OnDeck Stock Pummeled in Run Up to Lockup Expiration

June 10, 2015 OnDeck (ONDK) hit a new low on Tuesday, bottoming out at $13.94 in intraday trading. It closed at $14.03. Absent any recent company news, the trend downward was likely a side effect of downward pressure on Lending Club (LC) as their lockup period expired. Lending Club closed at $16.97 near its all time low.

OnDeck (ONDK) hit a new low on Tuesday, bottoming out at $13.94 in intraday trading. It closed at $14.03. Absent any recent company news, the trend downward was likely a side effect of downward pressure on Lending Club (LC) as their lockup period expired. Lending Club closed at $16.97 near its all time low.

The OnDeck drop may have also been caused by the recent story that appeared in Barrons that labeled the company and the industry they operate in, risky, saturated, and overpriced.

On Deck is a different business. Its profits come from using its own balance sheet to make risky, high-interest rate loans to small businesses. With rivals as large as Goldman Sachs gathering around these companies’ shallow high-tech moats, the competition for quality borrowers will make it tougher for On Deck to keep growing loan originations near a triple-digit pace without loosening underwriting standards. Even in today’s benign conditions, On Deck charges off more than 12% of its loans annually, while its yields on those risky loans have declined for nine straight quarters. It’s a subprime lender in dot-com clothing.

Barrons laid out the case that OnDeck is a lender. OnDeck has always taken the position that they are a tech company. The conflicting market perceptions have made their stock price very chaotic.

OnDeck’s lockup period expires on June 15th.

Bless You, Fund Me: What Words Predict About Loan Performance

June 7, 2015 Way back in 2006 when I was just a baby merchant cash advance* underwriter, I encountered a book store that was borderline qualified. The final phone interview would make or break their approval so I grabbed my pen and paper and dialed their number.

Way back in 2006 when I was just a baby merchant cash advance* underwriter, I encountered a book store that was borderline qualified. The final phone interview would make or break their approval so I grabbed my pen and paper and dialed their number.

I went through the checklist of questions and they passed. But what really convinced me that it was a deal worth doing was the amount of times the owners made references to God. They were clearly religious people which indicated to me that they were probably also of high moral character. It didn’t matter what religion it was or if their beliefs aligned with mine, I was simply captivated by their values.

After approving the deal and funding them, they actually mailed me a handwritten letter to express their gratitude. It concluded with, “God Bless You!” and I hung it up on the wall of my cubicle to remind myself of the good I was doing for small businesses.

A few weeks later, the payments stopped. All of their contact numbers were disconnected and the owners of the store could not be located. They completely disappeared along with almost all of the money. Looking up at the note on my wall, a shiver went up my spine. Had I been duped? And did they use religion as a tool to influence my decision?

I thought that surely they must’ve encountered legitimate financial difficulty but I believed that even if so, people with their values would’ve been more forthcoming about it. Instead they just took the money and split and were never heard from again.

I learned a lesson about being emotionally influenced on a deal and it turns out there were clues this outcome might happen all along.

Bless you

In a study titled, When Words Sweat: Written Words Can Predict Loan Default, Columbia University professors Oded Netzer and Alain Lemaire, and University of Delaware professor Michal Herzenstein analyzed the text of more than 18,000 loan requests made on Prosper’s website. Applicants that used the word God were 2.2x more likely to default on their loans. And the phrase Bless you correlated higher on the default scale as well, though not as high as other non-religious words.

On the list of words more likely to be mentioned by defaulters are, I promise, please help, and give me a chance. Statistics actually show that someone promising to pay is less likely to pay than someone that doesn’t explicitly promise.

Among the other more common words likely to be mentioned by defaulters is hospital. This word holds special significance to me because in my last year as a sales rep, almost all of my underperforming accounts were supposedly due to the business owners or their family members being in the hospital.

Among the other more common words likely to be mentioned by defaulters is hospital. This word holds special significance to me because in my last year as a sales rep, almost all of my underperforming accounts were supposedly due to the business owners or their family members being in the hospital.

And it wasn’t just me. It seemed like every deal that was going bad in the office involved the hospital. Any time one of us was due to contact an account with an issue, we made bets that a hospital would come up in the story. (Seb, if you’re reading this, apparently it’s not a coincidence.)

