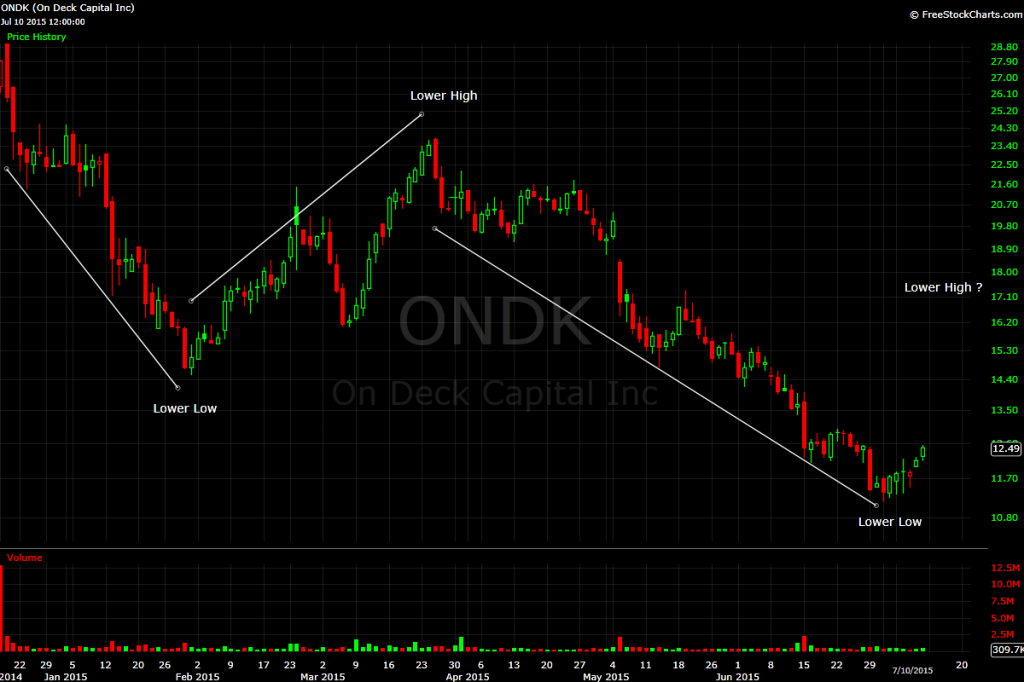

An OnDeck (ONDK) Technical Analysis

July 12, 2015For some of us working in the merchant cash advance industry, we saw the IPO of OnDeck (ONDK) as a major stepping stone in getting recognized by main street and receiving overall exposure. Unfortunately it has not been the best representative of us in the stock market. I started monitoring ONDK on the first day it started to trade and after 7 months, it clearly hasn’t looked positive.

I am a student in technical analysis. In layman’s terms, it is the study of price action of a traded financial instrument to make an informed investment decision. The following is my view.

The first thing that pops out when viewing the chart is that the single biggest day of volume (number of shares traded) was the IPO day. The stock has yet to trade in that kind of volume since then.

The other obvious thing that pops out is that the stock has been in downtrend, a series of lower lows and lower highs. As the old Wall Street adage says, “The trend is your friend.” Trying to call a bottom in this stock has been useless as it seems like those that have, are catching a falling knife.

Moving averages are used to determine whether the stock is trending or not. With very few trading days the longer term averages are not able to be rendered. In May the stock met resistance at the 20/50 EMA crossover. Coincidentally this was also the beginning of the latest down leg. It is also worth noting that the stock has not closed above the 20 day EMA since it was breached. There was one failed attempt that resulted in the continuation of the down trend in the middle of May. The stock is currently at the 20 EMA and is testing this level again. A close above this could be an indication of a possible change in trend.

The bottom of the chart has the RSI. This is a measurement of Overbought and Oversold conditions, which is telling us that the stock has been oversold for a couple of months. It recently started moving upward from the oversold condition.

The MACD is another technical indicator used. It measures the momentum of the stock. I like to think of momentum as the thrust/force of the move in a stock. This indicator points two things to me. As the stock has been going lower there hasn’t been a lower low in the indicator. It actually seems there is a slight uptrend in the indicator, which tells me as the stock has gone lower, there hasn’t been the same force/thrust to the move. This is a classic example of divergence, meaning the stock is doing one thing while the momentum indicator is doing another.

