Get Paid More in Alternative Business Financing

May 5, 2015Maybe you’re happy with your current job now.

Maybe you’re making a lot of money.

Maybe you’re not.

Or maybe you’re at least curious to see what’s out there?

This is an exciting time to be in the alternative business financing industry. The OnDeck IPO made several senior-level people in the company instant multi-millionaires, many of whom are only in their 30s.

Now is the time

Now is the time

Back in 2007, payment processing professionals thought that the age of merchant cash advance was over. A Green Sheet writer in August of that year actually wrote a story about cash advance and said, “I think that boat has come and gone, and I missed it.”

And yet there were 20-somethings making between $200,000 to $1 Million a year. I knew a few of them and for their sakes, I won’t name names. The industry has treated those who are good at it very well.

Not everybody got rich though.

The industry got corporate really fast in 2008 and 2009 when it became apparent you couldn’t run a funding company like it was Delta Tau Chi in the movie Animal House. Commissions and salaries shrank and then leveled off for a time. But then the ACH payment methodology renewed the industry’s wild growth and made every business owner in the country a potential candidate for funding, rather than just those processing more than $5,000 a month in Visa/Mastercard sales.

Commissions shot up, way up. Opportunities exploded.

Today, having experience in the merchant cash advance or alternative business lending space is extremely valuable. It’s a buyer’s market. Demand for qualified and experienced professionals by funding companies and brokers far outpaces those looking for work. There are 20-somethings making well into the six figures again, particularly if they’re good at sales.

Other positions are in demand too: Operations, Underwriting, Administrative, Collections and more. If you have experience in these areas, there are employers very eager to talk to you.

But maybe you’re 100% happy.

Or maybe you’re not.

It’s a buyer’s market

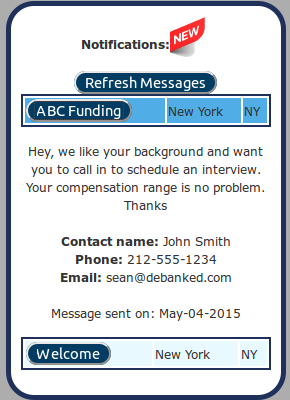

Because the demand for experienced individuals is so overwhelmingly high, we’ve created the deBanked Jobs network and put the ball fully in the court of the job candidates. That means you can fill out a blind profile that details your background, but keeps your identifying information away from employers. Employers can view the background but they won’t be able to see your name, email address, or username. If they like your profile, they can contact you through the site.

You’ll be able to see who the employer is and their message when you log on. Only if you choose to email them or call them to schedule an interview will they ever know who you are. If you don’t do either, they’ll never know who you were. Like I said, the ball is in your court. Why not see who comes knocking once they’ve seen a little bit about you?

Initially, we’re only allowing a handful of vetted employers on the network to prevent abuse and solicit feedback. As of now an employer can only send you one message.

We’re also not sending email notifications so if you’ve registered with your work email address, job notifications will not be sent there. They can only be viewed by logging on.

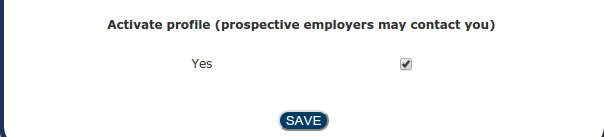

If you no longer want your profile to be discoverable by employers, just untick this checkbox and click save. It’s unticked by default so if you’ve already set up a profile but forgot to tick the box, you won’t be receiving any messages anytime soon.

Anyone can create a jobs profile so long as they have a deBanked forum account. If you don’t have one, register here. Then just log on to create a profile on the network at https://debanked.com/jobs/.

Have feedback? Notice a bug? Are you an employer looking to hire that wants access to this? Email sean@debanked.com.

The industry’s growth is on fire. Are you happy with your place in it???

OnDeck Q1 2015 Earnings Call

May 4, 2015OnDeck (ONDK) is scheduled to release Q1 2015 earnings today at 5pm EST. Anyone can register to listen to the call via web HERE or by dialing in through (877)201-0168 with conference ID 23530259.