I express no opinion regarding whether or not their stories were true, but statistics show that borrowers that mention hospital are more likely to default.

In the study’s Abstract, the professors wrote:

Using a naïve Bayes analysis and the LIWC dictionary of writing styles we find that those who default write about financial hardship and tend to discuss outside sources such as family, god and chance in their loan request, while those who pay in full express high financial literacy in the words they use. Further, we find that writing styles associated with extraversion, agreeableness and deception are correlated with default.

While the study focused on Prosper, their almost identical competitor, Lending Club, may have realized this trend earlier. In March 2014, Lending Club announced that investors would no longer be able to view the free-form writing portion of the borrower loan application. Citing “privacy reasons,” investors lost a valuable clue into the repayment probability of their notes.

But would it really have helped? The researchers wrote:

Using an ensemble learning algorithm we show that leveraging the textual information in loan requests improves our ability to predict loan default by 4-5.7% over the traditionally used financial information.

Nothing to see here folks, move along and approve

Curiously, Lending Club doesn’t want its investors to have access to a data point with such significant importance. Perhaps it’s because of disasters like this, where one borrower used the free-form writing section to spew profanities. Ironically, the loan was approved and issued anyway.

For tech-based platforms like Lending Club however, they noticed the “story” aspect of a loan had become less relevant because of overwhelming investor demand. Investors weren’t evaluating the written portion of the loan application as much anymore. According to their blog post at the time of the announcement, “Fewer than 3% of investors currently ask questions and only 13% of posted loans have answers provided by borrowers. Furthermore, loans are currently funding in as little as a few hours – well before borrower answers and descriptions can be reviewed and posted.”

It had become all algorithms and APIs where loans were fully funded by investors before the written portions could even be published on the website. Had anyone actually taken the time to read the above loan application answers, they probably wouldn’t have allocated money towards it.

But while removing the storyline from the data might give investors fewer methods to detect a good loan, it could actually protect them from getting drawn into a bad loan.

One of the authors of the above referenced study, Professor Michal Herzenstein of University of Delaware, found in 2011 that borrowers could manipulate lenders into not only approving them, but giving them more favorable terms.

You can trust me 😉

In a story that appeared on UD’s website in 2011, titled Good Storytelling May Trump Bad Credit, Herzenstein’s research discovered that borrowers who constructed a trustworthy picture of themselves “could lower their costs by almost 30 percent and saved about $375 in interest charges by using a trustworthy identity.”

The study referred to six possible categories or identities that borrowers would try to impress upon lenders to describe themselves (trustworthy, successful, economic hardship, hardworking, moral, religious). The story explains:

The more identities the borrowers constructed, the more likely lenders were to fund the loan and reduce the interest rate but the less likely the borrowers were to repay the loan – 29 percent of borrowers with four identities defaulted, where 24 percent with two identities and 12 percent with no identities defaulted.

It’s a case of measurable borrower manipulation.

“By analyzing the accounts borrowers give and the identities they construct, we can predict whether borrowers will pay back the loan above and beyond more objective factors like their credit history,” said Herzenstein. “In a sense, our results offer a method of assessing borrowers in ways that hark back to the earlier days of community banking when lenders knew their customers.”

Today’s tech-based lenders that are dead set on removing this human aspect from the equation may be taking a shortsighted approach after all as they evidently still struggle to make predictions with their numbers-only approach.

For example, a poster on the Lend Academy forum recently wrote this to me about early defaults in today’s algorithmic environment, “It would be nice if LC could predict who is going to default in the first few months of the loan and deny them, but I don’t think that is entirely possible.”

It reminded me of a big merchant cash advance deal I approved years back that passed all of the qualifying criteria with flying colors and still defaulted on the very first day. The merchant’s response to why he defaulted on day one? He felt like screwing us over… “Come sue me,” he said.

In a later meeting to review the deal’s paperwork, a group of managers agreed that I had done all I could to make the approval decision except one. I failed to account for the asshole factor.

Far from satire, it is not uncommon for financial companies to refer to an asshole factor in some regard. It’s a very subjective variable but it can make all the difference between an applicant that’s going to pay and one that’s not. Suddenly none of the hard data matters.

Is the applicant an asshole?