The information above points to two possibilities. The first is that the stock is currently taking a breather from its downtrend. This is normal in a stock cycle; after all, stocks do not go up or down in straight lines. The other is that the stock could be in the beginning stages of stabilizing. Stabilizing does not mean that the stock will begin a new uptrend. It means the stock could be range bound for a couple of months.

A Decade of Funding

July 7, 2015Next month is my 9 year anniversary in the merchant cash advance industry, which means I’ll be starting my 10th year. A decade of merchant cash advance… holy shit. I’ve had the opportunity to view it from many different angles and have accrued my fair share of adventures, plenty of which I’ve written about and others I’ll have to take to my grave.

I also launched this very website exactly 5-years ago under its original name MerchantProcessingResource.com. Not many people can say they’ve authored more than 600 stories (yes, seriously) on merchant cash advance, but I can. I’m fortunate to have turned something I merely enjoyed in the beginning into a business of its own.

I also launched this very website exactly 5-years ago under its original name MerchantProcessingResource.com. Not many people can say they’ve authored more than 600 stories (yes, seriously) on merchant cash advance, but I can. I’m fortunate to have turned something I merely enjoyed in the beginning into a business of its own.

Looking back now, there weren’t many people keeping a live diary of events as the industry dove headfirst into the financial crisis. Who would’ve bothered to report on an industry that was arguably made up of only a thousand people?

In April 2009, even before deBanked launched, I submitted a story to the only merchant cash advance magazine of its kind. It didn’t have a very clever name, just Merchant Cash Advance Publication. My story, titled, An Underwriter in Salesman’s Clothing, rambled on about the end of the industry’s glory days, the wave of declined deals in the recession, and how funders should be more appreciative of ISOs.

Here’s a summary of what I wrote more than six years ago:

Here’s a summary of what I wrote more than six years ago:

I was complaining about stacking as far back as 2007 apparently. I addressed it as a merchant problem. Merchants were taking advantage of funders, not the other way around like some frame the argument in 2015.

I left my post as Director of Underwriting in late 2008 because “I wanted the ringing phones, the commotion, the markerboards with stats, the glory, the $20,000 [monthly] checks.”

Funding companies became super conservative during the financial crisis and all my deals were being killed (25 deals declined in a row at one point.)

I had recently charged my first closing fee, felt bad about it, and got in trouble for it.

I said 1.40 factor rates wouldn’t last (I was wrong about this!)

I bitched about algorithmic declines (I apparently thought computers underwriting files was a good way to upset ISOs.)

I acknowledged my own hypocrisy when I realized how hard it was to be a sales rep after thinking sales reps were overpaid and overrated in my previous years as an underwriter.

I continued on as a sales rep for another two and a half years after I wrote that. That means that in 2010 when I started deBanked, I was still calling UCCs, closing deals and boarding merchant accounts while sitting in a windowless room rented by a startup ISO.