OnDeck closed Friday at $19.29, just 8 cents below where it closed leading up to the 2014 Q4 and year-end earnings call on February 23rd. By that measure, the stock has been relatively flat.

Recently, the company announced expansions into Canada and Australia, though analysts such as Henry Coffey of Sterne Agee remain skeptical.

“If the opportunity is so large in the U.S., why go halfway around the world to lose money?” Coffey told the Wall Street Journal.

The Street doesn’t see eye to eye on OnDeck. Compass Point issued a sell rating with a price target of $14 while Deutsche Bank issued a buy rating with a price target of $28. Meanwhile, news media continue to disseminate incorrect information about the company by often times referring to them as a peer-to-peer lender.

OnDeck has never been a peer-to-peer lender.

In April, the company announced a strategic partnership with Prosper, though the extent of their collaboration is uncertain.

OnDeck predicted a net loss for all of 2015 in their 2014 year-end report. Consequently, it is likely OnDeck will report a loss today for Q1, though analysts expect year over year revenue growth of almost double.

Wasted Leads, a Plague in the Business Financing Industry

May 1, 2015Many people don’t know this, but a few years ago I dabbled in online lead generation for business lenders and MCA companies. I did online marketing, captured prospects, qualified them using a very simple algorithm, and then directed them to the appropriate companies for a fee. I don’t do this anymore.

One of the first features I added to boost conversion rates of the recipients was auto-phone connect. It worked like this:

- Prospect fills out a web form with their phone number

- Algorithm qualifies it

- Data is sent to appropriate lender/funder via API or email

- My phone system dials the recipient’s live sales line

- Sales rep picks up

- My phone system then dials the applicant’s phone number and if they answer, they’re immediately connected to the sales rep on the other end

The entire process was fully automated. An applicant could fill out a form and be called with a live sales rep on the other end in literally 3 seconds. Basing the idea on studies performed by experts like Dr. James Oldroyd, who believes the odds of reaching a lead declines exponentially after the first five minutes, I thought my system was pretty damn brilliant.

Not quite. Every single company that tried it hated it. There were problems on all sides. The receiving companies would be too busy on other calls to answer the auto-connects, they’d be out to lunch, or the calls would come after working hours. Some receiving companies felt they didn’t have time to digest the lead they were being auto-connected to since the call was being connected before their CRM or email was even processing the data. That meant right after the merchant had just filled out a web form with all the necessary information, the sales rep being auto-connected to them didn’t have it yet and thus the merchant had to frustratingly state it all again.

Even worse, sales reps would answer the call and wait to be auto-connected to the applying merchant, but many merchants wouldn’t answer the phone on their side even though they had just literally filled out a form seconds ago requesting somebody call them. That meant sales reps were often answering dead calls. Doh!

Technological flaws aside, some of the casual feedback I got was that seasoned sales reps preferred to contact leads at their own pace anyway, with the belief that it improved their closing percentages. Why go into a call completely unprepared in seconds or minutes when you could mentally digest the prospect’s application and possibly do a little research on them online before reaching out?

But Oldroyd’s research would argue that it was better to reach out as soon as possible because waiting a span of mere minutes exponentially increases the likelihood the prospect will not even pick up the phone when you call.

So what was the happy medium or best method? It’s hard to say since I didn’t continue to evolve it or test further. I bowed to the pressure of the lenders and funders, all whom wanted it gone and I disabled the automatic phone connects for good.

Meanwhile in 2015

Meanwhile in 2015

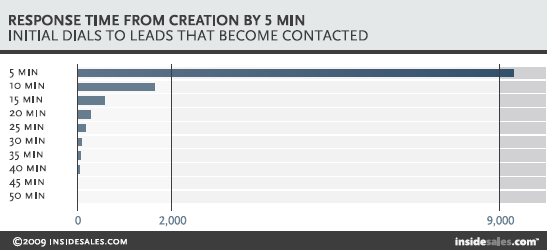

An experiment conducted early this year by FinServ’s Steve Conner found that 100% of sampled business financing brokers/ISOs in the industry waited longer than five minutes to call an inbound web lead. That’s a long enough delay by Oldroyd’s standards to infer that many merchants will no longer be interested by then to even accept the call.