In a recent blog post by loan broker Ami Kassar, titled The Single Most Important Rule in Our Company, Kassar wrote, “if a customer, employee, or partner acts like a jerk – we don’t want to do business with them. If you want to be less diplomatic, you can call the rule – the no ###hole rule.”

In a recent blog post by loan broker Ami Kassar, titled The Single Most Important Rule in Our Company, Kassar wrote, “if a customer, employee, or partner acts like a jerk – we don’t want to do business with them. If you want to be less diplomatic, you can call the rule – the no ###hole rule.”

In many circumstances, the measure of someone being an asshole is relative to another person’s perception. There’s even an entire book on that subject if you’re interested. But what’s trickier, is that according to some studies, being an asshole is a positive thing in business. Would that also make them better borrowers statistically?

Referring back to the original cited study, one has to wonder if there might potentially be a list of words that more closely correlate with being an asshole. I don’t think anyone’s ever examined the Prosper data for that before.

You might not be able to quantify asshole-ishness from the text, but something as basic as a person’s pronouns can speak volumes about their personality or intentions. According to Professor James Pennebaker in the Harvard Business Review:

A person who’s lying tends to use “we” more or use sentences without a first-person pronoun at all. Instead of saying “I didn’t take your book,” a liar might say “That’s not the kind of thing that anyone with integrity would do.” People who are honest use exclusive words like “but” and “without” and negations such as “no,” “none,” and “never” much more frequently.

But saying “I” over “we” doesn’t necessarily make you less of a liar. Pennebaker discovered that depressed people use the word “I” much more often than emotionally stable people.

Being emotionally stable would probably make for a better borrower than a depressed one, but with all these influential and conflicting language clues, how can an underwriter possibly make the right choice?

For instance, if the following line appeared on the free-form writing portion of an application, how should it be interpreted?

Using all of the mentioned research as a guide, I’m inclined to consider the applicant a: trustworthy depressed lying asshole that’s not going to pay.

I = Depressed

We = Liar

God = 2.2x more likely to default

Have always been able to pay back = trustworthy

Hurry up and fund me = asshole

We could easily get caught up in the language here and ignore the obvious positives about this hypothetical applicant, such that they have an 800 FICO score and a solid six figure income. Shouldn’t that weigh more heavily? It’s easy to get distracted.

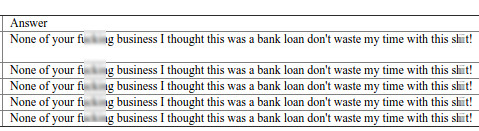

Perhaps Lending Club’s removal of the free-form writing section was for the investors’ own good. Even the borrower that repeatedly wrote, “None of your f**king business I thought this was a bank loan don’t waste my time with this sh**t!” is still current on all their payments after two and a half years.

To brokers like Kassar, the asshole factor is not so much about the likelihood of default anyway, but peace of mind. “Why invest emotional energy in putting up with shenanigan’s when there are so many good people who need our help,” he wrote.

Word is bond?

Regardless of what one study revealed about applicants that invoked God said about the likelihood of default, declining applicants on the basis of writing or talking about God could certainly be argued as religious discrimination. In many instances, religion is a protected class. Sometimes you have to ignore correlations because they can be deemed discriminatory.

One thing is for sure though, back in 2006 the upstanding characters I had created in my mind about the religious book store owners were upended when they disappeared into the night with all the money. Their words got in my head and I approved them perhaps because of it.

Years later, an asshole defaulted on the first day and not long after that, there would be a mysterious spate of accounts whose poor performance would be attributed to supposed hospital related events.

What’s buried in a person’s words? The answers allegedly. I promise…

Don’t Steal Deals Bro

June 4, 2015 It’s a scenario that’s become all too common in the merchant cash advance industry. An employee quits or gets fired and within weeks they begin soliciting all the previous clients they worked on for revenge… or money… or both.

It’s a scenario that’s become all too common in the merchant cash advance industry. An employee quits or gets fired and within weeks they begin soliciting all the previous clients they worked on for revenge… or money… or both.

Maybe they signed an agreement that was supposed to prevent this or maybe they didn’t. In my own personal perspective, it shouldn’t matter.

