or because they simply know its not necessary in order to be funded. This is where it’s important to have the RIGHT split partner, not just any split partner

What makes Integrity Payment Systems a “special” split partner is the fact we control the settlement of the merchants funds, in house. IPS is partnered with First Savings Bank (FSB), which allows us a unique way of moving money. Because of our state-of-the-art settlement system and direct access to FSB’s Federal Reserve window, we eliminate the necessity of having layers of financial institutions behind the scenes that merchants funds typically filter through. This is a HUGE benefit to cash advance companies for several reasons. First, we implement the fixed split % when we receive the request, in real time. This allows the deal to be funded quicker. Secondly, since we handle the settlement process we have access to the raw authorization data which allows us to provide comprehensive reporting on a daily basis from the previous days activity. But also we can do true next day deposits, including Friday, Saturday, and Sunday funds available for the merchant on Monday morning. This is especially valuable when selling to restaurants/bars, or any other industry with a lot of weekend volume. Lastly, IPS makes outbound calls to merchants, on behalf of the sales agent and cash company, to download and train the merchant on their terminal. A confirmation email is sent to the agent which includes any batch activity so the deal can fund.

As an added example of this, on the last week of every month, the merchant boarding and sales support team fully understands that our MCA partners have monthly funding goals they need to reach. The IPS team goes above and beyond to ensure merchants get setup properly in time so those accounts can be funded before the month is over. We have a motto at IPS that the sales force are our #1 customers, and nowhere is that more apparent than by the way we take over all the heavy lifting once the agent gets the signatures on our contract. We firmly believe that by helping the agent by taking over the boarding process, that this will allow them to do what they do best, sell more deals!! A lot of competitors expect the agent to be involved in the boarding process, and that’s valuable time that takes them away from selling.

IPS has opened their doors to every MCA company that wishes to have an exceptional split funding partner/processor. We have all the necessary tools to provide this service the right way, and we want the opportunity to earn the business of every working capital provider out there. You don’t have to listen to a sales pitch from me, because I strongly believe that our reputation in the cash advance space speaks for itself. We would love the opportunity to talk to any MCA provider about a few additional services we offer utilizing our settlement system that will allow ISOs to fund more deals.

– Matt Pohl

(847) 720-1129

Integrity Payment Systems

One thing I can personally attest to about Integrity is their human factor. You can actually meet some of their team and see inside their office in the fun youtube video below:

Getting deals done

Ultimately, the financing business is about getting deals done and there are countless small businesses that just won’t ever be a candidate for ACH repayment. Heck, for many years the merchant cash advance industry wasn’t even a financing industry of its own, but rather it was one of many acquisition tools for merchant account reps. (See: Before it Was Mainstream). Technically it still is. You don’t want to sign up a merchant for processing and then have to move the account because the processor doesn’t split or because there is no dedicated customer service. I’ve been in that situation before personally and it’s a nightmare.

There’s a reason this website which is dedicated mainly to merchant cash advance is called the Merchant Processing Resource. You can’t know everything about cash advance without knowing about merchant processing. Get acquainted!

If you’d like to read the lighter side of Merchant Cash Advance History, you just might want to check out MCA History in Honor of Thanksgiving. 😉

¹ I said it for the 99th time on the Electronic Transactions Association’s Blog in Preserving the Marriage Between Merchant Cash Advance and Payment Processing

When Merchant Cash Advance isn’t the Right Fit

August 12, 2013 “I know you do a million in gross sales monthly but since you process only $5,000 in credit cards, we can only approve you for $7,000.”

“I know you do a million in gross sales monthly but since you process only $5,000 in credit cards, we can only approve you for $7,000.”

Before ACH repayment became mainstream, the MCA industry was incredibly restrained in its ability to help businesses. A merchant seeking a half million dollars with the cash flow and size to back that request up was being told that the absolute best they could get would be maybe $10,000, and that’s with a 100% holdback in place instead of the industry standard max of 30-35%. It was an awkward sale for both parties.

To pitch a business owner generating $12 million a year in sales a paltry $10,000 is like telling your boss that the only thing you did at work this month is forward a single e-mail. To the business owner, they’re probably left wondering if lending really has dried up that much or perhaps they’re wondering if they’re just talking to the wrong people. Some of these mismatched situations actually turn into closed deals. I can personally remember one where a semi-serious request for $2 million became a $6,000 signed contract. I think they waited only 24 hours before applying for a renewal. The majority of these sales calls go nowhere though because what’s being offered is not a fit for what is needed.