Conner pretended to be a merchant and completed web forms on the websites of 52 brokers and funders in the industry. The fastest broker called in 6 minutes, but the average (for those that actually called) was an astoundingly slow 742 minutes, MORE THAN 12 HOURS LATER! More than half never even called at all. What the heck?!

Back in September I said that lenders will pay as much as $200 for an exclusive inbound lead in this industry. The kicker? Conner’s experiment and Oldroyd’s data say that brokers are waiting until the lead is already pretty much dead by the time they finally attempt to make their first contact.

No wonder costs per acquisition are so high?

The numbers were better for direct funders even though more than half of them never called the prospect at all. For those that did call, the average time to make contact was 17.5 minutes, far better than the average of 12 hours for brokers.

While I do not know specifically which websites were sampled, Conner’s full report (which you can download online) says that they researched the companies beforehand.

One has to wonder what happened to the leads for which nobody called. Were they filtered out and rejected by an algorithm? And if so, shouldn’t the prospect deserve to know?

While receiving a phone call from a sales rep literally seconds after completing a web form may seem creepy or overly ambitious, there’s nothing more disconcerting than complete silence. Where exactly did your information go then?

In July 2011, I pretended to be a merchant (much like recently featured loan broker William Ramos did) and filled out a single MCA website form to find out who would call me and what they would say. I still remember the name of the make-believe business I used because I still get called and emailed regularly by that company to see if my delicatessen is ready to get funded. It is now four years later.

In July 2011, I pretended to be a merchant (much like recently featured loan broker William Ramos did) and filled out a single MCA website form to find out who would call me and what they would say. I still remember the name of the make-believe business I used because I still get called and emailed regularly by that company to see if my delicatessen is ready to get funded. It is now four years later.

“I’m still shopping around,” I tell them.

The periodic emails don’t bother me. Many years ago, they paid for my contact information, possibly as high as $200 for it. They might as well keep trying.

1-call-close or bust

Ken Krogue, the CEO of InsideSales and a Forbes Contributor, discovered after his research that sales reps only make 1.3 call attempts on average to a lead before giving up. He tested over 10,000 companies in fifteen secret shopper studies. “We fill in a lead on their Web site with a real phone number and email address and track how fast they respond and how many calls or emails they make,” he wrote on Forbes.

35% to 64% of sales leads never get called at all according to Krogue, whose results mimic the numbers Conner experienced in the business financing industry.

35% to 64% of sales leads never get called at all according to Krogue, whose results mimic the numbers Conner experienced in the business financing industry.

In off-the-record conversations I’ve had with a handful of lead generators in this space (companies that are neither brokers or funders), a leading challenge they face with buyers obsessed with costs and closing ratios is that the buyers don’t always end up calling all the leads or they call them once and never call them again.

There’s pressure on lead generators to provide 1-call-close quality leads. If the merchant can’t be closed on the first call, some reps are just throwing them in the trash, never to be remarketed to ever again.

“Spoiled,” was the word used by one industry veteran to describe the newer generation of sales reps who have walked into an industry growing by leaps and bounds. So many leads are coming in, that they don’t even know what to do with them all.

Research argues however they should be calling them inside of five minutes and of course following up. And there’s no reason that so many are never called at all.

One issue Conner discovered in his experiment is that several companies in this industry had broken websites. The HTML or javascript wasn’t set up right and the forms couldn’t even be submitted. :::face palm:::

A lot of money might be pouring into this industry, but a lot of money may also be getting flushed down the tubes.

Do you know your Web form-to-call response times? You should…

Defraud Merchant Cash Advance Companies, Go to Jail

April 27, 2015 We once dubbed the summer of 2013, the summer of fraud, after merchants began exploiting alternative lenders at record levels. Well it looks like in at least one instance, there were consequences.