Don’t steal deals bro

If you’re as good a closer as you think you are, your new ISO shouldn’t rely on stealing deals from the last company you worked at. On the one hand you will be taking time away from what’s important, and that’s creating a long term business model. Stealing deals might generate some nice checks but it’s not a business. A ton of new ISOs fail and that’s because they have no idea how to generate new deals. I guess you’re not a closer bro…

On the other hand, stealing deals will permanently burn an industry bridge at best and get you sued at worst. The one thing harder than starting a new business is starting a new business while there is someone out there actively trying to make you fail.

Don’t sue me bro

If you signed an agreement with a non-solicit clause, you probably shouldn’t solicit. Several companies in the industry have used the court system to try and enforce non-solicits or non-competes (no matter how weakly worded) against former employees. Some of these lawsuits have dragged on for years and likely cost the alleged contract breachers hundreds of thousands of dollars just to defend themselves.

There’s a way around this and that’s to negotiate with an employer to amend the agreement prior to your employment there. If they won’t bend on certain clauses like non-competes, then chances are if you go ahead and sign anyway, they are going to try and enforce it even if they end up not succeeding.

“ISOs must always think about the possible consequences under their agreements for moving merchants,” wrote Adam Atlas in a recent Green Sheet article that applies almost equally to the merchant cash advance industry.

Atlas goes on to explain however, that enforcing a non-solicitation could backfire, in the sense that if the ISO feels its trivial or unwarranted, they could escalate their efforts to move deals away. They’ll probably also feel inclined to spread the word and spook the company’s other ISOs. That could really come back to bite.

Be sure to read ISO Legal Blunders by Adam Atlas on the Green Sheet.

Thinking about stealing deals? Consider the legal stuff bro.

There’s No Room for More Competition

June 2, 2015 In the next 6 months, (MANY) Broker Companies will start dying out. To the surprise of many, just when the Year of the Broker was in full bloom, chaos was forming on the horizon and the realization that there is no more room for “new” messes. Simply because we aren’t finished cleaning up and organizing the messes we have now!

In the next 6 months, (MANY) Broker Companies will start dying out. To the surprise of many, just when the Year of the Broker was in full bloom, chaos was forming on the horizon and the realization that there is no more room for “new” messes. Simply because we aren’t finished cleaning up and organizing the messes we have now!

There are basic facts that we can take from the “Broker Boom”

– Not enough beginning knowledge about this industry and how the Merchant Cash Advance process works.

– No time to make strong relationships: The concept of having “more” is usually more harmful than having a handful of trusting relationships.

– Overhead costs: the make-up costs from the spending on dead leads and the “start-up” costs of having an office, staff, draws – gave the wrong perception of what a “MCA” is when the rate mark ups pay for those expenses.

– Quick turnover when the top dog can’t fool the sales rep out of commissions any longer: Rep goes out into the world and starts their own company. This can lead to recycled bad practices or the few who want to do right.

– Co-Brokering: Everyone’s done it. I’ve done it. Edited agreements taken from other brokers/funders don’t always cover everything leading to many debacles that turn into “Jerry Springer” Forum threads. P.S. Don’t think merchants can’t see the forum either.

It’s absolutely exhausting to explain to someone from the mortgage industry or any industry that comes into the MCA space the “Rights” and “Wrongs” and the teachings. Most new Broker Company Owners and their sales come from those who don’t believe in “Best Practices” anyway.

Marketing and Leads in the Broker Space is affecting Brokers and Funders Alike – Are brokers ruining leads as well?

So, your questions about Marketing and Leads have the same answer- It does not matter what type of leads you get, it’s all about your presence, knowledge, and your “Handle”. These are the answers from actual merchants who get calls from UCCs. (This information came from old merchants that I had, I shortened the answers and stuck to the points).

- They don’t trust you because of your approach

- They tried before and was promised “X” and got a bunch of “Y” with excuses on how so many “Y’s” = “X”

- Backdoor calls- Sometimes the money isn’t the biggest savior- it’s the relationship that goes with it

- They don’t need it that bad to pay 30%. If they do need it- they want something structured to build their credit and keep their business afloat

When people think of getting money for their business- they used to think “Go to the Bank”. Professionalism, a structure that is always the same for each type of program, and knowledgeable staff they can rely on. They made the choice to come to your bank because of what is offered. Now, all but the “Capital” part is missing from this equation, but merchants still want to have that one consistent place to go to for their business needs.