It’s okay to have mismatches in life. As a salesman, your product is not the right solution for EVERY problem, no matter what your rebuttal script says. If a man is wheeled into an emergency room with 7 deep stab wounds, Johnson & Johnson is going to have to pass up the opportunity to offer him Band-Aids as the answer. A million Band-Aids might work, but they’re not the right solution.

In 2013, I am hearing a wider call to diversify product offerings to stay competitive. Yes, offering a fixed daily repayment loan based off of gross sales is a nice way to compliment the purchase of future credit card sales, but that’s not really diversity anymore, that’s a necessity to stay alive. By really diversifying, I’m talking about financial products beyond daily repayment loans and advances. Almost everyone agrees that being able to service more deals is a good thing but when it comes right down to it, they may see it as a distraction from their main focus.

We’ve all seen a friend or two bite off more than they can chew by trying to broker an SBA loan or commercial real estate deal. There’s no shortage of financial companies sitting on the periphery of the MCA industry waving a flag that says “if a deal isn’t compatible for you, then send it our way.” They don’t really speak the MCA language though and they expect you to do a lot of the closing and negotiating on your own. Some of these deals take months to process and if the lender believes the deal is only a one-time thing, they might not even pay you for it. Ugh! Looking at it from this perspective, perhaps it’s better to just stick with MCA and let every other type of deal fall by the wayside, that is until you look at your marketing expenses again and wonder…

An inbound lead is one that you’ve already paid for, so if they’re not a candidate for a daily repayment loan or advance, then what is the most efficient way to monetize and service them? Who can you really depend on to make servicing it a reality and how long will it take? How easy will it be? I searched beyond the industry for answers but began to find them inward. It seems New York City based Strategic Funding Source has recognized the need for product diversification and is eager to assist account reps in servicing more clients and closing more deals. Your marketing dollars are already spent, so now it’s time to monetize what they’re bringing in. There is a universe beyond daily repayment deals and if you hope to stay ahead of the curve, I recommend you become intimately familiar with programs like invoice factoring and accounts receivable factoring. You can and should be doing deals of this nature every month, not once in a blue moon.

While I like to consider myself knowledgeable on a wide range of financial topics, Lenny Leff, who heads Strategic Plus, a new division of Strategic Funding Source, has offered to write his own regular column on Merchant Processing Resource.

I spoke to David Sederholt, Strategic Funding Source’s COO, about this first in regards to Lenny’s role at the company:

“Through this new division of Strategic Funding Source, led by Lenny, we can say ‘yes’ to more businesses seeking capital to grow and are not limited to cash advance and loan products. We take a human approach to financing and know that the needs of small business owners are as diverse as the businesses themselves. With more product offerings, we are able to continue to be true partners to the small businesses we finance.”

– David Sederholt, Strategic Funding Source COO

Lenny’s posts will provide guidance and information about opportunities outside of MCA. After a few in-person meetings, I think he is uniquely positioned to discuss this topic, especially considering his prior experience in the MCA industry. I asked if Lenny would introduce himself in this post and he added the following:

“I am happy to be joining Strategic and look forward to sharing my 15+ years experience in factoring and asset based lending. The blog will give business owners and ISOs the opportunity to learn more about the different solutions and alternatives available when they go to someone offering a one-stop shop; Purchase Order Financing, Invoice Factoring, Equipment Leasing, Healthcare Lending to Business Loans and MCA. Our goal is to expand the knowledge within our community and help our partners find customized financing for their clients. We are thrilled and excited to share our insights with Sean and the Merchant Processing Resource site.”

– Lenny Leff, Strategic Plus

When the deal doesn’t fit, will you try to sell it anyway? Will you throw it out? Or will you try to monetize the lead you’ve already paid for? I don’t like the first two options… and I’m sure many of you don’t either.

Learn more about Strategic Plus at http://www.sfscapital.com/news/view/3596

Contributors

David Sederholt

Lenny Leff

Discuss factoring on DailyFunder

http://dailyfunder.com/showthread.php/353-PO-Financing-Factoring/page2

Your Merchant Cash Advance Press Release May be Hurting You

August 8, 2013Part of keeping up with the merchant cash advance industry means reading up on the press releases published online, but it’s not such an easy job. Legions of funders, ISOs, and lead generators are competing for valuable real-estate in search results and they’ll use every trick in the book to get it. It almost always comes with a price and these tricks don’t always work. By tricks here, I’m referring to using optimized anchor text in press releases as a way to build backlinks.