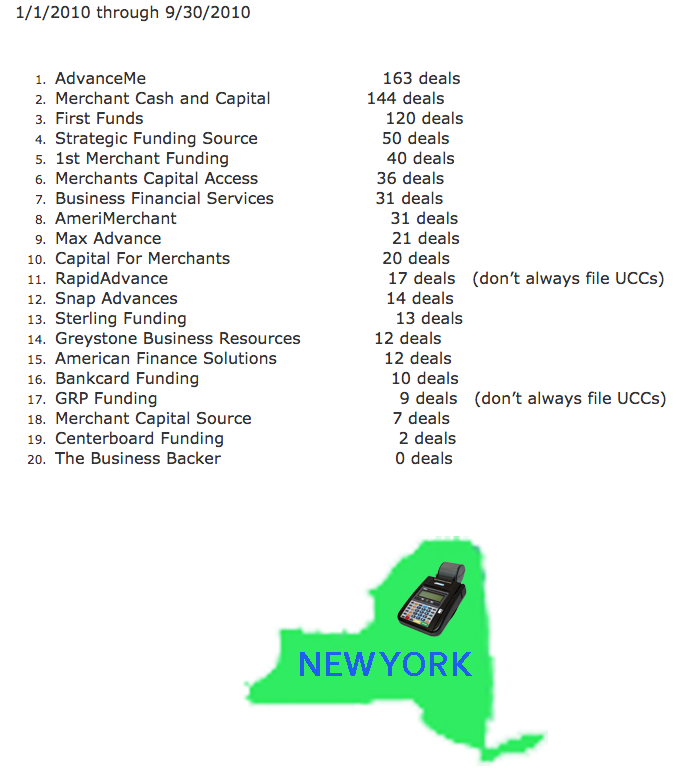

But what was there to blog about in 2010? Oh little stuff like who the biggest funding companies were at the time by checking UCC filings since almost everyone filed UCCs back then. Notably, the third largest merchant cash advance company of 2010, First Funds, is no longer in business.

I also wrote about shopping deals around and the impact that might have on a merchant’s credit report. That was the day-to-day stuff though, information I was just putting out there hoping someone on the Internet might see it. What got everyone excited was the 2010 New York State leaderboard which eventually prompted me to spend my nights and weekends investigating the industry on a wider level.

I began talking to people at other funding companies about their monthly numbers. It wasn’t that hard to get information as an industry insider, especially if you had deals to send somebody’s way. I also spent money to acquire secured party lists to count the number of UCC filings by funders in all 50 states rather than just look at one free state like I did with New York originally. I think I was the only person in the industry at the time running up their personal credit card bill to conduct such research. I had also been in the industry for four years at that point and had a great network of contacts who could clue me in on their volume.

While I said that I also looked at census records and department of labor records, I’ll admit that data wasn’t extremely useful. The end result was a best guess estimate that in 2010, there were approximately 21,000 merchant cash advances transacted for $524 million.

My data would go on to be republished in ISO&Agent Magazine, The Scotsman Guide, and Leasing News, and also end up in many other places I didn’t expect, like in the business plans of merchant cash advance companies that were looking to raise capital. In fact, in a private meeting I had with an MCA company months later in South Florida, the CEO let me take a peek at the docs they had just submitted to a bank for a credit facility. Included was a printout of these numbers with my name on it and all. Apparently there was something to this writing thing…

My last day as a sales rep was in the Fall of 2011. I left the commission-only life (oh what, you 2015 pansy closers actually get a base salary?) for something even more risky, an entrepreneurial life. For a couple years, I played underwriting consultant to a handful of merchant cash advance companies and industry expert to institutional investors interested in the space. I learned how to code in my spare time and spent more than a year in online lead generation.

I never stopped writing.

Along the way I’ve visited the offices of dozens of ISOs and funders, syndicated in deals, and test-drove new technology.

None of this makes me particularly special, especially when I hear about how much some of my old sales buddies are making these days on deals. “Are you SURE you don’t want to come back?” they ask. It’s enticing no doubt. A part of me wants to grab the phone out of their hand and attempt to shatter their record on the markerboard this month even though I’m pretty sure I’m rusty as hell.

One thing noticeable between now and 9-years ago is that my hair turned grey. This industry will do that to you (or at least it did to me.) And I still get a kick out of meeting folks who got into the industry years before I did. The 90s/early 2000s AdvanceMe crowd likes to tell me that they were funding merchants while I was still in diapers. They are practically right.

As I enter my own tenth year in the biz however, it’s exciting to think that the industry is just now getting started. OnDeck was the first IPO in the space and the general public is learning about short term business funding for the first time. There’s no shortage of news to report and that keeps me plenty busy these days.

And so even after a decade of MCA, it’s never too late to put on your Funded pants. Opportunity awaits and I hope you’ll continue to ride the wave with me. Thanks for reading since 2010!

OnDeck Q2 Earnings Announcement

July 6, 2015Update: The news reports that said OnDeck was reporting earnings today on July 6th were false

An OnDeck representative said they have not yet scheduled a date.

OnDeck (ONDK) was reportedly going to release 2015’s Q2 earnings after the market closed on Monday, July 6th (That information was confirmed as false.) Analysts predict the company will show a loss of 7 cents a share.

OnDeck (ONDK) was reportedly going to release 2015’s Q2 earnings after the market closed on Monday, July 6th (That information was confirmed as false.) Analysts predict the company will show a loss of 7 cents a share.