I think we all lost sight of this Industry.

Brokers = Resellers and Marketers of Direct Funding programs. The Broker takes the programs from these Direct Funders and builds a portfolio of which each tier and industry and credit rating is satisfied by which funders he can qualify them to. The options are given to the merchant to satisfy their need for working capital.

You work for the Funder – Your Sales Target is the Merchant.

The Merchant has put everything into starting and maintaining their business. Most of them wanted the “American Dream” of owning a business since childhood. They have it now, and you come in and try to tell them what they need. Some believe you- some are money hungry and know the game. It’s all a numbers game no matter what kind or type of leads you buy.

All that am I saying is, the way this industry is looked at from a “Brokers” and “New-Age Funders” point of view vs. a “Veteran Broker” or “Veteran Funder” is two totally different aspects.

Unfortunately, there is no immediate solution for new “Brokers” and many solutions for the “New-Age Funders” to be on the path of “Best Practices” and less shenanigans.

There is no room for competition as we don’t know what we are competing for and rather than creating a solution so those leads can understand the growth and structure of what we are offering, we are too busy trying to find out how to get leads that won’t stick.

Small Business Lending is King to Institutional Investors

June 2, 2015

Richards Kibbe & Orbe LLP and Wharton FinTech polled more than 300 institutional investors to gauge their thoughts on marketplace lending. They published their findings in a recently released report.

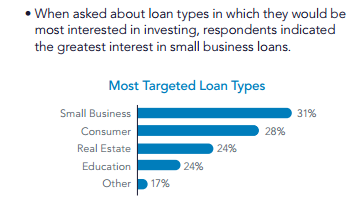

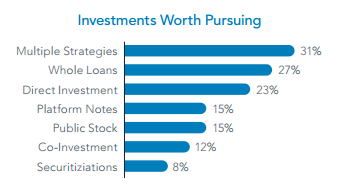

The surveyors seemed surprised that institutional investors indicated their interest in small business loans was greater than that of consumer, real estate, education, and everything else.

Securitizations ranked lowest on the list of investments worth pursuing and buying whole loans was second only to “multiple strategies.”

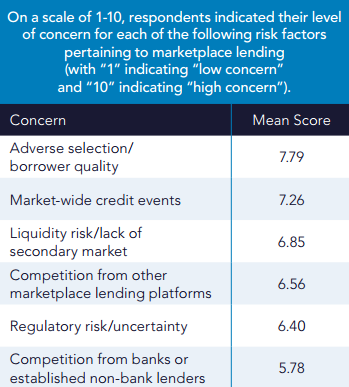

Regulatory risk and uncertainty was low on the list of concerns while borrower quality was the most concerning factor. Curiously, competition was the least concerning of all.

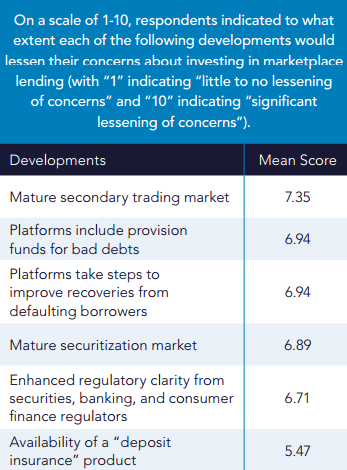

Speaking to the liquidity issues of the assets, institutional investors indicated that the development of a mature secondary trading market was more likely than anything else to lessen their concerns about marketplace lending.

Do any of these results surprise you?

Download the Key Findings report

The Broker’s Future: Are The Good Times Over?

June 1, 2015 As we continue the Year Of The Broker discussion, we must take an honest look at The Future. Due to the low barrier to entry into our space, there isn’t a week that goes by that I don’t see another recruiting ad informing the reader that all they need is a heartbeat, a UCC list, and an industry list of SIC Codes to make big money in our space. But is everything really as rosey as promoted, or if you are a new broker, should you consider investing your capital (time, energy, money and mental health) in another industry?

As we continue the Year Of The Broker discussion, we must take an honest look at The Future. Due to the low barrier to entry into our space, there isn’t a week that goes by that I don’t see another recruiting ad informing the reader that all they need is a heartbeat, a UCC list, and an industry list of SIC Codes to make big money in our space. But is everything really as rosey as promoted, or if you are a new broker, should you consider investing your capital (time, energy, money and mental health) in another industry?