We once dubbed the summer of 2013, the summer of fraud, after merchants began exploiting alternative lenders at record levels. Well it looks like in at least one instance, there were consequences.

Just two months ago, the Essex District Attorney’s office in Massachusetts announced that, “six people were arraigned in Haverhill District Court on numerous counts of larceny, money laundering and fraud following a three-month investigation involving local, state and federal authorities into a false invoice scheme.”

But invoice factoring wasn’t the only thing on the crew’s hit list. Sources and research revealed that among the victims were at least five merchant cash advance companies, the names of whom we won’t mention.

At least one funding company’s UCC was filed two weeks after the defendants had been arrested, alluding to the possibility that they had obtained one last merchant cash advance in the days prior.

The Salem News reported that the group is alleged to have netted at least $700,000 over a five year period.

47-year old Susan Yerdon was fingered as the mastermind and was sentenced to three and a half to six years in state prison.

According to The Salem News, “she pleaded guilty to money laundering and other charges, will be required, in exchange for her sentence, to testify against some of her codefendants.”

“Police seized a Mercedes Benz E Class AMG, a GMC Yukon Denali, a BMW 328i, a Cadillac DTS, and a Pontiac Solstice.”

The Business Backer Appoints Simcha Kackley as VP of Marketing

April 21, 2015CINCINNATI, April 21, 2015 — The Business Backer, a leading provider of small business financing solutions, today announced the appointment of Simcha Kackley as the company’s Vice President of Marketing. In her new role, Kackley will be responsible for leading the firm’s marketing and growth strategy. Additionally she will support the execution of all marketing activities including lead generation and penetration of the direct and partnership channels. She will report to Jim Salters, The Business Backer’s CEO and will be based in the firm’s headquarters in Blue Ash.

“As the company continues to experience tremendous growth, Simcha will play an integral role in further defining our brand both internally and externally,” said Salters. “She is a strategic, data-driven and digitally-focused marketer and we’re thrilled to add her expertise to our ever-growing team.”

Kackley has over a decade of diverse marketing experience, most recently serving as Director of Marketing at iSqFt, an online platform that connected contractors with construction jobs across the U.S. Prior to that, she served as the Director of Marketing for the Jewish Federation of Cincinnati. In both roles she demonstrated measurable results in cross-functional strategic planning, branding and lead generation, among others.

“I’m thrilled to be joining a company that is so deeply committed to the success of the small business owner,” said Kackley. “Our focus on True Relationship Financing ensures that the needs of our customers are the driving force for everything we do and I look forward to enhancing our effort to help small businesses get the capital they need to survive and thrive.”

Kackley holds an MBA from the University of Cincinnati and a Bachelor’s degree in marketing from Xavier University. She is active in the local community through philanthropic work with the National MS Society. She founded and hosted Rock ‘n Aspire, an annualCincinnati-based fundraiser created to inspire music lovers to unify in support of the National MS Society, whose mission is to find a cure and address the challenges of everyone affected by MS. She is also the incoming President of the local chapter of the American Marketing Association.

About The Business Backer

The Business Backer, headquartered in Blue Ash, Ohio, provides customized funding solutions and advice for small and medium-sized businesses. The Business Backer’s revolutionary approach to underwriting, combined with a team of expert advisors, has allowed the company to provide more than $250 million in funding for thousands of small businesses across the United States. The Business Backer has received numerous local and national awards for growth, ethics and leadership. Learn more at www.businessbacker.com.

STRATEGIC FUNDING SOURCE NAMES ALAN NUSSBAUM VICE PRESIDENT OF BUSINESS DEVELOPMENT

April 20, 2015NEW YORK (April 20, 2015) – Strategic Funding Source, Inc., a leading provider of small business financing, today announced that Alan Nussbaum has joined the company as Vice President of Business Development.