The company has faced a fierce sell-off in recent weeks, moving the stock to all time lows and down more than 50% from its high. The trend began after the Q1 report in which company executives argued that a decrease in the interest rates charged to their customers was not a response to competitive pressure.

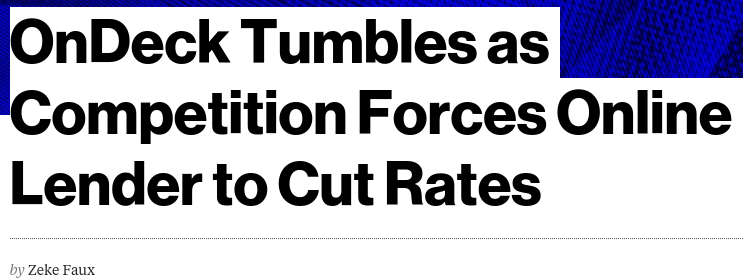

Bloomberg’s Zeke Faux ran the following headline anyway:

Since then, the stock has struggled to recover. I posted a summary of why that might be on June 29th, in a short piece tiled, What Happened to OnDeck.

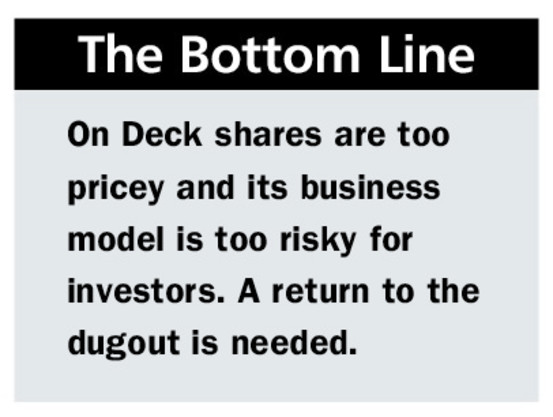

Barron’s was particularly tough on them, labeling them a subprime lender in dot-com clothing. For now, the key to an OnDeck rebounds seems to be about shedding that toxic label and convincing investors that despite a crowded field, they are the clear standout choice.

An increase in the default rate this quarter however would probably evoke a further negative response.

Are You Robodialing? The TCPA and FCC Scoop You Need to Know

July 2, 2015 In 1991, when Congress began regulating autodialers via the Telephone Consumer Protection Act, our phones and our relationships with them were vastly different from what that equipment and those relationships look like today. At that time, Congress was regulating a world without text messages and ubiquitous cell phones and a world where autodialers were infuriating consumers nationwide for their ability to generate and dial telephone numbers indiscriminately without regard for who was on the receiving end of the call.

In 1991, when Congress began regulating autodialers via the Telephone Consumer Protection Act, our phones and our relationships with them were vastly different from what that equipment and those relationships look like today. At that time, Congress was regulating a world without text messages and ubiquitous cell phones and a world where autodialers were infuriating consumers nationwide for their ability to generate and dial telephone numbers indiscriminately without regard for who was on the receiving end of the call.

In the intervening years, Congress has made modest TCPA amendments to address unsolicited faxes and nefarious manipulation of caller ID information, but it has otherwise failed to adjust the law to reflect the way we communicate today. The FCC has tried harder than Congress to update its TCPA rules, but it too has failed in this regard. The result is a set of obsolete standards whose significance vastly outpaces their sense due to the TCPA’s private right of action and rigid statutory damages calculation. Companies hoping the FCC would pivot toward sanity in its recent announcement of TCPA guidance are surely disappointed today.

The TCPA has always defined a regulated “autodialer” as equipment with the capacity to store or produce telephone numbers to be called using a random or sequential number generator and to dial such numbers. The FCC’s TCPA rules retain that formal definition, but the FCC has explained that predictive dialers and other equipment enhancing dialing efficiency are also regulated as autodialers because of their capacity to dial numbers without human intervention. The FCC has repeatedly confirmed that the focus of the “autodialer” standard is on the equipment’s capacity, not its actual use.