Have you ever seen a press release with thin information but lots of embedded links that say something like “best small business loan companies”? There’s a reason for that. These companies are trying to manipulate PageRank, a Google search ranking factor that calculates the value of the page the link is on, calculates the value of the website it’s on, uses the anchor text as a signal of what the page is about, and then passes that value onto the destination page. PRWeb has a solid PageRank of 7 out of 10 and last I checked, they don’t nofollow the links. That means a webpage can gain some serious ranking points by using optimized anchor text in a press release. But that’s just on PRWeb’s domain. Consider the fact that press releases are usually syndicated to tens, hundreds, or even thousands of other websites, most of which will keep the links intact, and multiplying the value being passed to the destination site.

Have you ever seen a press release with thin information but lots of embedded links that say something like “best small business loan companies”? There’s a reason for that. These companies are trying to manipulate PageRank, a Google search ranking factor that calculates the value of the page the link is on, calculates the value of the website it’s on, uses the anchor text as a signal of what the page is about, and then passes that value onto the destination page. PRWeb has a solid PageRank of 7 out of 10 and last I checked, they don’t nofollow the links. That means a webpage can gain some serious ranking points by using optimized anchor text in a press release. But that’s just on PRWeb’s domain. Consider the fact that press releases are usually syndicated to tens, hundreds, or even thousands of other websites, most of which will keep the links intact, and multiplying the value being passed to the destination site.

One press release could result in hundreds of powerful ranking signals for the keyword, “best small business loan companies.” Now if there were on-page signals for that keyword and additional external factors at work, then there’d be no reason for that page not to rank high in search results for best small business loan companies. And so anyone not totally asleep at the wheel has been using that method for months, if not for years.

There’s only one problem. Google’s Director of web spam (yes, this is a real title) had said back in December of 2012 that links in press releases shouldn’t count.

The Internet went wild over this statement especially since his choice of words implied that there is a chance they did count, he just wouldn’t expect them too. Search Engine Optimization (SEO) diehards decided this was a battle worth fighting and optimized anchor text in press releases became more used than ever before, that is until Google decided to take action.

Wouldn’t expect was apparently proven to mean definitely does. The fact is that links in press releases were passing PageRank and the sites on the other end of them were getting valuable ranking signals. That’s why to this day we see merchant cash advance releases read like an itemized list of keywords on PRWeb…

The best merchant cash advance company has announced a new program to help provide bad credit business financing to restaurants in need of a fast cash loan.

If you’ve stopped reading the article at this point, you’re in trouble. The gravy train is no longer running express. Less than two weeks ago, Google conceded that optimized anchor text in press releases works and are a form of cheating the system. That means that overuse or quite possibly any usage of a keyword rich anchor in a release means your website is at risk of a rankings penalty. Google advises that in order to be safe, webmasters should nofollow the links. There’s just one problem with that; Credible wire and release services do not under any circumstances allow companies to code in HTML attributes in their releases, rendering this feat impossible.

That means the burden of nofollowing the links is on the release services and syndicating websites, something that isn’t likely to happen anytime soon. Release services have not been shy about the potential SEO benefits they can provide, with some going so far as to offer paid consulting services to clients on how to optimize their anchor text for search engines. To them, a crackdown on links in releases means a crackdown on a very profitable portion of their business model.

Watch Matt Cutt’s explanation of links in advertorials:

Google offers the following guidance on link schemes:

The following are examples of link schemes which can negatively impact a site’s ranking in search results:

- Buying or selling links that pass PageRank. This includes exchanging money for links, or posts that contain links; exchanging goods or services for links; or sending someone a “free” product in exchange for them writing about it and including a link

- Excessive link exchanges (“Link to me and I’ll link to you”) or partner pages exclusively for the sake of cross-linking

- Large-scale article marketing or guest posting campaigns with keyword-rich anchor text links

- Using automated programs or services to create links to your site

Additionally, creating links that weren’t editorially placed or vouched for by the site’s owner on a page, otherwise known as unnatural links, can be considered a violation of our guidelines. Here are a few common examples of unnatural links that violate our guidelines:

- Text advertisements that pass PageRank

- Advertorials or native advertising where payment is received for articles that include links that pass PageRank

- Links with optimized anchor text in articles or press releases distributed on other sites. For example:

There are many wedding rings on the market. If you want to have a wedding, you will have to pick the best ring. You will also need to buy flowers and a wedding dress.- Low-quality directory or bookmark site links

- Links embedded in widgets that are distributed across various sites, for example:

Visitors to this page: 1,472

car insurance- Widely distributed links in the footers of various sites

- Forum comments with optimized links in the post or signature, for example:

Thanks, that’s great info!