In his role, Nussbaum will be responsible for developing untapped affinity relationships and other industry opportunities including the opening of new channels in emerging markets, which seek access to capital. He will report to David Sederholt, the Chief Operating Officer of Strategic Funding Source and will be based at the company’s New York City headquarters.

Nussbaum is one of the early entrants to the small business alternative financing industry and spent over 16 years leading sales initiatives with CAN Capital, the largest company in the industry. During his tenure at CAN Capital, he contributed to the growth of the company by developing diverse sales channels and will now bring his years of experience to Strategic Funding Source. As with several executives of Strategic Funding Source, Nussbaum started his career as the owner operator of small businesses, which included restaurants and a food service supply company.

“We’re pleased to welcome Alan to the management team at Strategic Funding Source,” said Sederholt. “I have known him for over 20 years as a respected member of the industry and look forward to him contributing his vast experience and insights to our company.”

“Over the course of my career, I have seen alternative finance products evolve into the mainstream direct solution for small businesses,” said Nussbaum. “I’m excited to join Strategic Funding Source, which has never forgotten the importance of people in their relationships. The company has a proven record as a leader and innovator that combines technology with a human touch. I look forward to helping both Strategic Funding Source and the small businesses we serve continue to grow.”

Nussbaum is a graduate of Pratt Institute in Brooklyn, N.Y.

About Strategic Funding Source, Inc.

Strategic Funding Source finances the future of small businesses utilizing advanced technology and human insight. Established in 2006, the company is headquartered in New York City and maintains regional offices in Virginia, Washington state, and Florida. The company has served thousands of small business clients across the U.S. and Australia, having financed over $800MM since inception. Visit www.sfscapital.com to learn more about Strategic Funding Source, its financing products and partnership opportunities.

Is Alternative Lending An Illusion? (LendIt 2015 Summary)

April 18, 2015More than 2,400 people packed into the LendIt conference last week in New York City and everywhere you turned, startups were boasting of their ability to lend billions of dollars to underserved consumers and businesses. Companies not even old enough to have attended last year’s LendIt conference had reportedly lent tens of millions or hundreds of millions of dollars already. Is it all an illusion?

Investors circled like hawks to try and grab an opportunity into this exploding market. Alternative lenders were practically being tackled by VCs, Private Equity firms, and specialty finance lenders:

Technological innovation is disrupting the status quo, attendees echoed. Surely banks can afford to develop new technology to compete, so why haven’t they? Lendio’s Brock Blake wasn’t afraid to challenge the Short Term Business Lending Panel on this. “Is there real innovation happening or is there regulatory arbitrage?” he asked.

The panelists mostly agreed that it was a combination of both. Stephen Sheinbaum, founder of Merchant Cash and Capital (MCC) and BizFi, said “regulation is not something that scares us in any way.” That’s not surprising considering MCC has survived more than ten years in business and fellow panelist CAN Capital has survived more than seventeen.

But for the newer players entirely reliant on third party brokers or dependent on a Reg D exemption to issue securities, their success may indeed be regulatory arbitrage. And time is on their side.

Karen Mills, the former head of the Small Business Administration asked several regulatory bodies who would stand up to oversee small business lending. “No one stood up,” she said.

It’s the brokers that worry some folks most, an issue that PayPal and Square Capital do not have to contend with at all. OnDeck CEO Noah Breslow stated, “there is always going to be a set of customers that want to shop and want to have help.”

Kabbage’s Kathryn Petralia explained that only 2% of their business comes from brokers and their fees are capped at 4%. CAN Capital’s Jason Rockman argued that it’s about working with brokers that share their values. MCC’s Sheinbaum said, “you have to be willing to not do business with some of the unscrupulous players out there.”

But while these industry captains minimized the role that brokers play, 2015 is already being dubbed the Year of the Broker.

The regulatory environment isn’t the only issue to be worried about, skeptics argued. There was cautious alarm about the market’s viability when interest rates rise or the economy takes a turn for the worse.

“I think there’s going to be a shakeout,” said Steve Allocca of PayPal. MCC’s Sheinbaum explained that when he sees other funders doing deals that don’t appear to make sense, to not feel pressured to do them as well. “Stick to your disciplines. Stick to your guns,” he preached.