A number of courts have tried to make this “capacity” standard more concrete by limiting it to the equipment’s present capacity, that is, what the equipment was capable of doing when the calls at issue were replaced, without considering what the equipment could be reconfigured to do at some future time. These courts explained that a focus on present capacity was necessary to ensure that every person’s smartphone would not be regulated as an autodialer based on what it could be reprogrammed to do.

The FCC received a number of petitions seeking more formal, universal guidance on the TCPA’s “autodialer” standard. We are still waiting for the FCC to publish the guidance it has approved, but according to the FCC’s June 18, open meeting, that guidance will not make this issue any clearer. According to the FCC’s preview, that guidance will affirm that the TCPA’s “autodialer” standard focuses on the equipment’s capacity, ensuring that “robocallers cannot skirt consumer consent requirements through changes in calling technology design or by calling from a list of numbers.” If this is an accurate summary of the FCC’s guidance, it will do absolutely nothing to resolve the most pressing concerns on this issue. It will not address whether “click-to-dial” technology, which involves some human intervention but may have the capacity to operate without it, is regulated as an “autodialer.” It will not address whether the definition’s “capacity” element is limited to present capacity or also includes possible future capacity. The surge in private TCPA litigation makes these ambiguities treacherous.

The FCC received a number of petitions seeking more formal, universal guidance on the TCPA’s “autodialer” standard. We are still waiting for the FCC to publish the guidance it has approved, but according to the FCC’s June 18, open meeting, that guidance will not make this issue any clearer. According to the FCC’s preview, that guidance will affirm that the TCPA’s “autodialer” standard focuses on the equipment’s capacity, ensuring that “robocallers cannot skirt consumer consent requirements through changes in calling technology design or by calling from a list of numbers.” If this is an accurate summary of the FCC’s guidance, it will do absolutely nothing to resolve the most pressing concerns on this issue. It will not address whether “click-to-dial” technology, which involves some human intervention but may have the capacity to operate without it, is regulated as an “autodialer.” It will not address whether the definition’s “capacity” element is limited to present capacity or also includes possible future capacity. The surge in private TCPA litigation makes these ambiguities treacherous.

Although the FCC discussion of its TCPA guidance touts the protections provided to consumers, the autodialer provisions apply equally to business-to-business calling. MCA companies must be aware of the TCPA’s autodialer requirements for B2B calling campaigns. They can be sued for improper calls placed to businesses, as well as errant B2B calls that are answered by individual consumers. The FCC’s TCPA rules establish that callers must have the call recipient’s “prior express written consent” for sales calls placed to cell phones using an autodialer or a prerecorded message. This form of consent requires a signed writing from the call recipient and requires certain “magic words” disclosures that must be provided when the consent is obtained. This consent requirement applies to B2B calls as well as B2C calls, and the existence of an established business relationship between the parties to the call does not provide any relief from this requirement. Non-sales calls to cell phones using an autodialer or a prerecorded message require “prior express consent.” This term is not defined, but the FCC has explained that a call recipient provides valid consent to a creditor by volunteering his or her cell phone number to the creditor, such as on a credit application. There are tricky details in this standard, so MCA companies should proceed with caution in order to establish valid TCPA consent.

Technology makes our lives easier, but it makes our TCPA compliance analysis more complicated. The TCPA should not impede technological developments that do no harm, but the law’s enforcement scheme encourages “professional plaintiffs” and greatly increases the likelihood that a TCPA violation will result in a lawsuit. The FCC is presently fumbling an opportunity to address this. It’s unclear when another such opportunity will arise or what it will take for the FCC to decide to align its TCPA rules with the real world.

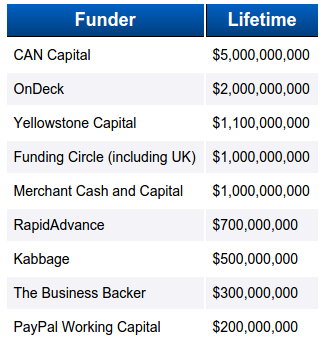

The Rest of the Alternative Lending Industry’s Funding Numbers

July 1, 2015 Let’s be serious, the industry’s much bigger than we may have let on when we published the industry leaderboard (some mods have been made) in the May/June issue.

Let’s be serious, the industry’s much bigger than we may have let on when we published the industry leaderboard (some mods have been made) in the May/June issue.