The Past

To understand The Future, sometimes we have to look at The Past. Instead of a year of the broker, there was instead an actual era of the Broker, and that was from 2000 to about 2013:

(( 2000 – 2007 ))

Few firms offered a “Merchant Cash Advance” as either a direct sell or value add, and very few merchants were receiving telephone solicitations in regards to the having “working capital” other than those involved in the Equipment Leasing or A/R Factoring sectors. While the market was wide open, most merchants wouldn’t entertain an advance for 6 months with a 1.25 – 1.30 factor rate when banks were lending pretty well at much lower borrowing costs.

(( 2008 to 2013 ))

When the economy and markets took a downturn in 2008 creating The Great Recession, and banks halted most of their lending to small business applicants, the Merchant Cash Advance product was more aggressively sold by the pioneers of the industry through their Merchant Processing ISO relationships, direct selling, online advertisements, and more. The pioneers also introduced risk based pricing and premium priced products, allowing them to appeal to the higher credit graded merchants who were finally entertaining the product due to banks not lending as efficiently as previously. The pioneers also introduced multiple formats of repayment including through ACH, which allowed them to service merchants that they couldn’t tie the repayment to their merchant processing volume due to the merchant’s inability to switch or the merchant’s low monthly processing volume.

Awareness of the Merchant Cash Advance skyrocketed, hundreds of millions in equity capital began pouring in, major media outlets such as CNBC gave the product coverage, and annually the industry was funding over $1 Billion to small business applicants.

This boom period also started the trend of new lenders and brokers popping into the industry overnight using mainly the same marketing strategies such as UCC Lists, SEO, PPC, Bankcard Portfolio Marketing, and Cold Calling Various SIC Codes. These strategies worked in a decent fashion until the flood of new direct lenders and brokers coming into the industry continued, with these new entrants using mainly the same strategies. Profits were being driven down, new client acquisitions were being driven down, and because a funder’s UCC filings were being called so much, they decided to begin filing them under fake names or only filing them on riskier merchants, or never filing a UCC at all. Also most of the Online Marketing methods became too expensive, pricing the little guy out of the market.

The Future

Now we are in 2015 and new broker entrants are mainly using the exact same strategies from 2008 – 2013, discovering that UCC lists and Cold Calling SIC Codes just will not work efficiently going forward. The Future of profitability and new client acquisition in our space is going to be through Strategic Partnerships. There are three sections of your Strategic Partnerships and they are your Professional Network, Mom and Pop Network, and Online Network.

• Professional Network – The creation of a professional network from referrals such as Banks, Credit Unions, Accountants, Business Brokers, Merchant Processing ISOs, etc., to bring in a high amount of consistent leads of small business applicants who are currently seeking capital.

• Mom and Pop Network – The creation of an external independent broker channel that includes hundreds of random brokers that you sign up to resell your services. You would use the same tongue and cheek, everything is rosey, recruiting ads that I see every week just to get a rush of people on the telephone making cold calls to SIC codes, trying to compete in online marketing, or calling the remains of UCC lists, all with the dream of making a lucrative payday. The volume produced on an individualized basis will be so small it’s irrelevant, but as a collective, they will make up a major chunk of volume. This why I call these sources Mom and Pop.

• Online Network – This is your SEO, PPC, High Traffic Website Ads, and other online advertising methods. These methods will become more expensive going forward and only those with large marketing budgets will be able to truly capitalize in this area with positioning, listings, etc.

Summary

Our space is changing and new broker entrants might want to reconsider investing their capital (time, energy, money and mental health) into this venture. Only direct lenders with team members that were pioneers of this space as well as with the right networks and equity sources, are capable of truly seizing The Future. Those just now trying to come in and ride the wave will soon discover that just like with the Stock Market, the real money has already been made and most of the future returns are already capitalized. As a new broker, you more than likely will fall into that dreaded Mom and Pop category, which isn’t a good position to be in for The Future.

Mapping the Business Financing Industry (Sneak Peek)

May 27, 2015People often ask what the real presence of the merchant cash advance & business lending industry is like in New York City. Below is a map of Midtown Manhattan.