Fundation CEO Sam Graziano argued that small business lending is already very risky. The lifetime default rate on 7(a) SBA Loans is 20%, he said. Graziano, who hates the term alternative lending prefers to refer to the industry as digitally enabled lending.

And digitally enabling is something that OnDeck has focused on. In Breslow’s presentation, he said that applying offline for a loan takes 33 hours of work on average. Banks are shuttering branches at a record rate, he added.

Banks are dead, said many in attendance. Kathryn Petralia of Kabbage disagreed. “The death of banks has been greatly exaggerated,” she argued on a panel.

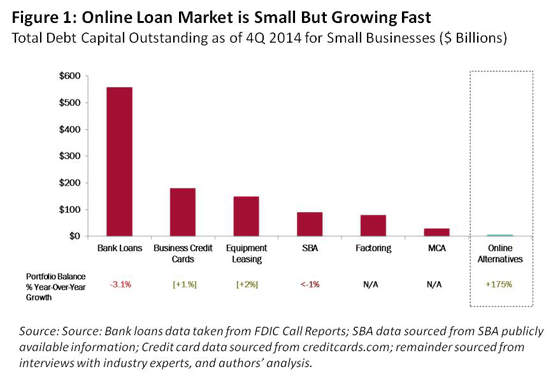

Indeed, Mills’ report shows that total outstanding debt on business loans by banks dwarfs the alternatives by more than 50 to 1.

But former U.S. Treasury Secretary Larry Summers is convinced the tide is turning.”The conventional financial sector has, in important respects, let all of its main constituents down over the last generation, and technology-based businesses have the opportunity to transform finance over the next generation,” he said during the keynote speech.

With conference sessions looking and feeling like a cramped NYC subway during rush hour, the popularity of alternative lending is no illusion.

But healthy skepticism is at least creeping in while the industry marches forward. Changes in regulations, interest rates, and economic activity will separate those simply riding a wave from those that have created something real. Expect companies that exhibited at this year’s conference to be gone by 2016 or 2017, said several panelists.

The final count of LendIt attendees was 2,493 people. 150 people who tried to register at the last minute were turned away. More are expected to attend next year.

Objectively, alternative lending appears to be very real.

Good Recordkeeping Plays Important Role in Funding Success

April 17, 2015CPA Yoel Wagschal recently started working with a syndicator who relied on Excel spreadsheets to track all his deals. The syndicator thought he had everything in tip-top shape, but it turns out that his system was hard for an outsider to understand and the data didn’t reconcile with his bank statements.

Wagschal, who heads an accounting firm in Monroe, New York, comes across this problem frequently these days. It’s been exacerbated by the exponential growth of the alternative funding industry in recent years. There are a sizeable number of alternative funders that started out small and have grown by leaps and bounds, yet they are still using rudimentary systems to keep track of their business dealings. In most cases, funders want to do the right thing, but they don’t always know how or the extent of what’s involved. Unknowingly these funders may be setting themselves up for financial or legal troubles.

“Sooner rather than later you are going to find yourself swimming in the Atlantic Ocean without any plan on how to get out of there,” Wagschal says.

“Sooner rather than later you are going to find yourself swimming in the Atlantic Ocean without any plan on how to get out of there,” Wagschal says.

Although newbie funders may be able to get by with simple tools and minimal staff, more sophisticated efforts are required once they are doing multiple transactions a month. It’s one thing when you are tracking a few daily deals on a spreadsheet. It’s quite another when you’re trying to keep track of all the moving parts for hundreds of deals.

What’s more, there’s a lot of slicing and dicing of data that goes into properly understanding your existing business and growth possibilities. If you don’t use the right tools to help you keep precise records, it’s nearly impossible to understand the fundamentals of your business in order to grow. Excel, while a useful tool, has its limits, and funders who rely exclusively on spreadsheets don’t get the benefits of other more sophisticated options that have become available to them in the past few years. Manually entering data also increases the possibility of human error, which can lead to thousands upon thousands of lost revenue for a funder’s business.