Right after deBanked sent the final file off to the printers in May, PayPal announced that the widely circulated $200 million lifetime funding figures were slightly outdated.

How off were they?

Oh, just by about $300 million or so. By May 7th, PayPal’s Working Capital program for small businesses had already exceeded $500 million. The industry leaderboard has been revised to reflect the news. PayPal says they are funding loans at the rate of $2 million per day, which puts them on pace for more than $700 million a year. Um, wow?

One name that’s missing from that list is Amazon, whose secretive short term business loan program is reported to have already generated hundreds of millions of dollars in loans. Given the $300 million discrepancy that PayPal let ruminate for months, we’re in no position to speculate on Amazon. Anyone could try to assess what they’ve been up to however, since they file UCCs on their clients under the secured party name “AMAZON CAPITAL SERVICES, INC.”

Of course if you’re craving specific numbers, an anonymous source inside Yellowstone Capital revealed that Yellowstone produced $35.5 Million worth of deals in the month of June alone. Yellowstone has a strategically diverse business model that allows them to either fund small businesses in-house (essentially on their own balance sheet) or broker them out to other funders. Yellowstone was listed on deBanked’s May/June industry leaderboard at $1.1 Billion in lifetime deals and $290 Million in 2014. June’s figures indicate that they are probably well on their way to surpassing last year’s numbers.

Curiously, platform/lender/broker/marketplace company Biz2Credit has been hanging on to the same stodgy old number for more than a year.

Funded over $1.2 billion. 200,000+ happy customers.http://t.co/3h64lI4cgG #smallbusiness #Funding

— Biz2Credit (@biz2credit) June 19, 2015

They were touting that same $1.2 Billion number exactly 1 year ago. Surely they have done more since then? Biz2Credit’s service covers a much wider scope however so a direct comparison with their peers may not be appropriate. A lot of their loans are arranged through traditional banks which are typically transacted in amounts larger than the average $25,000 deal alternative lenders do.

A source familiar with Biz2Credit’s breadth said he observed a deal where the company helped a businessman in Mexico obtain financing to purchase a new helicopter, a transaction which apparently necessitated a team to fly down there to sign paperwork. Definitely not a standard transaction!

When we published the industry leaderboard initially, it admittedly omitted some of the industry’s largest players. Many firms are fairly secretive about the numbers they release and we’re in no position to disclose numbers that aren’t supposed to be public. Below is data that we hadn’t published previously.

The industry’s unsung behemoths

The industry’s unsung behemoths

The $300 million lifetime funding figure publicized by NYC-based Fora Financial can’t be that stale. It’s the number currently stated on their website and a late February 2015 company announcement revealed they were only at $295 million at the time. We feel comfortable enough to now have Fora Financial on the leaderboard.

In 2014, Delaware-based Swift Capital revealed that they had funded more than $500 million. It’s unclear how much that’s increased since then.

Credibly (formerly RetailCapital), has publicized that they’ve funded more than $140 million in their lifetime. Founded in Michigan, the company has opened offices in New York, Arizona, and Massachusetts. They’ve been added to the lifetime leaderboard.

New York City-based AmeriMerchant has a claim on their website that they have funded more than $500 million since inception. How much more exactly? We’re not sure.

Coral Springs, FL-based Business Financial Services keeps their figures mostly under wraps but a good guess would place their lifetime figures at somewhere between $700 million and $1.2 billion.

Miami, FL-based 1st Merchant Funding had reportedly funded close to $100 million in the Spring of 2014. It’s uncertain as to where they might be now.

Woodland Hills, CA-based ForwardLine surpassed $250 million in funding as far back as 2013.

Orange, CA-based Quick Bridge Funding disclosed more than $200 million in funding in late 2014.

Troy, MI-based Capital For Merchants has funded $220 million since inception. But there’s more to the story. Capital For Merchants is owned by North American Bancard, a merchant processing firm that acquired another merchant cash advance company, Miami, FL-based Rapid Capital Funding in late 2014. And coincidentally, Rapid Capital Funding had just acquired American Finance Solutions months earlier, which is an Anaheim, CA-based merchant cash advance company that had funded more than $250 million since inception. All told, North American Bancard owns at least three merchant cash advance companies: Capital For Merchants ($220 million), American Finance Solutions ($250 million+), and Rapid Capital Funding (undisclosed). There are rumors that they’re in talks to acquire at least one more company in the space, which, if true, would make North American Bancard one of the industry’s most powerful players.