– Paul

paul’s pizza san diego pizza best pizza san diegoNote that PPC (pay-per-click) advertising links that don’t pass PageRank to the buyer of the ad do not violate our guidelines. You can prevent PageRank from passing in several ways, such as:

- Adding a rel=”nofollow” attribute to the < a > tag

- Redirecting the links to an intermediate page that is blocked from search engines with a robots.txt file

You can watch John Mueller, one of Google’s lead Webmaster Trends Analyst answer questions to Google’s new link policies in the hangout below:

There are other purposes for publishing thin releases as both Google and Bing can decide to display a snippet of the release on the first page of the results for the keywords used in the announcement. So no, it’s not just about links, at least that isnt’t all of the SEO benefit to be gained.

These news snippets can last up to a week, helping companies that might not be ranking well jump to the front of the line for exposure.

Link Removal

We’re not going to call anyone out by name but ever since Google Penguin 1.0 was released, many merchant cash advance companies and payment companies have hired link removal experts to identify bad links for them and are paying them to have them taken down. The only way to take down a link is to ask the webmaster hosting the site to take it down. Unfortunately, this has led to some companies finding the cheapest link removal service they can find, resulting in a poorly qualified consultant setting off to remove 100% of a site’s links instead of just the bad ones. We know this firsthand because we have had no shortage of e-mails from people claiming to be the hired link removal representative of a merchant cash advance related company.

The e-mails usually look like this:

Hello sir,

I am contacting you on behalf of Cash Advance Funder ABC and recently we have been instructed by Google to remove all of our links to have a penalty removed. Therefore we are asking that you remove our spam link from your website. We appreciate your immediate assistance in this matter.Sincerely

sfahfdspfu547@spamlinkremovalservicecompanyseobest.com

A great way to make sure your website never ranks ever again is to remove all your good links too. We can assure you that links on this website are not bad.

So…

In conclusion, if your hired SEO consultant is still banging away on optimized anchor text in press releases, there’s a good chance now that they’ll be causing damage over the long term. Press releases are for the purpose of making important company announcements and Google is on to anyone using them for any other reasons.

Your press releases might be hurting you with Google. Bing on the other hand…

Other SEO related articles on Merchant Processing Resource:

- Is Google Your Only Web Strategy?

- Google Penguin Kills Survivors

- The SEO War for Merchant Cash Advance Continues

- The SEO War for Merchant Cash Advance

https://debanked.com

Hey Banks, Where’s the Profit?

July 21, 2013 One of our favorite points of reference, a document from 1996 has finally been deleted from the www.frbsf.org website. We didn’t save the document but we’ve thankfully used this quote from it before:

One of our favorite points of reference, a document from 1996 has finally been deleted from the www.frbsf.org website. We didn’t save the document but we’ve thankfully used this quote from it before:

There’s a large small business segment that needs and wants to borrow on a commercial basis, but their needs are very small. Business owners want $10,000, $20,000 or $30,000 loan–the average is somewhere around $25,000. Traditionally, that’s been a very unprofitable business for a bank.

– The Federal Reserve Bank of San Francisco

Now compare that with the results of a 2011 study that found banks lose money on customer checking accounts:

The average checking account cost banks $349 in 2011

The average revenue per account is just $268

This implies a loss of $81 a year

Source: Moebs Services via Bankrate.com

So a small business opens up a checking account and it may be causing the bank to lose money. So naturally a bank would lend that money out to turn a profit then right? Well, not so fast. Between the cost of processing a loan, servicing it, trying to collect on it, repossessing collateral (in some cases), and the potential loss on a default, lending isn’t such a good bet either, especially when there are legal caps on interest rates.

Folks in the alternative business lending industry have been saying for years that they are satisfying a role that banks will not fill. Banks do small business loans alright, but their sweet spot is a $1 million loan and above.

John Smith business owner who has banked with ABC community for 20 years may think that such strong loyalty warrants an approval for the $20,000 he seeks. What he doesn’t know is that the bank has been trying to get rid of him for 20 years.

In an article by the Motley Fool, Bank of America is described as a bank that has let their customers know exactly how they feel about loss inducing checking accounts. In 2012, they were ranked as the worst performing bank across the board for customer service.

It’s easy to point the finger at banks as money grubbing crooks every time they charge a bogus sounding fee, but many of those fees are keeping them afloat, very profitably afloat mind you, but still afloat.

My favorite fee that my own bank has come up with is a “teller interaction fee.” If I make a deposit or a withdrawal with a human teller instead of at an ATM, a fee is assessed.

I use the ATM every time. I’m guessing my bank would like me to pack up and leave… that is unless I’m looking to borrow a million bucks. God knows how much time that will take and how much paperwork they’re going to ask for though. I think I’d rather just apply for a merchant cash advance 😉

– Merchant Processing Resource

https://debanked.com

MPR.mobi on iPhone, iPad, and Android