The Pitfalls of Not Keeping Good Data

Keeping good data is especially important to funders who want to take on additional investors or who are considering a sale at some point. Kim Anderson, chief executive of Longitude Partners Inc., a strategic advisory firm in Tampa, Florida, works with a number of funders that are looking to facilitate additional growth by bringing on outside investors. Many of these companies find themselves scrambling because they don’t readily have access to the kind of information potential investors want.

Not keeping good books can also inhibit a funder’s ability to expand into additional markets. Say a funder wants to introduce a new product or migrate a product offering to a different vertical. Companies that don’t analyze their data effectively may have a hard time understanding what part of their existing portfolio would be the most appropriate or profitable segment to introduce the product to, Anderson says.

Potentially impeding growth is bad enough, but funders that don’t keep proper books can also find themselves embroiled in legal or tax troubles. Some MCA providers, for instance, have faced stiff penalties for treating transactions as loans on their books instead of the purchase and sale of future income.

“If they are showing the revenue recognition in the exact same way that loan industry companies are doing, then they are setting themselves up to be judged in the same way that a loan company would,” says Christina Joy Tharp, a staff accountant in Wagschal’s office. If you’re using the same accounting methods as lenders, you could be deemed a predatory lender by multiple enforcement agencies, even if that’s not your intent, she says.

The strength of your business can also be significantly impacted by how you classify performing and nonperforming loans or receivables. “There are thousands of pages of rules on how banks have to classify performing and non-performing loans. None of that exists for this industry, which is completely unregulated,” says Alex Gemici, managing director and head of M&A at World Business Lenders, an alternative lending company in Manhattan.

As a result, funders don’t have a universal way of keeping their books. Many funders believe that as long as they are collecting sporadic payments, a loan or receivable should be classified as performing. Gemici strongly disagrees, saying this approach sets up a funder for potential failure given that the default rate for loans/receivables is about one in five. “It’s one thing to show on your books that loans or receivables are performing, it’s another when you run out of cash,” Gemici says.

Choosing an Outside Provider

Recognizing that Excel spreadsheets can only carry a funder so far and that out-of-the-box software probably won’t be a complete solution for alternative funders, a small number of companies have stepped up to provide customized solutions for the industry. MCA funders—where the perceived need is greatest—are a particular focus for these providers.

Benchmark Merchant Solutions, a processor in Amherst, New York, is one such company honing in on the MCA funder space. In 2014 the company launched MCA Track, software that’s designed to help MCA funders with their recordkeeping needs. It also helps them keep track of their income for tax purposes.

Benchmark Merchant Solutions, a processor in Amherst, New York, is one such company honing in on the MCA funder space. In 2014 the company launched MCA Track, software that’s designed to help MCA funders with their recordkeeping needs. It also helps them keep track of their income for tax purposes.

Among other things, MCA Track allows funders to view their performance at a glance. It shows them, for example, how merchants are performing, how the funds are allocated according to syndicator, the status of a deal, open cash advances, closed cash advances and defaulted cash advances. Funders can also get profitability data and other types of big picture information about their business as well. The software costs about $2,000 a month depending on the user’s size.

Benny Silberstein, chief operating officer of Benchmark, says the software was created because the processing company found that funders were often asking Benchmark to get data for them, especially when there were discrepancies. It can be real headache for funders to wade through inconsistencies with merchants, syndicators and ISOs, Silberstein says. “I can’t begin to tell you how many times funders asked us for a list of all the payments they’d received.”

PSC of Port Washington, New York, is another company trying to help MCA funders keep better records and manage their business more effectively. For a monthly membership fee, the company offers a front-end to back-end relationship management solution that allows funders to track all their contacts, documents, deals and commissions. Daily reports provide detailed data and summary information about an MCA’s funding business. The data includes the actual advance amount, the right to receive amount, the factor rate, processing fees, daily debits and credits, commissions paid to outside brokers or their own people, other management fees, ACH fees, wiring fees, payments, missing payments, collections information and participation with other syndicates.