Don’t bother counting up the above totals

These figures all barely scratch the surface as deBanked’s database indicates there are literally hundreds of genuine direct funders in the industry.

Thanks to the company representatives that took the time to confirm their funding numbers with us directly. Anyone interested in sharing their figures can email sean@debanked.com. If there is a gross inaccuracy somewhere as well, please report it to us.

This page might be updated in the future so check back!

Tech-based Lenders Clobbered On Dose of Bad Economic News

June 29, 2015How would tech-based lenders fare in a slumping market? Not very well apparently…

OnDeck (ONDK) and Lending Club (LC) set new record lows earlier today amid bad news coming out of Greece and Puerto Rico. OnDeck is down almost 43% from its IPO price and down 61% from its all time high. It was down more than 8% today even though the Dow was only down 2%.

$ONDK was unaware that it focused on Greek loans…. interesting 8.6% drop.

— Mark Holder (@StoneFoxCapital) Jun. 29 at 05:48 PM

The downward trend was dissected in a post that was published just hours before today’s further fall.

Meanwhile Lending Club is in new territory, down 3% from its IPO price and down 50% from its high. So what are investors saying about this?

$LC hmm i really dunno what to say about this…

— mike pham (@mincogneto) Jun. 29 at 05:30 PM

That’s kind of the overall gut feeling. Many feel this company is being unfairly dragged down and yet it continues to fall. A mounting campaign by the Puerto Rican government to declare bankruptcy and a Greek debt disaster clobbered everything today including Lending Club. One tweeter came up with a great idea last week, bail out Greece with a loan from Lending Club…

If all else fails with the IMF #Greece should just apply on @LendingClub pic.twitter.com/RbtnMm5JaO

— World First USA (@WorldFirstUS) June 22, 2015

Last week no one was even talking about Puerto Rico. Now all of the sudden they’re in a “death spiral.”

Watch the death spiral coverage on CNN

The market’s tech lending darlings might’ve gotten pummeled like everyone else but the ease with which they drop should probably be a warning sign. Neither offshore dilemma stands to have any impact on their businesses. So what would happen if a relevant issue were to arise such as a domestic disaster, a sudden rise in unemployment, a recession, a financial crisis, skyrocketing fuel prices, a steep increase in the fed funds rate, or even something no one dares talk about like a legal ruling that could jeopardize the entire bank charter model?

It’s quite possible that both companies haven’t bottomed out just yet….

——–

Note: I have no equity positions in either company. I do own Lending Club notes however.

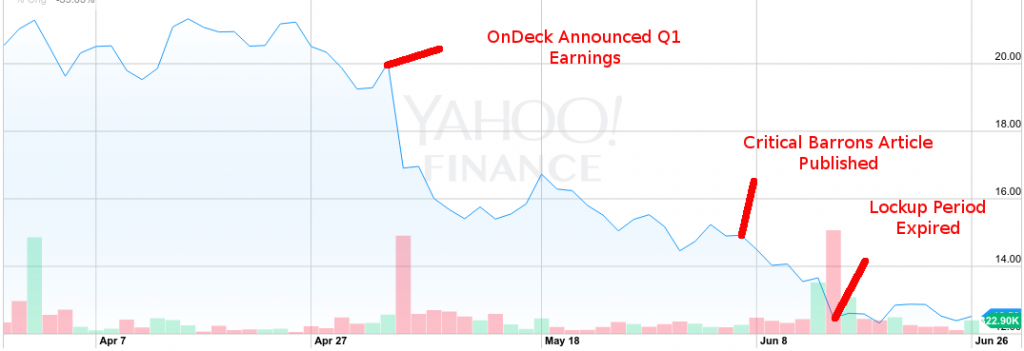

What Happened to OnDeck? (ONDK)

June 29, 2015The lockup expiration came and went but the fall of OnDeck’s stock price started much before that. There were no insider stock sales reported to the SEC since shares became unrestricted anyway.