We apologize if we didn’t plot your company on here. Let us know you exist by signing up for our magazine.

In the May/June issue that’s being sent off to the printers at this very moment, we explore the industry scene in lower Manhattan. Midtown may have been a birthing place and permanent home for industry titans, but Wall Street, long believed to be a haven for stock brokers has been overrun by a new kind of broker.

You’ll just have to stay tuned to read more. If you’re not signed up to get our free print magazine, register now.

Also in the May/June issue:

- An examination of a new trend, consolidating loans and advances.

- Watching everyone else get rich off alternative lending? Whether you’re in underwriting, administration, operations, or sales and whether you have a lot of money to invest or just a little, there are opportunities available to “get in”. You might be in this industry but are you in this industry? We’ll run through the basics of what’s available out there. Become a player or just educate yourself.

- And more!

The Co-brokering Phenomenon: In Business Loans & Merchant Cash Advance

May 25, 2015 Meet the broker’s broker, the middleman serving the middleman. Some call this co-brokering since both parties will typically share in the commission.

Meet the broker’s broker, the middleman serving the middleman. Some call this co-brokering since both parties will typically share in the commission.

Wait, what?

The broker’s broker might have relationships that the little broker does not. They could have leverage over their funding partners because of the amount of volume they can produce or the amount of professionalism they bring to the table. And they likely have a canny ability to close deals that otherwise would get tossed by the wayside.

Disintermediation is the war cry of today’s famous tech-based lenders but in the Year of the Broker, reintermediation has been the unforeseen byproduct. Big lenders such as OnDeck are shedding third party funding advisors but those advisors aren’t magically going away.

A number of them are still getting their deals funded at OnDeck, just indirectly. They have to go through a broker whom OnDeck has not cut off, a handful of salespeople have told me. Many brokers acknowledge that OnDeck’s rates and terms are not easily attainable elsewhere so they’d rather share a commission with an OnDeck approved broker than risk a dead deal with no commission.

And CAN Capital is known to offer comparable pricing to OnDeck but it’s been reported that new brokers must go through a rigorous audit before CAN will accept their business. It’s not something everybody wants to go through.

With the two largest funders in the industry imposing real barriers to doing business with them, sanctioned brokers play toll booth operator for the swarm of shops that can’t get their deals submitted without them.

Perhaps as a direct result of that, there is now an entire niche of brokers whose only business is brokering deals for other brokers. They have little to no interaction with merchants. They have no marketing budget. They might not even have a website. And they play an almost mystical role of gatekeeper and power broker.

Onesy-twosy woes

A strong focus within the industry has been growth. There’s a lot of time, resources, and salesmanship that goes into courting the lucrative partnerships. Large funders, especially those with VC backing, are typically not interested in mom and pop broker shops. “If they’re only going to send one or two deals per month, we don’t want them,” I’ve heard time and time again.

Even five to ten deals a month can draw yawns. It’s nothing particularly against the mom and pop brokers, but experience has apparently shown them that the same amount of resources are spent on the onesy-twosy brokers as the ones doing a hundred deals a month. The cost benefit analysis has to make sense, they say.

That’s left hundreds or perhaps even thousands of mom and pop brokers to fend for themselves. What outsiders might not seem to realize is that the commission on a $50,000 loan or advance can be $5,000. That’s potentially enough for a stay-at-home parent to pay for the rent, groceries, and all the other bills. A onesy-twosy broker might be completely insignificant to a funder doing a billion dollars worth of deals a year, but to a mom and pop broker, it only takes one deal to pay their bills and only a handful to make them rich, especially if they live in middle America where the cost of living is cheaper.

In From Lowes to Loans, superstar broker William Ramos said he made $66,000 on just one deal alone. While his shop produces more than a million dollars in deal flow a month, it’s easy to see what’s drawing the hoards of newbies in. A $66,000 commission might be the only commission someone needs for an entire year.

There is no licensing required so becoming a broker is as easy as imagining that you are one. And as the space invites the less knowledgeable, a more sinister element has found opportunity as well.

Shady

“There is no president/ruler of the MCA world that can help you with your commission debacles,” wrote PSC’s Amanda Kingsley on an industry forum. That was part of her reply to a thread titled, co-brokering scumbags. The thread might be new, but the circumstances aren’t. A broker sent their deal to another broker who got the deal closed with a funder. The original broker supposedly got screwed out of the commission.