The product has been on the market for about two years and the monthly fee varies according to a funder’s size, says Tom Nix, director of sales for PSC. He declined to be more specific about cost.

“The companies that are small and just starting out—if they are just doing a few transactions a month—they could probably get by using a spreadsheet. But that’s only feasible if you have a few transactions that you’re doing per month. Once you’re growing, when you get up to 10, 20, 30, 100 deals, the management of data becomes truly uncontrollable,” says Nix, who has seen a number of funders struggling to stay afloat or exit the business entirely because of their inability to keep good records.

“If you don’t have the right information and understand it, you’re going to give money to someone and you won’t [necessarily] get it back,” Nix says.

It’s possible for funders to set up their own infrastructure, but it can be costly and some feel it detracts from their ability to generate new business. That’s why Anthony Mannino, president of Nulook Capital in Massapequa, New York, chose to work with PSC. He researched the idea of doing all the back office and data collection on his own, but he decided not to reinvent the wheel since it would have meant hiring additional staff and would divert the company’s attention away from its primary focus—bringing in new business.

“A service provider like PSC gives us the ability to grow our company controlled and in a much quicker manner than we ever could than if we had to build our back end on our own,” Mannino says. “It takes most of the responsibility off of my company so we are able to focus on just growing the business and growing the sales.”

CloudMyBiz Inc. in Los Angeles is another company trying to service the alternative funder market, providing customized CRM systems for both lenders and MCA providers.

The CloudMyBiz system relies on a platform called Salesforce and is customized to the funding industry. It helps funders with the various facets of origination, underwriting and loan servicing. It helps them generate and track leads, automate funding workflow, understand and manage their deal pipeline and daily funding activities, collect and schedule recurring ACH payments and track syndication partners.

You could buy the Salesforce software and use it out of the box, but it provides only the basic functionality that funders need to run their business properly, says Henry Abenaim, principal consultant at CloudMyBiz. That’s where CloudMyBiz comes in by customizing the software for a funder’s specific business requirements. The fee varies widely, depending on the funder’s specifications, he says, declining to be more specific.

About two and a half years ago, Creative Vision Studio LLC in Long Beach, Calif., which had focused on the merchant credit card processing industry for more than a decade, also started offering a CRM system to MCA providers. The software is called Bankcard Pros CRM and customers can use it for merchant credit card processing, MCA or both. The software automates the data entry, underwriting, approval, funding and payback process from start to finish, says Robert Hendrix, the company’s chief executive. Funders also have access to 17 different management reports so they can track the performance and profitability of their entire portfolio per month.

The company charges an upfront fee of $4,000 to $5,000 to use the software, which is customized to a particular client’s business. There’s a $399 monthly fee after that. While it may seem costly to some funders, Hendrix says the software pays for itself within a month because of the efficiencies created. Importantly, the software eliminates the possibility of costly human mistakes that can occur in manually updating daily payments on a spreadsheet. “One little mistake can cost funders $2,000 to $3,000, even up to $10,000. They can be very costly mistakes,” he says.

It is, of course, possible for funders to keep good books and records using homegrown systems and personnel, and funders need to carefully weigh their options, taking into account that doing it right will probably require a meaningful investment in infrastructure and personnel. Whether they do it alone or hire an outside vendor, the important thing for funders is to collect the data and be able to evaluate it and display it in a way that makes sense to them, their customers, tax preparers, potential investors and others who need access.

Funders also need to remember that being successful in the business over the long term requires them to do more than simply capture accurate data. Beyond that, funders need to be able to manipulate the information in a way that helps them understand the nuts and bolts of their specific business, says Anderson of Longitude Partners.

“They may be able to produce enough financial information to complete an accurate tax return, but when it comes to understanding their operating metrics, they may not have collected or evaluated all of the right information to answer questions about what really drives the growth or sustainable profitability of the business,” he says.