There’s very little trading volume on an average day and investors on the big message boards either ignore this stock or don’t understand it.

The trend started on May 4th when they released Q1 earnings. The direction wasn’t very much different than Q4. Loan volume went up, interest rates came down, and no profits were to be had, nor were any expected for the rest of the year.

The market interpreted decreasing interest rates as pressure from competitive forces however and down went the stock price.

OnDeck’s execs insisted that they had lowered rates as part of a deliberate strategy to create stickier customers and attract new borrowers. CEO Noah Breslow himself said during the previous 2014 Q4 earnings call that “there’s so much search cost associated with going out and looking at other places and so much uncertainty around that, they [small businesses] typically just take that offer that OnDeck has provided to them.”

His theory is supported by the results of Lending Tree’s recent survey that revealed nearly 60% of small businesses did not comparison shop business loans online during their loan application process.

It’s possible though that the drop had little to do with OnDeck’s actual performance. That same day, Goldman Sachs hinted that they would be joining the tech-based lending field when they announced the hire of Harit Talwar from Discover Financial Services.

But before they had a chance to recover, Barrons published a story that was highly critical of OnDeck just a month later on June 5th. “It’s a subprime lender in dot-com clothing,” the author wrote. It was a tough characterization for them to refute, what with their 50% interest rates and double digit percentage charge-offs and all.

And then the lockup expiration on June 15th coincided with the big reveal of Goldman’s intentions to compete in the marketplace. News sources that picked up the story predicted that the move would impact online lenders like Lending Club and OnDeck. OnDeck’s stock hit a record low that day.

OnDeck has been stuck in the 12s ever since. Can they dig themselves out?

If competition is a factor in the market’s perception, and it probably should be, then investors should keep an eye on the industry’s other top players. OnDeck is not alone in this space and Goldman Sachs will be in for a bigger fight than they probably expect.

Source: deBanked’s May/June Magazine issue

The CFPB is Pretty Busy With Actual Consumers

June 28, 2015 It’s often theorized by industry insiders that the Consumer Financial Protection Bureau (CFPB) will play a role in business to business transactions. But when you actually talk to those employed by the government agency, it seems very unlikely. The CFPB is already very busy playing the role of Better Business Bureau, albeit a nationalized version.

It’s often theorized by industry insiders that the Consumer Financial Protection Bureau (CFPB) will play a role in business to business transactions. But when you actually talk to those employed by the government agency, it seems very unlikely. The CFPB is already very busy playing the role of Better Business Bureau, albeit a nationalized version.

There is currently no categorical option to report business loan or merchant cash advances on their website and the complaints lodged by consumers pertain to very basic consumer problems, such as issues with their credit cards or student loans.

Here’s an example of a CFPB complaint:

2009 XXXX XXXX, XXXX XXXX Thursday of every month I got pulled from class to get a new loan for my living and tuition expenses. I was at XXXX for one year and if I didn’t go to sign the papers for my new loan every month I wouldn’t be able to continue my classes to XXXX. I missed out on important class information and had to make them up on my own time. Homework and other hands on tasks became more difficult to accomplish if I didn’t make up the lost time going to sign loan papers. I was told a rough amount that my school loan would be. About {$15000.00}. I started paying {$120.00} a month for my loan agreement then Genesis Lending increased it to {$190.00}. I called to ask why the increase in payment amount each month. I was told they saw i had a higher income so they adjusted the payment accordingly. Is that legal? I’ve been paying this amount for 6 years and still owe {$13000.00}. I called Genesis Lending and come to find out they have been rolling over all the interest I pay on the loan every year. So all I’m paying is interest basically for the last 6 years. I don’t think I ‘m being treated fairly or legally.

Many complaints are just like this, where consumers are not actually reporting illegal activity but instead using the CFPB to vent their frustration. In this situation, the victim was busy with homework and wasn’t sure how their student loan worked so they filed a complaint with the federal government…

The end result was that the lender responded by saying it wasn’t really their problem, the borrower didn’t dispute this response and the CFPB marked the case as closed. Seems like a great use of everybody’s time.

In the handful of presentations I’ve attended by the CFPB, they said they often find themselves redirecting complaints to the business that the consumer is complaining about much like the BBB would do.