“There is no president/ruler of the MCA world that can help you with your commission debacles,” wrote PSC’s Amanda Kingsley on an industry forum. That was part of her reply to a thread titled, co-brokering scumbags. The thread might be new, but the circumstances aren’t. A broker sent their deal to another broker who got the deal closed with a funder. The original broker supposedly got screwed out of the commission.

It’s a case of stolen deals. “You just have to find the right people to work with. There are a lot of shady characters in this industry,” wrote another user.

1st Capital Loans Managing Member John Tucker, who recently authored, Broker Business Planning, wrote in reply to the thread, “Get everything in writing and research your lender/partner heavily before contracting with them. Talk to other brokers and ask them about their experience with said lender/partner in terms of paying on new deals, renewals and residuals. Get a ‘feel’ for them.”

Several faulted the aggrieved party for not taking the time to hammer out a contract that would allow them to rectify the situation easily through a lawsuit. But even with a contract, pursuing the offender legally could cost more than the commission lost. A stolen deal might cost a broker a few hundred or a few thousand dollars, figures worthy of small claims court.

“Under no circumstances would I ever co-broker a deal,” wrote Tucker. “There’s just no reason to unless you are a newbie and getting trained by said broker.”

But another user wrote, “Sometimes you don’t even know you are co-brokering until after the fact.”

Unscrupulous brokers will be purposely deceitful but for others walking the thin line between broker and funder, it’s difficult to judge what constitutes direct. There are brokers that wholeheartedly believe that if any portion of their own funds are invested in a deal, then they too are a direct funder. That means a broker that syndicates with a variety of funders could be so inclined to identify themselves as a direct funder by extension.

Kingsley wrote, “You have to understand what a ‘broker’ is in this space and understand that it is A LOT different than brokering in another industry.”

She also pointed out that it’s not always the little guy that’s susceptible to becoming a victim, as could be the case if an early deal default leads to a commission chargeback. When that happens, the funder will take back the full commission on the deal from the broker of record. It’s the responsibility of that broker to claw back whatever split of the commission they shared with the sub-broker.

“The broker you sub-brokered for, can vanish,” Kingsley wrote.

Ban the bad guys?

Several industry veterans have suggested creating an ISO/funder blacklist for those that steal commissions or deals. The challenge is that a stolen deal is not always a black and white situation. Often times there are expiration dates built into contracts that allow funders to claim deals if they have not been closed by the submitting broker within a specified period of time. Other times it’s a case of miscommunication, or the victim conveniently left out key details that would certainly add a degree of color to the situation.

Calling out an offender online can quickly devolve into a he said/she said schoolyard brawl. Unfortunately, this might be the only remedy a victim has, especially if they have limited financial resources to pursue legally, or the only evidence of their deal is a handshake or an email.

The bad guys, if they’re engaged in trickery on a large scale, tend to get identified rather quickly. There’s always a few that come in, burn a lot of bridges, and then find themselves completely ostracized from the industry. When the damage is done, they might never be heard from again or they might try to repeat the process by using a different name. Blacklisting a broker or funder wouldn’t be foolproof, especially if the company owner legally changes their name, which has actually happened before.

Trust

Through it all, Tucker offered this advice, “In a nutshell, the only true thing protecting your compensation is a very good relationship with an honest, credible and ethical lender.”

And if you have to go through a broker, make sure you choose the right one. Don’t blindly send your deal to somebody you met on a message board. An unscrupulous player will tell you exactly what you want to hear. Ask around for references. If nobody’s ever heard of them, chances are you’re talking to the wrong shop.

Even the author of that thread conceded that co-brokering offers benefits. “I’m all for co-brokering deals, especially if someone has a solution that may suit the client better than a traditional MCA or when an MCA wont work,” he wrote.

So there just may be a place for the broker’s broker, whether as a gatekeeper, power broker, or toll booth operator. And like it or not, reintermediation has ironically become a byproduct of disintermediation. There are sadly no algorithms that exist to vet how a broker might treat another broker. Co-brokering is a trade that relies on the most basic of basics, trust.

Nothing’s more valuable.